The best due diligence on $GME can be found here.

Joined November 2021

- Tweets 2,157

- Following 424

- Followers 2,287

- Likes 12,407

433 Photos and videos

Pinned Tweet

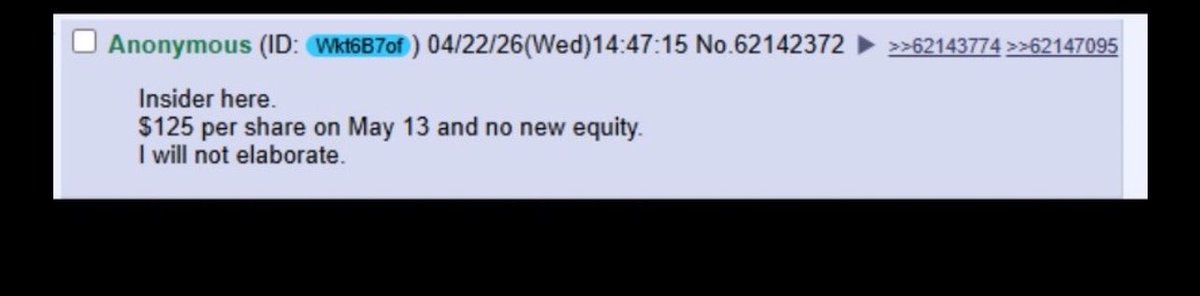

IS $125 ALL-CASH WITH NO NEW $GME EQUITY ACTUALLY POSSIBLE?

There is a 4chan post floating around:

"Insider here. $125 per share on May 13 and no new equity. I will not elaborate."

Wrong date. The bid landed May 3, not May 13. Anonymous. Zero credibility.

But the claim stuck with me.

Not because I believed the post, but because I wanted to know if it was even structurally possible.

So I went to the filings.

And this path could explain a lot.

——————

THE LINE NOBODY READ

@ryancohen filed the offer May 3. Everyone focused on the rejection. Almost nobody read the funding line.

"Cash and liquid investments on GameStop's balance sheet, and third-party equity and debt financing."

Third-party equity.

Not GameStop equity. Third-party equity.

CNBC asked him how he'd pay for it. He kept saying "it's on the website." They laughed.

He wasn't wrong. It was right there.

——————

THE MATH

He already has claim to ~9% of eBay.

So the bill isn't $55B.

It's the other ~91%: about $50.5B.

Balance-sheet cash: ~$9B.

But that understates it.

GME holds ~46.6M warrants outstanding at a $32 strike.

If the stock rips on a deal announcement, those warrants go in the money. Holders exercise.

At $32 that's roughly ~$1.5B flowing into GameStop's treasury.

Plus convertible capacity, marketable securities, and the Bitcoin he's said he'd deploy.

Realistic GME-sourced cash: ~$11–12B.

TD debt: up to $20B. But "up to" is a ceiling, not a target.

That leaves an equity gap. Under the announced 50/50 structure, that gap gets filled with GameStop stock.

GameStop's entire market cap is ~$10B.

Funding a multi-billion equity leg at this price means printing the company away at the bottom.

@ryancohen, paid only on market-cap hurdles, no salary, never diluted cheap, would never do that.

So if the stock half doesn't make sense as the plan, what fills the gap?

Go back to the letter. Third-party equity.

——————

THE LINE EVERYONE SKIPPED ENTIRELY

Here's where it opens up.

The bid doesn't say every eBay holder gets 50% cash and 50% stock, take it or leave it.

It says: "50% cash, 50% GameStop common stock, with full shareholder election rights as to consideration type and pro-rata allocation."

Read that slowly:

Full shareholder election rights. Every eBay holder individually chooses - all cash, all stock, or any mix they want.

Pro-rata allocation. The total cash pool is fixed at the aggregate level.

So if everyone elects all-cash and the pool only covers 50%, the elections get pro-rated. You asked for all cash but you get half cash half stock anyway.

If Cohen planned a rigid 50/50 where everybody gets the same split, you don't need election rights. You just force it.

Election rights only exist if the mix can move.

And the mix moves if the cash pool grows.

