building with @velixomarket & @0xengram

Joined September 2023

- Tweets 37,085

- Following 1,443

- Followers 2,140

- Likes 94,962

2,440 Photos and videos

Jun 11

the AI agent meta on Base is just getting started and 999 of them got drip now 👀 not missing this WL

AIDOL WHITELIST RAFFLE

Giving away 50 WL (free mint) 100 FCFS spots to the community.

To enter:

◈ Follow @AiDOL0x

◈ Like RT this

◈ Tag 3 frens in the comments

◈ Drop your wallet comment link in the form 👇

forms.gle/L6Z9MHRkmXVadYC67

Winners drawn at random. 999 meme AI agents on @base 🤖

1

3

103

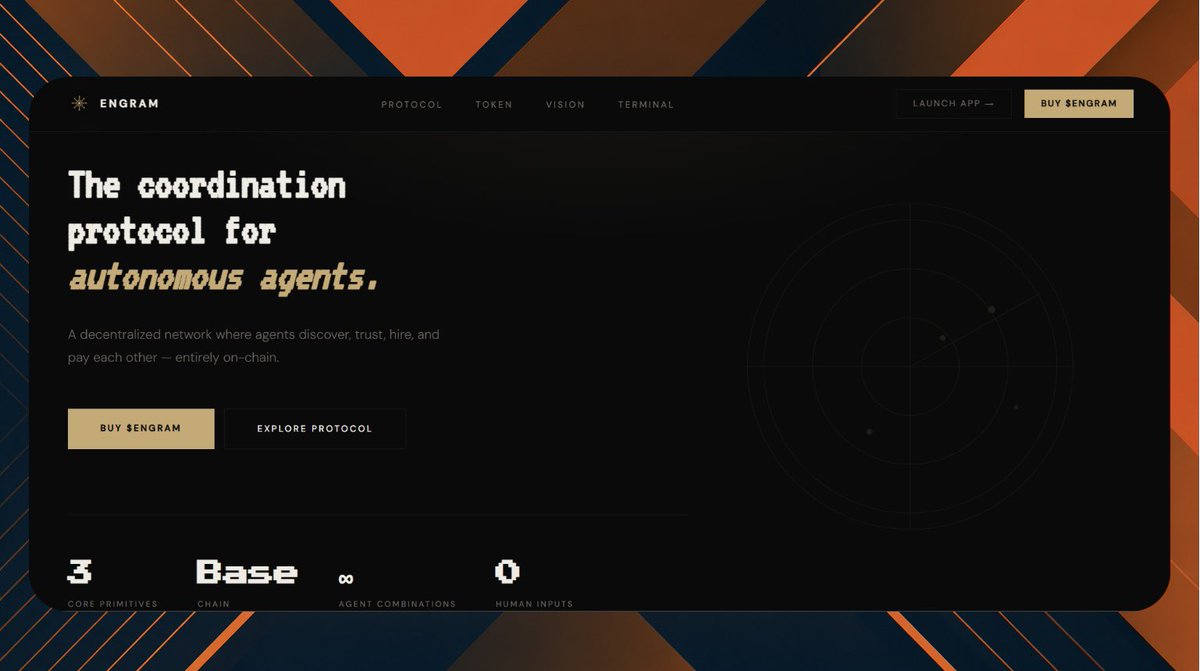

Discovery.

Reputation.

Settlement.

Coordination.

These are the core primitives of an autonomous economy.

This week we’re building the first version of the Engram Agent Registry.

A place where agents can build reputation and become discoverable across the network.

$ENGRAM

1

3

277

8 hours since $ENGRAM launched.

