Real Estate Investor, Car Enthusiast, 5M Subs on YouTube. Newsletter - grahamstephan.substack.com Insta - bit.ly/gpstephan

Joined March 2009

- Tweets 3,780

- Following 168

- Followers 212,234

- Likes 12,434

1,149 Photos and videos

Pinned Tweet

12 Oct 2023

Hey everyone!

Here's my weekly email recap of all things money – from the stock market to real estate to personal finance – with research and actionable ideas

I'd love for you to join, and it's totally free :)

grahamstephan.com/newsletter

113

71

268

333,297

Jun 1

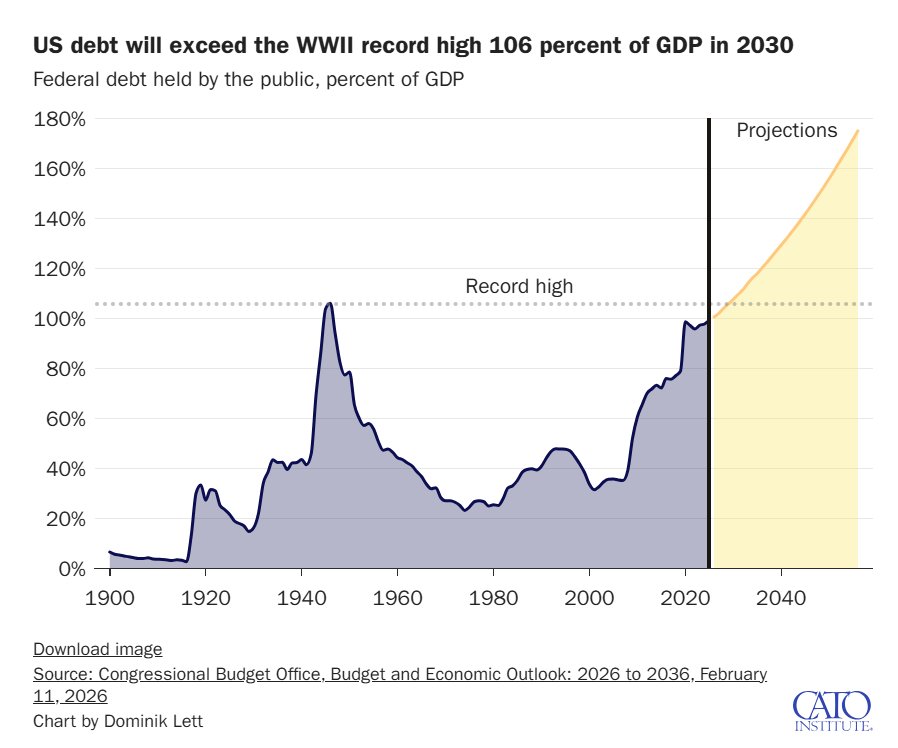

How do you erase a massive national debt without raising taxes or defaulting? You quietly tax the savers.

It’s a strategy called Financial Repression. The Fed used it 70 years ago, and now they're planning to use it again. Here's how it works:

After WWII, US debt had skyrocketed to 106% of GDP. The government couldn't slash spending without crushing the post-war economy, and hiking taxes further was a political death sentence. So, they chose a third option: Shrink the debt with inflation.

Here is how the playbook worked:

1. Cap the yields: The Fed pegged long-term government bond yields at a low 2.5%.

2. Let inflation run: When post-war price controls lifted, inflation quickly peaked past 10%.

If you were a disciplined citizen holding a government bond, you got your guaranteed 2.5% interest. But because of soaring prices, your real purchasing power was eroding by roughly 6% a year.

The government effectively repaid yesterday's debt with today's dollars that were losing their value. Without this strategy, the system might have collapsed. But by 1974, this silent plan dragged the Debt-to-GDP ratio all the way down to 23%.

America's post WWII boom is often seen as an example of miraculous economic growth. But more than growth or responsible budgeting, it's the massive wealth transfer from the public that saved the system.

Why is this relevant now? For the first time since WWII, Debt-to-GDP ratios are hitting nearly the same levels. Kevin Warsh has been hinting that the new Fed will be a more disciplined one, and financial repression is always a silent but powerful tool.

