alt coins w/ pictures and internet friends @GomaFanClub @Wumbolabs

Joined September 2018

- Tweets 13,321

- Following 2,417

- Followers 5,912

- Likes 272,812

5,473 Photos and videos

MercedHees retweeted

Jun 12

4

7

29

296

MercedHees retweeted

Jun 3

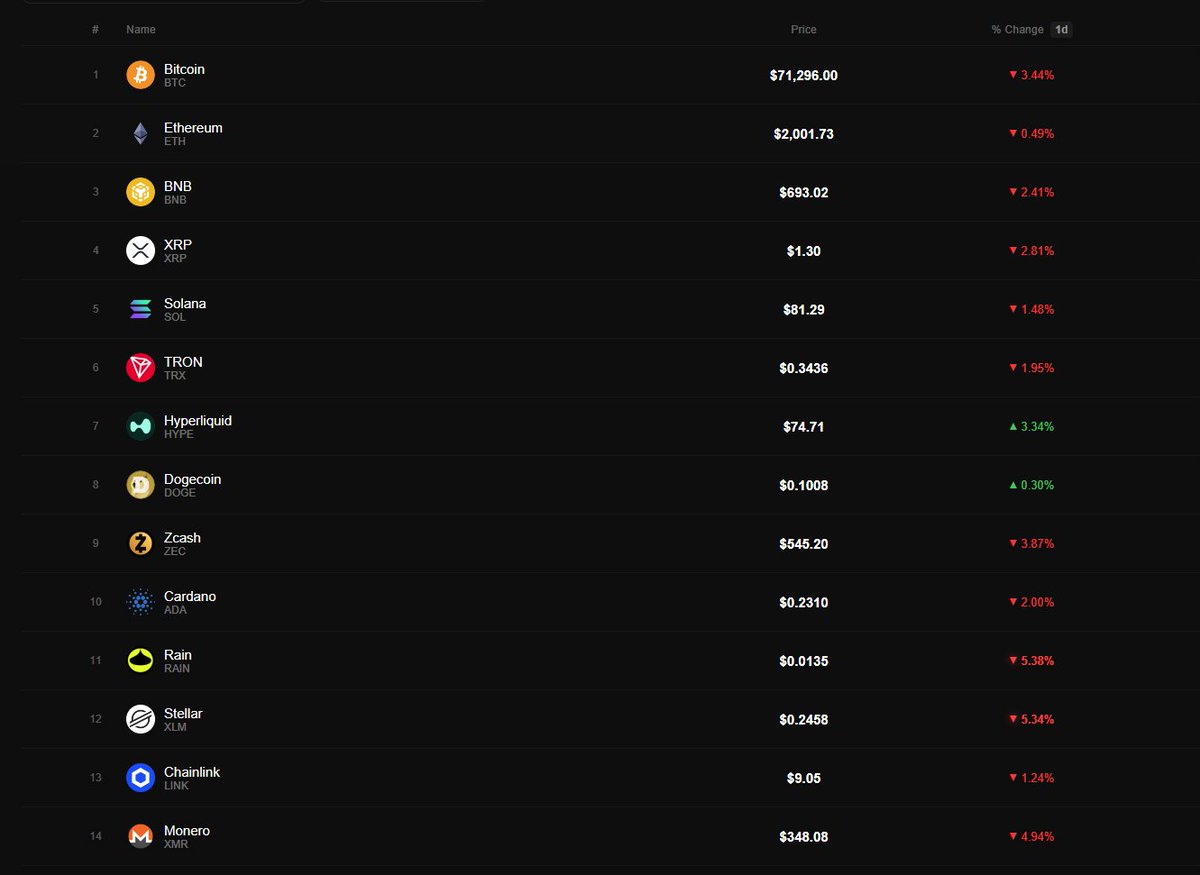

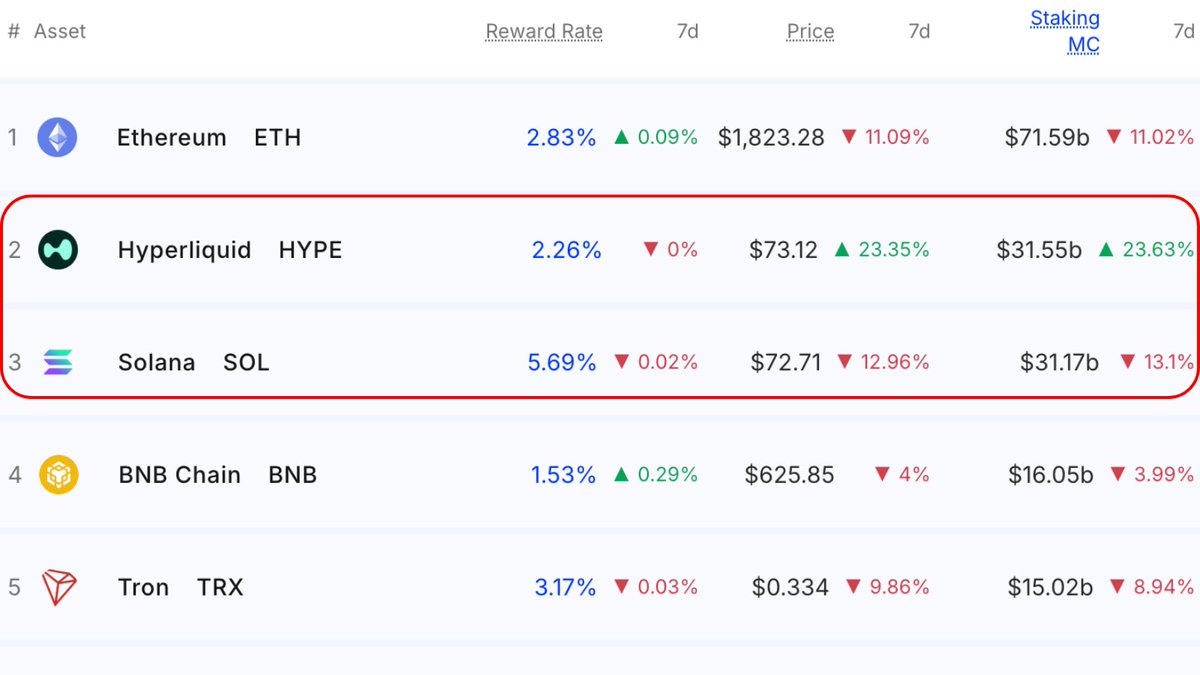

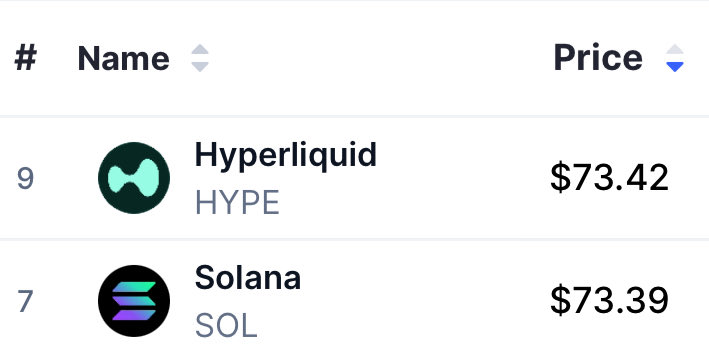

BREAKING: @HyperliquidX FLIPS @solana IN STAKING MARKET CAP - PER @StakingRewards DATA

