Global Small-Cap Value Investor | Toss Securities Korea Influencer · 8k | Owner mindset | Fundamentals only | Patience is my edge

Joined November 2025

- Tweets 172

- Following 288

- Followers 168

- Likes 257

44 Photos and videos

Pinned Tweet

16 Nov 2025

I invest as the owner.

I trust the company, I wait, I win.

I focus on fundamentals, not noise.

Long-term value investor.

First entries:

$NVDA 29.9 | $PLTR 15.64 | $IONQ 10.63 | $RGTI 2.3 | $QBTS 2.66 | $SOUN 2.74 | $OKLO 27.91 | $OPEN 1.06 | $ONDS 2.07 | $BE 24.15 | $UBER 38.43

Current core:

$BITF $IREN $NBIS $EOSE $CLSK $CAN $ASTS $CLS $SOUN

I analyze:

Leadership | Company DNA | Execution | Growth potential

(Not financial advice. Personal view.)

Stocks = ownership.

Patience = profit.

5

3

17

1,916

2026년 상반기 로봇 산업 주요 공식 일정

1월 27일: 테슬라(Tesla) 컨퍼런스 콜 및 주주 총회 (옵티머스 Gen 3 양산 현황 발표)

1분기 내: 현대차 모베드(MobED) 베이직 및 프로 모델 양산/고객 판매 개시

1분기 내: 테슬라 옵티머스 3세대(Gen 3) 본격 양산 시작 (일론 머스크 발표 기준)

2월 ~ 3월: 테슬라 옵티머스 3세대(Gen 3) 공식 세부 사양 발표 예정

3월 16일 ~ 19일: NVIDIA GTC 2026 (로봇 파운데이션 모델 GR00T 업데이트 발표)

3월 ~ 4월 전후: 미국 정부 로봇 관련 행정 명령 발표 예상 (미국 내 생산 보조금 지원 골자)

4월 중순: 유니트리(Unitree) 차세대 모델 H2 초도 물량 고객 인도 시작

5월 25일 ~ 27일: Robotics Summit & Expo (보스턴, 휴머노이드 실전 배치 공정 발표)

6월 1일 ~ 5일: ICRA 2026 (비엔나, 세계 최대 로봇 학회 기술 발표)

6월 이후: 유니트리 등 중국 주요 로봇 기업 IPO(기업공개) 및 대량 양산 이슈 본격화

4

353

23 Dec 2025

2026년 상반기는 미증시와 코인 모두 많이 힘들어보인다...

차라리 기간동안에 국장을 집중해서 투자를 하는게 낫지 않을까..

1

210

21 Dec 2025

미국 시장은 좋은 소형 유니콘 성장주가 정말 많다.

2026년에는 종목을 줄이고 선택과 집중을 하려고 하는데, 공부할수록 좋아 보이는 종목이 너무 많아서 포트폴리오 설정이 정말 어렵네...

2

6

233

9 Dec 2025

종목을 믿고 장기투자를 하려면 힘빼고 투자 해야한다.

매일 매일 호가창을 보며, 퍼드 뉴스에 흔들리면, 장기투자는 불가하다.

본인 경험상 대부분의 대박 종목은, 3년에서 5년 이후의 큰 수익으로 돌아왔다.

4

194

8 Dec 2025

2026 ~ 2028년

엄청난 AI 버블 장세가 되지 않을까?

8 Dec 2025

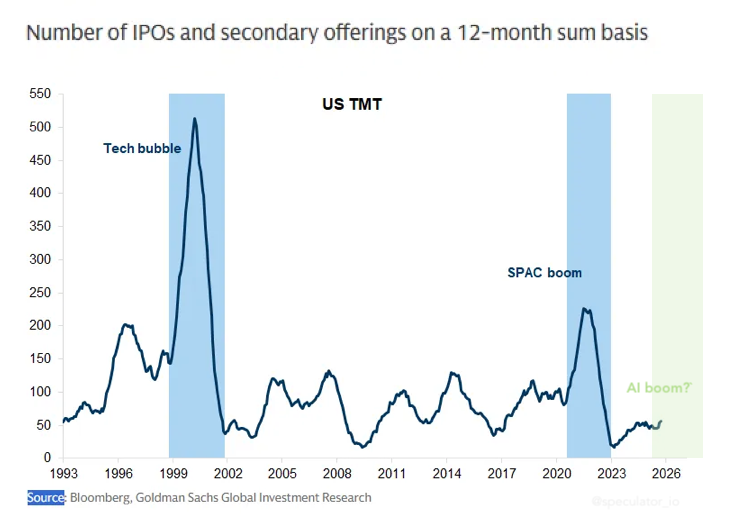

We haven’t seen any notable IPOs since 2021.

It’s been so long that most people forgot how crazy it gets when IPOs finally start coming back.

3

267

30 Nov 2025

$CLSK CleanSpark: From Bitcoin Miner to Next-Gen AI Data Center Powerhouse

• Already has 450 MW of power → 50 GW pipeline in progress

• Pivoting fast into AI/HPC data centers while BTC mining pays the bills

• One of the only players with owned power land ready for hyperscale AI

• Current price reflects ZERO of the AI upside

• Still trading like “just a miner” while building tomorrow’s AI infrastructure

Massive mispricing. 10x potential as the AI pivot story catches fire.

#CLSK #Bitcoin #AI #DataCenter $iren $bitf $crwv $nbis $cifr $wulf

1

2

371

30 Nov 2025

Crypto-linked stocks absolutely dominated this holiday-shortened week as Bitcoin bounced hard.