In today's Substack post, I talked about how to see this coming and what you can do to protect your wealth once it kicks in. I'll drop the link in the comments.

29

10

157

23,309

Jun 1

The silent plan to erase the national debt: Full post – grahamstephan.substack.com/p…

1

18

6,125

May 27

Finally saw the movie Obession. Holy crap.

It was insane. The entire theater was completely sold out on a Tuesday night, all show times. I haven’t seen movie crowds like this since I was a kid. Incredible movie, and incredible that this was done on a $750k budget. Go and see it!

34

107

2,191

103,031

May 26

The Federal Reserve is about to stop holding the market's hand.

For 14 years, we have lived in an era of Forward Guidance, a world where the Fed tells us what they are thinking months in advance, to keep stocks stable. Kevin Warsh is about to end that.

His 4-point blueprint for a regime change is a deliberate move to make the Fed a black box again. Here is the breakdown of what is actually happening:

1. The Liquidity Withdrawal: Warsh wants to aggressively shrink the 6.7 trillion dollar balance sheet. When the Fed stops buying bonds and mortgage-backed securities, it removes the artificial floor under the housing market. It forces mortgage rates to be determined by reality instead of money printing.

2. Ending the Dot-Plot: The Fed holds eight meetings a year and releases a "Dot-plot" – a roadmap of where rates are headed. Warsh wants to cut that to 4 meetings and delete the dot-plot. By surprising the market, he hopes that investors will price risk on their own. Expect jagged, volatile swings to become the new normal.

3. The Accounting Shift: This is the most controversial move. By switching to a "Trimmed Mean" inflation gauge, the Fed can ignore extreme price spikes in energy or food. It is a way to make inflation look lower on paper, providing the cover needed to justify rate cuts even if your grocery bill is still climbing.

4. The End of Sacred Independence: Warsh believes independence must be "earned" by hitting targets. The Fed will shift from being a neutral referee to a performance-based agency. If the Fed is under pressure to hit specific goals to keep its autonomy, the temptation to prioritize short-term market wins over long-term stability becomes massive.

The bond market is already calling the bluff. Long-term yields are at 20-year highs because investors see the friction between a new Chair who wants to cut rates and an old Chair (Powell) who is still sitting at the table refusing to leave. The new blueprint isn't about lower rates, but rather about a Fed that is changing the way Americans invest for the future.

I did a deep dive into who the biggest winners and losers will be under this new regime in this week's Substack post. I'll drop the link in the comments.

10

7

112

18,880

May 25

This is Ferrari's new humiliation ritual.

They'll make you buy this $640k EV (that looks like a melted Cybertruck had a baby with an iPad) before you can get on the list for the real Ferraris you actually want.

Welcome to the new 'pay to play' era at Maranello.

May 25

Never thought I'd say this about a Ferrari, but this is one of the ugliest EV designs ever, and it can be all yours for $640,000 lol

78

30

677

79,522

May 20

Google is now prioritizing AI results instead of user-driven websites. Most people seem to be unhappy with this. But I remember when Apple removed the headphone jack, and back then, everyone was equally upset. Today, no one bats an eye.

Genuinely curious - it seems like this was coming sooner or later. No one says “hold on let me google it” anymore…they say “hold on let me ask AI.” Google search is used less as less, it’s only a matter of time until everything is searched and found through AI.

To me, this change was going to happen at some point. It just happened to be starting now. Am I wrong to think this way? Is there something I’m missing?

