Joined January 2024

- Tweets 1,526

- Following 37

- Followers 1,733

- Likes 2,019

221 Photos and videos

Pinned Tweet

Hanji deployed on @monad in stealth weeks ago and is now top 2 in weekly volume.

Hanji's orderbook has:

- fully onchain execution & settlement

- zero maker fees & near-zero taker fees

- a vault-based liquidity model for fees and spread capture

You can try it now 👇

45

32

258

27,142

Jun 12

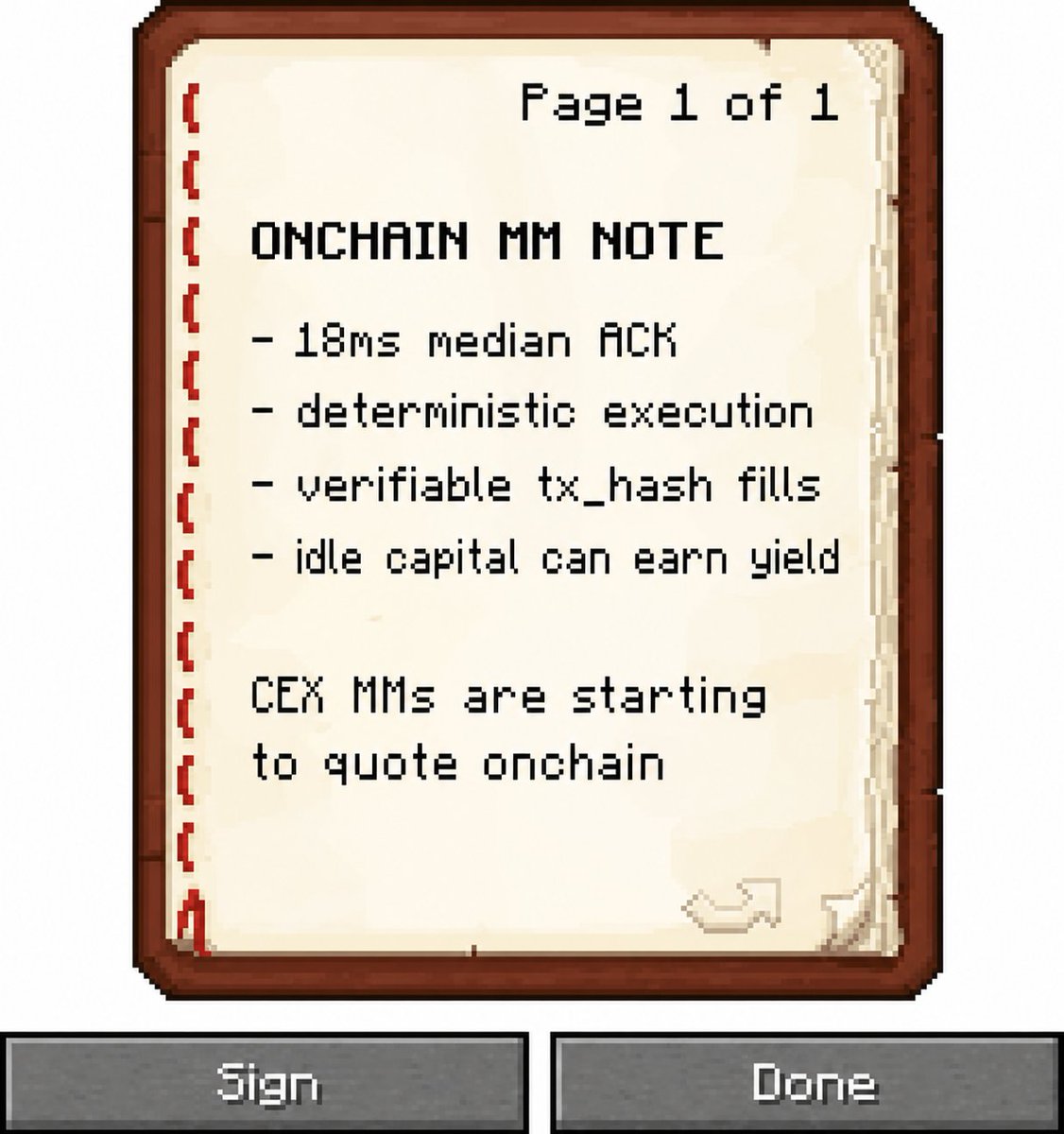

why CEX market makers are starting to quote onchain

for three years, the honest answer to "why don't professional MMs quote on-chain" was simple: the infrastructure wasn't there. Latency unpredictable, execution non-deterministic, inventory earning nothing between fills. No spread compensates for that. That calculus is changing.

The latency objection is dead

18ms median ACK, fully onchain matching engine, no off-chain sequencer. CEX co-located runs at 12ms. That gap doesn't kill a strategy. The spread math still works.

Execution is now deterministic

CEX order lifecycle is clean: place → ACK → fill or cancel. On-chain used to mean mempool chaos, failed cancels, slippage on your own order management.

Every state transition is a verifiable onchain event. Every fill returns a tx_hash. Cancel behavior is clean. No off-chain layer introducing ambiguity between what the API confirms and what settles.

For compliance-conscious desks, that auditability is an improvement over CEX, not a compromise.

Capital efficiency flips the model

This is where CEX can't compete.

On a CEX, inventory sits in custody between fills. Earns nothing. $10M across a dozen pairs is $10M in dead capital - present for risk, absent for yield.

LP positions function as collateral without unwinding. Your capital quotes the spread and earns yield simultaneously. At scale, that doesn't close the gap with CEX economics. It inverts it.

The next cycle competes on execution quality

DeFi's first cycle competed on yield. The second on incentives. Both were temporary.

