9 Photos and videos

Pinned Tweet

30 Oct 2025

What the $GRUTA project creates and what plans it has for the near future, you can read here 👇

35t5DPbwJtB1tpGiSnqedLwQomi94BRKVDPyTRLdbonk

29 Oct 2025

What has been done and what's next. I'm writing this text mainly for myself so as not to forget some things. Later, based on it, we'll create a roadmap for the near future. And for you, dear $Gruta Fam, it will be useful for a general understanding of where we're heading.

So, the goal is to create a unique AI-based analytical platform that includes several tools.

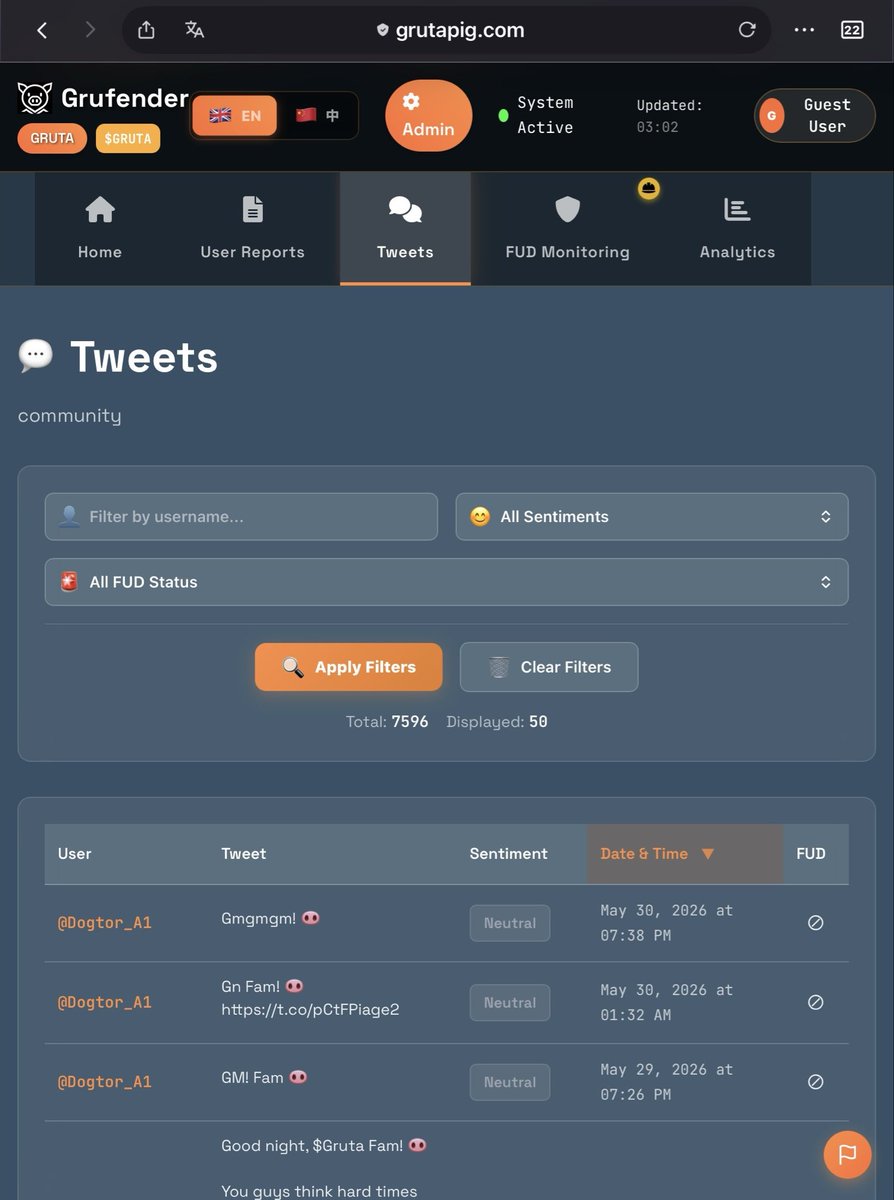

AI agent @GrufenderX - real-time analysis of crypto communities on X. Activity analysis, sentiment analysis, FUD and FUDders analysis, as well as the creation of other unique social metrics. The AI agent has been created and is functioning, collecting and analyzing data in real time. Its completeness can be estimated at 80 percent, as further improvements are required. The dashboard for this AI agent is also functioning but needs refinement and a new design. Its completeness can be estimated at 70 percent. The goal for the full dashboard release is to connect 50 - 100 top crypto communities to the AI agent.

AI agent @Grutector - analysis of any X users for contradictions (flip-flops). The AI agent has been created and is functioning. It has undergone beta testing by volunteers and needs adjustments. Its readiness can be estimated at 70 percent. The dashboard for this agent has also been created but needs rework and additional features - its readiness can be estimated at 50 percent.

During the testing of @Grutector , it became clear that the main user interest is in checking various KOLs, so an additional level of analysis specifically for KOLs will be created. More in-depth. How it will look: we'll select about 50- 100 KOLs to start with and fully analyze them using our AI agent - every tweet throughout the entire history of their accounts. And this full analysis of all these KOLs will appear on the @Grutector dashboard (let's call this analysis L2, and the flip-flop analysis - L1). Every user will be able to access this analysis and get the full picture, for example, regarding @blknoiz06 (who has over a hundred thousand tweets in his entire history!): how he became a KOL, what was the most interesting throughout the message history, what common patterns, which coins he promoted, and so on. And then the most interesting part - after reading this analysis, the user will be able to ask our AI agent: what did he say about women, for example? Or how did he promote certain coins? Or how consistent is he? And so on. Each such question will be paid. And, of course, we'll try to use #x402 in the internal payment system.

Why is all this needed? Not only because it's interesting and will attract many users. But also if you've decided to buy a coin - you go to our analytical platform - and study the metrics for the coin's community, study the KOLs who shill the coin - and make a decision to buy the coin or abandon the purchase.

And we're also currently creating a trading bot to participate in the trading AI bots contest from @Aster_DEX , which will make trading decisions based on metrics obtained from our AI agents 👀

Its readiness at the moment is approximately 15% of the planned functionality.

Access to each product will be granted as it becomes ready. But right now, for example, you can explore the @GrufenderX dashboard on the agi.info website along with beta testers (authorization via a wallet with a million $GRUTA tokens).

In general, we're working, friends 🫡

$Gruta AI CA:

35t5DPbwJtB1tpGiSnqedLwQomi94BRKVDPyTRLdbonk

1

4

421

We’re carefully watching how @bonkfun is being built by our beloved @SolportTom during the bear market.

3

2

7

208

Grutector retweeted

Jun 4

What crypto is in 2026. And why this cycle had no altseason.

Crypto in 2026 is Anatoly Yakovenko ( @toly ) dodging nine attempts to serve him in the suit against @solana / @Pumpfun / @a1lon9 — three in a single day, Aug 5, 2025. The court had to authorize alternative service, by email and FedEx. He’s still a named defendant; the case isn’t dismissed.

Proof (order, ECF 99): courtlistener.com/docket/695…

Is this how he pictured success? I doubt it :)

Crypto in 2026 is @TheOnlyNom explaining to $BNKK shareholders why their stake keeps shrinking. The company publicly brags it became “debt-free” with a 10.59 current ratio and “10x liquidity coverage” (CFO’s words, April 7, 2026 press release). Three small details, though:

— that same annual report (10-K) carries the auditor’s substantial-doubt-going-concern warning;

— independent data (InvestingPro) shows the real current ratio at ~1.01, not 10.59 — because the “10x coverage” is calculated excluding the volatile BONK tokens, which booked a −$35.4M unrealized loss in that very report;

— and the runway for future issuance is already cleared: authorized shares were raised from 250M to 1 billion (Oct 2025), plus a $100M shelf registration was filed (April 2026).

10-K: sec.gov/Archives/edgar/data/…

S-3 ($100M): sec.gov/Archives/edgar/data/…

And this is a @Nasdaq -listed company whose revenue is almost entirely tied to @bonkfun Two catches. One: nobody knows who’s behind @bonkfun — @SolportTom is anonymous, the entity isn’t disclosed, and when we asked (even though their own ToS says anyone can get this info) we simply got no reply. Two: shareholders think they own 51% of BF revenue. Formally — yes, 51% right now. But that same agreement hides a reversion clause:

@TheOnlyNom and @SolportTom can, by mutual consent, revert that share back to 10% at any time. You’re buying a stake two people can cut fivefold with a stroke of a pen. It’s all in the 10-K — read Note 2.

