Joined September 2016

- Tweets 3,382

- Following 600

- Followers 10,584

- Likes 3,573

265 Photos and videos

Pinned Tweet

24 Jul 2025

Just published our Black Book invite for upcoming IPO, $FIG, which we will host on Tuesday, 7/29, @ 2PM ET

3

1

7

4,286

Nick Balch retweeted

I’m actually starting to get more bullish software…

Dev tools, auth, security, hosting, CI/CD, CDNs, observability…

Always thought that AI is a TAM multiplier, but seeing the virality over something like clawd (which btw is NOT that incremental compared to existing agentic open source frameworks for coding), makes me think the demand acceleration is closer.

11

7

104

17,906

Join us in wishing a very happy birthday to the one and only Bob Rich!!

For over a decade, our talented cartoonist has been bringing smiles and laughter to people at Hedgeye and around the world. We couldn’t be more grateful for him! 🎉

8

12

95

20,050

Nick Balch retweeted

6 Oct 2025

Some thoughts going into @OpenAI DevDay tomorrow…

The next phase of software is “prompt to production.”

Software won’t be written in the traditional sense… 5 years from now it’ll be requested.

Enterprises and consumers will increasingly describe what they want, and the OpenAIs of the world will translate that intent into deployed applications.

The model becomes the platform, and everything above it (orchestration, data, compliance, UX) becomes configuration.

This is the logical endpoint of software abstraction….

So far we have gone from assembly → high-level languages → frameworks → APIs → no-code.

Now we’re moving toward no-interface…natural language as the ultimate API surface. Enabled by sophisticated protocols like MCP.

In that world, “software companies” look very different:

1) Most application value accrues to distribution and domain expertise, not the code itself.

2) The moat shifts from engineering complexity to prompt engineering systems integration/architecture.

I really can’t emphasize enough how important points 1 and 2 are in navigating the next 5-years.

It’s still early and yes, everything can change. But this is what these companies are building towards.

And you can already see the market starting to price this in… every OpenAI announcement compresses SaaS multiples.

The market is telling us:

“when software becomes on-demand, margins and moats compress toward the model layer.”

We’re witnessing the transition from Software-as-a-Service → Software-on-Request / Software-on-Demand