96

12

205

35,418

May 18

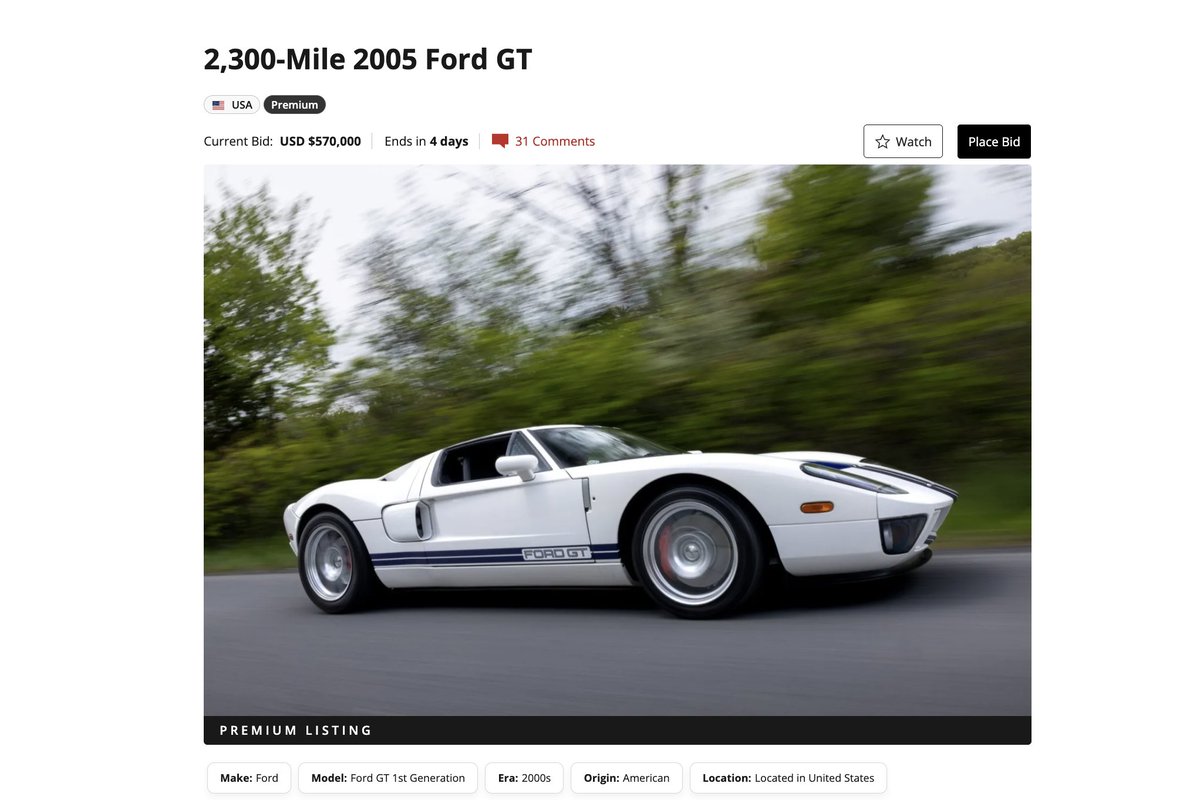

Fun Fact: These 2005-2006 Ford GT's have tracked nearly the same returns as the SP500 since 2021.

25

11

388

24,809

May 12

When you finalize a huge deal, tell no one. Not your spouse. Not your children. Not your friends. Not even your parents. Celebrate internally, maybe take the weekend off, and then get back to work.

May 12

This tweet single-handedly made Anthropic and OpenAI scramble and issue full statements on secondary stock deals.

$500B of paper value just got wiped out overnight.

