#NOLA Learning and Growing myself through this life #gigdriver #AsphaltLegendsUnite #Asphalt9Legends #Hypercars #CrossPlay #Gameloft #ForzaHorizon #Gaming

Joined January 2021

- Tweets 17,619

- Following 5,882

- Followers 5,529

- Likes 38,900

2,528 Photos and videos

Pinned Tweet

28 Oct 2025

I just invited you to earn with Uber. Earn at least $1,374 for your first 151 passenger trips in 30 days. 🤑 💲💲💲💲💲🤑💵💵💵💵💵 🎉🎉🎉 #job #sidegig #gigoftheday #WONDERING drivers.uber.com/i/dbs4a1g

1

331

GrumpyGigDriver 🇺🇲🇺🇸🔞💸🎲🏈🎆🎇🧨✨ retweeted

Jun 15

So, Trump is gonna give Iran $300 billion to open a strait that wasn’t closed, so long as they promise not build a nuke they didn’t have?

Do I have that just about right?

2,822

5,622

30,691

538,585

RT @humacyte: June is Men’s Health Month, an important time to focus on conditions that quietly impact long‑term health—starting with vascu…

6

GrumpyGigDriver 🇺🇲🇺🇸🔞💸🎲🏈🎆🎇🧨✨ retweeted

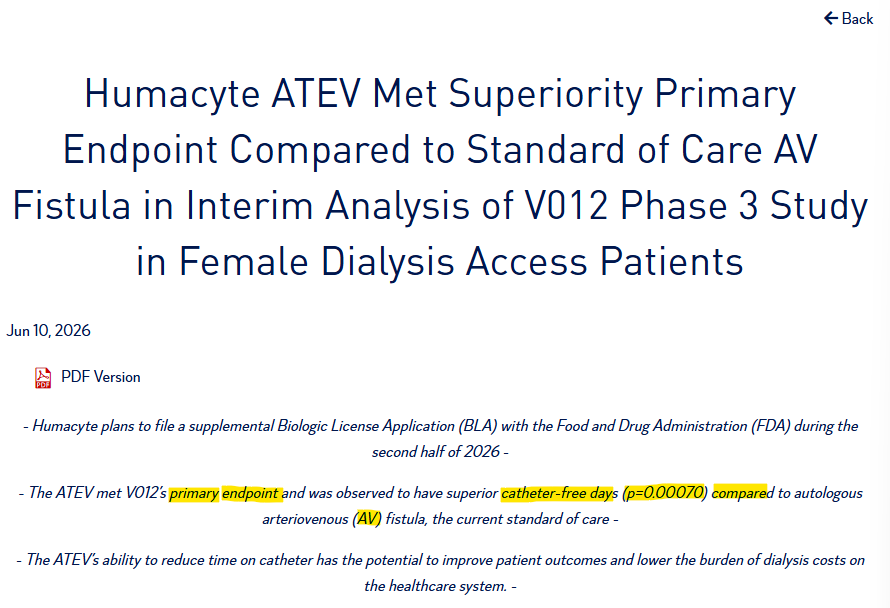

$HUMA just presented their V012 Interim Data and it was on point.

Everything went as expected.

Key Points from their Press Release:

➡️[...] patients implanted with the ATEV achieved an average of 220 catheter-free days compared to 129 catheter-free days for patients who received an AV fistula. The result was statistically significant (p=0.00070), meeting the primary endpoint of the study.

➡️Patients receiving the ATEV incurred infections at a rate of six per 100 patient years, as compared to 23 per 100 patient years for patients receiving an AV fistula procedure.

➡️There were no study access-associated infections reported in the ATEV patients, while there were three among the AV fistula patients.

➡️Humacyte plans to file a supplemental BLA with the FDA during the second half of 2026.

Why is the stock down?

