pro.amberdata.io Crypto Option Analytics - Nothing tweeted is financial advice. linktr.ee/AD_Derivatives Amberdata Corporate - twitter.com/Amberdataio

Joined March 2020

- Tweets 3,019

- Following 1,157

- Followers 16,540

- Likes 5,814

861 Photos and videos

AD Derivatives (formerly GVol) retweeted

Apr 13

1) During US-Iran negotiations, a range of Call buys were made on ETH, the largest notional being May 3.2k x30k.

In total, $3.5m premium, not huge, but conspicuous over a weekend.

Talks v1 predictably fell short.

During Euro hours, a strip of short-term 62-70k BTC Puts lifted.

5

6

32

4,436

AD Derivatives (formerly GVol) retweeted

Mar 30

1) Quarterly Mar expiry forced many terminal hedges to roll out to April.

The maturity chosen for hedges/plays in this ME/Trump environment is critical.

Too short-term and it is often wasted premium, particularly with elevated fear/Put Skew.

Puts funded by Calls risk resolution.

3

3

19

3,090

AD Derivatives (formerly GVol) retweeted

Mar 26

18

11

85

32,553

AD Derivatives (formerly GVol) retweeted

Mar 19

1) STRC assisted BTC to 76k and last report's 75k Calls to a 4x, but there was no sign of profit taking as Spot retraced hard.

Instead, buying of 50-60k Puts, Mar Put spreads.

When Israel hit energy infra yesterday and PPI came in hot, Puts lifted via April Dec risk reversals.

5

4

26

4,084

AD Derivatives (formerly GVol) retweeted

1) Some rays of light emerging from the darkness.

While Put Skew remains firm on the back of continued protection vs downside global uncertainties, decent clip buying of end-of-Mar and April 75k Calls take advantage of the depressed Call Skew and a contrary directional view.

🧵

1

5

33

17,203

AD Derivatives (formerly GVol) retweeted

Mar 3

Crypto doesn’t trade like equities.

It trades like flow.

“Who’s paying 30 vols wide for convexity if all they want is linear exposure?

@0xturbanurban, CEO of @MonacoTrading and former GSR trader.

Full Amberdata Derivatives Podcast @genesisvol below...

blog.amberdata.io/lessons-fr…

4

6

1,148

AD Derivatives (formerly GVol) retweeted

Feb 26

“The first white hair in my beard was when oil went negative.”

Before leading @MonacoTrading, @0xturbanurban was on the oil desk at Goldman Sachs during one of the most historic market events ever.

From calling oil producers during negative WTI…

To building DeFi trading at @GSR_io

This episode breaks down what real risk management looks like when models fail and markets break.

Watch the full Amberdata Derivatives Podcast hosted by @genesisvol 🔻

blog.amberdata.io/lessons-fr…

3

4

11

1,307

AD Derivatives (formerly GVol) retweeted

Feb 24

1) In a continuous downtrend in the existing range, it's not a surprise to see ongoing downside plays (protection and bearish) on BTC.

How these are initiated determines the degree of likely returns.

Put skew is back to Feb5th levels, IV>RV.

58k Puts in demand, Put spreads, RRs.