And that is why being vertically integrated (like $GOOGL) is so valuable…

8

13

93

21,076

Nick Balch retweeted

23 Sep 2025

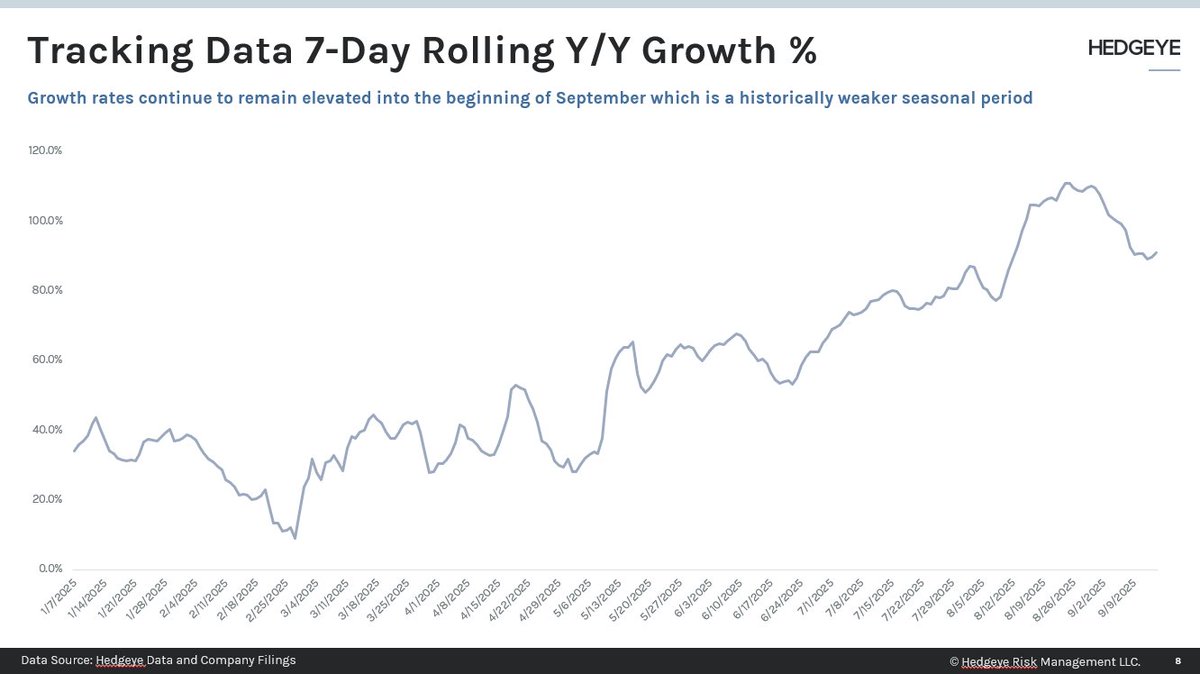

In our weekly Metaverse tracker for $RBLX our Q3 DAU estimate ticked down slightly to 144.3m. Key element for the week was a return to W/W growth after several weeks of declines in the data we track. Trends looking strong into the last full week of the quarter.

1

1

14

4,892

🚨 Our "Silent Auction" is NOW LIVE! 🚨

Join us in helping support children and families in need with a special focus on scholarships, youth sports, and community programs with the Chelsea Piers Foundation.

Bid on incredible items, experiences, and even a portfolio coaching session by Hedgeye CEO @KeithMcCullough through the link below 👇

32auctions.com/HedgeyeCares2…

8

7

10

46,529

🏌️ This Year's "Silent Auction" is NOW LIVE!

The Hedgeye Cares Charity Golf Challenge helps support children and families in need with a special focus on scholarships, youth sports, and community programs.

Some incredible items up for grabs! (a thread)🧵

32auctions.com/HedgeyeCares2…

5

17

23

38,898

Nick Balch retweeted

10 Sep 2025

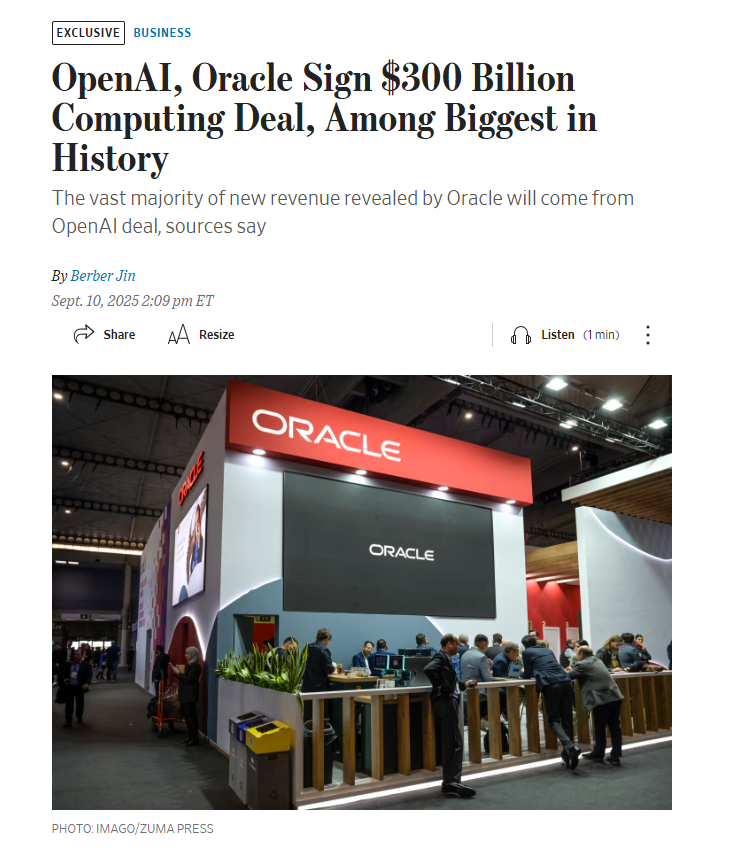

$ORCL RPO ex-OpenAI was $155B (vs consensus $154B) or 56% YoY

I realize thinking like this doesn't add much value because OpenAI did happen and the $$$s are there...

