Joined March 2023

- Tweets 12,028

- Following 418

- Followers 6,189

- Likes 23,727

1,898 Photos and videos

Pinned Tweet

I believe there is a non-zero probability that the United States eventually revalues its gold reserves as part of a broader monetary restructuring.

I believe there is a possibility that a revaluation event could occur around July 4th, 2026.

I could be completely wrong.

The timing could be wrong.

Nothing may happen at all.

However, after publishing the thesis, I wanted to find a way to put a small amount of capital behind the idea.

This report explains exactly how I am expressing that view today.

Link below/bio 🔗

6

5

42

5,812

Grey Rabbit Finance 🥕 retweeted

Jun 12

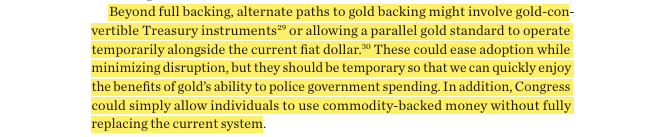

Probably the best way to illustrate what we’re seeing in the metals market today.

The show goes on….

open.substack.com/pub/tavico…

@LukeGromen

16

49

425

24,623

Grey Rabbit Finance 🥕 retweeted

This article is worth a read, especially considering Powell campaigned against having Judy Shelton on the Fed board. x.com/i/status/2065901428028…

7

30

5,623

Grey Rabbit Finance 🥕 retweeted

Jun 13

I DON'T EVEN KNOW WHERE PARAGUAY IS

489

4,030

92,978

5,616,770

Grey Rabbit Finance 🥕 retweeted

Jun 13

At what price will you sell your #gold and #silver?

This is the wrong question to ask.

Viewing gold in terms of dollars is a mistake. Whats important is what an ounce of gold gets you.

One of the best indicators is the Dow Jones to gold ratio.

Its not unheard of to wait for 1 oz of gold to buy the Dow Jones.

Will they meet at $25,000? $100,000? Higher? That is the question.