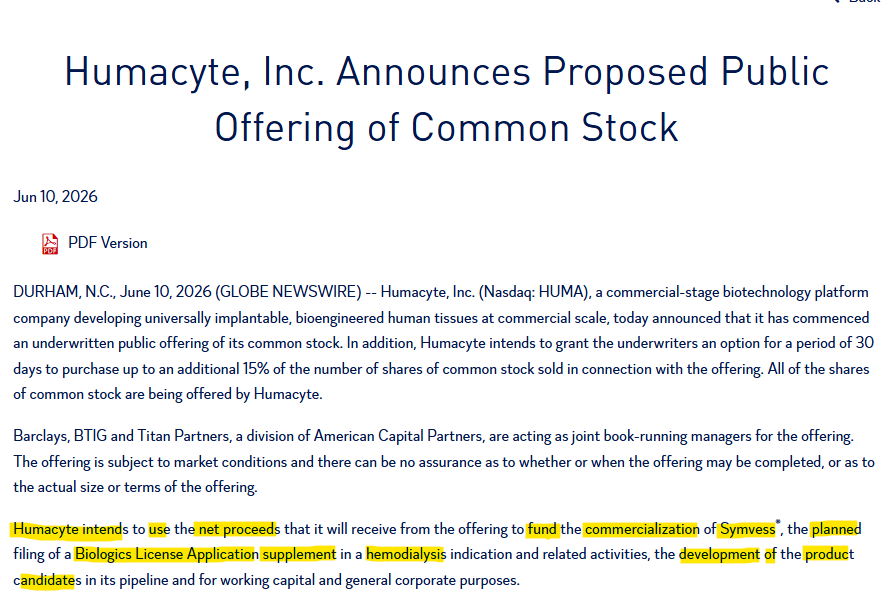

$HUMA announced a Public Offering to fund operations and BLA application. Something that should've been expected.

IMO the 12% dip is a perfect entry point for anyone looking to buy into the stock.

I would've expected the stock to raise considerably after the positive news but the Stock Offering blunted the market.

In any case, $HUMA just de-risked considerably and is now intrinsically worth much much more than just yesterday.

3

11

2,442

GrumpyGigDriver 🇺🇲🇺🇸🔞💸🎲🏈🎆🎇🧨✨ retweeted

@DrLauraNiklason @humacyte congratulations! Great day for Humacyte and medical advancement. 🎉🥳

1

5

405

Wages Are Falling. Wealth Is Surging. No Wonder Americans Are Unhappy

nytimes.com/2026/06/13/busin…

16

GrumpyGigDriver 🇺🇲🇺🇸🔞💸🎲🏈🎆🎇🧨✨ retweeted

Jun 11

$HUMA: Humacyte (-20.9%) trading lower premarket after announcing top-line interim results for the V012 Phase 3 study and pricing an offering of 47,619,048 shares of common stock at $1.05/share.

1

1

1,129

GrumpyGigDriver 🇺🇲🇺🇸🔞💸🎲🏈🎆🎇🧨✨ retweeted

Jun 10

Humacyte (Nasdaq: $HUMA): V012 Phase 3 Win Strengthens the Dialysis Access Story, but Public Offering Keeps Dilution Risk Front and Center merlintrader.com/humacyte-ju…

1

3

3

1,238

GrumpyGigDriver 🇺🇲🇺🇸🔞💸🎲🏈🎆🎇🧨✨ retweeted

Jun 12

H.C. Wainwright raises Humacyte stock price target on trial data investing.com/news/analyst-r…

2

5

375

GrumpyGigDriver 🇺🇲🇺🇸🔞💸🎲🏈🎆🎇🧨✨ retweeted

Jun 12

$HUMA Humacyte The 3.5mm bioengineered coronary vessels are getting ready for their first-in-human CABG clinical trials! But every great journey needs a powerful team. @American_Heart and @gatesfoundation, let’s join forces to change the future #HeartHealth

3

4

688

GrumpyGigDriver 🇺🇲🇺🇸🔞💸🎲🏈🎆🎇🧨✨ retweeted

Jun 12

$huma im a type 1 diabetic and i would like to know whatever happen to the BIOVASCULAR PANCREAS humacyte was working on. this could be a game changer?