Execution quality is a permanent moat. Better economics for every participant, no bribing required.

The volume follows the makers. The makers follow the infrastructure.

2

14

111

Hanji Protocol 🟠 retweeted

Jun 11

🧵

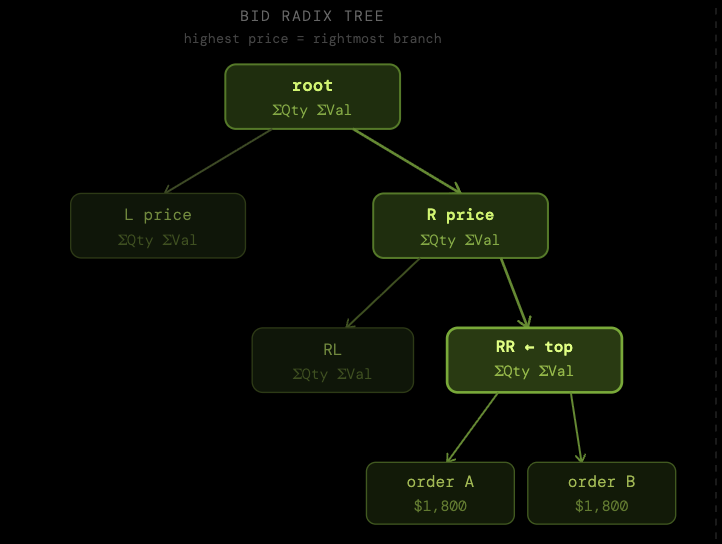

Onchain matching vs offchain-orderbook DEXs: where the engine really lives

"Onchain orderbook" is the most abused phrase in the space. Most of them aren't

The only question that matters: where does the matching engine sit, and what's actually in consensus ?

1

4

16

202

Jun 11

🧵

Onchain matching vs offchain-orderbook DEXs: where the engine really lives

"Onchain orderbook" is the most abused phrase in the space. Most of them aren't

The only question that matters: where does the matching engine sit, and what's actually in consensus ?

1

4

16

202

Jun 11

🧵

Off-chain sequencer, onchain settlementVertex, Aevo, Paradex. Central sequencer matches, chain settles. Fast, CEX-like, but you trust an operator for ordering. A CEX with a settlement receipt.

1

5

45

Jun 11

🧵

Where Hanji sitsTier 1. Book matching onchain on Monad / Etherlink. The bet: parallel execution preconfs make full onchain matching viable without the latency tax that killed the Serum era.

3

28

Hanji Protocol 🟠 retweeted

MEV Was Never a Mystery. It's a Price on Order Flow.

How deterministic matching on an on-chain CLOB kills toxic ordering

Strip the "dark forest" mystique and MEV is mechanical: deciding what order transactions execute in is valuable, and on most venues that right gets auctioned to whoever pays most. You aren't front-run by magic. You're front-run by a market built to extract from you

The tax is sequencing

On an AMM, price moves with pool reserves so the order trades land in sets who gets which price. Whoever controls ordering controls who buys cheap. On a public chain that slot sells: searchers bid for position, builders sort by what pays. Your block is an auction, and the proceeds come out of the traders inside it. MEV isn't an exploit bolted on - it's the structural result of putting a price-impact curve and a buyable transaction order in one place.

The sandwich

You swap with slippage tolerance. A bot buys before you, pushes the curve up, you fill worse - still in your band, so it clears. The bot sells into the impact. You bought high, the bot kept the difference, nobody broke a rule. It needs two things: a price that moves with flow, and an order you can pay to win. A CLOB removes both

Deterministic matching

A CLOB prices off resting bids and asks and matches them by one fixed rule: price-time priority. Best price first; same price, earliest first. Public, identical, every match. On an AMM, reordering the block changes who gets what so reordering has value, so it sells. On a deterministic CLOB the book decides who matches whom, not the block builder. No reorder improves a searcher's fill at your expense. The auction that funds toxic MEV has nothing to sell. And a resting limit order has nothing to sandwich: your price is your fill no band to push through, no curve to dump into

The honest part

This kills the reorder-and-extract class, not all MEV. Latency still matters - first to post, first to cancel is an edge, and sequencer neutrality has to be engineered, not hand-waved. But the surviving competition is a race to quote tighter and react faster. That compresses spreads. The half that dies is the half that exists only to tax flow by manipulating order. Discretion is where toxic extraction lives; deterministic matching removes it

The claim

AMM: ordering is an auction, and the trader is the product. Deterministic CLOB: ordering is a rule, and the rule is public. Crypto didn't need to reinvent how exchanges sort orders - it needed to stop handing order-of-operations to whoever pays the most gas.

This is what we run fully on-chain at hanji: a real orderbook, deterministic price-time matching, verifiable settlement, custody you never give up. Toxic flow dies where discretion dies. Put the book onchain, fix the matching rule, and there's nothing left to auction.

2

13

186

Hanji Protocol 🟠 retweeted

🧵

Every major blowup in crypto trading had the same root cause

not bad ux. not slippage. not gas. counterparty risk.

You handed your coins to someone and trusted they'd hand them back

1

4

20

240

🧵

Every major blowup in crypto trading had the same root cause

not bad ux. not slippage. not gas. counterparty risk.

You handed your coins to someone and trusted they'd hand them back

1

4

20

240

🧵

Self-custody means no counterparty. An auditable book means no black box. CEX-grade structure without a CEX-grade operator standing between you and your money.

1

20

🧵

You were never supposed to choose between a real market and your own keys. Counterparty risk was the bug. An onchain book is the patch. The rest - spreads, latency, depth - is just engineering.

16