Holding my own NUTs

Joined December 2020

- Tweets 1,714

- Following 103

- Followers 64

- Likes 5,407

46 Photos and videos

Sac money bye bye #PulseChain

11

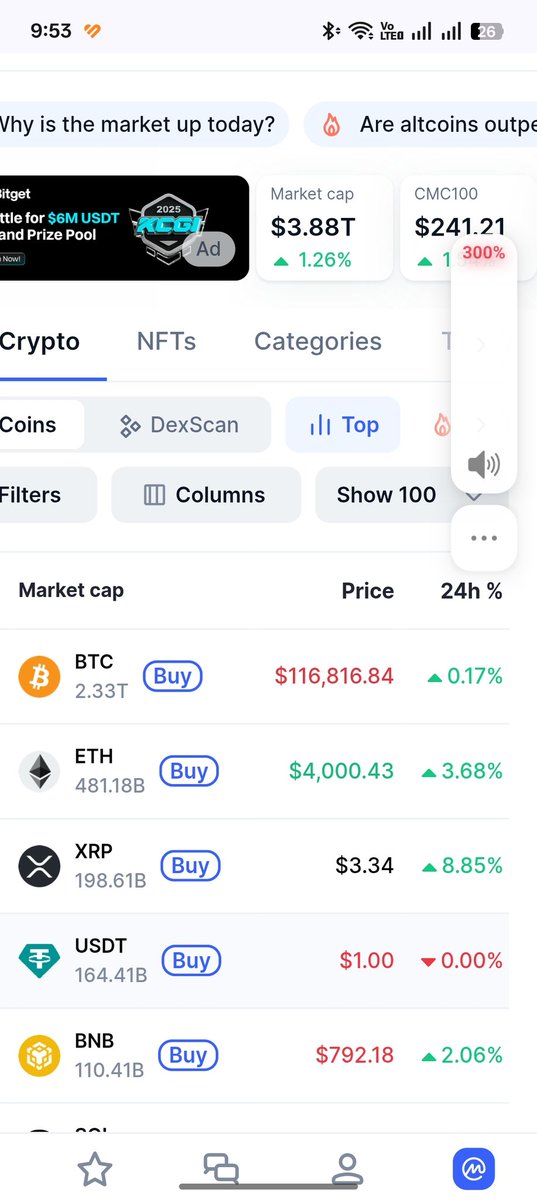

He is accumulating $BTC. That's why.

1

79

I am BULLISH

23 Oct 2025

Retweet this tweet if your bullish on PulseChain

Lets see if this tweet can get a 555 RTs

1

20

Butt hurt to see all major crypto have already 2x their price from lowest ...except #PulseChain core coins. Extreme experience I must say. But gonna hold on until the end of the cycle.

26

Awesome if it executes. $pDAI is BULLISH.

27 Sep 2025

pDAI & COLLATERAL - how it works - my understanding 🧵

- how much collateral is needed?

for the L2 model, you don’t need collateral equal to circulating supply, because there’s no 1:1 redemption line. instead you need just enough credible locked value to convince arb bots and traders they won’t get rugged. coverage ratio targets 150–250% of the active float that’s re-minted on L2, not the full dirty 44B supply. That’s why locking L1 float is essential (it shrinks the denominator)...which is what we are seeing built.

- where will the collateral come from?

> OA bags / founder assets: PLS, PLSX, HEX, other Pulse-native tokens

> ETH, WBTC, etc. that can be deposited cross-chain (depends on bridge trust...@LibertySwapFi)

> validator staking returns, PulseLend lending pools, LP fees. These increase the collateral buffer over time

- how does it hold against millions/billions withdrawn at once if that were to occur?

users can’t line up at the vault and demand $1 collateral. that firehose doesn’t exist. they can only sell into pools. so, if a billion pDAI is dumped (i dont think that would happen):

1. it pushes price down on one chain.

2. arb bots buy discounted pDAI, route it cross-chain, and resell or lock it, earning the spread.

3. fees spike automatically (deviation fee curve), making further selling more costly.

4. treasury yield bot profits accumulate, reinforcing reserves.

collateral is never sold out to meet redemptions. It just sits locked, proving over-collateralization.

3

85

#Pump fun coin is strong enough to have bounce to its ICO price. In fairness to #PulseChain, it did 2x SAC price

at the wrong time. Did not sustain the momentum. Still cheap DCA . NFA

2

79

Tic tic.. countdown timer which did help #PulseChain pumped to half Sac? LibertySwpa, or @RichardHeartWin tactical electronic devices and pump.tires? See it's obvious, #pDAI will be successful because fudded by RH. NFA.

1

49

Buy #PLS . It's ridiculously CHEAP $500 is approximately 10,000,000 PLS.Also #pDAI. Ignore @RichardHeartWin warning about it.

1

28

In crypto, many blindly believe in founders and then went on to get rekt. Exception is Vitalik. The rest pure garbage. I pity #PulseChain Sac people. If only they DCA like I still do, it feels better. @IvanOnTech is really having a great time laughing at us. Well he has millions.

21

Electronic devices that @RichardHeartWin sent for free have not made an impact for #PulseChain. People including me have rolling our eyes on different crypto platforms already had their 3x pre bullrun. Men crypto community really Hate and don't support this. It's a 🤣 🤣🤣

1

1

37

People who sac are feeling bitter. #HEX was a one hit wonder. I Never invest in it. Just DCA both #pDAI, #PLS and #PLSX. WAITING FOR PRICE DISCOVERY. Not expecting any BIG X's. Unless @RichardHeartWin do something, #PulseChain will not be as good.

4

95

#PulseChain holders this is the thing we have been waiting for...BULLISH

1 Sep 2025

It's funny how people don't know how to math. Imagine this example. Math works like $10,000,000 to one person, or $1,000,000 to 10 people, or $100,000 to 100 people, or $10,000 to 1,000 people, or $1,000 to 10,000 people, or $100 to $100,000, or $10 to 1 million, or $1 to 10M...

2

41

This is a thing... if #pDAI is stupidly worthless, why bother being rugged? Only noise witnessed on #PulseChain

1

34