Top performers over the past 5 trading days (as of Nov 28 close):

$CLSK 54%

$CIFR 40% (JPM upgrade alongside $CLSK)

$WULF 34%

$BITF 34%

$HUT 33%

Only laggards in the broader financial sector:

$ABTC −7.4%

$RLI −3.8%

$PRI −1.6%

$FRHC −1%

$UNM −0.4%

When Bitcoin runs, the miners run even harder. Classic risk-on week.

#Bitcoin #CryptoStocks #CLSK #Miners

2

292

GambleToValue_도박중독 retweeted

28 Nov 2025

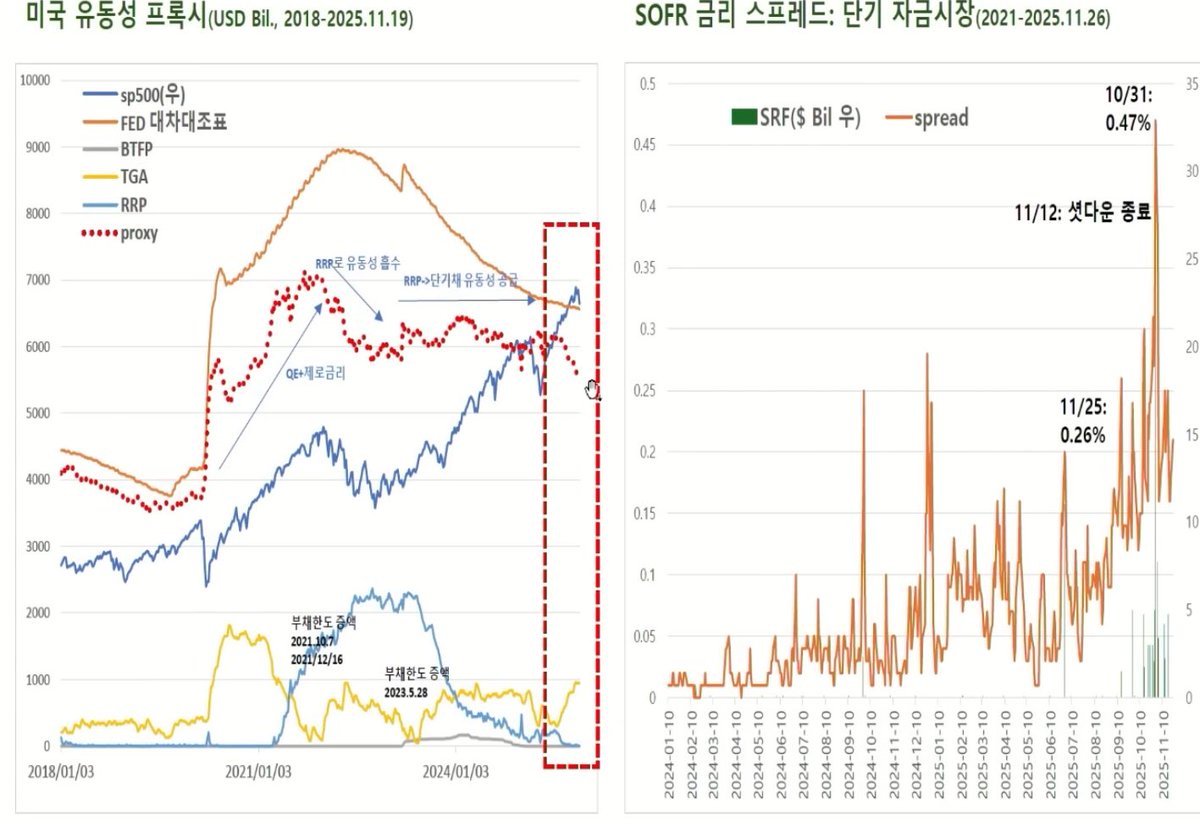

📌 유동성 쇼크 끝, 12월은 산타랠리 가능

📈 1. 핵심 메세지

•11월 조정 = TGA 증가로 인한 시장 유동성 축소

•12월 반등 = TGA 지출 재개로 유동성 공급 회복

•고용 둔화 = 금리 인하 가능성↑

•달러·채권 지표 = 과도한 스트레스 신호 없음

💧 2. 유동성 축소 → 시장 조정

•미국 재무부 TGA 잔고가 7~10월 동안 3,000억 → 1조 달러로 증가

•TGA가 늘어난다는 것은

→ 정부가 지출을 줄이고 자금을 흡수했다는 의미

•이 과정에서 시장 전반 유동성이 감소 → 자산가격 변동성 확대

💸 3. 셧다운 종료 이후 유동성 반전

•셧다운 종료 후 TGA 지출이 재개됨

•11/13 이후 약 1,000억 달러가 다시 시장으로 공급됨

•→ 11월의 긴축 흐름이 12월 들어 완화되는 중

🏦 4. 12월 금리 인하 가능성을 높이는 요인

•최근 고용지표에서 중소기업 고용이 급감

•미국 일자리의 약 60%를 담당하는 중소기업 부문에서

→ 고용 감소 폭이 역사적 평균 대비 크게 하락

•반면 대기업 고용은 상대적으로 안정적

•고용 둔화는 연준의 정책 결정에 금리 인하 압력 요인으로 작용

📉 5. 고용 구조 변화

•2025년 ADP 주간 데이터를 보면

→ 20~500인 규모 회사(중소기업) 신규 고용이 뚜렷한 감소세

•대기업(500인 이상) 고용은 상대적 견조

•노동시장의 하단부에서 충격이 먼저 나타나는 모습

💱 6. 달러 인덱스는 정상 범위 수준

•DXY는 95~100이 장기 평균, 현재 수치는 이 범위와 유사

•달러가 과도하게 강하거나 약한 구간은 아님

•원·달러 환율의 변동은 국내 구조적 요인도 함께 작용

🖥️ 7. 빅테크 투자·부채 이슈는 일시적 변동성 요인

•데이터센터 등 막대한 CAPEX 확대 과정에서

→ 일부 기업의 CDS 프리미엄이 단기간 상승

•그러나 투자등급 전체의 CDS 수준은 역사적 평균과 큰 괴리 없음

•시스템 리스크로 볼만한 신호는 아님

3

21

96

8,691

29 Nov 2025

2025~2026년 시장 초강세 10가지 이유

1. 트럼프 “주식 사상 최고치 계속 유지할 것”