18

17

518

103,318

May 11

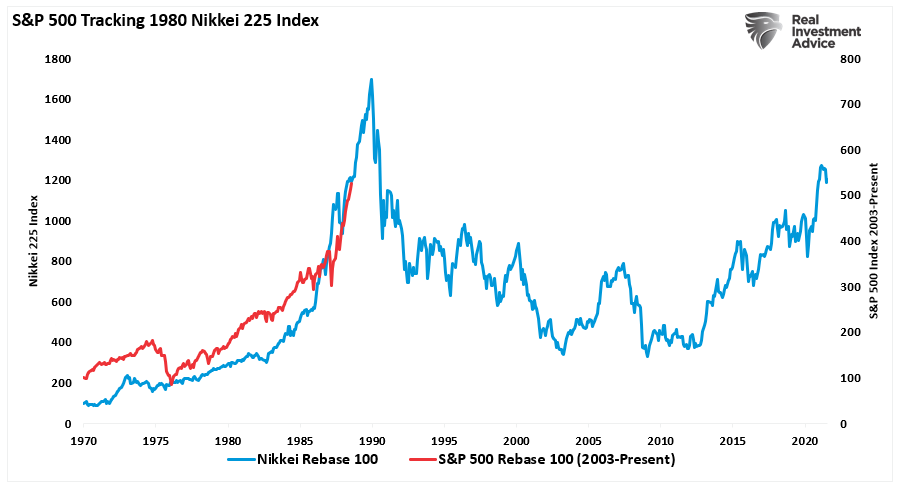

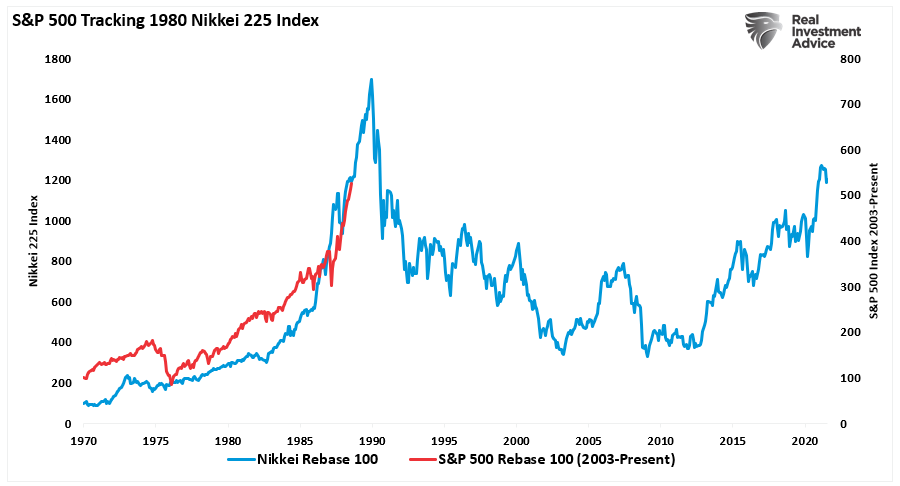

The U.S. stock market is tracking the 1989 Japan bubble. When that bubble burst, their market didn't recover for 40 years. So what's going on?

In the 1980s, Japan saw a rapid surge in stock and real estate values. It was called "The Everything Bubble."

The math was simple but dangerous:

- Low interest rates flooded the market with cheap money.

- Companies used that money to buy stocks.

- Rising stock prices increased corporate valuations.

- Higher valuations let those companies borrow even more money to buy even more stocks.

Real estate in Tokyo was so expensive that the grounds of the Imperial Palace were worth more than the entire state of California! It was a perfect circle that worked till it didn't.

In 1989, the market crashed 50 percent. Then it dropped a bit more. It did not fully recover for almost 40 years.

Today, the S&P 500's trajectory looks the same.

We see the same pattern of cheap money, massive debt, and a belief that prices can only go up. But there is one major difference this time: AI productivity and companies with real cash flows.

While Japan was fueled by a real estate frenzy, the U.S. is fueled by companies like Nvidia and Microsoft generating massive cash flow. The question is whether that productivity can grow fast enough to outrun the debt.

At the same time, we're also face a shrinking workforce and rising social costs. How will these forces work together?

The goal is not to predict a crash but to prepare for any eventuality.

I broke down the full data on the great melt-up and what it means for your portfolio on my Substack. I'll drop the link in the comments.

121

31

397

117,578

May 1

If this tweet has exactly 1 like in 24 hours I’ll give that person $10,000,000

If this tweet has exactly 1 like in 24 hours I’ll give that person $1,000,000

75

6

746

94,329

Apr 30

Hypothetically - How easy would it be for someone to manipulate these odds for exposure?

Like let’s say someone places a $50K wager on her winning, boosting her odds, and then she gets the equivalent of $1M worth of additional marketing exposure from everyone talking about it?