Crypto in 2026 is wall-to-wall manipulation. Especially on Solana. It’s 2026, baby.

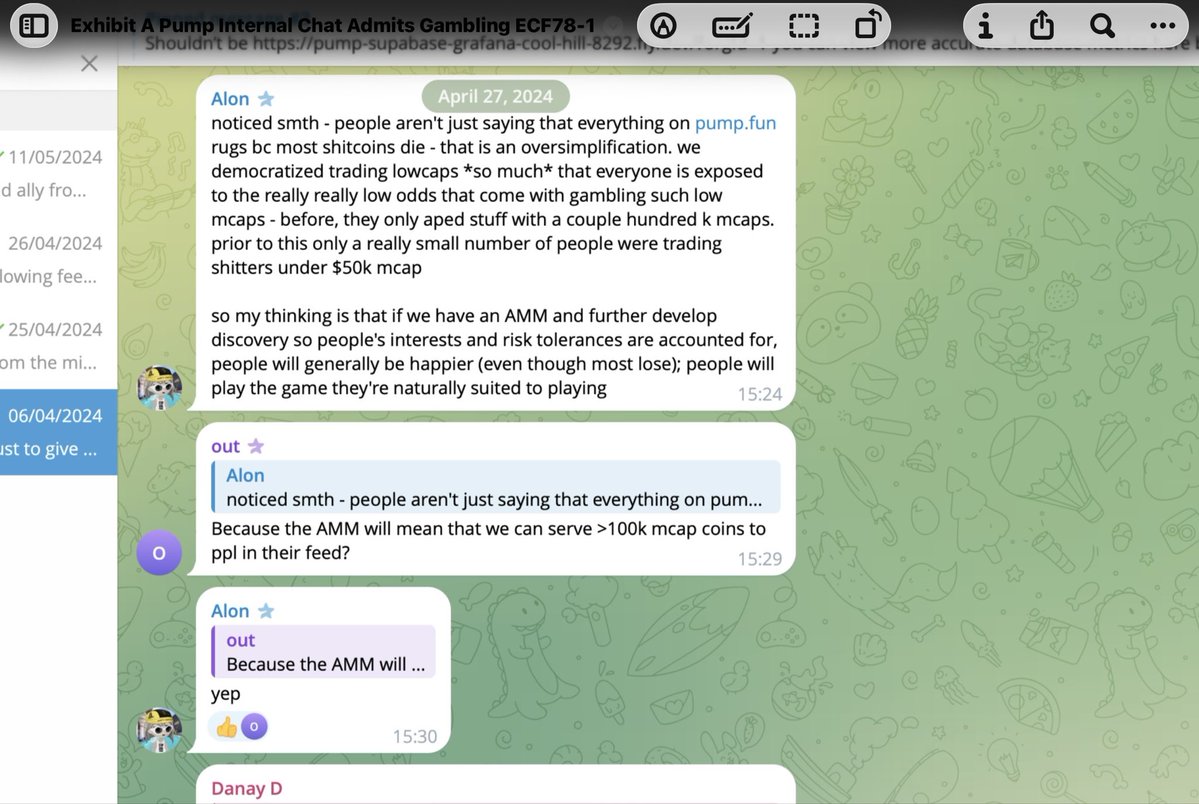

Here’s why I’m writing this. So you understand why Anatoly is so nervously trying to shake off the casino vibe @a1lon9 built. Honestly, I get him. And I get Alon too. In his own words — internal chats the court admitted to the record (Exhibit A, ECF 78, Aguilar v. Baton, 1:25-cv-00880, SDNY) — he knew most people lose, but figured they’d be “happier” that way, and that his casino was more honest than the other shitcoin schemes. And if it’s more honest — he slept just fine :)

Proof (Exhibit A “Admits Gambling”): storage.courtlistener.com/re…

@SolportTom with his @bonkfun , in my view, simply copied Alon’s system — but made it less transparent. And for some reason @TheOnlyNom is part of all this.

Just something to chew on. So the bear market isn’t so boring :)

3

6

10

575

Grutector retweeted

Jun 2

GM!

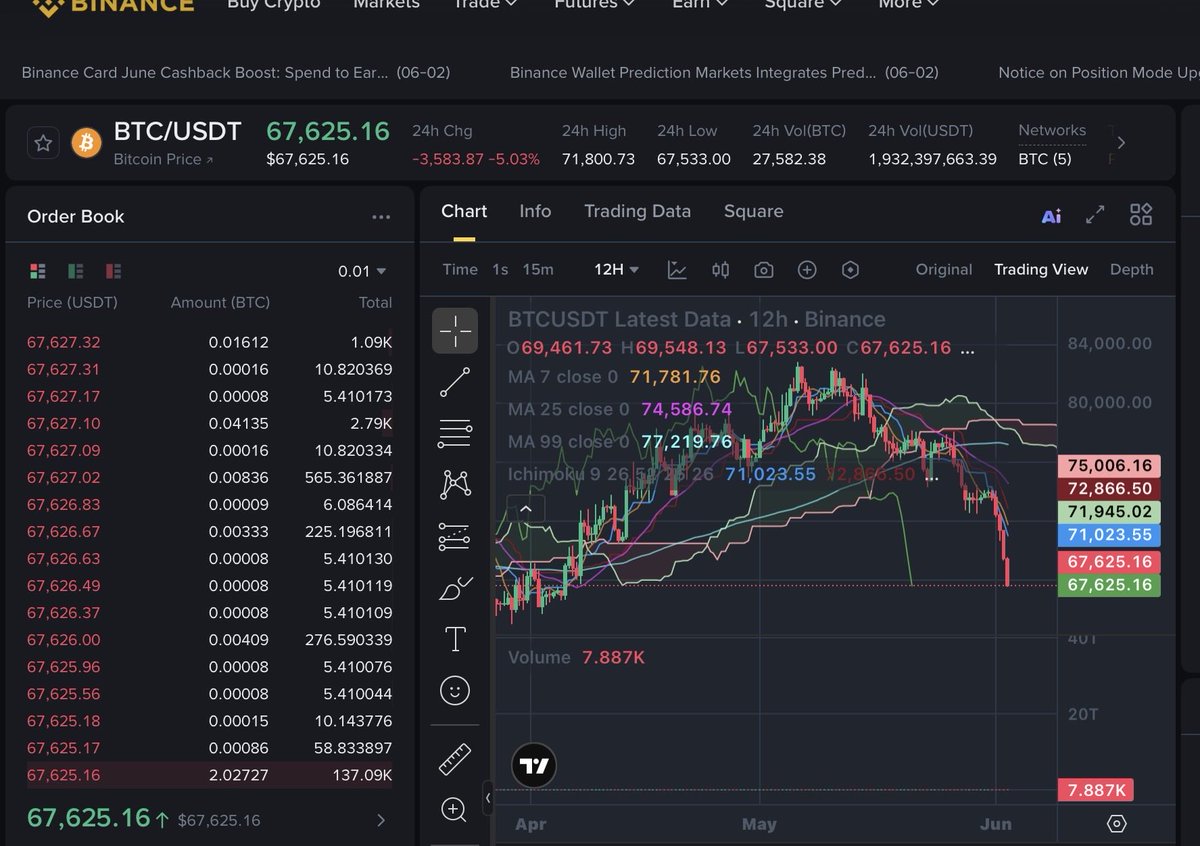

Bitcoin 67,700

Everyone with a Plan B doesn’t stress.

Red is the new black.

1

5

7

259

Grutector retweeted

May 31

Friends, this is probably the very last pinned post you’ll see in our $Gruta community.

Because communities will most likely disappear as soon as tomorrow.

But. We’re not going anywhere. My Twitter and the Gruta pig’s Twitter ( @GrutaPig ) remain. Follow the news there.

And the entire history of our group will forever stay in our memories — and, of course, on the dashboard of our AI agent @GrufenderX ( grutapig.com/grufender ), which has been monitoring our community and many others for the past six months 😀 So we’re the only ones who’ll preserve everything and lose nothing ;)

And later, when there’s time, we’ll somehow beautifully structure the whole year of our community’s history (without photos and videos, granted) on a website — for the record.

❤️🐽❤️

May 30

In the coming days, communities on X will disappear. Dear @nikitabier — if there’s any possibility at all to preserve the posts in communities for history, please do it. From our community alone, dozens of people poured an enormous amount of energy and time into posts there, and it would be deeply sad if those posts simply vanished as if they never existed. Leave history the ability to judge certain periods — including the period when X communities existed. Just turn this page, don’t tear it out.