SOURCE: stakingrewards.com/assets/pr…

21

35

237

32,556

1 to this

i was absolutely balls deep in SOL during most of the two previous runs, was the only ecosystem i knew and most of my net worth was in the token

this hype run feels v similar from an in group / out group point of view on CT. it is extremely obvious who is sidelined and who is enjoying

ppl wanted to just categorise solana as a shitty chain for poor ppl with bad investors that goes down all the time, but the economic activity and the dApps told a much brighter story

i had a friend who i even gave SOL to in 2022 and started a phantom to try get him to understand and he didn't even use it bc he was so convinced solana was shit

now ppl with hype are saying the same shit. it's just a DEX, where's the moat, regulation, hacking risk, competition

the worst thing you can do in crypto is have an unfalsifiable thesis, for those who were conservative on regulation imo you were somewhat falsified with the circle / coinbase announcement, or at least risk reduced. that was a signal to change thesis and still get a good entry, but many were already stuck in their opinion

the same is true with the perps approval in the US, that was a signal but those already stuck somehow paint new competition as bearish

there is finally a good product in crypto that is seeing mass adoption and literally disrupting global trade, if you're in this industry you want to see this product win

the other main thing ppl are midcurving is that whether a token goes up or down is solely determined by the buyers vs the sellers. there is substantial buy pressure that is hard-coded into the token and holders are still reluctant sellers, it does not take as much demand as you think it does for this thing to continue to send

if you don't own the coin, the very least you can do for yourself is to try not short it. there is a treasure trove of overvalued assets that deserve to be shorted, but the strongest asset of this year is not one of them

you may have missed out on the opportunity to make money but there's no reason to lose money on rage shorts

there is no hype beta

i love u

i remember dec '23 i got rekt shorting sol on that move from 70->90 because i wasn't onchain on sol and didn't understand it, so i thought the move was bs

imagine that'll happen here to a bunch of tourists/naysayers who don't understand whats happening, i see a lot of bad takes

17

30

298

50,658

MercedHees retweeted

May 29

[ ZOOMER ]

THE CFTC APPROVES PERPS TO OPERATE AND BE OFFERED TO US USERS: FILING

242

215

1,734

681,514

MercedHees retweeted

May 18

In the best way possible, Hyperliquid is starting to feel like a radical online cult building a digital cathedral for global finance.

It’s amusing seeing all these centralized crypto companies buy $HYPE to signal alignment to the community as if it’s tribute.

I don’t recall this ever happening with any asset other than $BTC.

Beyond the obvious flows benefit, the practical implication here is that an increasingly wide and powerful network of people and institutions in the crypto ecosystem are all highly incentivized to make Hyperliquid a massive success.

I honestly believe this dynamic wouldn’t exist if Hyperliquid didn’t do a fair launch and rekindle crypto’s original spirit.

My bet is this will remain a compounding advantage for Hyperliquid well into the future.

49

68

622

27,053

MercedHees retweeted

BREAKING: The SEC is set to release its so-called "innovation exemption" for tokenized stocks which will pave the path for trading digital versions of securities, per Bloomberg.

Details include:

1. In a "surprise move," the SEC is leaning toward allowing the trading of tokenized assets

2. These tokenized assets would be tradeable on decentralized crypto platforms

3. The move could "reshape the landscape of the American stock market"

4. This would also be one of the US' biggest shifts into crypto infrastructure yet

Tokenized assets are rapidly expanding.

520

1,429

8,607

1,587,607

MercedHees retweeted

May 17

SpaceX pre-IPO trading could very likely be another breakout moment for Hyperliquid.

HYPE ran up 70% from $22 -> $38 when SILVER was trading billions in daily volume earlier this year.

Now imagine how much attention Hyperliquid could get when it's the primary venue to trade the largest, most news-driven IPO of all time.

A potentially pivotal moment for Hyperliquid and all of perps.

May 17

T-minus 24 hours

26

23

374

50,574

MercedHees retweeted

May 15

Price dump 10% on the @zoomerfied tweet, but the article is a real goldmine. Bullish.

"Michael Selig, chairman of the CFTC, said at a conference in early May that Hyperliquid could “end up influencing the spot market price or the futures market price on our registered platforms.”