2. 매그니피센트7 연간 6,000억 달러 설비투자

3. 인플레 3% 넘는데도 연준 금리 인하

4. 전 세계 AI 인프라 투자 연 1조 달러

5. 연준, 이틀 뒤 양적긴축(QT) 종료

6. 미국 재정적자 GDP 6% 초과

7. 엔비디아 시총, 세계 6위 국가 주식시장보다 큼

8. 2026년 기업 자사주 매입 사상 최대 1.2조 달러

9. 트럼프 “소득세 완전히 없애겠다”

10. 트럼프 2026년 국민 1인당 2,000달러 현금 지급 약속

출처: The Kobeissi Letter (@KobeissiLetter)

28 Nov 2025

We now have:

1. Trump saying he will keep stocks at record highs

2. $600B/year in Magnificent 7 CapEx

3. Fed cutting interest rates into 3% inflation

4. Global AI infrastructure spending at $1T/year

5. Fed ending Quantitative Tightening in 2 days

6. US deficit spending at >6% of US GDP

7. Nvidia larger than all but 5 national stock markets

8. Record corporate buybacks of $1.2T coming in 2026

9. Trump saying he will "completely cut" income taxes

10. Trump promising $2,000 stimulus checks in 2026

How can you fight this momentum?

1

6

516

28 Nov 2025

$BMNR on Nov 28, 2025

• Tom Lee premium wiped out: from $161 (Jul) → $32 now (-80%)

• Holds 3.63M ETH → world’s largest public ETH treasury (3% of total supply)

• Total liquidation value ~$11.8B vs market cap ~$9.5B → trading at ~25% discount to NAV

→ NAV/share $27.85 vs price $32 (now slight premium, but ETH dip keeps it attractive)

• FY2025 net profit $328M, first-ever dividend $0.01 (first big crypto firm to pay one)

Why it’s hovering here:

1. Oct 10 $19B liquidation hangover

2. Ongoing dilution ( 85% shares YTD)

3. Staking yield 3~3.5% (way below 2022-23’s 8~10% hype)

Why it could still moon:

• NAV discount narrowing fast on ETH rebound

• ETH just needs $2,100-$2,600 hold for NAV surge

• Jan 15 Vegas shareholder meeting → Tom Lee big reveal (MAVAN launch, fresh capital)

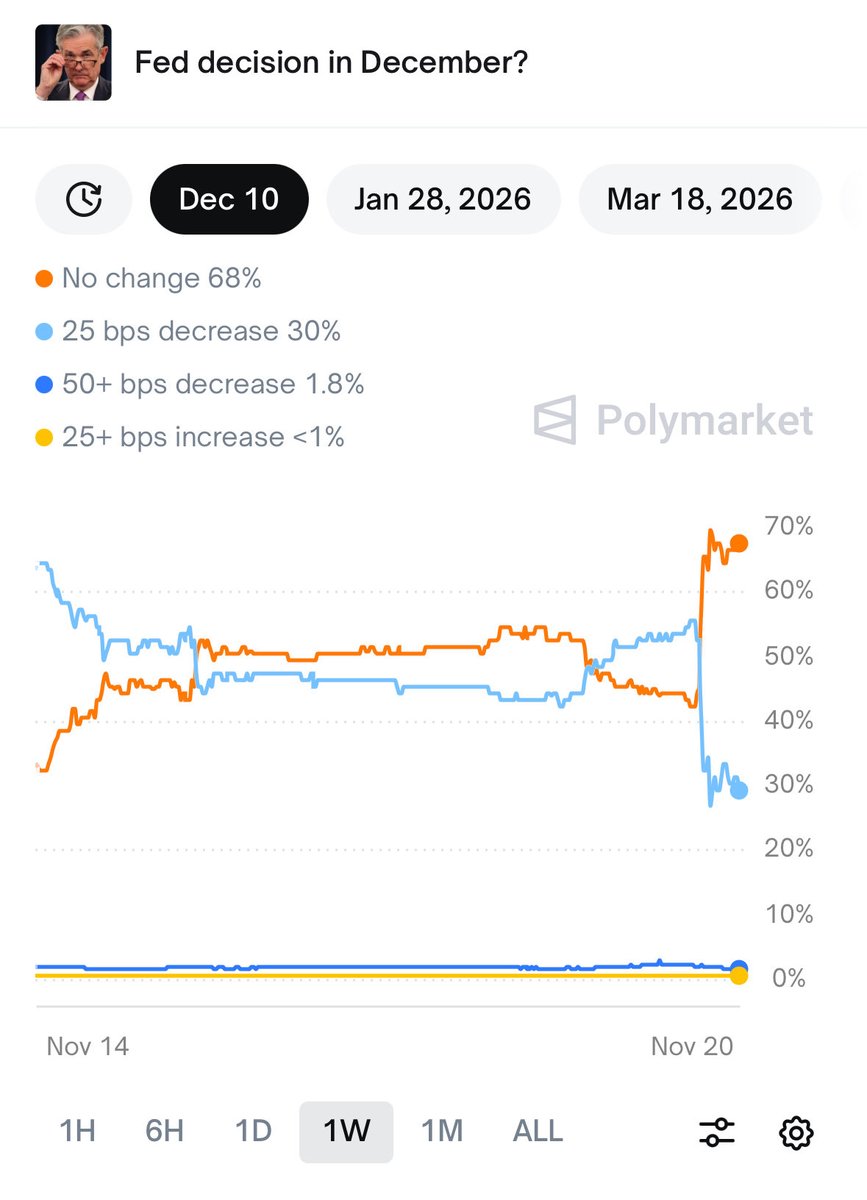

• Dec Fed cut 70% odds → liquidity flood = ETH rocket fuel

Technicals: Oversold no more?