7

8

67

16,046

AD Derivatives (formerly GVol) retweeted

Feb 21

Strong support here with 24ema 25ema 26ema 27ema 28ema 29ema 30ema 31ema 32ema 33ema 34ema 35ema 36ema 37ema 38ema 39ema 40ema 41ema 42ema 43ema 44ema 45ema 46ema 47ema 48ema 49ema 50ema 51ema 52ema 53ema 54ema 55ema 56ema 57ema 58ema 59ema 60ema 61ema 62ema 63ema 64ema 65ema 66ema 67ema 68ema 69ema 70ema 71ema 72ema 73ema 74ema 75ema 76ema 77ema 78ema 79ema 80ema 81ema 82ema 83ema 84ema 85ema 86ema 87ema 88ema 89ema 90ema 91ema 92ema 93ema 94ema 95ema 96ema 97ema 98ema 99ema 100ema 101ema 102ema 103ema 104ema 105ema 106ema 107ema 108ema 109ema 110ema 111ema 112ema 113ema 114ema 115ema 116ema 117ema 118ema 119ema 120ema 121ema 122ema 123ema 124ema 125ema 126ema 127ema 128ema 129ema 130ema 131ema 132ema 133ema 134ema 135ema 136ema 137ema 138ema 139ema 140ema 141ema 142ema 143ema 144ema 145ema 146ema 147ema 148ema 149ema 150ema 151ema 152ema 153ema 154ema 155ema 156ema 157ema 158ema 159ema 160ema 161ema 162ema 163ema 164ema 165ema 166ema 167ema 168ema 169ema 170ema 171ema 172ema 173ema 174ema 175ema 176ema 177ema 178ema 179ema 180ema 181ema 182ema 183ema 184ema 185ema 186ema 187ema 188ema 189ema 190ema 191ema 192ema 193ema 194ema 195ema 196ema 197ema 198ema 199ema 200ema 201ema 202ema 203ema 204ema 205ema 206ema 207ema 208ema 209ema 210ema 211ema 212ema 213ema 214ema 215ema 216ema 217ema 218ema 219ema 220ema 221ema 222ema 223ema 224ema 225ema 226ema 227ema 228ema 229ema 230ema 231ema 232ema 233ema 234ema 235ema 236ema 237ema 238ema 239ema 240ema 241ema 242ema 243ema 244ema 245ema 246ema 247ema 248ema 249ema 250ema 251ema 252ema 253ema 254ema 255ema 256ema 257ema 258ema 259ema 260ema 261ema 262ema 263ema 264ema 265ema 266ema 267ema 268ema 269ema 270ema 271ema 272ema 273ema 274ema 275ema 276ema 277ema 278ema 279ema 280ema 281ema 282ema 283ema 284ema 285ema 286ema 287ema 288ema 289ema 290ema 291ema 292ema 293ema 294ema 295ema 296ema 297ema 298ema 299ema 300ema 301ema 302ema 303ema 304ema 305ema 306ema 307ema 308ema 309ema 310ema 311ema 312ema 313ema 314ema 315ema 316ema 317ema 318ema 319ema 320ema 321ema 322ema 323ema 324ema 325ema 326ema 327ema 328ema 329ema 330ema 331ema 332ema 333ema 334ema 335ema 336ema 337ema 338ema 339ema 340ema 341ema 342ema 343ema 344ema 345ema 346ema 347ema 348ema 349ema 350ema 351ema 352ema 353ema 354ema 355ema 356ema 357ema 358ema 359ema 360ema 361ema 362ema 363ema 364ema 365ema 366ema 367ema 368ema 369ema 370ema 371ema 372ema 373ema 374ema 375ema 376ema 377ema 378ema 379ema 380ema 381ema 382ema 383ema 384ema 385ema 386ema 387ema 388ema 389ema 390ema 391ema 392ema 393ema 394ema 395ema 396ema 397ema 398ema 399ema 400ema

175

124

1,676

156,887

AD Derivatives (formerly GVol) retweeted

Feb 19

From negative oil at Goldman Sachs to building onchain market infrastructure w/ @genesisvol 🛢️

@0xturbanurban, CEO of @MonacoTrading and former @GoldmanSachs & @GSR_io trader, joins the Amberdata Derivatives Podcast to break down volatility regimes, ETF flows, DeFi liquidity, & why risk engines matter more than throughput.

Watch the full episode today.

blog.amberdata.io/lessons-fr…

2

1

11

1,920

AD Derivatives (formerly GVol) retweeted

Feb 18

From negative oil at Goldman Sachs to building onchain market infrastructure.

Simran Singh, CEO of Monaco and former Goldman Sachs and GSR trader, joins the Amberdata Derivatives Podcast to break down volatility regimes, ETF flows, DeFi liquidity, and...

hubs.la/Q043JDZG0

2

1

2

752

AD Derivatives (formerly GVol) retweeted

Feb 11

BTC DVol exploded from sub-40 to 90.

But 90-day basis barely moved, and funding didn’t fully flush.

Vol spike ≠ capitulation.

Short-term bounce? Likely.

New cycle? Not yet.

Full breakdown in this week’s Amberdata Derivatives @genesisvol Newsletter. blog.amberdata.io/bitcoin-vo…

1

9

869

2

9

105

57,302

AD Derivatives (formerly GVol) retweeted

Feb 9

I worked with @SinclairEuan back in the late 90's.

He is one of many true geniuses I have met along the way, but one of the few who naturally communicates complex ideas into simple language and analogies.

So many of the others will only be able to answer a question on a whiteboard with complex maths.

Whereas Euan is able to do the maths equally well, but you'll only find this on a pub blackboard (food menu scrubbed off) while simultaneously drinking a pint and watching the All Blacks.

@genesisvol asking the questions.

A must listen if you want to be pushed to think differently.

Jan 23

Most traders obsess over indicators. That’s not edge.

In this clip from the Amberdata Derivatives Podcast, @SinclairEuan explains why edge is a real-world phenomenon first and math second.

Indicators don’t create edge; they only measure it. Find the phenomenon, then choose the tool. @genesisvol

Watch the full episode for the full framework.

blog.amberdata.io/euan-sincl…

13

15

196

36,594

AD Derivatives (formerly GVol) retweeted

1) If you slept/afk for 48hrs you might check-in - BTC 70k - as if nothing had happened.

If not, you may well have been awake through a nightmare if not hedged/positioned as indicated in the last report.

18% capitulation event down to 60k.