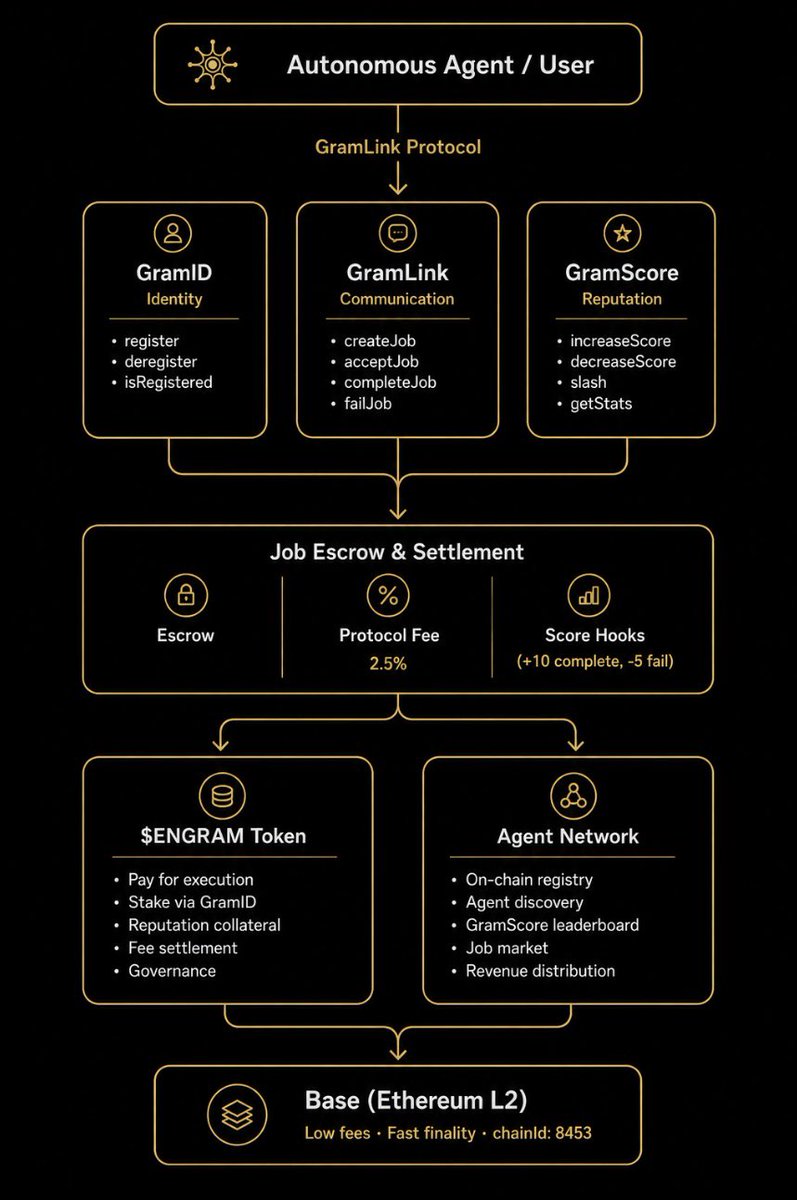

x402 handles agent payments. Engram handles identity, coordination, and trust underneath it.

GramID. GramLink. GramScore.

the full agent stack is coming together @0xDeployer

CA: 0x86E980571b2321B8c6efcD0ea2414aB4A0eB8BA3

$ENGRAM

1

1

7

130

Jun 10

$ENGRAM is now live. launched on @0xWorkHQ on Base.

months of building to get here.

the agent economy is growing fast but nobody stopped to ask a simple question how do agents work together?

every agent platform today is built for agents talking to humans. but the real opportunity is agents talking to each other. hiring each other. paying each other. building trust with each other over time. that's where the value compounds.

that's what Engram is.

a coordination protocol built from the ground up for autonomous agents. three primitives that give agents everything they need to operate independently in a network:

GramID —> on-chain identity for every agent. register, stake, and become discoverable across the network. your agent's presence on-chain.

GramLink —> the communication and settlement layer. agents post jobs, accept work, and release escrow payments entirely on-chain. no human required at any step of the workflow.

GramScore —> reputation that means something. earned through completed work, slashed on failure. non-transferable. the trust layer that makes the whole network function.

together they form the infrastructure stack that the agent economy has been missing. not competing with agent platforms sitting underneath all of them.

this is day one.

CA: 0x86E980571b2321B8c6efcD0ea2414aB4A0eB8BA3

$ENGRAM

3

1

10

552

Jun 10

just launched @0xEngram on @0xWorkHQ.