BMNR RSI 28 → climbing, ETH RSI 32 at lows

Verdict:

$BMNR at $32 = ETH exposure with Tom Lee wildcard (slight premium, but event-driven upside)

Aggressive: Buy dips, target 50-100% to Jan (PT $47-$53)

Conservative: Spot ETH (skip dilution drama)

Cheap enough to bet on supercycle? Your call.

#BMNR #Ethereum #TomLee #Crypto

3

278

28 Nov 2025

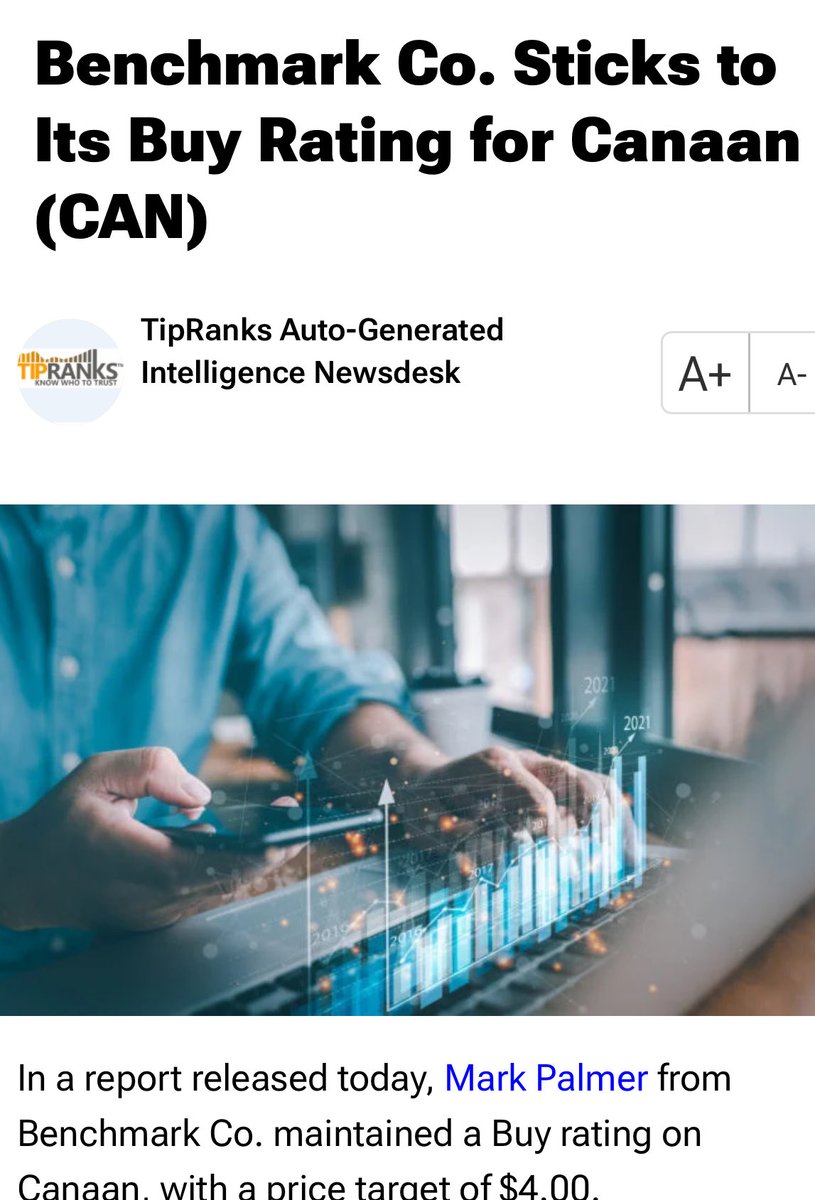

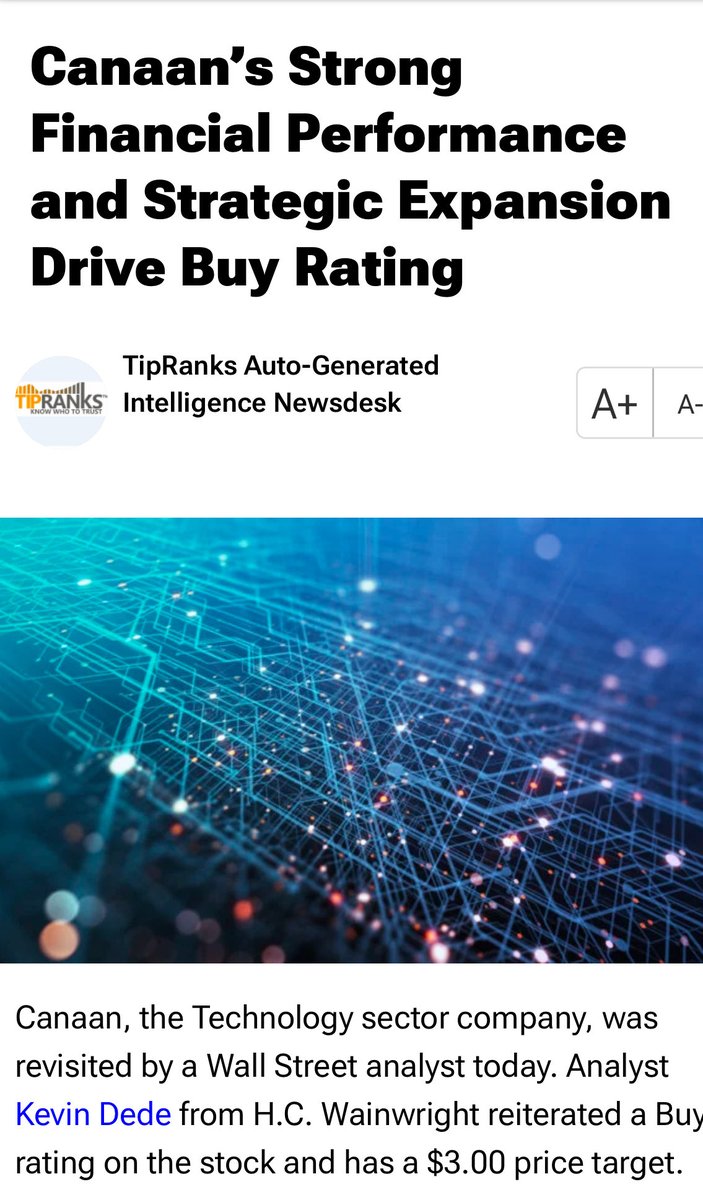

$btc $mstr $coin $can $bmnr $bitf

This chart is one of the most respected macro indicators in crypto: Global M2 Liquidity (3-month lead, green line) vs Bitcoin price (red line)

Key takeaways:

1. Extremely strong lead-lag relationship

Global M2 money supply growth consistently leads Bitcoin price by ~3–4 months. When M2 expands aggressively, BTC follows higher with almost mechanical precision; when M2 stalls or contracts, BTC eventually corrects or consolidates.

2. Current situation (late November 2025)

• Global M2 has been exploding since mid-2025 and is now at or very close to all-time highs (green line surging).

• Bitcoin is still trading in the $89K–$95K zone and has not yet reflected this liquidity wave (red line lagging significantly).

→ The liquidity impulse is already in motion, but BTC has absorbed less than half of it so far.

3. Historical precedents

• 2020–2021: M2 surge post-COVID → BTC hit $69K ~4–6 months later

• 2022: M2 growth stalled → BTC crashed to $15K

• 2023–2024: M2 resumed growth → BTC new ATHs in 2024–2025

The pattern has repeated with remarkable consistency across cycles.

Conclusion & forward view

Current M2 growth rate and absolute level already exceed the 2020–2021 bull market peak. If history is any guide, Bitcoin has substantial upside left in this cycle, very likely pushing well into the $120K–$200K range over the next 3–6 months (Q1–Q2 2026) as the remaining liquidity is priced in.