2

2

6

1,012

GrumpyGigDriver 🇺🇲🇺🇸🔞💸🎲🏈🎆🎇🧨✨ retweeted

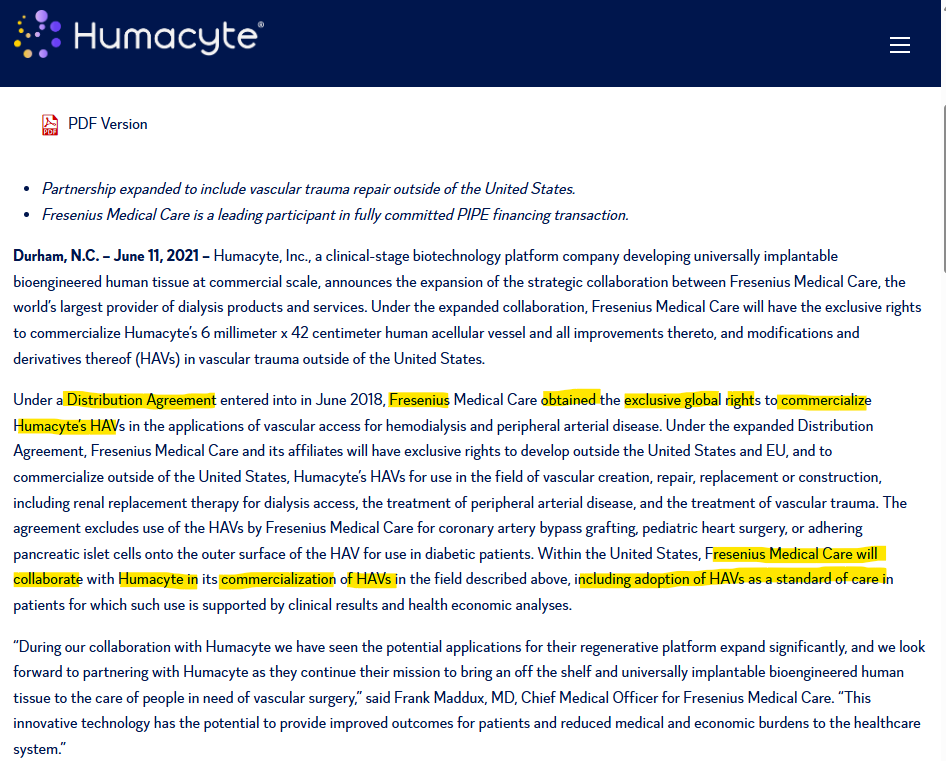

Most of your comment is wrong btw...

The Fresenius - Humacyte relationship is governed by a distribution agreement. Fresenius is contractually obligated to adopt Symvess as SoC for patients where clinical data supports its use.

As I've said in my above comment, Fresenius is one of the two largest dialysis clinic operators in the US, if Fresenius institutes a clinical protocol stating that certain patient profiles should receive a Humacyte ATEV to lower infection rates and eliminate catheter time (which they contractually have to), its clinical network will refer those patients to surgeons with instructions to use an ATEV.

Any hospital VAC and vascular surgeons will approve and adopt a device if a dominant provider network like Fresenius is aggressively feeding them patients specifically marked for that technology.

Given the potential of the $HUMA's ATEV, it would be stupid for Fresenius not to offer their ATEV's, mainly because $HUMA has potential to surpass Fresenius market cap, and a 8% incentivises Fresenius to adopt ATEV's asap.

Maybe you should start reading press releases...

2

2

7

701

GrumpyGigDriver 🇺🇲🇺🇸🔞💸🎲🏈🎆🎇🧨✨ retweeted

Jun 11

Que mal timing con el stock offering Humacyte.

$HUMA

Los resultados del estudio V012 de fase 3 en pacientes femeninas en diálisis alcanzó su objetivo principal, las pacientes que recibieron el vaso sanguíneo de ingeniería tisular acelular (ATEV) de la compañía tuvieron un promedio de 220 días sin catéter, frente a 129 días para aquellas que recibieron una fístula arteriovenosa estándar. El director médico de la compañía describió este resultado como "una mejora muy significativa para las pacientes, que a menudo tienen menos opciones adecuadas".

1

1

5

411

GrumpyGigDriver 🇺🇲🇺🇸🔞💸🎲🏈🎆🎇🧨✨ retweeted

Humacyte $HUMA V012 Phase 3 primary endpoint met convincingly.