——————

THE POOL

The election mechanism is already in the offer. It doesn't need to be renegotiated. Doesn't need eBay's board to agree. Doesn't need a new filing.

The 50/50 isn't a structure. It's a cap on the cash pool.

If third-party equity replaces the stock half with more cash, the pool grows. If it grows to cover 100% of elections, every holder who elected cash gets their full election.

Same $125. Same offer. Same filing.

The bid goes from half-cash to all-cash without changing a single word BUT just by filling the pool.

He built the flexibility into the offer on May 3. The mechanism to deliver all-cash was in the first document.

People read "50% stock" and stopped.

——————

WHAT FILLS THE POOL

The third-party equity comes in as preferred stock from an outside anchor.

Preferred counts as equity on the balance sheet which keeps the credit rating intact but it's not common stock.

No dilution. Cohen keeps the votes.

And this isn't a hypothetical instrument. Look at GME's own balance sheet.

~$4.17B in zero-coupon convertible debt. Zero interest. Converts to common only at a premium strike.

~46.6M warrants at $32. Deferred cash that flows in on exercise.

He's already raised billions in capital that funds like cash today and only becomes equity at a higher price.

The instruments already exist. He's already built, tested, and deployed these exact structures at scale on the public markets.

The anchor gets the same package - just bigger and at the holdco level:

- Convertible preferred with a coupon (same as the converts, but with a yield since sovereign capital demands income).

- Warrants at a high strike for equity upside in the combined entity (same mechanic as GMEWS). Both proven.

Both already sitting on the balance sheet as live examples.

——————

THE SPLIT - AND WHY THE ANCHOR IS LARGER THAN TD

Everyone's been assuming ~$20B TD and ~$21B anchor.

That's backward.

TD is a bank. Banks don't want to hold $20B of risk, they want to originate paper and syndicate it out the door.

The less they have to sell, the easier their job. A $12–15B syndication is dramatically easier than $20B, especially near the edge of investment-grade.

TD would prefer a smaller piece.

The anchor is permanent capital. Sovereign funds don't syndicate. They sit for a decade.

A sovereign writing $28–30B of preferred into a moated cash cow at a skeptic's discount is doing exactly what sovereign capital exists to do: deploy size, hold long, buy when others flinch.

So the natural split pulls more toward the anchor and less toward TD:

~$11–12B GME-sourced cash

~$12–15B TD debt

~$28–30B anchor preferred

= ~$51–57B

Leverage drops from the ~9x Moody's flagged to ~4–5x.

TD's condition is trivially satisfied.

Syndication is easy because the debt is small with a massive equity cushion underneath.

That's a Buffett structure. Equity-heavy. Low leverage. Permanent capital.

And a sovereign deploying $28–30B while the bank arranges $12–15B underneath isn't the junior partner filling a gap.

It's the capital partner.

The bank is the service provider.

That's the natural hierarchy.

——————

WHO ENDS UP OWNING WHAT

This is the part that flips the mainstream narrative. Everyone assumes the eBay deal dilutes GME holders. Under this structure it does the opposite.

After close:

eBay holders → gone. Cashed out at $125. Zero ownership.

TD → debt. A creditor. Gets interest. No ownership.

Anchor → preferred. Senior claim, coupon, liquidation preference, warrants at a high strike. Gets paid first and protected. But preferred is not common.

GME holders → the common.

The same shares. No new ones printed.

But now those shares own the residual equity of a holdco that controls eBay's ~$2B in annual free cash flow, GME's assets, the full platform.

With the preferred and debt serviced out of eBay's own cash generation.

Today each GME share owns a piece of a ~$10B cash-box retailer with a declining core.

After close each share owns a piece of the residual equity above all senior claims in a Berkshire-style holdco throwing off real cash.

And the $2B buyback authorized June 2 means the share count could be actively shrinking, so each remaining share owns a bigger piece of a much bigger entity.

Cohen structured this so dilution only happens at the top, never at the bottom.

------------

WHY $125 ALL-CASH ENDS THE FIGHT

All-cash changes everything.

$125 cash is $125. No "what is GME worth" debate. No judgment call.

A fund manager turning down a 25–46% premium in certain cash has to explain that to LPs.