"Several traders told Bloomberg they watch weekend trading on Hyperliquid for cues on where prices may open"

"Don Wilson, the founder of DRW, a Chicago-based high-speed trading firm with more than 2,000 employees, said in an interview that his firm transacts on Hyperliquid through employees based abroad. He said that its growth will likely force the exchanges to change their business models."

"While the traditional exchanges have been raising concerns about Hyperliquid, US officials are also investigating suspicious activity on their platforms. The CFTC is probing well-timed trades in oil futures on CME and ICE’s platforms,"

Hyperliquid.

May 15

[ ZOOMER ]

CME AND NYSE ARE PUSHING THE US TO REGULATE HYPERLIQUID, DUE TO CONCERNS ABOUT MARKET MANIPULATION AND SANCTIONS EVASION: BBG

13

62

388

64,420

MercedHees retweeted

May 13

This is the most unique perps exchange design I've seen in a while. Particularly because of the $PAPER mechanism.

Here's how it works:

> @papertrade_xyz is a synthetic perps protocol on HyperEVM without fees, funding, or slippage.

> If you lose a trade, your full margin goes to the LP. If you win, you get paid but the protocol takes a fee on your gain - the fee is smaller for big moves, bigger for tiny moves. That haircut is the protocol's only revenue.

> The LP starts at $0. It fills purely from trader losses. If the LP can't pay a winner immediately, the payout enters an onchain FIFO debt queue and gets paid as the LP refills.

> Losing traders receive PAPER tokens. The lower the LP balance, the more PAPER you mint per dollar lost.

> PAPER can be staked to earn USDC dividends - a continuous cut of LP revenue. Once the LP exceeds $5M, all surplus gains go entirely to stakers.

> When the LP is low, emissions are high, so this is theoretically the time to accumulate PAPER cheap (also the riskiest period - if volume dries up, the LP doesn't earn any revenue and the whole flywheel breaks).

> When the LP is high ($5M), dividends are high, so this is theoretically best time to be staking.

> With sufficient volume, both states create buying/holding pressure on the token.

-----

Holding/staking $PAPER is essentially betting that traders will lose against the house, which is arguably one of the most reliable bets you can make (and a good hedge if you're a degen perps trader).

proud to introduce @papertrade_xyz - a fair-launched, fully-onchain perpetuals exchange built on hyperliquid by @izebel_eth & @blurr

-1000x leverage

-0 slippage

-No funding costs

-Self-bootstrapping LP

coming soon. learn more at: docs.papertrade.xyz

69

57

902

171,085

MercedHees retweeted

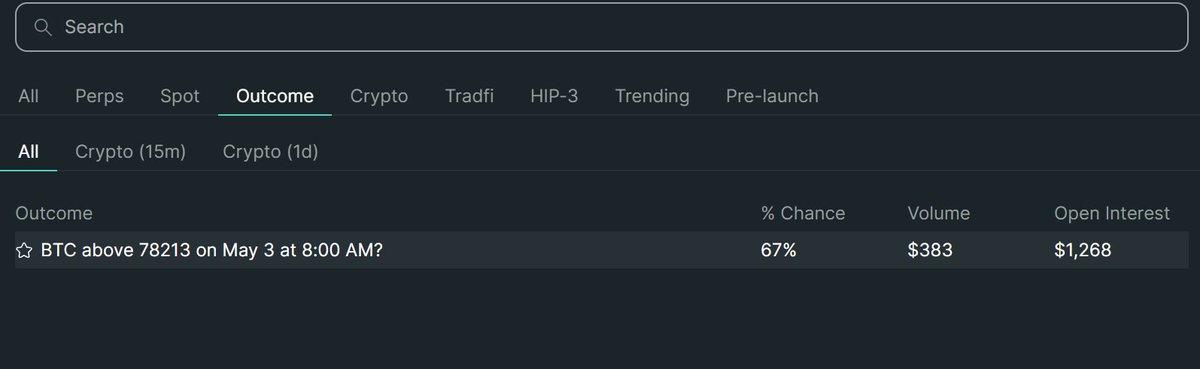

Outcomes (HIP-4) are now live on mainnet.