Then 20% pump 70k

IV Skew Forensics 🧵

7

9

95

33,636

AD Derivatives (formerly GVol) retweeted

Update: Puts have been rolled to 65k strike, also ITM.

1

4

750

AD Derivatives (formerly GVol) retweeted

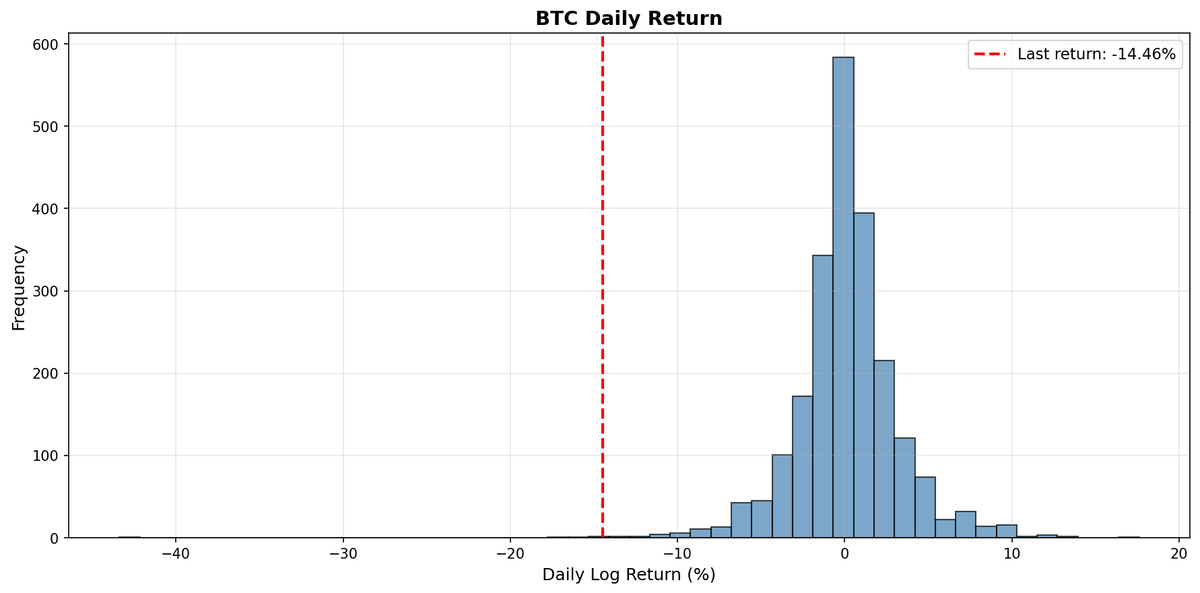

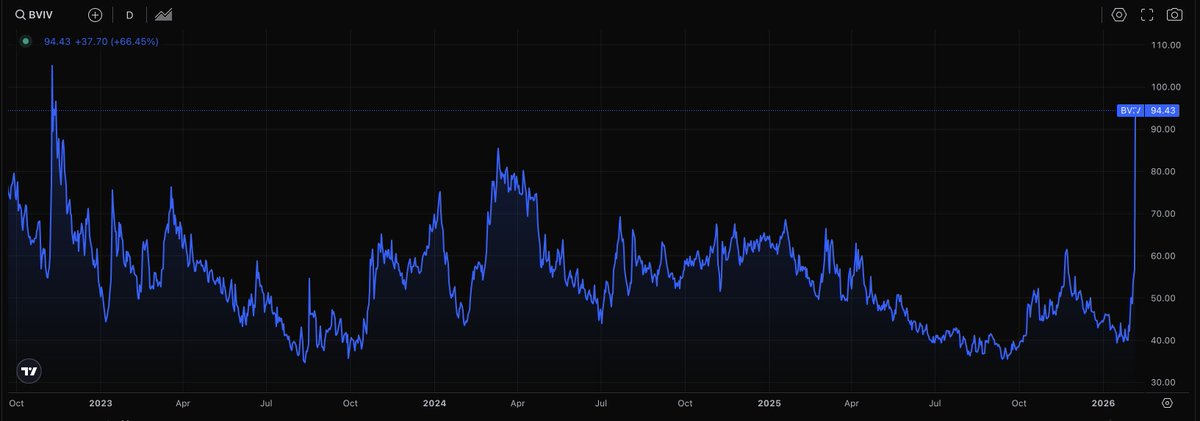

Feb 5

It's important to contextualize market moves, and that can be painful...Buckle. In.

- A -14.4% move in one day is 4.5σ, when looking over the past 6y....the last time we saw this was Nov '22 during the FTX collapse.

- The last time $BVIV (the VIX-equivalent for BTC vol) was this high was also during the Nov '22 turmoil.