"I believed in eBay management" is a career-ending sentence when the alternative was guaranteed money.

After June 17, Cohen delivers it directly.

Tender offer straight to eBay's owners.

No board permission. Elect cash, get cash.

——————

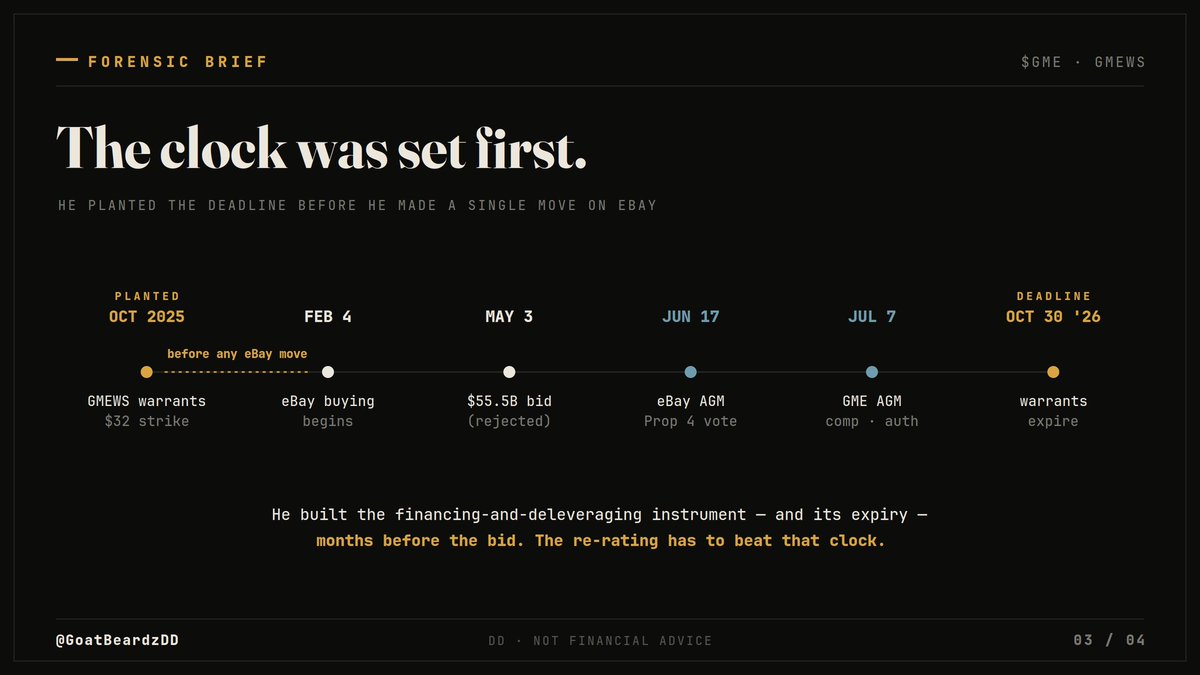

WHY HE ATE THE REJECTION

A fully-financed bid can't be rejected. It has to be engaged. Engagement means price goes up.

A dismissible bid gets refused.

Look at how they refused: "neither credible nor attractive."

They attacked the financing. Not the $125. They left the price standing.

When financing firms up, their objection disappears. And they've already conceded the number by never fighting it.

The rejection locked $125.

Opened the hostile lane.

And kept eBay cheap while he tripled his direct stake: 827,648 to 2,480,467 in five days, into the June 16 ballot lock, funded with cash, the 39M-share conversion untouched.

Direct shares vote. The conversion is held in reserve.

The $2B buyback authorized June 2 says the rest. You don't announce a buyback beside a deal that needs stock issuance, unless you don't plan to issue.

——————

TL;DR:

The 4chan post is garbage. Wrong date, anonymous, no proof.

But $125, no new equity has a real path.

And it was in the filing from day one.

"Third-party equity." Election rights that turn 50/50 into all-cash by filling the pool.

And the cap table:

- eBay holders cashed out,

- TD paid and gone,

- the anchor on preferred,

And finally:

GME common holders owning the residual of a holdco with eBay's cash flows underneath, same shares, no new ones printed, the buyback shrinking the count.