As for everything else — we calmly keep working. And we’ll only tell you about it in broad strokes. It’s Web2. And that’s all we can say. Why? Because crypto is, fucking honestly, a synonym for fraud and total cluelessness — the situation is even worse than in 2021, if I’m being real. A simple example: we receive credits from large companies for AI infrastructure, and what do you think is written in capital letters in the terms of those credits? “If it’s not connected to crypto — we’re ready to help.”

Why did it turn out this way? Everyone has to ask themselves that question, especially on @solana @toly , of course, has his own answer — and on a human level, I understand every one of his decisions. Every step. To understand a person, you have to understand their whole path, from beginning to end. I understand Anatoly — or so it seems to me. There’s only one thing I’ll never understand: I’ll never forget how, at the peak of success (as it seemed to all of us back then), he destroyed — just like that, for no real reason — the project of an actual developer who had answered Anatoly’s own call to build Solana forks, mocking him on a live stream. Calling his project useless (a project the man had spent many months of work and resources on). And the most interesting part is that for that very stream, this person — with the $Los Analos token, if I’m not mistaken — had paid tens of thousands of dollars. That was the exact moment everything became clear to me about Solana, about how people outside the “in-crowd” get supported, and I had no more questions — neither for Anatoly nor for Solana. It’s interesting: now that even formerly outspoken Solana supporters are voicing doubts about its prospects — would @toly joke the same way again, and again not apologize for a destroyed project and a destroyed life?

This is Solana. That’s all I understood in a year inside this ecosystem.

There was also $Dark — @edgarpavlovsky project, which I backed from the very beginning, putting sums into it that were very large for me, and not even just tens of thousands of dollars :) The logic was simple: the person is open, the person is from the Solana in-crowd — he simply can’t deceive everyone. Well, it turned out how it turned out — I got wrecked there. I’ll note that Edgar, even though he has adventurer-like traits in his character and sometimes probably feels like he’s grabbed God by the balls — is a genuinely very promising person. A big talent. Who, for the sake of ordinary life, for many reasons, is forced to get involved in…

But that’s a separate story, known only to him. In any case, I hold no grudge against him, even though I really did lose serious money — serious for me — on his token. I see it as an investment in a person I believe in, even though I’ll never receive any dividends. But we’re all just the sword of God, we’re His conduit, and if I helped someone — even at some cost to myself — then that’s how it was meant to be. I’ll say it again: Edgar is a big talent, and it’s not a shame at all to sometimes help people like that.

And now, moving on — we created our token $Gruta in the Bonk ecosystem. Believing the promises that this was something first-of-its-kind, open, something that cared about its own reputation. @TheOnlyNom was the beacon of that movement, the one overseeing @SolportTom How Tom screwed everyone over through BF — I don’t think I even need to explain. Against his backdrop, @a1lon9 honestly looks like a damn saint.

3

3

8

381

Grutector retweeted

May 30

In the coming days, communities on X will disappear. Dear @nikitabier — if there’s any possibility at all to preserve the posts in communities for history, please do it. From our community alone, dozens of people poured an enormous amount of energy and time into posts there, and it would be deeply sad if those posts simply vanished as if they never existed. Leave history the ability to judge certain periods — including the period when X communities existed. Just turn this page, don’t tear it out.

As for everything else — we calmly keep working. And we’ll only tell you about it in broad strokes. It’s Web2. And that’s all we can say. Why? Because crypto is, fucking honestly, a synonym for fraud and total cluelessness — the situation is even worse than in 2021, if I’m being real. A simple example: we receive credits from large companies for AI infrastructure, and what do you think is written in capital letters in the terms of those credits? “If it’s not connected to crypto — we’re ready to help.”

Why did it turn out this way? Everyone has to ask themselves that question, especially on @solana @toly , of course, has his own answer — and on a human level, I understand every one of his decisions. Every step. To understand a person, you have to understand their whole path, from beginning to end. I understand Anatoly — or so it seems to me. There’s only one thing I’ll never understand: I’ll never forget how, at the peak of success (as it seemed to all of us back then), he destroyed — just like that, for no real reason — the project of an actual developer who had answered Anatoly’s own call to build Solana forks, mocking him on a live stream. Calling his project useless (a project the man had spent many months of work and resources on). And the most interesting part is that for that very stream, this person — with the $Los Analos token, if I’m not mistaken — had paid tens of thousands of dollars. That was the exact moment everything became clear to me about Solana, about how people outside the “in-crowd” get supported, and I had no more questions — neither for Anatoly nor for Solana. It’s interesting: now that even formerly outspoken Solana supporters are voicing doubts about its prospects — would @toly joke the same way again, and again not apologize for a destroyed project and a destroyed life?

This is Solana. That’s all I understood in a year inside this ecosystem.

There was also $Dark — @edgarpavlovsky project, which I backed from the very beginning, putting sums into it that were very large for me, and not even just tens of thousands of dollars :) The logic was simple: the person is open, the person is from the Solana in-crowd — he simply can’t deceive everyone. Well, it turned out how it turned out — I got wrecked there. I’ll note that Edgar, even though he has adventurer-like traits in his character and sometimes probably feels like he’s grabbed God by the balls — is a genuinely very promising person. A big talent. Who, for the sake of ordinary life, for many reasons, is forced to get involved in…

But that’s a separate story, known only to him. In any case, I hold no grudge against him, even though I really did lose serious money — serious for me — on his token. I see it as an investment in a person I believe in, even though I’ll never receive any dividends. But we’re all just the sword of God, we’re His conduit, and if I helped someone — even at some cost to myself — then that’s how it was meant to be. I’ll say it again: Edgar is a big talent, and it’s not a shame at all to sometimes help people like that.

And now, moving on — we created our token $Gruta in the Bonk ecosystem. Believing the promises that this was something first-of-its-kind, open, something that cared about its own reputation. @TheOnlyNom was the beacon of that movement, the one overseeing @SolportTom How Tom screwed everyone over through BF — I don’t think I even need to explain. Against his backdrop, @a1lon9 honestly looks like a damn saint.

2

5

9

617

Grutector retweeted

May 18

A long time ago, friends, I promised you we wouldn’t leave or disappear suddenly — and we kept that promise.

A long time ago I told you that what would destroy Solana is this terrible casino-for-suckers vibe, where every builder started treating investors like mentally ill guppy fish with a 10-second memory. We said this was unacceptable and we said we would be honest — even though it would be hard.

That’s why, when it was completely inconvenient for us, we told you that a bear market was beginning (nobody, by the way, believed it or said it publicly at the time), and the price was very far above one hundred thousand per bitcoin. I warned you so you could save your money.

I said honestly that, in our view, this situation would last quite a long time — most likely until 2027.

And we, by fate, ended up in the Bonk eco. And since that’s how it turned out, we honestly started describing what we see, hoping to change the situation before the bull market.

We were the first to point out the leadership problem at BF in the person of @SolportTom — does anyone think we were wrong? Is anyone satisfied with his leadership?

But the problem is getting worse, the crisis is spreading. And now we see how the respected @TheOnlyNom is consciously putting out hype-driven manipulation instead of real achievements. Why consciously, in our view? Because as President of $BNKK (appointed in April) he simply cannot have been unaware that these positions are standard passive index holdings that BlackRock has held since 2021, going back to the days of Jupiter Wellness, through broad-market index funds. This is not an active decision to “invest in BONK” — it’s mechanical index tracking.

But he wrote “welcome aboard.” He did it.

And we honestly say — this is a huge mistake. @TheOnlyNom was (and I hope still is) one of the most respected figures in @Solana , and if even he has started doing things like this — then maybe things really are bad?

I don’t want to think that. In any case, we hope our honest perspective will allow Nom to deliver real achievements to people going forward — not the kind of questionable, manipulative content that every serious investor sees through immediately.

Maybe this way we’ll help him preserve his reputation and save and revive $Bonk

I’d like to believe that — which is why we speak honestly. Openness is the last thing that can save the situation we’re currently in.

But if nothing changes, all of this will die. And it will be the fault of every participant, including us.

But we have nothing to lose. We can calmly migrate to, for example, @ethereum As a long-time ETH holder and investor in many projects on that blockchain, I have the strong sense that Ethereum has long since entered a phase of maturity — unlike Solana and many of the actors operating within it. That’s enough for us to keep building calmly.

And behind the scenes, we’re calmly building in Web2. Everything is going to plan.

Because we are $Gruta 🐽

May 18

Read the headline — “BlackRock buying memecoins”?

@TheOnlyNom replied “Welcome aboard.”