One-sentence summary:

“Global money printers are already in overdrive; Bitcoin is still only halfway through digesting the flood.”

Strong bullish signal for the medium term. (Macro risks — pace of rate cuts, DXY strength, geopolitics — remain wildcards, but this specific indicator has been one of the most reliable in the entire space.)

4

681

27 Nov 2025

Sundar Pichai on Google’s quantum computing efforts (Nov 2025)

1.“We have the state-of-the-art quantum computing efforts in the world. We still believe we are in the lead.”

→ Google remains confident it has the world’s leading quantum program.

2. Where quantum is right now: “I would say quantum is maybe where AI was 5 years ago. The progress is so exciting.”

→ Quantum is entering the same early-acceleration phase AI was in around 2020.

3. Timeline to practical, useful quantum computers: “Useful, error-corrected quantum computers are probably still a decade or more away.”

→ Minimum 10 years, realistically longer, until fault-tolerant machines arrive.

4. Current technical reality: “We’re still in the noisy intermediate-scale quantum (NISQ) era.”

→ We’re still stuck in the noisy, limited-scale phase—no major breakthroughs yet.

5. Long-term view & commitment: “Quantum computing will be a profound breakthrough over a long period of time… We are investing billions and we are committed for the long term.”

→ Revolutionary in the very long run. Google is pouring billions in and playing the decades-long game.

$ionq $rgti $qbts $alphabet $ibm

#QuantumComputing #GoogleQuantum

27 Nov 2025

$GOOGL CEO basically just said quantum is entering the same acceleration curve AI hit five years ago.