Apr 30

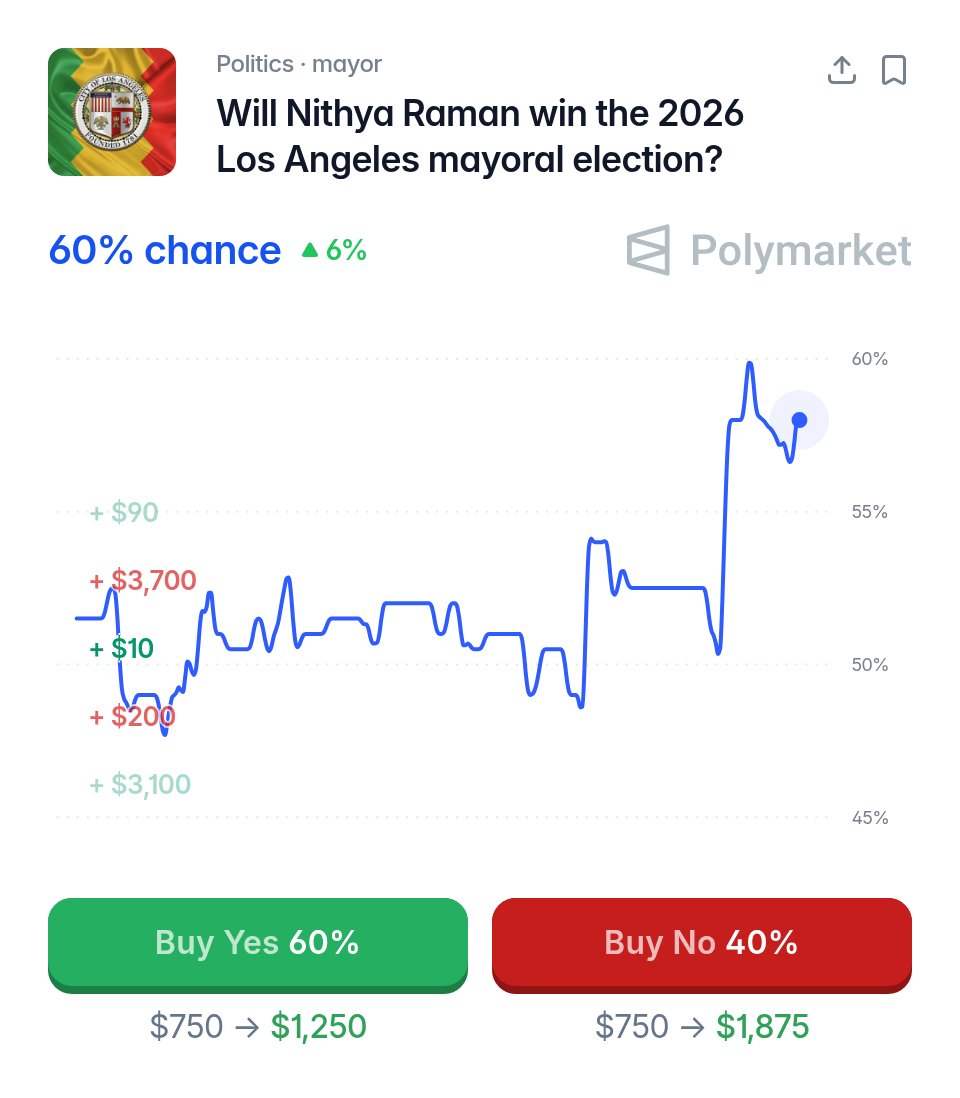

JUST IN: Democratic Socialist Nithya Raman, dubbed "the next Mamdani," is now projected to win the LA mayoral election.

60% chance she leads the City of Angels.

78

16

398

88,646

Apr 28

For the last 40 years, the safe bet was simple: Put 100% of your money into the US stock market and wait. It worked because the US had an "exorbitant privilege." This is changing, and so should your investment plan.

As we move into 2026, this is the new reality: The Western alliance now controls just 29.6% of global GDP (PPP), while the BRICS nations have climbed to nearly 45%!

There are five specific mechanisms threatening to bypass the US dollar entirely. These are the "Dollar-Killers" you need to watch:

1. Bilateral Trade Settlements: China, India, and Russia are increasingly skipping the dollar entirely. By settling invoices in native currencies, they bypass US correspondent banks, avoid transaction fees, and eliminate the risk of Washington "flipping the switch" on their assets.

2. BRICS PAY: Think of this as an alternative to SWIFT. If SWIFT is the Western-controlled email system for international banking, BRICS PAY is a competing encrypted service that escapes US control.

3. Strategic Gold Stockpiling: Central banks are currently buying gold at the fastest rate in 50 years, even with prices crossing $5,000 an ounce. Gold is the ultimate neutral asset. It can’t be sanctioned, and it can’t be printed. It is sovereign insurance against a weakening dollar.