Planned sBLA filing H2 2026. Possible dialysis approval in sight.

Dilution stings. But they're raising to fund the exact catalyst that could rerate this stock.

This is the data we were waiting for.

1

5

13

1,710

GrumpyGigDriver 🇺🇲🇺🇸🔞💸🎲🏈🎆🎇🧨✨ retweeted

Humacyte $HUMA

Symvess FDA approved. World-class founder. Fresenius backing (world's largest dialysis provider)

June 11 Phase 3 data announcement = unlocks potential dialysis sBLA.

Distressed = opportunity.

Discover more 👉 youtube.com/@InvestWithOlivi…

5

17

1,900

GrumpyGigDriver 🇺🇲🇺🇸🔞💸🎲🏈🎆🎇🧨✨ retweeted

$HUMA - D-Day is here - Does Humacyte make or break? - Routes forward after announcement

Humacyte is due to publish results from V012. Looking at the slow market adoption of Symvess in the trauma indication (we haven’t seen any (!) further sales published via USAspending in recent weeks (!)), positive V012 is crucial for the survival of Humacyte – It is as easy as that.

Dialysis is the only bullet left to change the narrative here, followed by an immediate endorsement by Fresenius Medical Care (et al), and ideally further dialysis service providers.

Expected share price development:

FAILURE: We would expect an immediate reaction down by 60-70%, well below the USD 1.00 mark – Realistically Humacyte will need to follow with a reverse split (10:1) and a cap raise in the c 50% dilution range to reach c. USD 40-60m proceeds, enough to survive for 8-10 months. Trauma would then need to pick up, or the company will be stuck in a death spiral – We would expect even harder cost cutting / FTE reduction, in line with our proposed Restructuring Plan.

SUCCESS: Could lead to a 1.5-2.0x of the current share price – followed by an immediate or short-term cap raise (2-3 weeks), and a cap raise of 10-15%, with proceeds c. USD 50-90m – But far better medium-term perspective from 2027 onwards (dialysis adoption).

In case of failure, we will immediately revisit our position – and might revisit our Restructuring Plan in communication to key shareholders (whoever is left by then).

1

2

7

1,664

GrumpyGigDriver 🇺🇲🇺🇸🔞💸🎲🏈🎆🎇🧨✨ retweeted

Jun 9

$HUMA 🩸 Humacyte se acerca a su dia D.

Pendiente de presentación de resultados V012 y subiendo hoy un 7%🟢

¿Qué crees que pasará? ¿La veremos en 3-4$?

¿O se irá al pozo? 🤔

Sea lo que fuere. Faltan 48h ⌛ y se nota...

May 28

Buena subidita la de hoy en mi cartera de acciones 😃

Estoy a -5% en $HUMA Humacyte y nos acercamos al mes Crucial donde veremos si sigue su tendencia 📈🩸

Diálisis será la clave

3

1

9

3,178

GrumpyGigDriver 🇺🇲🇺🇸🔞💸🎲🏈🎆🎇🧨✨ retweeted

Jun 9

Humacyte (Nasdaq: $HUMA): heading into the June 11 V012 readout merlintrader.com/humacyte-ju…