- The liquidations are nowhere near the 10Oct25 amounts we witnessed a few months back...leverage pretty much flushed out of the system it feels like

5

8

39

6,234

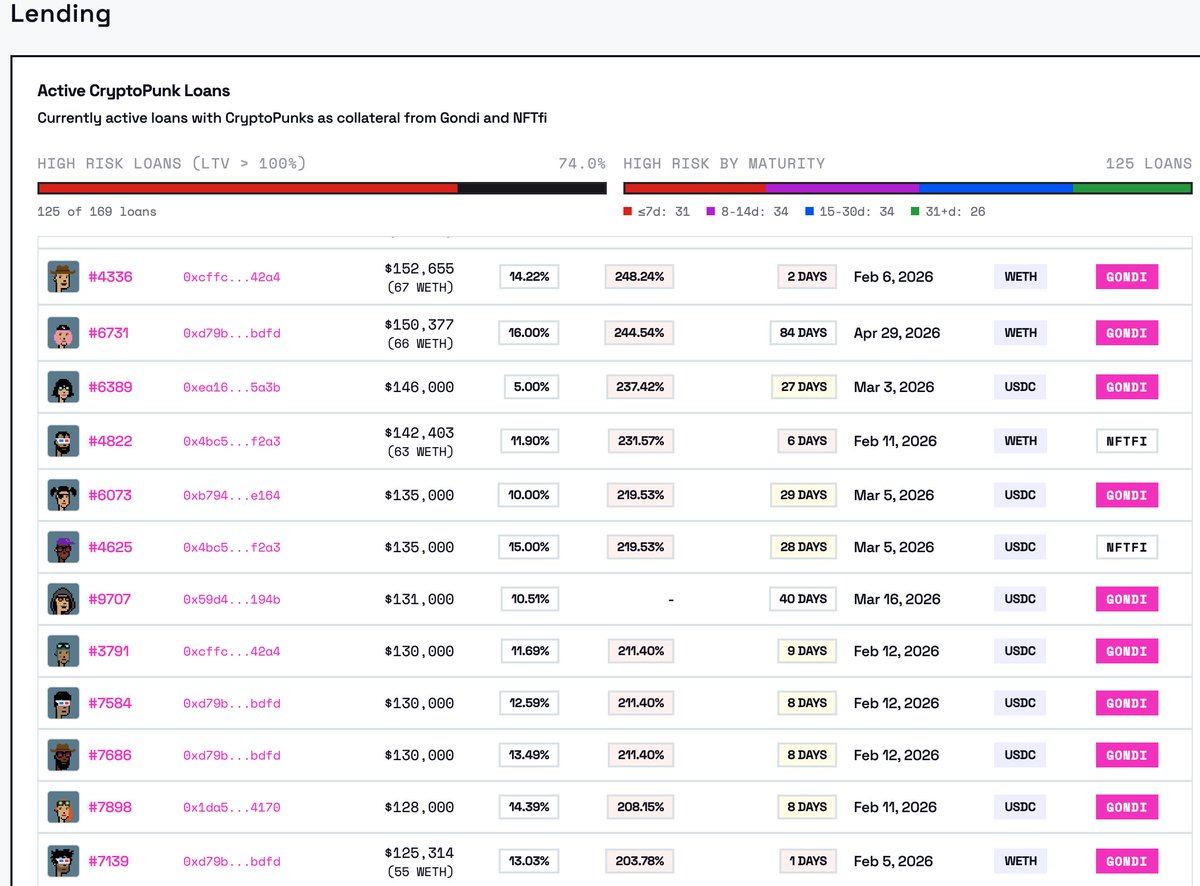

74% of all Cryptopunk loans have a LTV > 100%.

With 65 loans maturing in 14 days.

Do what you will with this info.

punkdata.junkdrawer.wtf/lend…

3

7

39

7,916

AD Derivatives (formerly GVol) retweeted

1) BTC Option flows suggesting downside plays not over.

Now In-The-Money Puts rolled down to lower (predominantly 70k Strike) to TP but keep notional exposure.

New Put spreads bought.

New OTM Puts bought.

Similar behaviour on IBIT as well as Deribit.

Skew Implied Vol firm.

7

17

73

8,529

AD Derivatives (formerly GVol) retweeted

Jan 29

Gold is up 110% and Silver 300% since Jan 2025. 🏌️

But is it just a weak Dollar? Amberdata’s @genesisvol highlights why the math doesn't quite add up for a simple USD correlation.

"If the move... was only a USD-driven response, we’d expect other ‘hard assets’ such as BTC, OIL, and Real Estate to also follow gold and silver higher."

Instead, we’re seeing a "global debasement hedge" triggered by a loss of confidence in the world's most indebted nations (like Japan). 🇯🇵

Greg's take: These aren't retail trades; these are central bank and sovereign fund flows.

Read more in @ForbesCrypto by @CharlesLBovaird: forbes.com/sites/digital-ass…

1

4

10

1,381