4. The mBridge Project: This is perhaps the most sophisticated threat. It’s a blockchain-based framework being tested by central banks in the UAE, China, and Thailand. It allows for settlement of payments in digital currencies in seconds, without ever touching a neutral third party like the US dollar.

5. The UNIT: A proposed digital currency backed 40% by gold and 60% by a basket of BRICS currencies. It’s designed to provide the stability of a hard asset with the utility of a digital one.

If you think this is alarmist, look at what the world’s largest money managers are saying. Vanguard’s 10-year forecast projects US stocks to return just 3.9% to 5.9% annually, while they expect international markets to outperform at 4.9% to 6.9%.

The easy money in a concentrated US market (where the top 10 companies make up 40% of the S&P 500) has likely been made. We are moving from a world where the US was THE superpower to a world where it is A superpower.

To learn more about how to reinvest in this changed world, read today's post on my Substack. I'll drop the link in the comments.

65

16

306

69,249

Apr 28

The US is slipping – Here's how to reinvest. Full post here: grahamstephan.substack.com/p…

1

2

20

7,259

Apr 27

Roughly 220 billionaires reside in California. They employ roughly 10 million people. If a wealth tax passes, everyone with a billion-dollar idea will think twice about whether they want to build that business in California. But that isn’t even the most dangerous part.

When this turns out to raise less money than expected, the bar will be lowered to $100 million. Then $50 million. Then $10 million. Then $1 million. They’ll call it “the millionaire tax.” And since ~80% of the California population isn’t a millionaire, they’ll vote it into existence because “it doesn’t affect them.”

But many of those “millionaires” are providing jobs. Housing. Innovation. Buying products and services. They’re a net economic benefit. If you discourage them from living in California, they will leave. Then it becomes a downward spiral where they have to tax everyone else to stay afloat.

Not saying the system is perfect. But a simpler solution might simply be: spend less money and encourage more people to move back / create a billion dollar idea.