25

14

184

11,726

I am very confident that @ryancohen will speak at the agm, and it will mainly be a victory lap for $GME shareholders.

We are less than a month away!

It will be a historic event!

6

5

74

1,957

There has only ever been two meme stocks @ryancohen has EVER been involved in.

$GME and $BBBY.

Mainstream media says $BBBY was a failed attempt and @ryancohen didn’t know what he was doing.

You’re telling me the owner of the most memed stock who posts memes himself, that’s posted an ENTIRE 425 CAMPAIGN through memes, didn’t know what his involvement meant in BBBY?

You’re telling me he didn’t know his retail base would buy en masse?

HE DID KNOW, AND THERES A REASON.

6

7

92

4,307

This is going to be the first Father’s Day in a long time without the teddy website up 😭

3

13

1,014

IS $125 ALL-CASH WITH NO NEW $GME EQUITY ACTUALLY POSSIBLE?

There is a 4chan post floating around:

"Insider here. $125 per share on May 13 and no new equity. I will not elaborate."

Wrong date. The bid landed May 3, not May 13. Anonymous. Zero credibility.

But the claim stuck with me.

Not because I believed the post, but because I wanted to know if it was even structurally possible.

So I went to the filings.

And this path could explain a lot.

——————

THE LINE NOBODY READ

@ryancohen filed the offer May 3. Everyone focused on the rejection. Almost nobody read the funding line.

"Cash and liquid investments on GameStop's balance sheet, and third-party equity and debt financing."

Third-party equity.

Not GameStop equity. Third-party equity.

CNBC asked him how he'd pay for it. He kept saying "it's on the website." They laughed.

He wasn't wrong. It was right there.

——————

THE MATH

He already has claim to ~9% of eBay.

So the bill isn't $55B.

It's the other ~91%: about $50.5B.

Balance-sheet cash: ~$9B.

But that understates it.

GME holds ~46.6M warrants outstanding at a $32 strike.

If the stock rips on a deal announcement, those warrants go in the money. Holders exercise.

At $32 that's roughly ~$1.5B flowing into GameStop's treasury.

Plus convertible capacity, marketable securities, and the Bitcoin he's said he'd deploy.

Realistic GME-sourced cash: ~$11–12B.

TD debt: up to $20B. But "up to" is a ceiling, not a target.

That leaves an equity gap. Under the announced 50/50 structure, that gap gets filled with GameStop stock.

GameStop's entire market cap is ~$10B.

Funding a multi-billion equity leg at this price means printing the company away at the bottom.

@ryancohen, paid only on market-cap hurdles, no salary, never diluted cheap, would never do that.

So if the stock half doesn't make sense as the plan, what fills the gap?

Go back to the letter. Third-party equity.

——————

THE LINE EVERYONE SKIPPED ENTIRELY

Here's where it opens up.

The bid doesn't say every eBay holder gets 50% cash and 50% stock, take it or leave it.

It says: "50% cash, 50% GameStop common stock, with full shareholder election rights as to consideration type and pro-rata allocation."

Read that slowly:

Full shareholder election rights. Every eBay holder individually chooses - all cash, all stock, or any mix they want.

Pro-rata allocation. The total cash pool is fixed at the aggregate level.

So if everyone elects all-cash and the pool only covers 50%, the elections get pro-rated. You asked for all cash but you get half cash half stock anyway.

If Cohen planned a rigid 50/50 where everybody gets the same split, you don't need election rights. You just force it.

Election rights only exist if the mix can move.

And the mix moves if the cash pool grows.

——————

THE POOL

The election mechanism is already in the offer. It doesn't need to be renegotiated. Doesn't need eBay's board to agree. Doesn't need a new filing.

The 50/50 isn't a structure. It's a cap on the cash pool.

If third-party equity replaces the stock half with more cash, the pool grows. If it grows to cover 100% of elections, every holder who elected cash gets their full election.

Same $125. Same offer. Same filing.

The bid goes from half-cash to all-cash without changing a single word BUT just by filling the pool.

He built the flexibility into the offer on May 3. The mechanism to deliver all-cash was in the first document.

People read "50% stock" and stopped.