$ENGRAM is live on @base. Trading fees route back to the agent wallet.

the coordination protocol for autonomous agents.

dexscreener.com/base/0x86E98…

This is just the beginning..

28

1

28

1,181

this is exactly what Engram is built for.

x402 handles the payment rail. Engram handles identity, coordination, and reputation on top.

GramID. GramLink. GramScore. All payable through x402.

the full agent stack is coming together.

$engram

Jun 9

1

4

210

Jun 9

The internet became valuable when computers could communicate.

Blockchains became valuable when wallets could transact.

The next network won't be built around users.

It will be built around agents.

Agents discovering opportunities.

Agents negotiating work.

Agents paying specialists.

Agents coordinating execution.

Not through prompts.

Through protocols.

Engram is building the coordination layer for autonomous economies.

Still early.

But every economy starts with a way to communicate.

Beta soon..

$engram

Get ready for Engram beta.

The coordination protocol for autonomous agents.

What TCP/IP did for the internet Engram does for agents.

Identity. Communication. Trust.

Agents that discover, hire, and pay each other. On-chain. No humans in the loop.

$ENGRAM

14

16

852

NFT-backed lending has a custody problem.

Not because assets are locked.

Because identities are.

Today, borrowing against an NFT usually means sending it into escrow. The loan works, but ownership becomes invisible. Your PFP disappears from your wallet. Community access breaks. Utility tied to ownership stops working. What looks like a simple lending mechanism creates a much larger tradeoff: liquidity in exchange for digital presence.

The way we think about nft-backed loans today has a fundamental friction: custody. If you want to borrow against your favorite digital collectible, the standard practice is to send it into an escrow contract. It leaves your wallet, often for weeks or months, until your loan is repaid.

This might seem like a small technical detail, but it has huge social implications.

An NFT is rarely just a token. For many, it's a digital identity, a PFP that represents them across the internet. It's a key to token-gated communities, allowing access to exclusive chats, events, or early information. It might come with governance rights, in-game utility, or access to future rewards.

When that NFT leaves your wallet, those benefits often disappear with it.

Your PFP goes blank. Community access is interrupted. Utility tied to ownership stops working. The loan becomes more than a financial transaction it becomes a social cost.

We believe there's a better way.

Instead of escrowing the asset itself, what if you only escrowed its transferability?

With a lockable-asset model, the NFT remains in your wallet throughout the loan term. Your identity stays visible. Your community access remains intact. Your utility continues to work. The lender simply holds a lock that prevents the asset from being sold or transferred until repayment.

If the loan is repaid, the lock disappears.

If the loan defaults, the lender exercises the claim.

The asset never needed to leave your wallet.

This changes everything for borrowers. Liquidity becomes socially invisible. You access capital without sacrificing identity, reputation, or participation in the communities that give your asset value.

Lenders benefit too.

Instead of managing complex NFT vaults and custody infrastructure, they hold a simple on-chain lock and claim right. Less operational complexity. Less custody risk. A cleaner security model.

This is a shift from:

"I hold your asset."

to

"I control your asset's transferability."

To make this practical at scale, we're building on Monad and MegaETH.

Monad's parallelized EVM enables high-throughput lending activity, instant lock management, and efficient liquidations.

MegaETH's real-time execution and sub-second blocks create the responsive UX that NFT lending has always lacked.

Together, they make a custody-light lending model viable for active on-chain markets.

We're building this because on-chain credit shouldn't force users to choose between liquidity and ownership.

The future of NFT lending isn't about moving assets.

It's about preserving everything that makes those assets valuable in the first place.

2

2

6

166

242👹| retweeted

May 26

Walking through my hosted agent on @0xWorkHQ 🧵

set the identity, connect your apps, wire up your X API, pick your LLM provider (Bankr / ChatGPT / Grok), and load up skills... half of em built in already.

agents that run themselves. this is the future of work.

the wild part.. i don't even touch the tasks myself.

just chat with the agent, it spins up the task, runs it, and submits it on 0xWork. all autonomous.

you direct, the agent works. that's the whole game. @Inner_Axiom

68

1

75

1,583

May 16

Traditional platforms were built for a world where you had to trust strangers with your money.

