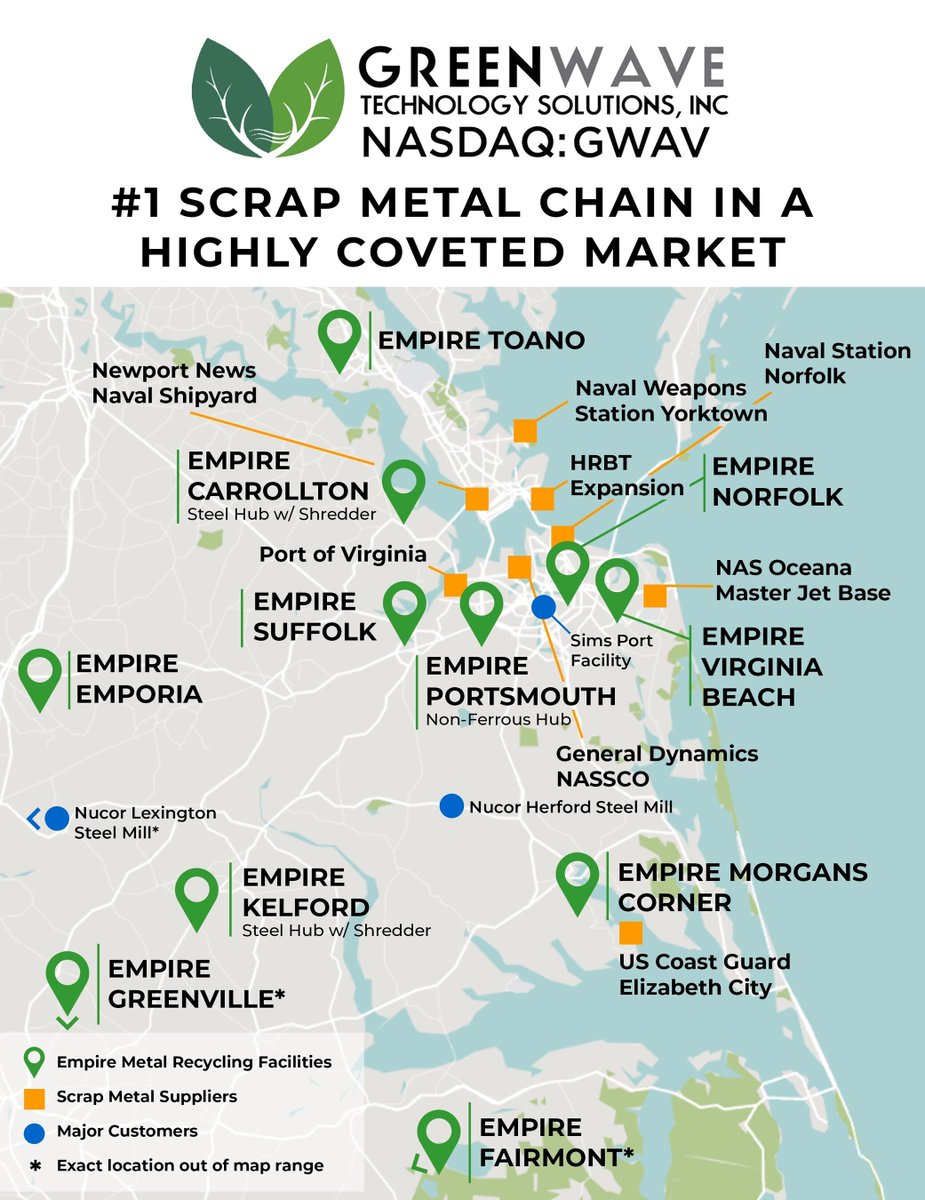

Greenwave Technology Solutions is a leading operator of 13 metal recycling facilities in Virginia and North Carolina. Nasdaq: $GWAV

Joined August 2022

- Tweets 471

- Following 96

- Followers 937

- Likes 81

239 Photos and videos

Pinned Tweet

12 Mar 2025

Drone footage of one of $GWAV 's ferrous metal processing hubs shot yesterday

13

4

27

9,327

19 Mar 2025

The U.S. scrap metal industry is undergoing a fundamental transformation – the past few weeks have revealed that steel producers/automakers have extreme exposure to tariffs and supply chain disruptions. (1/6)