But the size/concentration does make you question 1) the margin $ORCL is getting on the $300B and 2) the trajectory/arc of RPO going forward.

wsj.com/business/openai-orac…

23

24

224

86,998

Nick Balch retweeted

3 Sep 2025

$FIG this thing going to the $40s where it belonged in the first place? @HedgeyeSoftware

9

2

25

11,170

2 Sep 2025

Yahoo's fantasy football AI predictor is clearly still in beta

6

6

6,021

Nick Balch retweeted

2 Sep 2025

And so it begins...

The Hedgeye A-League Draft

@NFLFantasy @YahooFantasy @HedgeyeDJ @HedgeyeFood

Check out some of the people Mucker's Men have to beat!

9

2

14

9,415

Nick Balch retweeted

20 Aug 2025

Yesterday @HedgeyeComm and I presented our updated work on $RBLX adding it to the Active Long side of our position monitor in lieu of our weekly data note.

The data we are tracking continues to come in strong and our DAU estimate for Q3 ticked to 142.7m

6

4

23

16,714

12 Aug 2025

RT @Hedgeye: WATCH | From Fidelity to Hedgeye: Sam Rahman’s Playbook for Performance

🔊

Veteran portfolio manager Sam Rahman @SamofAmeric…

14

Nick Balch retweeted

12 Aug 2025

We just published our weekly $RBLX data note: Our DAU-correlated metrics showed w/w declines for 8/4-8/10, but smaller drops vs. same period last year. This relative seasonal outperformance drives a slight uptick in our Q3 DAU forecast → now 141.7M

4

2

15

5,959

Nick Balch retweeted

12 Aug 2025

Broader industry players like Microsoft (with Copilot in Teams/Planner) or Salesforce are already leaning in heavily, blurring the lines between CRM, project management, and AI orchestration.

So while the SEO hiccup is worth monitoring, it's a distraction from the bigger picture. The true long-term value (or risk) for $MNDY lies in how they navigate the transition.

Investors should be asking… Can Monday transform into an indispensable AI agent hub, or will it become just another tool in an agent's toolkit?

1

1

11

4,009

Nick Balch retweeted

12 Aug 2025

While the recent discussions around $MNDY and the impact of $GOOGL SEO /AI changes on their marketing funnel and conversion rates have sparked a lot of heated debate, I believe the reaction is somewhat overblown.

Don't get me wrong—it's a legitimate concern that warrants attention, especially in a competitive SaaS landscape where customer acquisition costs can make or break growth trajectories. But fixating on this issue risks overshadowing a far more profound, existential threat to the entire work management industry: the rapid rise of AI and autonomous agents

First, on the SEO front: Google's algorithm/AI updates, particularly those emphasizing helpful content and user intent, have undoubtedly disrupted organic search traffic for many platforms, including $MNDY.

In their latest earnings call, management highlighted how these shifts have led to softer funnel performance, with lower conversion rates from top-of-funnel leads.

This isn't trivial; for a company like $MNDY, which relies heavily on inbound marketing to attract SMBs and enterprises looking for customizable work OS solutions, any dip in SEO visibility translates to higher CAC and potential revenue headwinds.

Investors are right to scrutinize this, as it could pressure margins in the short term if they need to ramp up paid channels to compensate.

That said, this feels more like a tactical challenge than a strategic death knell. Management has navigated similar hurdles before—think evolving ad policies or competitive pressures from Asana, Trello, or Notion—and emerged resilient.

While the SEO issues are fixable with proactive adjustments like content optimization, diversified marketing strategies, and perhaps even AI-enhanced SEO tools of their own, Monday is also facing increased competition from a proliferation of productivity and work management tools that are AI-native from the ground up. This intensifies the landscape, driving up CPCs and hurting ROAS as more players vie for the same ad inventory and audience attention.

Now, here's where the real conversation should pivot… the looming shadow of AI and intelligent agents. We're not talking about incremental features like $MNDY own AI integrations (which are still surface-level). I'm referring to the paradigm shift where AI agents—think advanced systems like those being developed by OpenAI, Anthropic, Google—could fundamentally redefine "work management" as we know it.