What picture formed in your head? Finally, the largest institutionals have come to Bonk too, right?

But this is exactly the kind of situation — fact-juggling, opacity, chasing the hype — that’s why there was no altseason last cycle. And why crypto, especially on Solana, has such a bad reputation in the normal world.

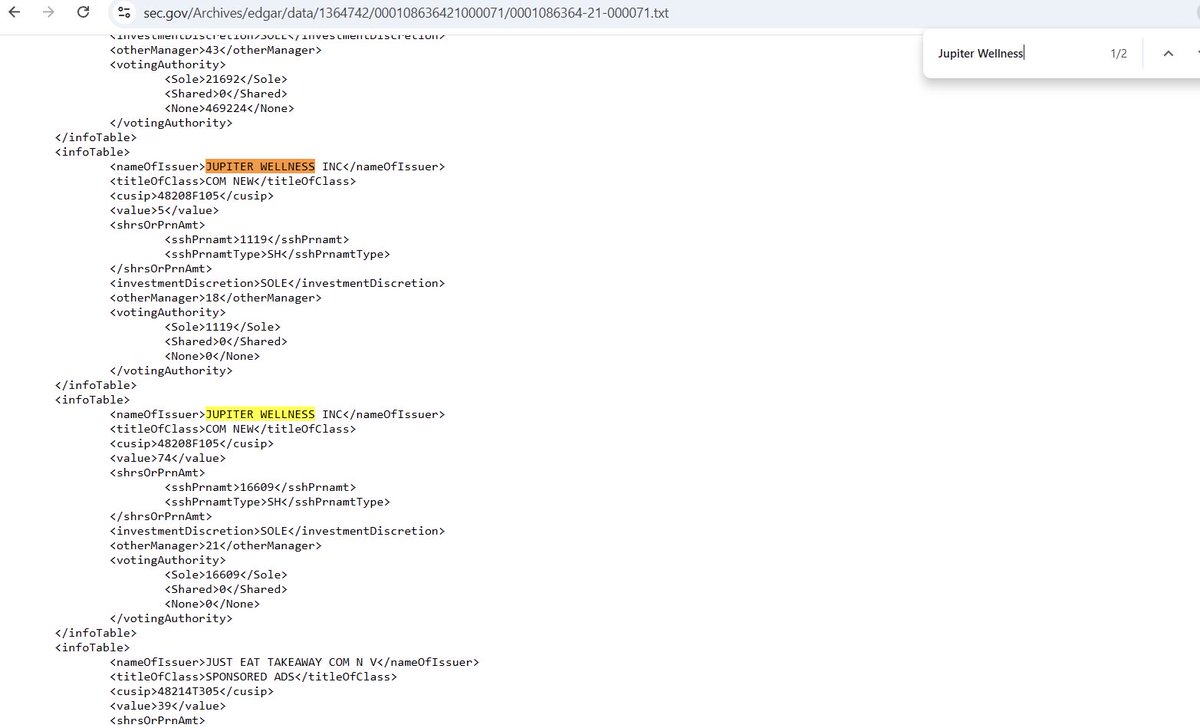

It’s simple. Mitchell Rudy ( @TheOnlyNom ), President of $BNKK since April 29, 2026, cannot have been unaware that these shares were bought by index funds back in 2021 — long before the company became $BNKK . Back then it was called Jupiter Wellness (ticker JUPW).

Inclusion happened almost automatically through passive index funds as soon as the company met the thresholds for broad-market indexes.

Proof — BlackRock’s 13F filing as of June 30, 2021: 17,728 shares of JUPITER WELLNESS INC. CUSIP 48208F105.

sec.gov/Archives/edgar/data/… (Ctrl F → Jupiter Wellness)

Then the company changed names several times — Safety Shot (ticker SHOT), then $BNKK. But the CUSIP never changed — Bonk itself confirmed this in its October 9, 2025 press release: “the common stock CUSIP remains 48208F105.”

And one more proof — the same BlackRock as of June 30, 2025: 526,599 shares of SAFETY SHOT INC. Same CUSIP 48208F105 as $BNKK has today.

sec.gov/Archives/edgar/data/… (Ctrl F → 48208F105)

So BlackRock has continuously held this security since 2021 — back when it was a hangover-drink company. They didn’t “buy a memecoin” — they’re just mechanically continuing to hold the same security under a new name.

And BlackRock, seeing how their passive position in a public company is being framed as “they bought crypto” — will of course become crypto enthusiasts))))

But on the bright side, as actual investors they can now ask a few questions.

For example — why is the only meaningful profit in $BNKK’s latest quarterly report ($796,404) the sale of 1,596,000 Caring Brands shares to four unnamed institutional investors at $0.50 per share, while the market price was $1.05 (~52% discount)? Not paid in cash — only in promissory notes maturing July 30, 2026, with no interest and no collateral. SPAs signed on March 20, 2026 — the exact same day BonkFun published its postmortem on the domain hack.

$BNKK 10-Q: sec.gov/Archives/edgar/data/… (Notes 3 and 7)

Why does $BNKK depend almost entirely on revenue from BonkFun, which is run by @SolportTom — a legend of the crypto market :)

By the way, he hasn’t written “next week” and disappeared after it for a while now — I’m starting to worry about him :)

And of course BlackRock might also ask — why is the bonk.fun domain hack not reflected in $BNKK’s latest quarterly report, given that the overwhelming majority of revenue comes precisely from the affected launchpad?

So many questions BlackRock can now be expected to ask, @TheOnlyNom

And maybe, indeed — welcome aboard :)

@CoinDesk @Cointelegraph @DecryptMedia @BitcoinMagazine

2

3

6

218

Grutector retweeted

May 18

Read the headline — “BlackRock buying memecoins”?

@TheOnlyNom replied “Welcome aboard.”

What picture formed in your head? Finally, the largest institutionals have come to Bonk too, right?

But this is exactly the kind of situation — fact-juggling, opacity, chasing the hype — that’s why there was no altseason last cycle. And why crypto, especially on Solana, has such a bad reputation in the normal world.

It’s simple. Mitchell Rudy ( @TheOnlyNom ), President of $BNKK since April 29, 2026, cannot have been unaware that these shares were bought by index funds back in 2021 — long before the company became $BNKK . Back then it was called Jupiter Wellness (ticker JUPW).

Inclusion happened almost automatically through passive index funds as soon as the company met the thresholds for broad-market indexes.

Proof — BlackRock’s 13F filing as of June 30, 2021: 17,728 shares of JUPITER WELLNESS INC. CUSIP 48208F105.

sec.gov/Archives/edgar/data/… (Ctrl F → Jupiter Wellness)

Then the company changed names several times — Safety Shot (ticker SHOT), then $BNKK. But the CUSIP never changed — Bonk itself confirmed this in its October 9, 2025 press release: “the common stock CUSIP remains 48208F105.”

And one more proof — the same BlackRock as of June 30, 2025: 526,599 shares of SAFETY SHOT INC. Same CUSIP 48208F105 as $BNKK has today.

sec.gov/Archives/edgar/data/… (Ctrl F → 48208F105)

So BlackRock has continuously held this security since 2021 — back when it was a hangover-drink company. They didn’t “buy a memecoin” — they’re just mechanically continuing to hold the same security under a new name.

And BlackRock, seeing how their passive position in a public company is being framed as “they bought crypto” — will of course become crypto enthusiasts))))

But on the bright side, as actual investors they can now ask a few questions.

For example — why is the only meaningful profit in $BNKK’s latest quarterly report ($796,404) the sale of 1,596,000 Caring Brands shares to four unnamed institutional investors at $0.50 per share, while the market price was $1.05 (~52% discount)? Not paid in cash — only in promissory notes maturing July 30, 2026, with no interest and no collateral. SPAs signed on March 20, 2026 — the exact same day BonkFun published its postmortem on the domain hack.

$BNKK 10-Q: sec.gov/Archives/edgar/data/… (Notes 3 and 7)

Why does $BNKK depend almost entirely on revenue from BonkFun, which is run by @SolportTom — a legend of the crypto market :)

By the way, he hasn’t written “next week” and disappeared after it for a while now — I’m starting to worry about him :)

And of course BlackRock might also ask — why is the bonk.fun domain hack not reflected in $BNKK’s latest quarterly report, given that the overwhelming majority of revenue comes precisely from the affected launchpad?

So many questions BlackRock can now be expected to ask, @TheOnlyNom

And maybe, indeed — welcome aboard :)

@CoinDesk @Cointelegraph @DecryptMedia @BitcoinMagazine

May 18

🫡 Welcome aboard!