7

14

7,743

19 Mar 2025

Since early February, domestic scrap steel prices are up 32% and demand is already far exceeding supply. These are the market conditions in which $GWAV performs the best -- and we're moving quickly to expand our operations. (5/6)

1

8

4,938

19 Mar 2025

When the dust settles, we expect the leading steel producers will likely own supply channels producing a significant portion of the raw material required to operate – and there’s limited U.S. scrap metal chains remaining. (6/6)

2

9

3,829

16 Mar 2025

Take a look at $RDUS / Schnitzer’s last 10-Q – massive net loss, cash burned in operations, and $582 million in shareholder’s equity.

So why would Toyota pay $1.34 billion all cash – a 120% premium – to buy it?

Toyota just locked down Schnitzer’s supply of scrap metal – which, until 48 hours ago, was the largest independent scrap metal chain in America.

This mitigates Toyota’s exposure to tariffs/supply chain disruptions – and Toyota was willing to pay a $757 million cash premium to secure it. It appears Toyota did not base their valuation on Schnitzer’s current operations but on the value their supply of scrap metal would provide to their operations.

$GWAV believes the scrap metal industry is undergoing a fundamental transformation – major steel producers are moving decisively to de-risk their supply chains by acquiring scrap metal companies, locking down a consistent supply of low-cost metal. Even before the tariffs, this was driving rapid consolidation of U.S. scrap metal companies.

We estimate there are ~50 scrap yard chains with significant supply volume left in the U.S. – the rest have already been acquired by one of the conglomerates. $GWAV expects the consolidation of U.S. scrap metal companies by steel producers to likely accelerate.

Two days ago, Toyota paid $1.34 billion cash – a $757 million premium – to buy the largest independent U.S. scrap metal company. We believe this is a clear indicator the market could be significantly undervaluing U.S. scrap metal chains.

2

1

13

3,652

16 Mar 2025

The speed at which Toyota moved to pay $1.34 billion all-cash – a 120% premium – for $RDUS / Schnitzer is a powerful indicator

The U.S. scrap metal industry is undergoing a fundamental transformation driven by countries and corporations locking down their supply chains

Steel mills are rapidly consolidating the U.S. scrap metal industry to de-risk by owning a perpetual supply of low-cost metal -- with acquisition costs usually recouped through savings on raw material within 3-5 years

1

20

3,442

14 Mar 2025

Toyota Tsusho America just announced it is acquiring U.S. steel recycler Radius $RDUS for $1.34 Billion

The U.S. scrap metal industry is being rapidly consolidated by mills and manufacturers de-risking their operations by securing supply chains

$GWAV is perfect positioned

3 Feb 2025

"U.S. steel producers are expanding and dominating the scrap metal M&A landscape as they seek control of raw material input to feed new mills."

info.bglco.com/bgl-metals-in…

2

3

16

5,202

14 Mar 2025

Toyota Tsusho America Acquires U.S. Steel Recycler Radius Recycling $RDUS for $1.34 Billion

The rapid consolidation of the U.S. scrap metal industry is being driven by steel mills and manufactures locking down their supply chains.

Great news for $GWAV.

reuters.com/markets/deals/to…

3

9

1,864

12 Mar 2025

New tariffs take effect as Trump’s trade war ramps up. $GWAV CEO Danny Meeks featured on @GMA ~2:41. Watch by clicking the link below. bit.ly/3DyfwA5

2

10

1,711

12 Mar 2025

$GWAV CEO Danny Meeks to be Interviewed on @GMA to Discuss Tariffs on Steel and Aluminum Imports Today. Read the press release below. prn.to/3FjEqnE

4

16

6,784

12 Mar 2025

$GWAV CEO Danny Meeks' interview with ABC News' Chief Business, Technology and Economics Correspondent, Rebecca Jarvis, will air on Good Morning America this morning.

Tariffs are now effective on all foreign steel and aluminum imports without exception or exclusion.

2

1

16

1,901