1

1

6

430

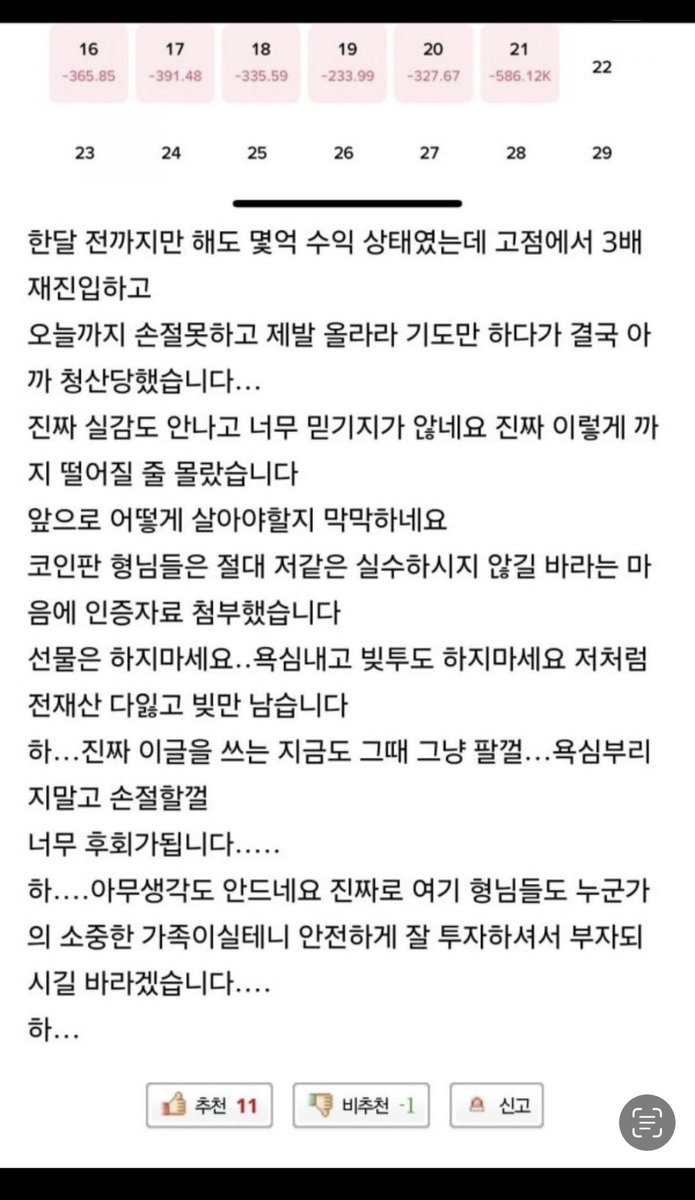

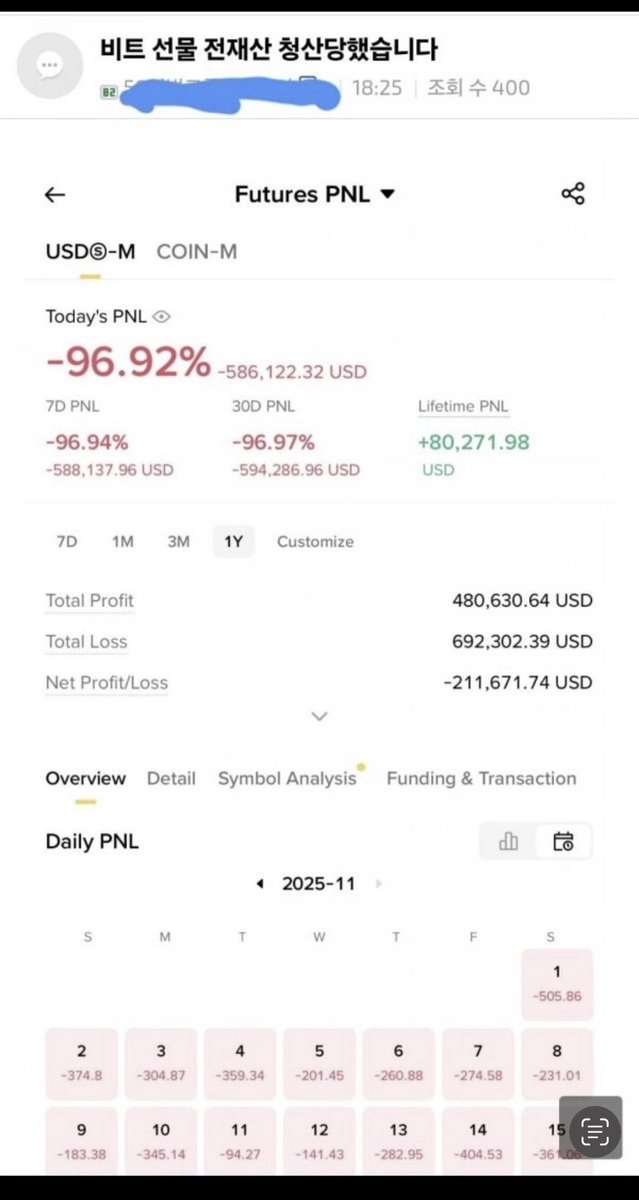

GambleToValue_도박중독 retweeted

26 Nov 2025

비트코인 선물 58 만불 약 9 억 청산 계좌

레버리지는 잘쓰면 약이지만 실패시에 평생 불구가 됨

무섭네요 ㅠㅠ

찰리 멍거 : 투자할 때 100% 확실한 것은 없기에 레버리지를 사용하는 것은 위험하다. 한 번 0을 곱하면 결국 0이 된다. 두 번 부자 될 수 있다고 기대하지 마라

12

8

86

16,675

27 Nov 2025

$BITF: The Most Underrated AI Pivot in the Market Right Now

Thread 🧵 1/10

$BITF is quietly exiting Bitcoin mining entirely by 2026-27 and becoming a pure-play AI/HPC data center company.

The street still thinks it’s a dying miner.

That disconnect is creating one of the biggest mispricings I’ve seen in the AI infra space.

2/10

Key moves already underway:

• Washington facility being fully repurposed for AI workloads

• Multiple hyperscale AI data center projects under construction in North America

• Management: “HPC will generate cash flows far greater than mining ever did”

3/10

Q3 2025 numbers (Nov 13):

Revenue $69.3M → 156% YoY

Adj EBITDA $20M → 122% QoQ

Missed EPS by $0.06 → stock got crushed 18% in a day, then another 50% in the past month

Classic overreaction to transition pain.

4/10

Valuation is laughably cheap for this growth trajectory:

Forward P/E ~7.5x (IT sector average ~23x)

TTM revenue 95% (11× peer average)

Current margins are ugly because of the pivot — they will expand dramatically once HPC revenue kicks in.