1

3

792

GrumpyGigDriver 🇺🇲🇺🇸🔞💸🎲🏈🎆🎇🧨✨ retweeted

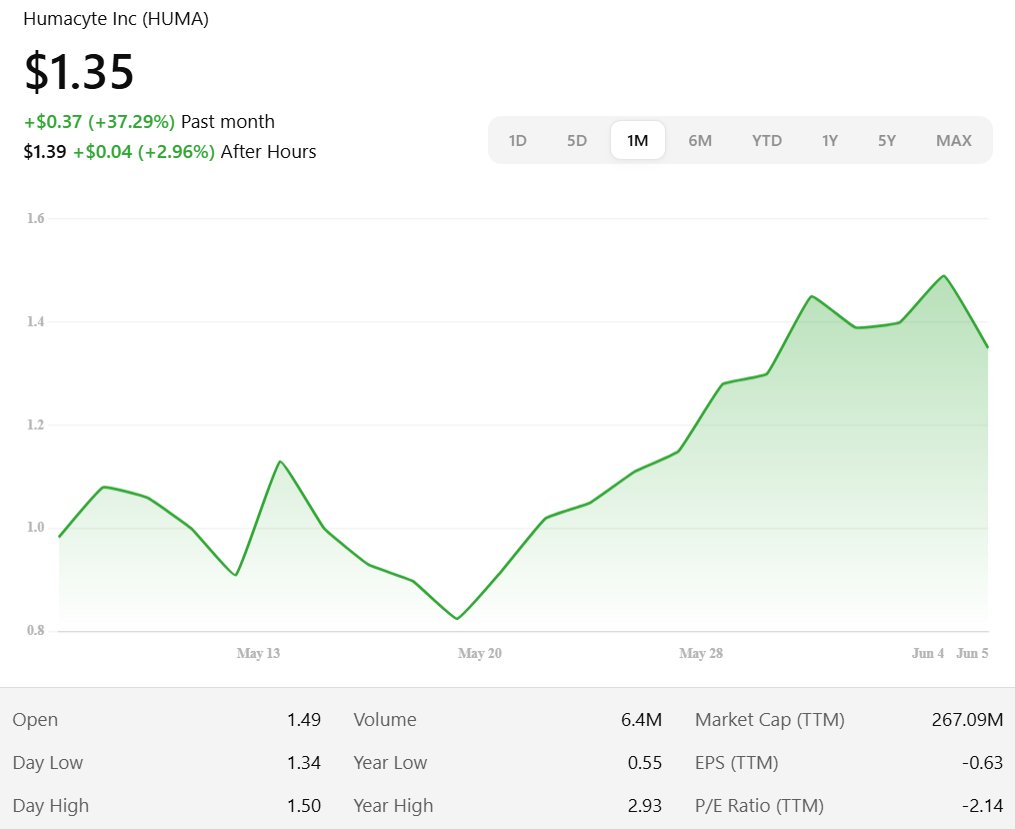

$HUMA DD

Been watching HUMA here because the setup is starting to get interesting again.

The stock is still beaten down and trading around the $1.35–$1.37 area, but the latest filing cleaned up one of the bigger issues: Humacyte regained Nasdaq compliance after getting a delisting notice in May.

That matters because small-cap biotech names can get crushed just from that kind of overhang. Now that the compliance risk is off the table, the market can go back to focusing on the actual business updates.

The main bullish piece for me is the VA contract for Symvess. Humacyte announced that Symvess is now under contract with the U.S. Department of Veterans Affairs, which makes it more accessible across roughly 170 VA hospitals. For a company that still needs to prove commercial adoption, that is not a small update.

They also have the international side of the story with the Saudi Arabia deal and potential Israeli approval. Any real progress there could add fuel because the stock is already priced like expectations are pretty low.

That said, this is definitely not a clean balance sheet story.

The risk is dilution. The company has already raised money through a discounted direct offering, and the going concern language is still a real issue. Revenue is still low, and they may need more capital if sales do not ramp fast enough.

There is also the fiduciary duty investigation headline from June 5, which could keep some pressure on sentiment until there is more clarity.

Why it can rip:

Nasdaq compliance regained, VA contract, possible international expansion, and the stock is still sitting near depressed levels.

Why it can tank:

Going concern risk, dilution risk, weak revenue base, and legal/investigation noise.

For me, this is a high-risk biotech watchlist name, not a “safe” trade. The setup is cleaner than it was a few weeks ago, but the next move probably depends on whether Symvess starts showing real commercial traction.

Source / filings: wiseek.ai/ticker/huma/

3

3

5

845

RT @humacyte: There are clear unmet needs in AV Access for Women.1,2

Join leaders in vascular innovation at the Women in Vascular Surgery…

7

GrumpyGigDriver 🇺🇲🇺🇸🔞💸🎲🏈🎆🎇🧨✨ retweeted

Jun 7

Every time I see this picture it makes me question whether Trump is trying to finally get something off his chest! 😂😂

98

56

242

5,777