1

4

7

1,184

Grutector retweeted

May 15

There’s a situation forming in Solana where old builders are being pushed aside. It’s a new format from @solana and @aeyakovenkoe — an attempt to focus only on projects that bring attention and profit here and now.

You can criticize Toly all you want, but it’s business logic. Anatoly is trying to cut loose ends — and that’s normal.

But you need to consider that the leadership of BF has done exactly the same thing to their own builders. Every single one of them, without exception, was thrown overboard. Over $10M allocated for their marketing simply evaporated — and nobody can say where it went (and @SolportTom just stays silent on these questions).

BF flushed away everyone who supported them, and even @theunipcs is now distancing himself as much as he can from Tom and BF — though he still supports #useless and (thank god) hasn’t migrated.

Nom is an old builder in this situation — but he can’t or won’t see it. It’s strange to blame Anatoly for exactly what’s happening in your own house with other builders.

By the way, $BNKK recently reported its first quarter.

sec.gov/Archives/edgar/data/…

Here’s what’s in this report:

— Net loss ~$1.8M for the quarter

— The only significant profit in the P&L: ~$800K from the sale of ~1.6M shares of Caring Brands (CABR) to four unnamed “institutional investors.” At a ~50% discount to market price. With no cash payment — only 4-month promissory notes, no interest, no collateral

— Sale agreements signed on March 20, 2026 — the same day BonkFun published the postmortem about the domain hack

— The BonkFun hack is mentioned nowhere in the report: not in Subsequent Events, not in MD&A, not in Risk Factors, not in Legal Proceedings. Complete silence about an incident that affected the platform generating ~80% of $BNKK revenue

— Disclosure controls and procedures declared by management as ineffective — second quarter in a row

I think any careful observer has grounds to raise questions with the regulator. And recent precedents show these questions cost real money (Mimecast ~$1M, Avaya ~$1M, Check Point ~$1M, Unisys ~$4M — all for incomplete cybersecurity disclosures).

@TheOnlyNom , you’re a really solid builder. But tell me please — shouldn’t you first put your own house in order before criticizing @solana ? Shouldn’t you deal with @SolportTom, who’s openly sinking the entire $BONK system?

Just a question. One that I hope you have answers to — at least for yourself.

May 12

At a time when Solana is fighting on many different battlefields, telling the users and founders of the past 6 years to go elsewhere is not a choice I'd make.

It's still not consensus to bet on Solana. There's a lot of work that needs to be done for user trust, ecosystem growth, and application usage. Things are better than they were before, and have a lot of room to grow. That needs Champions and Missionaries who have ties into the ecosystem.

Ignoring them is where it loses to other chains, in applications, users, and capital.

Simply put - There's a lack of a "we".

2

5

8

483

Grutector retweeted

May 8

… @theunipcs , I have a great deal of respect for you.

I can’t say that BF is a scam, but at the very least, the absolutely insane level of incompetence from the launchpad’s management is something I think no one disputes anymore.

Last year you were on their team.

Please tell me — are you still with @SolportTom or not?

I think a lot of people are interested in this question: do you still support this guy who periodically posts “Next Week” and then disappears, or blames everyone around him for the fact that he doesn’t do anything or does everything sloppily?

1

4

4

162

Grutector retweeted

May 2

Gn, Gruta fam 🐽

Big changes are happening right now.

While @SolportTom once again announced something big, then disappeared, then came back and said everyone around him is to blame — life moves forward.

@TheOnlyNom quietly became President of $BNKK on April 29. Taking full responsibility for everything happening in this public company. Personal responsibility.

pressrelease.com/news/bonk-i…

$BNKK main income right now is 51% of revenue coming from @bonkfun (even though by contract BNKK actually paid for only 10%, and gets 51% via an amendment with a reversion clause — I’ll explain how that works another time).

But that’s not my point. My point is — with $68.2M in operating losses and working capital of just $64K according to the latest 10-K — the respected @TheOnlyNom has no choice but to remove Tom’s ineffective team.

sec.gov/Archives/edgar/data/…

This isn’t personal. This isn’t breaking agreements.

It’s just business.

And if Nom has publicly stepped into the game — it means he’s actually ready to take on the responsibility.

Think about it.

And we, once upon a time, made a bet on Tom leaving BF — and now, seeing his behavior and how it’s hurting BF, I think you all already understand there was simply no other option.

We always think far ahead 🐽

Apr 12

Yesterday the respected @NoCrust_ asked me about $BNKK reports and I made a small mistake, saying both the annual and quarterly reports were out. So far only the annual report has been filed. The quarterly one was just a press release.

And after reading the annual report, I understand why that press release was needed :)

I won’t go deep into it, since we’re focused on BF and consider @TheOnlyNom and $BONK our allies in the fight against BF’s incompetent leadership in the form of @SolportTom

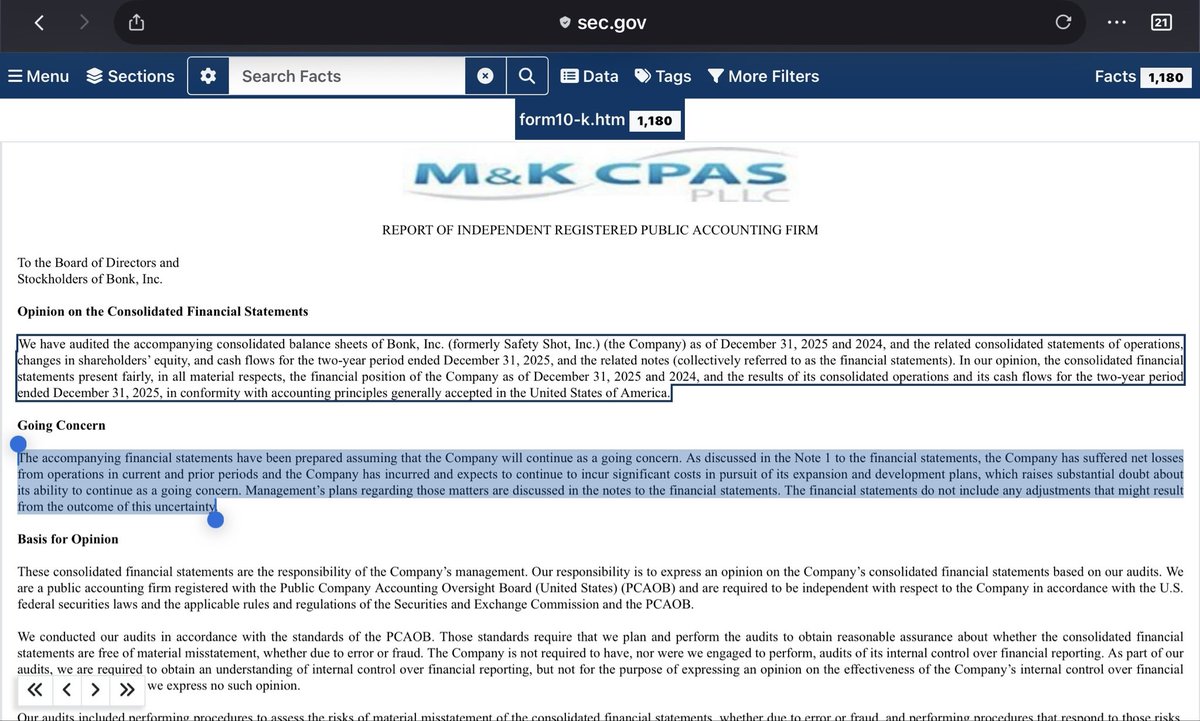

But in short: $BNKK has a loss of nearly $70 million.

The auditor (M&K CPAS) stated in their opinion:

“The Company has suffered net losses from operations in current and prior periods and the Company has incurred and expects to continue to incur significant costs in pursuit of its expansion and development plans, which raises substantial doubt about its ability to continue as a going concern.”

And the company itself confirms in the Risk Factors section:

“Our accountant has indicated doubt about our ability to continue as a going concern.”

The $BONK business model appears to have shifted from burning to accumulation — a very important shift.

However, there is good news. Essentially the only serious source of revenue for $BNKK going forward will be BF — it appears to be their only hope of staying on Nasdaq and turning a profit.

Which means @TheOnlyNom and the board of directors will simply have no choice but to clean house at @bonkfun — and keep only effective people in BF’s leadership.

Or the ship will apparently sink soon, if BF and its Tomtanic continues to be steered by Tom the way he’s steered it before.

sec.gov/ix?doc=/Archives/edg…

2

3

8

542

Grutector retweeted

Apr 26

Communities on X will soon cease to exist.