31

44

271

22,291

Grey Rabbit Finance 🥕 retweeted

Jun 13

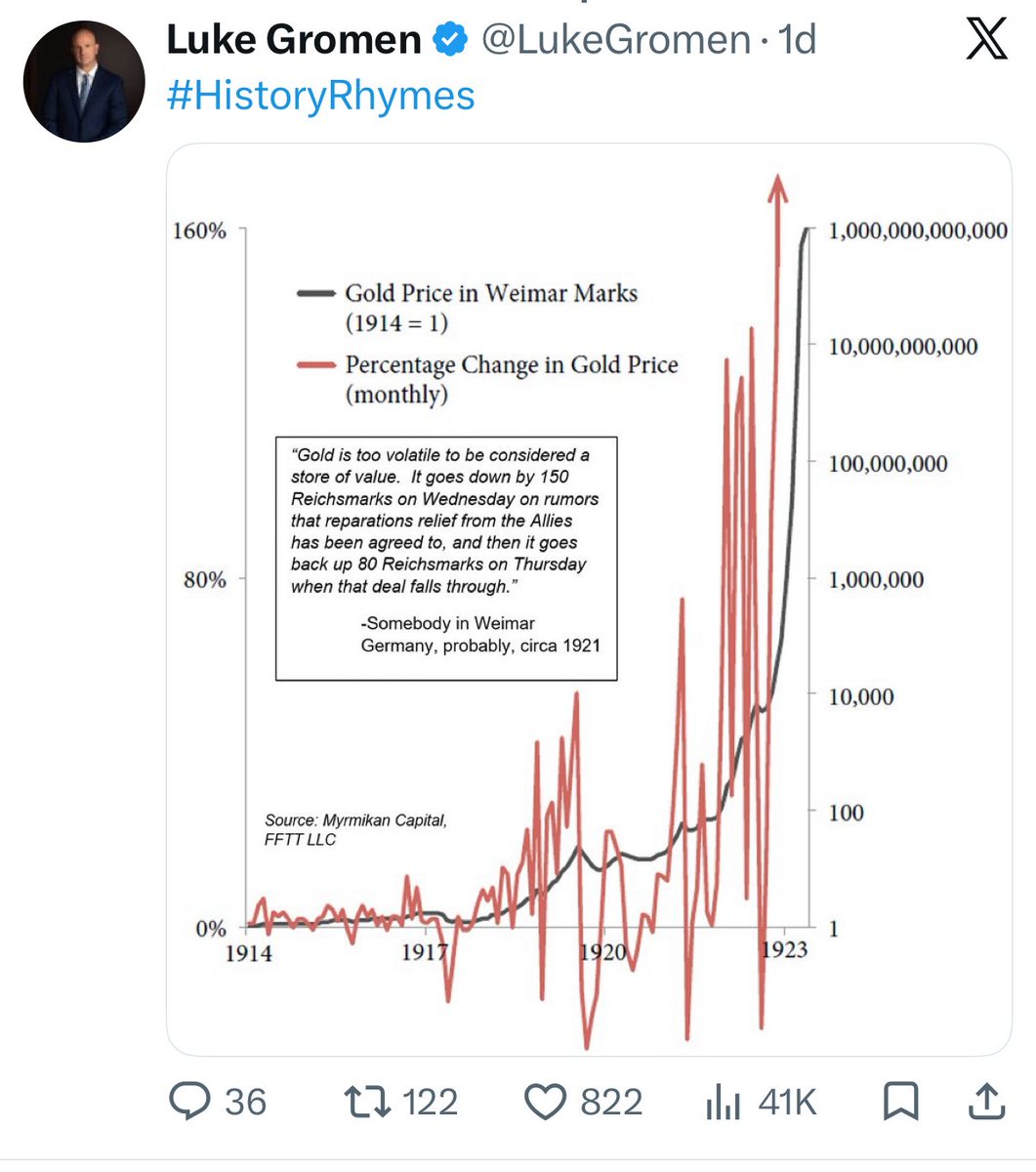

🔥Why QE Money Printing and UST Gold Revaluation Are NOT the Same Thing

QE is classic fiat expansion on the liability side. The Fed creates new reserves (digital dollars) out of thin air to buy U.S. Treasuries or MBS. Balance sheet balloons on both sides: more assets (bonds), more liabilities (new money).

When paired with massive deficits, it is debt monetization. The government spends, Treasury issues bonds, Fed buys them. This floods the system with new money that can chase goods, assets, and inflation.

Result? It damages the integrity and credibility of the U.S. Treasury market. Foreign buyers and markets see endless printing to fund deficits. Trust erodes. Risk premiums rise. Yields can eventually spike as the risk free label weakens. Pure dilution optics.

⭕️Gold Revaluation is fundamentally different.

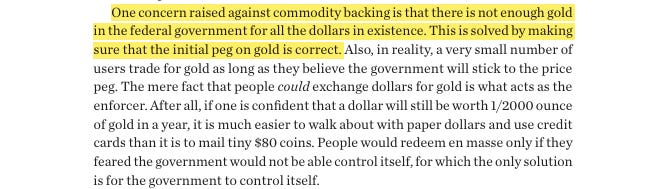

The U.S. Treasury sits on 261.5 million ounces of physical gold, still officially booked at the ancient $42.22/oz statutory price from 1973. Revaluing it to market (or a new higher statutory price) is an asset side accounting gain.

No new liabilities created. No printing from nothing. You are simply recognizing the real, higher value of a hard asset America already owns and cannot be printed. The Treasury can then issue gold certificates to the Fed, get credited in the TGA, and spend/use the gain all without selling one ounce of gold.

This is finite, tied to a tangible store of value, and has historical precedent (1934, early 1970s). It strengthens the reported balance sheet instead of weakening it.

Credibility impact is night and day. QE signals fiscal recklessness and reliance on the central bank printer. Gold revaluation signals alignment with real assets and bolsters confidence in U.S. finances without the monetization stigma. It preserves even restores Treasury market integrity.

What happens after revaluation? Expect a big Gold price overshoot, then a smackdown just like 1973 to 1975.

Official revaluation would ignite massive momentum: speculation, central bank buying, dollar pressure, and reset psychology. Gold runs hard, potentially way beyond fair value.

Look at history: Post Bretton Woods adjustments, gold surged from the 70s in 72 toward $200 by late 74 amid inflation and chaos. Then the Fed hiked rates aggressively to defend the dollar and fight inflation. Gold got crushed back down (toward $100 range) as higher yields raised the opportunity cost of holding non yielding metal and restored monetary discipline.

Same playbook likely awaits. Once the liquidity high and overshoot play out, the Fed will raise rates to protect USD credibility and Treasury market stability. Gold gets taken to the woodshed from its peak.

🎯Bottom line: QE erodes trust through endless liability creation. Gold revaluation leverages existing hard assets with cleaner optics.

#Gold #Silver #UST #MonetaryReset

34

49

273

17,696

Grey Rabbit Finance 🥕 retweeted

Jun 12

In the event of a #gold revaluation, we can all agree that there will be inflation.

But most of you will be shocked to hear that a revaluation to $5,000 gold would only produce 5% inflation.