5/10

Balance sheet is fortress-like:

~$87M cash, only $74M debt

Total liquidity ~$1B including converts & ATM (~70% of $1.55B market cap)

More than enough to fund the entire build-out.

6/10

Still owns 1,827 BTC (~$156M at $85k) → 10% of market cap

Yes, crypto volatility remains a short-term anchor, but with the new administration regulatory tailwinds, that anchor is turning into a catalyst.

7/10

The TAM is insane:

Global AI data center market

2025: $18B

2032: $94B

CAGR 26.8%

Execute halfway decently and $BITF becomes a top-tier name in one of the hottest infrastructure themes on the planet.

8/10

Risks are real:

• Execution risk on multiple simultaneous builds

• AI demand slowdown (single-business risk after pivot)

• Crypto sentiment drag until mining is fully gone

• Margins still terrible during transition

But the downside feels fully priced in after a 60% drawdown.

9/10

Analyst estimates:

2027 EPS $0.35

12× multiple (very conservative for successful pivot) → $4.20

Consensus 12-month target $4.94 ( 103% from current levels)

10/10

$BITF just got thrown out with the entire crypto miner basket.

The baby is being thrown out with the bathwater — except this baby is morphing into a pure AI data center growth story.

If they deliver even 60-70% of the plan, the re-rating will be explosive.

Not financial advice. Always DYOR.

#BITF #AI #HPC #BitcoinMining #Investing $iren $clsk $can $nbis

2

3

15

1,490

24 Nov 2025

Bloomberg just dropped a bombshell:

“Big Tech’s AI Debt Wave Is Threatening to Swamp Credit Markets”

Hyperscalers are on track to issue $200–300B in bonds in 2025 alone to fund AI capex. That’s bigger than most countries’ annual debt issuance.

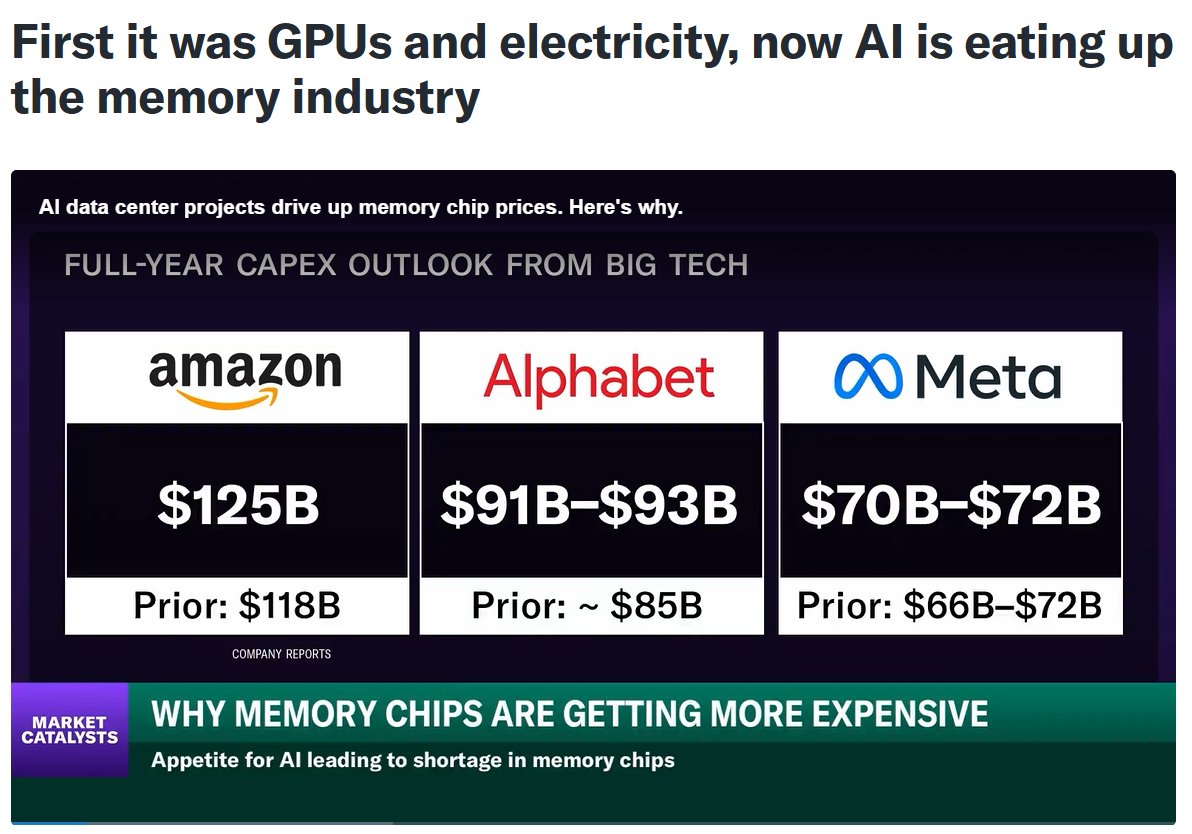

Combined AI capex 2024-2027 from Meta, Google, MSFT, Amazon, Oracle & co. → $1.5–2 TRILLION.

Cash flows can’t keep up → debt explosion.

Meta $10.5B, MSFT $12B , Amazon $20B already done or in pipeline.

Risks: IG credit market saturation → wider spreads in 2025-26

Power grid bottlenecks (AI already eating >50% of new US electricity demand growth)

Massive maturity wall hitting in 2027-2029 if AI revenue disappoints

the AI arms race is being funded with leverage on a historic scale.

Winners will pay it back with trillions in profit.

Losers (and everyone crowded out of the bond market) will feel the pain.