33

66

504

140,060

Introducing Pre-IPO Perpetuals (IPOP).

The weeks before an IPO are some of the most consequential in a company’s price history, and historically, the least observable. Private market quotes are stale and gated and Public markets haven’t started trading yet. Peak interest coincides with an absence of prices.

We’re introducing IPOP markets on XYZ to change that.

99

163

1,367

402,602

MercedHees retweeted

Apr 29

RT @/chumba

If you have a small pool of capital and insist on making it in public markets IMO you should be trying to find things that nobody else is talking about. Weird pockets of the market. Or things that are deeply hated where you have a variant view with conviction.

Niche securities that provide you with non recourse leverage. Over leveraged balance sheets where the equity value can change with small moves in enterprise value, and then figure out if the company survives, and buy non recourse leverage on that equity. Companies that have some ick associated with them where mass psychology has caused a mispricing.

----

the most money in markets is made in finding opportunities right before they become consensus longs, or in identifying the shift from non-consensus to consensus as it is happening and riding momentum

77

39

512

63,393

MercedHees retweeted

Apr 22

*Why your favorite TradFi firm launching perps won’t kill Hyperliquid*

Let’s establish this upfront. Perps are not just a simple payoff formula. They require a fundamental redesign of the exchange. The magic is in vertically integrating matching, margin, liquidation, and settlement into one continuous risk engine.

This provides the foundation for shared collateral pools, tight liquidation loops, 24/7 funding mechanisms, and 20-50x leverage. The resulting UX and capital efficiency is why perps decisively beat out dated futures and options products within crypto.

You can’t just “list perps” as if it were any other derivative. You have to reproduce the architecture. Coinbase has already demonstrated this empirically with their lackluster CFTC-regulated “perps” product despite plenty of talent and dollars thrown at it. As currently designed, they’re long-dated futures with 5-year expiries, 3-10x leverage depending on the contract, and funding that only settles twice daily.

Compare that to unregulated offshore venues like Binance or blockchains like Hyperliquid and it’s obvious why the product has underwhelmed. If Coinbase can’t figure it out, why should Kalshi or Polymarket, which have worse distribution for this product? If Coinbase as the most crypto-native regulated U.S. venue can’t deliver a compelling product, why should CME or ICE?

The reality is that U.S. regulated incumbents have been sidelined from truly competing. Dodd-Frank and the Commodities Exchange Act mandate centralized clearing, and separation between the different layers of the trading stack. This fragmentation structurally prevents the vertical integration necessary for real perps to work. And even if they didn’t, incumbents would still likely have regulatory limits on the amount of leverage they can offer to retail.

Fixing all this requires a full regulatory overhaul and infrastructure rebuild. HOOD and IBKR pumping out whatever subpar product their underlying exchange lists wouldn’t change the problem.

But regulation can change right? At a conference in March, CFTC Chairman Michael Selig suggested that the agency would allow perps for crypto soon. While CME and ICE may not have the right infrastructure in place to flip on perps anytime soon, Coinbase, Kalshi, and Polymarket could in theory offer real perps on crypto within weeks of formal guidance dropping. In fact, it is my full expectation that both Kalshi and Polymarket's upcoming perps products will be real perps with no expiry, unlike what Coinbase offers.

What then would be the advantage of decentralized venues like Hyperliquid if everyone was now on a more level playing field?

Well for one U.S. guidance would likely only be for crypto perps, not the equity or commodity perps which are the fastest growing segment of the market. They also might not remove limits on retail leverage.

But let’s just ignore these qualifications for now and assume that there’s simultaneously 1) no regulatory advantage for offshore venues anymore and 2) decentralized venues still cannot legally offer perps to U.S. retail users (despite the CFTC also working towards creating a pathway for this).

There’s a handful of long-term advantages decentralized venues like Hyperliquid have.