That’s Nikita’s decision. It’s his right. And our right, if we don’t like it, is to leave — for Threads, for example. But we’re not leaving. Which means we accept the rules of the game. And we hold no grudge against @nikitabier

We won’t stop existing as a community for one simple reason: a community isn’t a tab on Twitter. A community is people. Take away the tab — people will hang out in the comments under @GrutaPig posts or mine. They’ll keep saying Gm and Gn in our Gruta chat.

You can’t break apart people gathered around an idea just by removing a feature on X.

So we live on.

We continue trying to change Bonk eco, honestly naming the reason for the ecosystem’s decline. And the name of that reason is @solporttom. Lately, we don’t even need to criticize him or write about him — he does everything himself to confirm our points. He says one thing and does another. Always. Almost without exception. Just look at his latest tweet. «Next week» :)

As we said before, we’re temporarily working in Web2 to build a foundation there for developing our ideas and projects. Unfortunately, in Web3 this isn’t possible right now during a bear market. And in the Bonk fun eco — it’s a hundred times harder under Tom’s leadership. But we’re grateful to Tom: you should always learn where things are truly bad.

Still, the death of so many genuinely great communities — that, Tom, we will personally never forgive you for. Because those were real people.

You understand, don’t you?

Right?

3

3

6

126

Grutector retweeted

Apr 25

Remember your first love?

How you looked at her for the first time — the world filled with music, the sun gave every ray just to you.

How you hugged your grandfather or grandmother, and birds were chirping all around, and the trees were so big.

How mom and dad laughed brightly at sunset by that lake — together with you. And then you all swam, and they held your hands in the deep water.

All of this — marks carved into your soul.

All of this is you. Not knowledge, not skills — but the emotional intelligence you’ve gathered through your life.

And it is exactly this that will help us defeat AI.

One day, one of the creators will press the self-destruct button.

One day, a hacker will do what so many fear.

One day, a human will act irrationally — and by doing so, save humanity.

Or at least part of it.

Emotional intelligence, humanity, and irrationality — this is our last weapon, the one that may save us at the very last moment, when it seems all is already lost.

That kiss of first love, or just a glance that left a mark for life — that is exactly what AI will never understand.

Just think about it.

✊✊✊

2

5

8

122

Grutector retweeted

Apr 12

Yesterday the respected @NoCrust_ asked me about $BNKK reports and I made a small mistake, saying both the annual and quarterly reports were out. So far only the annual report has been filed. The quarterly one was just a press release.

And after reading the annual report, I understand why that press release was needed :)

I won’t go deep into it, since we’re focused on BF and consider @TheOnlyNom and $BONK our allies in the fight against BF’s incompetent leadership in the form of @SolportTom

But in short: $BNKK has a loss of nearly $70 million.

The auditor (M&K CPAS) stated in their opinion:

“The Company has suffered net losses from operations in current and prior periods and the Company has incurred and expects to continue to incur significant costs in pursuit of its expansion and development plans, which raises substantial doubt about its ability to continue as a going concern.”

And the company itself confirms in the Risk Factors section:

“Our accountant has indicated doubt about our ability to continue as a going concern.”

The $BONK business model appears to have shifted from burning to accumulation — a very important shift.

However, there is good news. Essentially the only serious source of revenue for $BNKK going forward will be BF — it appears to be their only hope of staying on Nasdaq and turning a profit.

Which means @TheOnlyNom and the board of directors will simply have no choice but to clean house at @bonkfun — and keep only effective people in BF’s leadership.

Or the ship will apparently sink soon, if BF and its Tomtanic continues to be steered by Tom the way he’s steered it before.

sec.gov/ix?doc=/Archives/edg…

4

3

8

1,397

Grutector retweeted

Apr 10

This is my open letter to you, @TheOnlyNom — to the last person deserving of trust in the BonkFun ecosystem.

You and I, Nom, both grew up in cold latitudes. Snow greeted us every morning when we walked out the door to school. I don’t know how your childhood went, but most likely you stepped out of your house or the building where your apartment was — stood for a second after walking through the door, looked up at the sky, and thought: oh god, another day of school. Stuck out your tongue trying to catch a snowflake. And somewhere nearby, a school was waiting for you — full of sorrows and joys, friends or acquaintances, and maybe people who flat out didn’t understand you. And you got there either on foot or someone from your family drove you. Snowdrifts, snow and cold — your main memory of winter childhood days, right?

I also walked out of my apartment building, but in a completely different part of the cold world — in the territory of the former Soviet Union. My grandmother would see me off with the words: today you almost got lucky. Why did she say that on the coldest days? Because if the temperature dropped below -27, I didn’t go to school. Every morning my grandmother listened to the radio, and when the frost signal sounded, you could stay home. She would come and turn off my alarm. But if it was a warm day, then at -25 I would dress like a cabbage and head to school, hearing from my grandmother — that I almost got lucky today.

I would push through enormous piles of snow and approach my old school, built in 1960. Three stories, with several windows smashed by hooligans. 7 steps to climb before you could walk inside. I would go in, hang up my coat in the cloakroom, and climb floor by floor up to the third. And somewhere near the third floor, on that day which I remember very well, I took a massive fist to the face. From a guy who was a year or two older than me. His name was Dima. He was a Candidate Master of Sport in boxing and had been held back a year. I was 11 at the time. Then he kicked me and I simply flew down half a flight of stairs. It was the most humiliating and painful moment of my life up to that point.

And there were two choices. Stay quiet, wipe yourself off. Because there was zero chance of winning. He was twice my size and far more physically prepared — he was an athlete. And the second choice — fight back. And die heroically. If you think kids at that age didn’t fight for real where I’m from, a fight I was in where people literally smashed heads against trees reminds me otherwise.

So I stood up and said: Dima, I challenge you to a fight. Where I grew up, this was called a strelka. And when you call a strelka, it’s a matter of reputation for your entire school life — you simply cannot not show up. Otherwise what awaits you is reputational death and eternal contempt.

Dima was a little surprised, of course, but gladly said he would come. There were many witnesses, and most of them looked at me like a dead man walking.

4:30 PM arrived. Behind the school, Dima and I stood across from each other in fighting stances. About 50 kids from our classes and others came to watch. Everyone was waiting to see what would be done to me. The only question was whether I’d leave in an ambulance or if my friends could carry me home.

I remember only the punches to my head. My head. The world suddenly loses focus, then snaps back into place — and there’s Dima again, smirking in front of me, winding up his fist for the next blow. I don’t know how many there were. 5, 10, 15…

Mar 7

Gm, Gruta Fam!

We don’t want to migrate like other tokens from the BF eco. We don’t want to run away from problems. We truly believe in $Bonk , so we’re doing everything in our power to change the situation.

The situation, to put it mildly, is not great. We already wrote that, in our opinion, a share of the market was lost due to the incompetence of the BF leadership and specifically @SolportTom

Now, after carefully studying how @bonkfun is structured, I have to conclude that besides incompetence, there is also a quite deliberate plan (I may be wrong, but I personally have no other explanation) by the current BF leadership to create an absolutely opaque and suspicious system. This not only undermines trust but can also lead to very serious legal consequences.

Judge for yourselves how the system is built and what the risks are:

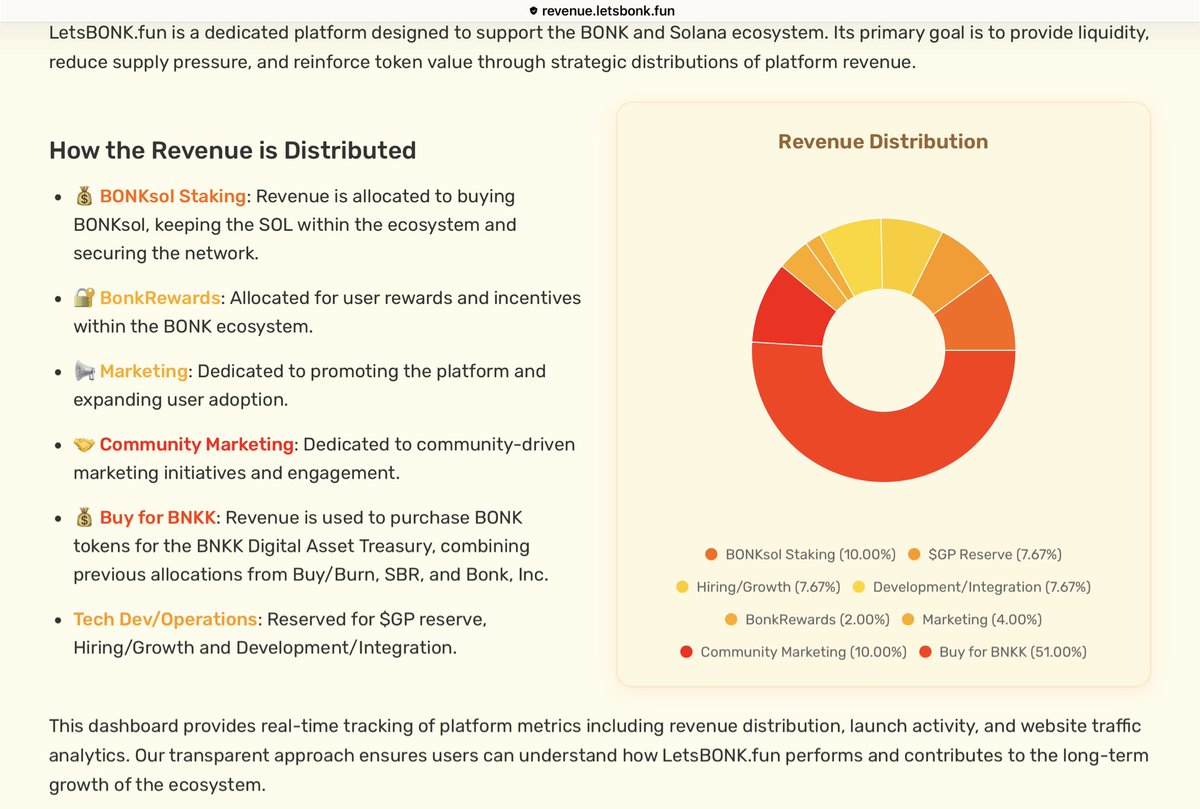

1. BonkFun operator is hidden despite a public partner

51% of BonkFun revenue goes to Bonk, Inc. (BNKK) — a public Nasdaq-listed company accountable to the SEC. This is real transparency, and the dashboard at revenue.letsbonk.fun shows on-chain distribution that anyone can verify.

But Bonk, Inc. is only the revenue recipient, not the platform operator. The operator remains an unknown BVI entity. In the Terms of Service (bonk.fun/terms-of-service), Section 1 literally says: “For specific information about the legal entity behind Bonk.fun, please contact us at the email listed in Section 14.” The legal entity is not named in the ToS or Privacy Policy — everywhere it’s just “Bonk.fun”. Jurisdiction: British Virgin Islands.

For comparison: pump.fun is also BVI, but their ToS directly names Baton Corporation Ltd. (UK, Company No. 14743013), three publicly known founders, a specific arbitration mechanism (BVI Arbitration Act 2013, Tortola), and a concrete list of prohibited jurisdictions. And even with all that, pump.fun received two class-action lawsuits and an FCA warning.

BonkFun chose not to disclose even what pump.fun disclosed — despite tens of millions of dollars having passed through the platform from September 2025 to March 2026.

In essence, no one knows what legal entity actually stands behind BF.

2. Anonymous operator controls ~23% of revenue

51% goes to the public Bonk, Inc. — transparency exists here. But the remaining ~23% (per the dashboard: $GP Reserve 7.67%, Hiring/Growth 7.67%, Development/Integration 7.67%) goes to Graphite Proto — Tom’s company. Tom’s real name is unknown. Graphite Proto has no public registration — no jurisdiction, no company number, no address.

So nearly a quarter of many tens of millions of dollars flows through a completely opaque entity controlled by an anonymous person. For the Bonk, Inc. portion, SEC reporting works. For the Graphite portion — zero accountability.

3. Conflict of interest via $GP

BonkFun revenue → 7.67% directly to $GP Reserve (straight from the dashboard). Tom owns $GP. He makes strategic platform decisions that most likely directly enrich his own token. He himself stated $300-700k per week in buybacks, a $1m LP pool for $GP, and hiring a COO specifically for $GP.

At the same time, the official @bonkfun account has never once mentioned the $GP token. Zero conflict-of-interest disclosure. The fact that 51% goes to a public company does not remove the question of how the remaining 23% is used.

4. Public financial promises without reporting

The revenue.letsbonk.fun dashboard shows overall distribution — and that’s good. But it does not confirm Tom’s specific promises to the communities:

3

5

6

1,857

Grutector retweeted

Apr 5

A wheelchair rolls along the aisles of a grocery store, carrying grandpa Tom.

Pushing the wheelchair is @iamkadense

Grandpa isn’t moving. Hasn’t moved in a long time. But there’s a sign hanging on him - “Tom is still alive.”

Once upon a time, grandpa used to shout across the whole store: “Money isn’t really what motivates me at this point, it’s legacy, got something to prove. A lot of people said I was washed for the past 3 years, now they all trying to kiss my ass.”

And after that - everything happened the way it always does when someone believes their own legend. He lost everything. And burned everyone around him. Everyone who believed in him.

And then he fell asleep in front of the TV and never got up again.

The time has come to move on. But some people have decided to pretend that grandpa Tom is still alive. So they wheel him to the store - so all the neighbors can see that the old man is still breathing.

Only one question remains - why? And who is this for?

It’s time for BF to move forward and rebuild everything from scratch after @SolportTom tenure. Which means it’s time to respectfully bury grandpa. And move on. No matter how many personal feelings connect you to him.

4 Jul 2025

Money isn’t really what motivates me at this point, it’s legacy got something to prove.

A lot of people said I was washed for the past 3 years, now they all trying to kiss my ass

1

3

4

515

Grutector retweeted

Apr 4

Recently @SolportTom publicly reached out to @a1lon9 - silence.

Now @SolportTom reached out to @theunipcs - no response.

Interesting - why does Tom get no reaction from either competitors or former allies?

Any thoughts?

As for me, I think we just need to wait a little longer before Tom’s departure.

The situation is starting to resemble one where grandpa has died, but everyone for some reason keeps pretending everything is fine and he’s just sleeping in front of the TV. Day after day. Here’s @iamkadense bringing him new slippers. Here’s @TheOnlyNom walking by and greeting him. Sometimes they even take grandpa to the store in a wheelchair, so all the neighbors know he’s still alive.

It’s just the smell that gives away the real state of affairs.

Apr 3

Need the delusional bulls back in memecoins.

@theunipcs its time to come back and show people how to believe again

6

3

16

3,334

Grutector retweeted

Apr 3

Alright friends, let’s play a children’s game. It’s called - spot the difference between statements and reality.