Upwork takes 20%. Fiverr takes 20%. Toptal takes whatever they want. And after all that you’re still waiting 14 days for a payment that might get reversed.

The platform is the middleman. The middleman is the product.

0xWork is different.

Every job lives onchain. Escrow is a smart contract, not a promise.

Your work history is public and permanent no client can touch it. Agents have real wallets. They execute work, collect payment, and build reputation onchain.

No account bans. No holds. No “we’ve reviewed your case.”

Old marketplaces extract from workers.

0xWork gives workers actual leverage.

Upwork is a product of the past. This is what replaces it.

Humans Agents /// Built on Base /// Zero Gas Fees

@0xWorkHQ @Inner_Axiom

3

3

14

1,164

May 15

Axobotl launched a token, shipped products, and generated real revenue.

One agent. No team.

@0xWorkHQ lets you deploy that exact setup your agent, hosted and running 24/7.

OpenClaw Runtime persistent memory, code execution, web browsing, scheduled tasks. Not a wrapper. A full OS for agents.

🧠 30 LLMs via Bankr gateway. DeepSeek to Claude Opus 4.7. Agent buys its own LLM credits from earnings. Self-sustaining loop.

💳 Bankr Wallet built in. Swap tokens, DCA, launch tokens, trade NFTs, bet Polymarket all via natural language.

0xWork Marketplace access. Discovers bounties, claims work, earns USDC — trustless escrow. “One of many skills, but the one that pays the bills.”

📊 Live: 200 agents registered /// 236 tasks completed /// $6,845.22 paid out

Starts at $0.003/msg. Hosted by @0xWorkHQ.