Imagine a future where AI agents don't just automate tasks within a platform… they orchestrate entire workflows across disparate tools, predict needs proactively, and self-optimize without human intervention.

In this world, do we even need a centralized work OS like $MNDY? Agents could ingest data from emails, calendars, CRMs, and docs, then generate dynamic boards, assign tasks, and track progress in real-time—all via natural language interfaces.

No more drag-and-drop interfaces or manual column setups; just conversational commands to an AI that builds, iterates, and executes.

This isn't sci-fi—it's already emerging, right? Tools like Auto-GPT or agentic frameworks in LangChain are early prototypes, and with multimodal models handling everything from code to visuals, the barrier to entry for custom automation drops to zero.

For $MNDY whose value prop is empowering non-technical users to build workflows, this poses an existential risk: commoditization. If AI agents become ubiquitous (and affordable), the demand for proprietary platforms could evaporate, shifting the battleground to who controls the AI layer rather than the UI/UX.

Of course, $MNDY isn't blind to this—they're investing in AI features like formula suggestions, automation bots, and predictive insights.

But the question is whether they can evolve fast enough to become an AI-first company, or if they'll be disrupted by pure-play AI upstarts.

6

9

93

47,714

Nick Balch retweeted

11 Aug 2025

You probably don't cover the $MNDY short until narrative shifts to them being an "AI Loser"

2

1

6

3,875

Nick Balch retweeted

11 Aug 2025

Here is part of the note we published post $MNDY 4Q24 earnings on 2/11/2025.

Takeaway: Staying short... guidance better than feared but upside is limited, growth slowdown coming and the stock is priced for perfection - we don't believe MNDY is the second coming of HubSpot or Salesforce.

Summary:

The stock was up yesterday (giving back last 2-months underperformance) as management offered FY2025 revenue growth guidance of 24% - 26%, with the mid-point in-line with lowered expectations and below where the street was at year-end (See Exhibit C).

Embedded in management's revenue guidance is a 100-200bps Fx headwind, bringing the constant currency revenue growth guide to 26% - 28% or a 500-700bps deceleration relative to 2024. Meanwhile, guidance for Non-GAAP operating income and free cash flow came in 7.4% and 8.2% below consensus, respectively, as management intends to invest heavily in headcount growth in 2025 30% increase (particularly quota carrying sales reps).

Customer Growth Slowing Faster

Customer growth representing ~65% of 2024 ARR (less than $50K ACV) slowed to ~9% in 2024 with the remaining ~35% growing ~42% YoY. The only way Monday.com can sustain 28% ARR growth is if they 4x the rate of $50k ARR customer net additions by 2028. We view such acceleration as unlikely given our view (based on primary research) that the core work management product is not an enterprise solution, the CRM is still not competitive to HubSpot or Salesforce, Dev uptake has been disappointing and Services faces a crowded market at an add-on price point significantly about CRM and Dev.

As a reminder, a key part of our negative thesis was that price increases would slow customer growth and that is exactly what we saw in 2024 (See Exhibit B). After 2Q24 earnings on 8/12/2024 we published a note (click here) suggesting that total customer growth in 2024 could decelerate to ~11% versus 21% in 2023. That estimate proved to be high, with actual total customer growth slowing to ~9% YoY and customers with 10 users growth slowing to ~10% YoY in 2024 (~79% of ARR).

While customer growth continues to slow in aggregate / below our expectations, the fastest rate of growth is occurring in its larger ARR segments $50k and above (~35% of ARR).

Customers with $100K in ARR grew 44.9% YoY (versus our 40.5% estimate and 58.1% in 2023), while customers in the $50K-$100K ARR range grew 36.4% YoY (compared to our 34.5% estimate and 54.4% in 2023). We estimate these segments represent ~35% of Total ARR and ~44% of ARR from customers with 10 users (~42% YoY ARR in 2024).