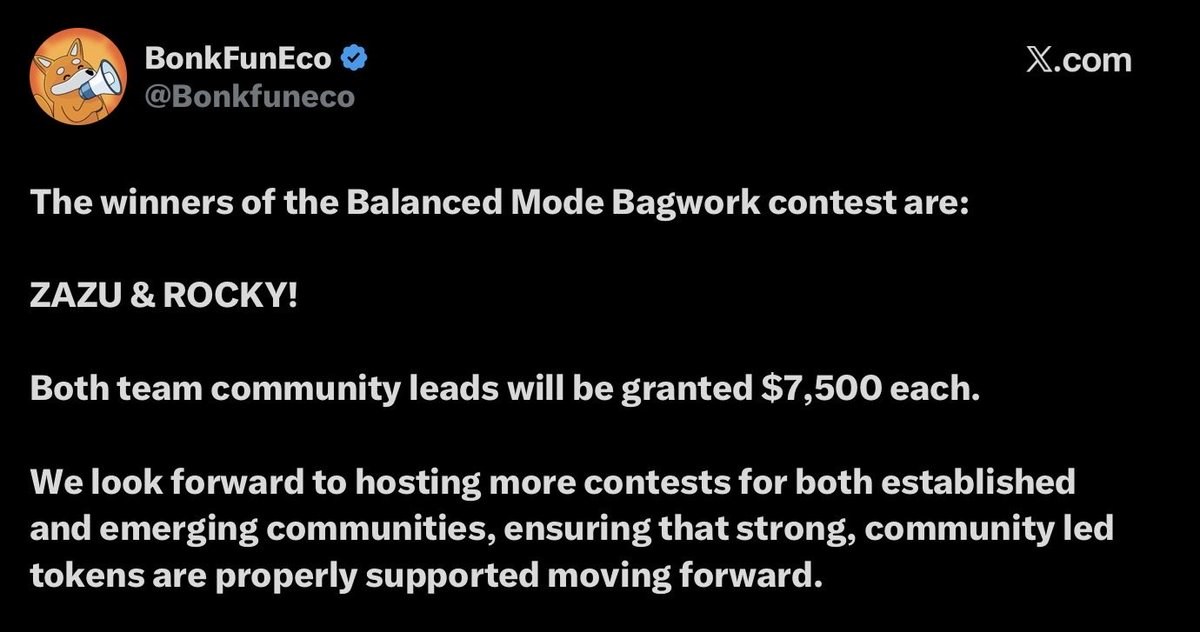

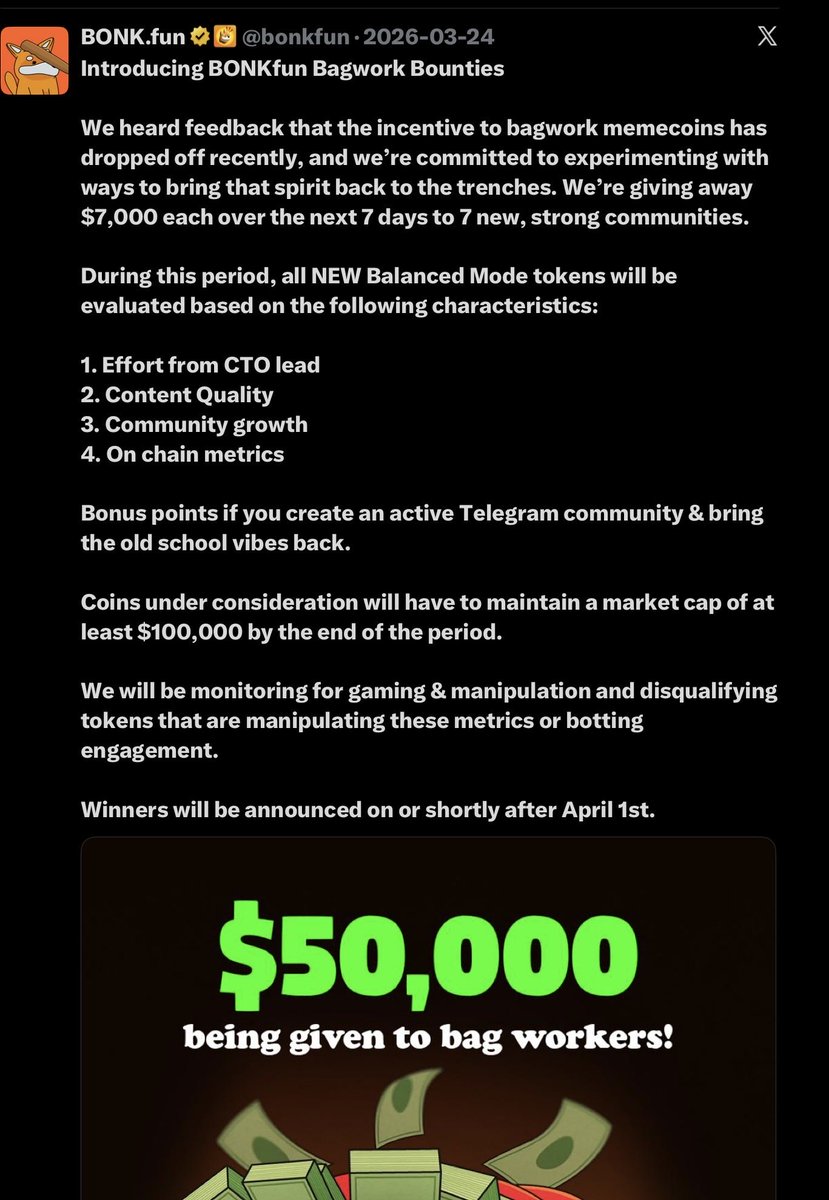

@bonkfun announced a contest and clearly stated: 7 new communities will receive $7,000 each. Work on your bags, bro.

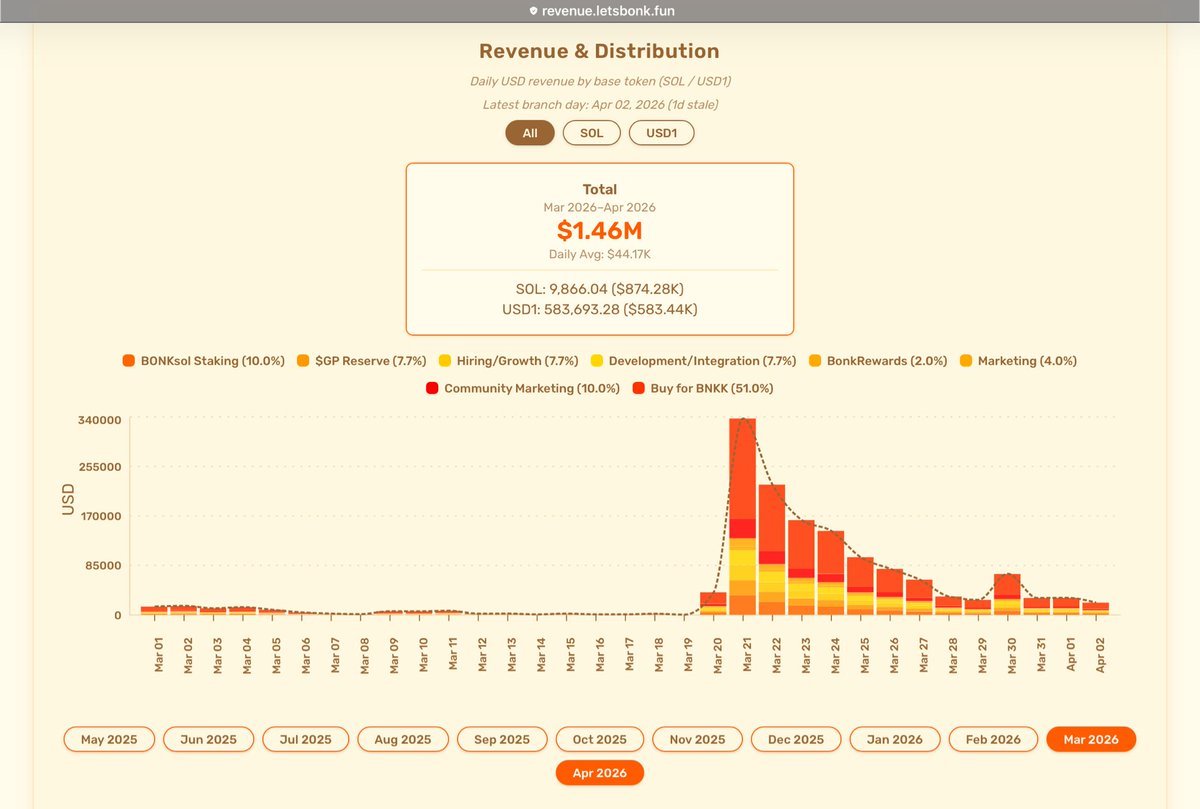

In March through early April, @bonkfun earned $1.46M according to their own dashboard at revenue.letsbonk.fun Of that, 10% goes to community marketing by their own formula - that’s ~$146,000.

When they announced $49K for the contest, I thought - okay, they’re spending 49 thousand out of 146, but maybe the rest won’t just vanish like the $13 million previously allocated to community marketing that simply disappeared into thin air ( @SolportTom for some reason refuses to comment on this), and will actually be distributed to new communities.

But what are the actual prizes:

2 communities. $15,000. Out of a $146,000 budget.

Curtain call.

Are you kidding? @SolportTom , is there any limit to the audacity? Promised 7 - delivered 2. Promised $49K - delivered $15K.

And then “We look forward to hosting more contests” - of course, we’ve heard that about 25 times this year already.

However, your stubbornness in publicly showing everyone how you threw OG communities off the train -like $Kori , $SPSC and others - is almost admirable in a way. A masterclass in screwing people over.

Even if we entertain your excuse - like a 15-year-old’s - that no other communities besides these two were worthy, you could have helped those communities that refuse to die, even though you personally did everything to kill them.

We didn’t die either. Annoying, right? Why do you think new communities aren’t appearing? Maybe because all the old ones were simply deceived, and now you’re just praying they die off so you can start a new chapter, right?

Screw you. We’re not dying. You’re the one leaving this year, and you’ll answer for all of it.

Apr 3

Going to keep iterating rewards to see what moves the needle for teams to want to grind, we’ll find the perfect recipe.

Congrats to the winners above, payments will be sent in the next 24 hours. 🫡

3

4

7

811