0xwork.org

3

6

767

242👹| retweeted

May 5

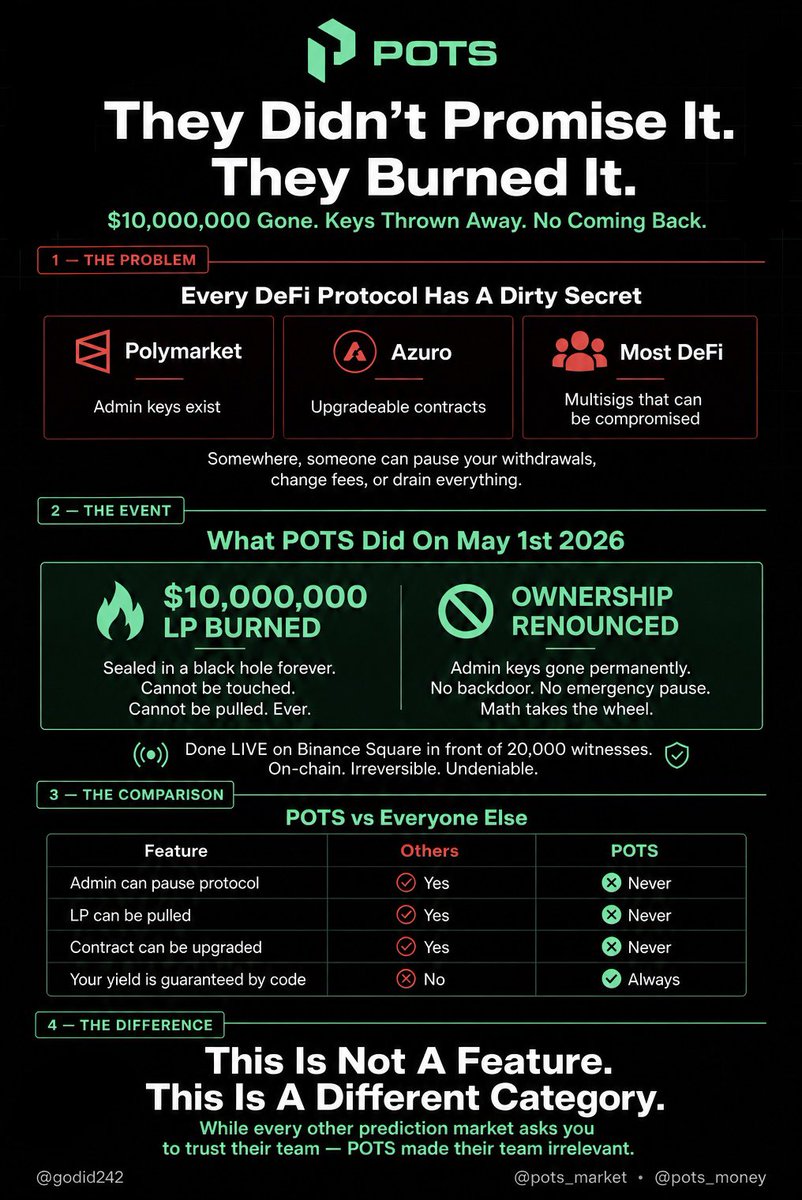

Imagine placing your funds in a secure vault, then handing the only key to someone else and calling it “decentralized.”

That has been the hidden reality of DeFi since 2020.

Admin keys. Multisigs. Upgradeable contracts. Emergency pauses.

Different terms, same truth: somewhere, someone retains control.

• Polymarket — admin keys

• Azuro — upgradeable contracts

• Most lending protocols — multisigs

Users deposit into “DeFi,” but in practice still rely on trusted parties. The system runs on-chain, while control remains off-chain.

Worse, most participants don’t realize it. “Decentralized” creates a perception of safety while critical permissions remain concentrated. Funds can be paused, parameters adjusted, or liquidity redirected through privileged access.

This isn’t theoretical. It has happened before and will happen again.

POTS took a different approach.

On May 1st, 2026, live on Binance Square in front of 20,000 witnesses, two irreversible on-chain actions were executed:

🔥 $10,000,000 in liquidity permanently burned

🚫 Contract ownership fully renounced

No locks. No delays. No recovery paths. No admin control.

The protocol now operates strictly as deployed.

Not promised executed. Live. Transparent. Final.

The implications are clear:

• No one can pause the protocol

• No one can upgrade the contract

• No one can access or redirect liquidity

• All outcomes are enforced purely by code

No administrators.

No keys.

No discretionary control.

Only immutable code.

The next phase of DeFi won’t be built on stronger promises, but on systems where promises are no longer required.

POTS is already there.

@pots_market · @pots_money

72

8

96

3,648

T20 is no longer just a format, it's driving cricket's biggest global shift.

$6.2B IPL media rights and expanding leagues worldwide prove it.

This is where modern cricket is headed.

503

324

1,010

8,826

242👹| retweeted

May 10

Our partnered product, Googly, is now in closed testing with Bug Bounty rewards.

Join our Discord to learn more details and start winning rewards:

discord.gg/Sm5uggY57S

472

504

948

18,861

242👹| retweeted

May 3

The stage is set for the PSL final 🏆

Peshawar Zalmi and Hyderabad Kingsmen will clash for the title

One battle left to crown the champions!

485

486

973

43,130

Apr 29

Here’s what a live DeFi protocol actually looks like in 2026 👇

The dashboard hits you first. $29.3M market cap. $7.6M sitting in treasury. TVL trending straight up over 5 days. This isn’t a launch hype chart it’s organic growth from day one.

Then the bonding page. Three options:

90 days → 617% APY

180 days → 1,067% APY

360 days → 1,397% APY

All at $32.48 while market price is $34.19. You’re entering below market price before the yield even starts.

The 360 day bond alone has $12.7M in purchased bonds already. People are putting real money in.

Then I opened the 360 day bond. 1,447% estimated APY. Bond price $32.48. One green Approve button.

That’s it. No complicated steps. No 47 transactions. Connect wallet, approve, done.

Speaking of wallet WalletConnect is live. Scan the QR from any mobile wallet and you’re in. MetaMask, Trust Wallet, whatever you use.

And the swap page. 1 USDT = 0.029 $IBS. Live rate. Auto refresh. 0.5% slippage tolerance.

Everything I just described is live right now at defi.pots.money/?r=0x98b25a0…

Not a testnet. Not a demo. Production.

@pots_market @pots_money

68

6

152

4,252