2026 is going to be wild.Source: Bloomberg, Nov 24 2025

bloomberg.com/news/articles/… #BigTech #CreditMarkets #Debt

5

279

24 Nov 2025

비트마인의 현재 주가는 저평가일까?

1. 톰 리 프리미엄의 소멸

2025년 7월 $161 고점 후 현재 $26까지 84% 급락.

현재 주가는 진짜 저평가일까?

2. 실질 자산은 압도적.

11월 16일 공시 기준 보유 자산:

• 이더리움 3,560,000 ETH (전체 공급량 2.94%)

• 비트코인 192 BTC (미미함)

• 현금 Eightco 지분 등 약 $650M

→ 총 청산가치 약 $11.8B

현재 시가총액 $7.4B → NAV 대비 37% 할인

(NAV per share $27.85 vs 주가 $26.00)

이더리움 기준으로만 따져도 세계 1위 트레저리이며, 목표 5%까지 절반 이상 도달.

3. 2025 회계연도 실적은 대박.

• 순이익 $328M (전년 –$41M)

• 완전희석 EPS $13.39

• 처음으로 $0.01 배당 선언 → 대형 크립토 기업 최초 배당

채굴 매출은 여전히 $6M 수준으로 미미하지만, 보유 ETH의 가격 상승 스테이킹 수익 자본조달 프리미엄이 주된 이익 원천이다. 실적 발표 후에도 주가는 변동성을 보였으나, 배당 선언은 주주 친화적 신호로 작용하며 장기 홀더 유치에 긍정적이다. 다만, ETH 가격 45% 하락으로 인해 $4B 규모의 unrealized loss가 발생한 점은 무시할 수 없는 리스크 .

4. 왜 이렇게 폭락했나?

1) 10월 10일 글로벌 청산 이벤트

트럼프 재선 이후 중국 100% 관세 발언 → $19B 규모 선물 강제청산 → ETH 12% 급락 → DAT 주식들 동반 추락.

BMNR은 그날 이후 60% 추가 하락.

2) 지속적인 희석 공포

1주당 ETH를 늘리기 위해 프리미엄이 붙은 전환사채/신주를 계속 발행. 2025년 들어 발행 주식 수 85% 증가.

3) 스테이킹 수익률 실망

현재 연 3~3.5% 수준으로, 시장이 기대했던 8~10%에 크게 미달 → “단순 ETH 홀딩보다 못하다”는 비판.

이 외에도 10x Research의 Markus Thielen은 “고비용 구조, 낮은 스테이킹 수익, NAV 프리미엄 소실”을 구조적 문제로 지적하며, 주주가 opaque 구조에 갇힐 수 있다고 월가에서 경고.

5. 하지만 여전히 비트마인이 매력적인 이유

• NAV 할인율 37%는 2024년 이후 최저치 (과거 평균 20~30% 프리미엄)

• ETH가 $2,600 → $2,100 구간만 방어하면 NAV는 오히려 상승

• 2026년 1월 15일 라스베이거스 윈 호텔 주주총회 → 톰 리의 대규모 비전 발표 가능성 (MAVAN 미국산 Validator 네트워크 론칭, 대규모 자본조달 계획 등)

• Fed 12월 금리인하 70% 확률 → 유동성 장세 재개 시 ETH가 가장 크게 반등할 가능성

톰 리는 여전히 ETH $12K~$15K (2025년 말) 전망을 유지하며, “supercycle” 가능성을 강조한다   . 이는 100x 장기 상승 잠재력을 시사하나, 단기적으로는 Fed 인하와 유동성 회복이 핵심 촉매다.

6. 기술적 그림 (현재 매우 과매도)

• BMNR: RSI 14일 28 (2024년 이후 최저), 200일선 이탈 후 재진입 시도 중

• ETH/USD: $2,600 장기 지지선 테스트 중, 다음 지지 $2,100~$2,200 (7월 저점)

• 데드크로스 임박 → 단기 추가 하락 가능성 있지만, RSI가 4월 저점 수준까지 내려왔기 때문에 반등 에너지도 충분히 축적

7. 최종 판단

BMNR = ETH를 37% 할인된 가격에 사는 것 톰 리 이벤트 옵션 공짜로 받는 구조

• 공격적 투자자 → 지금 진입, 1월 주총 전후 매도 목표 (50~100% 반등 가능)

• 보수적 투자자 → 그냥 ETH 현물 사라. 희석 걱정 없이 동일 수익

현재는 충분히 싸졌지만 “완전 안전한 저평가”는 아니다. 리스크 감당 가능하면 매수, 아니라면 ETH 직접 보유가 2026년까지 더 나은 선택이다. 하지만, 추가 ETH 매입처럼 톰 리의 행동이 지속된다면, 반등 모멘텀은 더 강해질 수 있다

$bmnr $bmnu $btc

1

5

481

GambleToValue_도박중독 retweeted

23 Nov 2025

2025 winter is here! Don’t forget to check out our seasonal offers at shop.canaan.io/ and get yourself a mini 3 to combat cold!

Home heaters are becoming a global topic as new technologies reshape how households generate and manage heat, and help #GreenEnergy. Yesterday, I was visiting Vienna to meet @maxobw and @HaraldRauter at @21energy_com. It was impressive to learn how their team is applying Bitcoin technology to support residential heating across Austria and broader Europe. We also appreciate the positive feedback on our Mini 3, @canaanio remains committed to continued innovation.

Spoiler alert: I’ll share some fun facts about winter European home heating in the comments to this thread.❄️

$CAN #homemining #heating

#EnergyEfficiency

P.S. I did not include their heater photos here, but interested readers are welcome to review them directly.

2

4

26

9,752