About $1 trillion would be printed on that move, and considering the M2 money supply is about $23 trillion, you’d get less than 5% inflation.

Remember, inflation is CORRECTLY defined as an increase in the money supply!

Its completely reasonable to expect gold to outperform inflation if it gets re-introduced to the monetary system.

26

31

229

29,700

Grey Rabbit Finance 🥕 retweeted

Jun 12

I want to see how he would shrink the Fed’s balance sheet without a U.S. Treasury Gold revaluation and without imploding the U.S. Treasury Bond market.

11

8

90

7,912

Buccees lol

2

469

Grey Rabbit Finance 🥕 retweeted

I believe there is a non-zero probability that the United States eventually revalues its gold reserves as part of a broader monetary restructuring.

I believe there is a possibility that a revaluation event could occur around July 4th, 2026.

I could be completely wrong.

The timing could be wrong.

Nothing may happen at all.

However, after publishing the thesis, I wanted to find a way to put a small amount of capital behind the idea.

This report explains exactly how I am expressing that view today.

Link below/bio 🔗

6

5

42

5,812

Grey Rabbit Finance 🥕 retweeted

NEW VIDEO: The Anaconda Strategy: How Governments Are Taxing You Into Communism (Leave The West Now) youtu.be/-wU-hNTovbI

4

11

49

5,827

Grey Rabbit Finance 🥕 retweeted

Jun 11

This is some crazy shit 💩…😂😭🙃

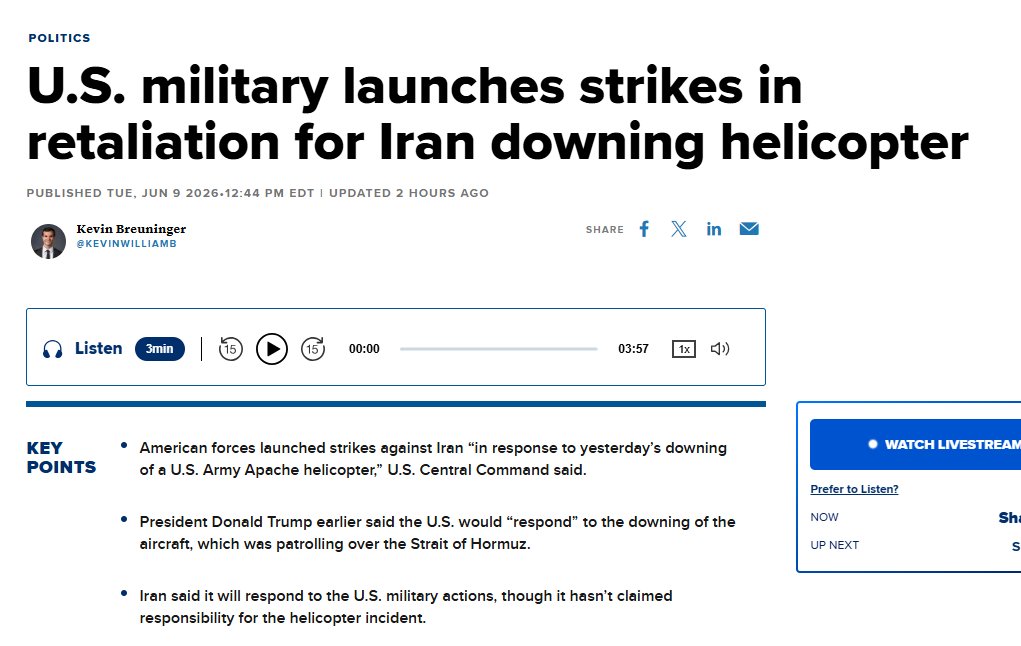

Jun 11

IRAN STRIKES CALLED OFF

President Trump says he has cancelled planned U.S. strikes and bombings against Iran scheduled for this evening. He stated that all parties have approved the discussions and final terms in principle and in detail. A naval blockade will remain in place until the agreement is finalized. The time and location for the signing ceremony will be announced shortly.

21

15

99

8,963

Poll results from my article "In the Air Tonight"

Link in Bio/below 🔗

1

2

465

I believe there is a non-zero probability that the United States eventually revalues its gold reserves as part of a broader monetary restructuring.

I believe there is a possibility that a revaluation event could occur around July 4th, 2026.

I could be completely wrong.

The timing could be wrong.

Nothing may happen at all.

However, after publishing the thesis, I wanted to find a way to put a small amount of capital behind the idea.

This report explains exactly how I am expressing that view today.

Link below/bio 🔗

6

5

42

5,812