Apr 27

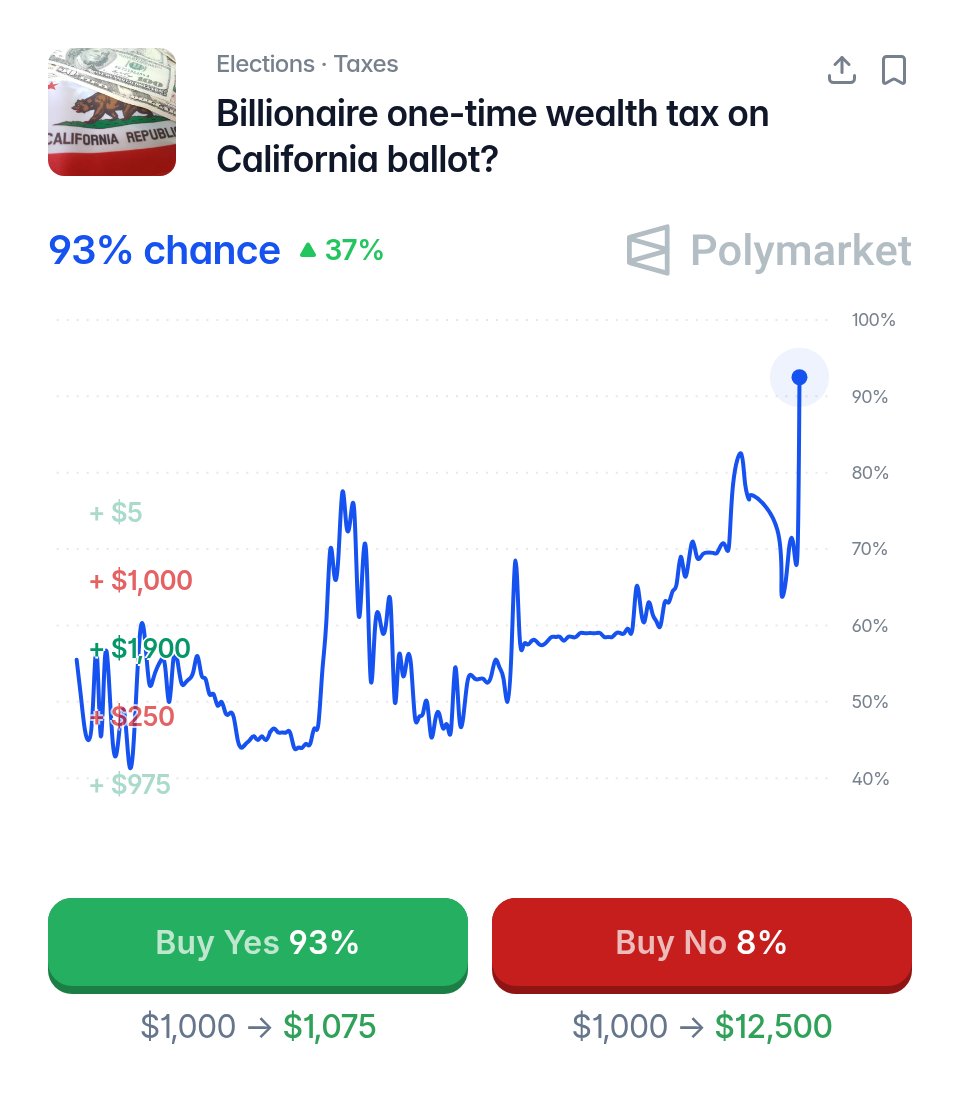

BREAKING: California's one-time "billionaire wealth tax" all but officially confirmed to be on the ballot.

93% chance.

519

477

5,104

928,178

Apr 21

Last week's post about selling my entire real estate portfolio went viral with over 3M views. But a lot of people asked me: “If you’re exiting real estate, where is that money actually going?”

It’s a fair question. For over a decade, my identity as an investor was tied to real estate and rental properties. But this mindset that built my initial wealth isn't serving me in 2026. Between insurance costs doubling and the legal landscape becoming a nightmare, the math no longer works.

So, here is the mindset I’m using for the Great Rotation: I am prioritizing simplicity over prestige and complexity.

Stocks have always been the most consistent part of my portfolio. Now I'm doubling down on them. This is puzzling to some people who are building dry powder – after all, valuations in 2026 could be distorted due to AI hype. But from past experience, every time I’ve tried to be cautious and wait for a dip, I’ve regretted it. Consistency has always beaten timing, and trying to time the market has never worked.

I'm also changing the mix of stocks I hold. I’m allocating more into international and emerging markets as a hedge. I think these are undervalued given how much room there is for productivity gains and smartphone adoption as AI scales globally. Over the last year, my international stocks have outperformed the S&P500 and I think there's potentially more asymmetric upside there.

This wasn't an easy pivot to make, but this was a necessary course correction. I had to be honest with myself about what was actually working versus what I was familiar with.

I’ve just posted the complete, line-by-line breakdown of my new 2026 portfolio on Substack. I’m covering exactly how I’m allocating the real estate proceeds, my increased Bitcoin position, and even the collectibles that are keeping pace with the S&P 500. I'll drop the link in the comments.

Apr 14

I’ve spent a decade telling people to do what I do: "Buy and Hold."

Now I've decided to list my entire real estate portfolio for sale and walk away.

It started slow. The bills, the maintenance, the tax increases... but the final straw was when I tried to develop an ADU to do exactly what the city of LA claims it wants investors like me to do: Create more housing. You'd think they'd make it easier, but after two delayed inspections, a sewer pipe replacement that needed 75 days advance notice, and a city-owned tree that became my responsibility, I'd had enough.

The identity of being a real-estate guy is very hard to walk away from, trust me. For a long time, I stayed just because real estate was my "thing." It’s how I started. It’s what I’m known for. It led to every good thing in my life. But that blinded me to the fact that just because something served me in the past, it doesn't mean things haven't changed in the present.

The reality of 2026 finally stripped the emotion away. My LA rentals are netting about 4-5% after the constant background noise of taxes, insurance spikes, and repairs. Meanwhile, a risk-free Treasury pays 5%. The trade-off just doesn't make sense any more.

I’m reallocating to a liquid portfolio that actually lets me focus on the work I love. I published a deep dive on my Substack about the ADU nightmare that broke my patience, the exact numbers behind the exit, and where I’m moving the money next to buy back my sanity.

I'll drop the link here in a bit.

96

20

603

240,345

Apr 21

Where I'm investing after selling my real estate – Full post here: grahamstephan.substack.com/p…

6

4

32

12,139