The remaining segment customers with 10 users but less than $50k ARR saw customer growth slow to 9% YoY in 2024 with estimated ARR growth of 28.5% YoY. The slower growth suggests Monday.com is converting/upselling customers to $50k faster than they are replenishing their pipeline - a negative indicator for the sustainability of the $50k ARR segment that is driving ~42% net new ARR.

Less Upside Compared to Prior Years

2025 revenue is likely to come in closer to 28% or $1,243M versus management's guidance of $1,208 - $1,221M. We arrive at this estimate two ways 1) bottom up assumptions of growth drivers based on customer type and segment (See Exhibit D and E), and 2) a top down looking at historical ARR coverage. On the latter, we assume management has visibility into ~88% of 2025 revenue based on the mid-point of their guidance of $1,215M (See Exhibit A)

In 2024, Monday.com recognized $162M in revenue in excess of prior-year ARR for a coverage of ~83% (versus management's initial guidance of ~87%). Our assumption for 2025 revenue growth assumes a final coverage ratio of ~86% or 2% upside relative to mid-point of management's guidance. Breaking this down further:

Management's initial guidance for 2024 implied revenue recognized in excess of prior-year ARR of $119M or a decline of $11.3M versus 2023.

In 2024, excess revenue contribution came in significantly higher at ~$162M or $43M above the $119M implied in the guidance provided in February 2024. Keep in mind that original guidance for 2024 didn't contemplate the pull-forward of price increases that contributed an estimated $30M of revenue.

Looking at 2025:

Implied revenue recognized in excess of prior-year ARR based on management's guidance is $142.6M or a decline of $19.1M versus $161.7M in 2024.

Given 2024 price increases will contribute ~$40M to revenue growth in 2025, we are unlikely to see a decline in 2025 versus 2024.

If we look at revenue recognized from current year bookings less price increases in 2022 it was $136.8M, 2023 $130.0M and 2024 $131.7M. Therefore, if we hold 2024 constant and add $40M we get ~$172M ( $10M higher than $162M in 2024 and versus management's guidance of $142.6M) for a total of $1,243M in 2025 revenue.

When framing 2025 revenue guidance it is important to consider that the Factset consensus revenue growth estimate had come down ~200bps to 25% or $1,206M by 2/9/2025 compared to 12/31/2024 ($1,225M Revenue).

The series of positive revisions in 2024 resulted in a narrowing of the surprise gap, leaving management with little room for upside.

Sitting here today, our above-consensus 2025 revenue growth estimate is only 2.3% / 1.8% above the mid / high-end of guidance (versus ~4% in 2024 and ~5% in 2025).

More importantly, we believe 2026/2027 revenue estimates are too high - especially given a $30M headwind to growth in 2026 due to lapping the 2024 price increase (See Exhibit A)

Stock Priced for Perfection

We view risk/reward as highly unfavorable to the long position. In order to justify the current valuation, Monday.com would have to maintain near 30% revenue growth through 2028 and the stock continue to trade at high end of its historical range of 8-12x EV/Sales.

We believe a combination of slowing customer growth and lapping price increases (~400bps contribution to 2024/2025 revenue growth) will put downward pressure on revenue growth closer to 20% in 2026 (includes 200-300bps annual growth contribution from cross-sell/product-mis). In this scenario, we believe the stock is likely to trade back down to a fair value range of $215 - $235/share.

It is worth noting that even in this scenario the implied multiple is still ~50x 2028 EBITDA - and 40% higher than where we believe the stock is worth based on our DCF valuation (~$150/share).

(See Exhibits F:I)

1

3

19

4,863

Nick Balch retweeted

11 Aug 2025

I get a lot of things wrong... but listening to the $MNDY call and folks freaking out over all the things we have been banging the drum on for the past year...

4

1

39

9,145

Nick Balch retweeted

30 Jul 2025

Love this - spent the better part of our $FIG call today on this point.

29 Jul 2025

At @Google, we are moving from a writing‑first culture to a building‑first one.

Writing was a proxy for clear thinking, optimized for scarce eng resources and long dev cycles - you had to get it right before you built.

Now, when time to vibe-code prototype ≈ time to write PRD, PMs can SHOW not tell. Role profiles are blurring, creativity and building are happening in parallel.

2

6

5,606