——————

WHAT FILLS THE POOL

The third-party equity comes in as preferred stock from an outside anchor.

Preferred counts as equity on the balance sheet which keeps the credit rating intact but it's not common stock.

No dilution. Cohen keeps the votes.

And this isn't a hypothetical instrument. Look at GME's own balance sheet.

~$4.17B in zero-coupon convertible debt. Zero interest. Converts to common only at a premium strike.

~46.6M warrants at $32. Deferred cash that flows in on exercise.

He's already raised billions in capital that funds like cash today and only becomes equity at a higher price.

The instruments already exist. He's already built, tested, and deployed these exact structures at scale on the public markets.

The anchor gets the same package - just bigger and at the holdco level:

- Convertible preferred with a coupon (same as the converts, but with a yield since sovereign capital demands income).

- Warrants at a high strike for equity upside in the combined entity (same mechanic as GMEWS). Both proven.

Both already sitting on the balance sheet as live examples.

——————

THE SPLIT - AND WHY THE ANCHOR IS LARGER THAN TD

Everyone's been assuming ~$20B TD and ~$21B anchor.

That's backward.

TD is a bank. Banks don't want to hold $20B of risk, they want to originate paper and syndicate it out the door.

The less they have to sell, the easier their job. A $12–15B syndication is dramatically easier than $20B, especially near the edge of investment-grade.

TD would prefer a smaller piece.

The anchor is permanent capital. Sovereign funds don't syndicate. They sit for a decade.

A sovereign writing $28–30B of preferred into a moated cash cow at a skeptic's discount is doing exactly what sovereign capital exists to do: deploy size, hold long, buy when others flinch.

So the natural split pulls more toward the anchor and less toward TD:

~$11–12B GME-sourced cash

~$12–15B TD debt

~$28–30B anchor preferred

= ~$51–57B

Leverage drops from the ~9x Moody's flagged to ~4–5x.

TD's condition is trivially satisfied.

Syndication is easy because the debt is small with a massive equity cushion underneath.

That's a Buffett structure. Equity-heavy. Low leverage. Permanent capital.

And a sovereign deploying $28–30B while the bank arranges $12–15B underneath isn't the junior partner filling a gap.

It's the capital partner.

The bank is the service provider.

That's the natural hierarchy.

——————

WHO ENDS UP OWNING WHAT

This is the part that flips the mainstream narrative. Everyone assumes the eBay deal dilutes GME holders. Under this structure it does the opposite.

After close:

eBay holders → gone. Cashed out at $125. Zero ownership.

TD → debt. A creditor. Gets interest. No ownership.

Anchor → preferred. Senior claim, coupon, liquidation preference, warrants at a high strike. Gets paid first and protected. But preferred is not common.

GME holders → the common.

The same shares. No new ones printed.

But now those shares own the residual equity of a holdco that controls eBay's ~$2B in annual free cash flow, GME's assets, the full platform.

With the preferred and debt serviced out of eBay's own cash generation.

Today each GME share owns a piece of a ~$10B cash-box retailer with a declining core.

After close each share owns a piece of the residual equity above all senior claims in a Berkshire-style holdco throwing off real cash.

And the $2B buyback authorized June 2 means the share count could be actively shrinking, so each remaining share owns a bigger piece of a much bigger entity.

Cohen structured this so dilution only happens at the top, never at the bottom.

------------

WHY $125 ALL-CASH ENDS THE FIGHT

All-cash changes everything.

$125 cash is $125. No "what is GME worth" debate. No judgment call.

A fund manager turning down a 25–46% premium in certain cash has to explain that to LPs.

"I believed in eBay management" is a career-ending sentence when the alternative was guaranteed money.

After June 17, Cohen delivers it directly.

Tender offer straight to eBay's owners.

No board permission. Elect cash, get cash.

——————

WHY HE ATE THE REJECTION

A fully-financed bid can't be rejected. It has to be engaged. Engagement means price goes up.

A dismissible bid gets refused.

Look at how they refused: "neither credible nor attractive."

They attacked the financing. Not the $125. They left the price standing.

When financing firms up, their objection disappears. And they've already conceded the number by never fighting it.