1) DEXs are structurally cheaper as they do not maintain fiat banking rails, large compliance teams, regional subsidiaries, customer support, or extensive custody and treasury operations

2) DEXs are permissionless, which provides significant scaling advantages over incumbents as anyone can launch and distribute new markets, creating a virtuous utility-and-distribution flywheel

3) DEXs are intrinsically global, enabling them to reach anyone on Earth so long as they have an internet connection

4) DEXs offer users substantially lower counterparty risk as they are real-time auditable and enable users to self custody their funds

And none of this is to mention the bigger picture concept that Hyperliquid isn’t just a perps venue anymore. Rather it’s a full-fledged platform where traders soon be able to cross-margin perps, options, predictions, and tokenized equities in a unified experience. Incorporating all of this into a single risk engine takes years of iteration and refinement, and a baseline level of liquidity across all markets.

x.com/RyanWatkins_/status/20…

With all this in mind, who do you think is best positioned to execute on this product? Is it really the regulatorily constrained, technologically disadvantaged, incumbents that have zero experience building this product? Or is it the pioneering team with breakneck product velocity and years of experience both trading and building these products?

It’s not wrong to worry about competition. I do expect TradFi firms will offer decent products over the coming quarters and help grow the market.

But eventually decentralized venues will be made legal in the U.S. too and their superiority will be proven over time. So the big question in my mind is not whether TradFi will win, it’s whether another blockchain like Solana, Lighter, or Base builds a better product, or if Hyperliquid will stay the king.

Time will tell.

Apr 9

Once you realize Hyperliquid is building the everything exchange, and cross-margin brings it all together, you realize that every other competitor is playing a much narrower, far less defensible game.

On Hyperliquid, perps, spot, options, predictions, RWAs, and related markets are not separate products so much as expressions of a single, unified trading experience powered by a shared risk engine.

At scale, the resulting liquidity and capital-efficiency flywheel should produce a winner-take-most market structure, leaving those who didn’t see the bigger picture fighting for scraps in siloed markets.

Excerpt below on the approaching $HYPE endgame over the coming years.

44

52

391

81,511

The Arbitrum Security Council has taken emergency action to freeze the 30,766 ETH being held in the address on Arbitrum One that is connected to the KelpDAO exploit. The Security Council acted with input from law enforcement as to the exploiter’s identity, and, at all times, weighed its commitment to the security and integrity of the Arbitrum community without impacting any Arbitrum users or applications.

After significant technical diligence and deliberation, the Security Council identified and executed a technical approach to move funds to safety without affecting any other chain state or Arbitrum users.

As of April 20 11:26pm ET the funds have been successfully transferred to an intermediary frozen wallet. They are no longer accessible to the address that originally held the funds, and can only be moved by further action by Arbitrum governance, which will be coordinated with relevant parties.

1,779

1,011

7,076

5,449,726

MercedHees retweeted

Apr 9

Once you realize Hyperliquid is building the everything exchange, and cross-margin brings it all together, you realize that every other competitor is playing a much narrower, far less defensible game.

On Hyperliquid, perps, spot, options, predictions, RWAs, and related markets are not separate products so much as expressions of a single, unified trading experience powered by a shared risk engine.

At scale, the resulting liquidity and capital-efficiency flywheel should produce a winner-take-most market structure, leaving those who didn’t see the bigger picture fighting for scraps in siloed markets.

Excerpt below on the approaching $HYPE endgame over the coming years.

34

79

470

36,152

Technorevenant, one of the biggest individual HYPE holders, unstaked 2.42M HYPE ($95M) on April 1.

hypurrscan.io/address/0x179f…

He sold a small amount to short HYPE and long XRP, SOL, and ETH, even traded a random coin called PENIS on Hyperliquid.

Then restaked the full amount on a new wallet.

hypurrscan.io/address/0x4eb8…

HYPE pumped over 3% right after, as a lot of people were watching his wallet and waiting to react.

Happy april fools.

61

50

671

83,536

MercedHees retweeted

Apr 8

125

231

1,045

479,209