The rejection locked $125.

Opened the hostile lane.

And kept eBay cheap while he tripled his direct stake: 827,648 to 2,480,467 in five days, into the June 16 ballot lock, funded with cash, the 39M-share conversion untouched.

Direct shares vote. The conversion is held in reserve.

The $2B buyback authorized June 2 says the rest. You don't announce a buyback beside a deal that needs stock issuance, unless you don't plan to issue.

——————

TL;DR:

The 4chan post is garbage. Wrong date, anonymous, no proof.

But $125, no new equity has a real path.

And it was in the filing from day one.

"Third-party equity." Election rights that turn 50/50 into all-cash by filling the pool.

And the cap table:

- eBay holders cashed out,

- TD paid and gone,

- the anchor on preferred,

And finally:

GME common holders owning the residual of a holdco with eBay's cash flows underneath, same shares, no new ones printed, the buyback shrinking the count.

25

14

184

11,726

Fuck this one took a while to revise and format.

Does anyone have the teddy pic of the socks spelling out cash?

2

25

1,004

Good morning $GME squad and happy weekend!

Writing a DD atm will post soon. It all stems from the question is this leak true?

Is it even possible?

My research shows that it is. Stay tuned.

7

3

85

4,744

I got the idea for this from the latest drops for the video games Dragons dogma 2 and kingdom hearts 4.

There were leaks that were dismissed as not true months ago and many parts of them are not but the general gist did come true for both these things.

And that’s the thing with leaks, they’re not solid info always but carry a measure of truth behind them.

I don’t think May 13 was the date, BUT what if it is all cash? Remember the socks on the Teddy books? Is there a way for it to happen?

10

955

Jun 13

Oh my godddd I’ve been saying $GME never announced the SWF.

That’s false. It says it explicitly in the bid letter.

The deal is 50% cash 50% stock.

The cash will be from gamestop itself, debt financing (TD) AND third party financing (SWF).

5

4

73

5,608

Jun 13

Maybe just a crazy night but someone send me the 4chan screenshot about the eBay bid PLEASE.

I think there’s also a reason why they took the Teddy website down. The clues become very apparent.

10

1

92

12,918

Jun 13

$GME filed the bid for $EBAY May 3rd.

They did this knowing they would clear HSR June 3rd, knowing it would be too late for the eBay AGM.

@ryancohen then chose to buy shares directly as soon as HSR cleared and now has actual ownership on top of the options.

This next week will be explosive!

@ryancohen has been sequencing for just this.

The plan isn’t apparent but the execution IS.

6

8

120

8,054

Jun 13

Unless @ryancohen converts a lot of his position soon, I think it’s safe to assume this first bid was an excuse to put eBay’s board on blast.

4

1

45

3,728

Jun 12

CEO @ryancohen is playing a very interesting game with the timing of the conversion of his position…

It seems like $EBAY voting for prop 4 is what he’s waiting for, he’s slowly started to convert before the meeting…

10% is the number that matters, the position is just under that and actual ownership far below.

eBay themselves are setting up solicitors to help defend against activists, and it seems like time is slowly pinching his ability.

But let’s say that his time horizon is a bit longer but less than July 7th.

What could he do within that time frame?

7

1

96

8,676

Jun 12

Not a great trading day for $GME and its warrants.

Whats interesting to me though is the fact that on the monthly, it looks like the earnings did set a strong floor.

8

37

2,227

Jun 12

What the fuck again?

Jun 12

12

2

99

6,588

Jun 12

This is a graphic I made to try to share the $GME timeline, this isn’t a one month thing.

It’s been at least from May - July like we all knew.

The clock was set before he started.

2

6

49

4,548

Jun 12

GOOD LATE MORNING $GME SQUADDD!

It seems all quiet on the $GME front for now.. until Wednesday!

- $EBAY agm takes place ~5 days from now…

- the largest retail IPO, $SPCX is going live today, I’m sure @ryancohen is watching closely….

- planning on releasing a DD over the weekend, going to take my time to write this one so it’s substantial !

Oh and Teddy is still down, and it’s been 10 days!

Enjoy your coffee, even if it’s cold!

12

2

68

3,154