Head of Savings & Retirement at @avivaplc ... runner, cycler, golfer and tenor. My views. alistair.mcqueen@aviva.com

Joined September 2012

- Tweets 16,479

- Following 1,585

- Followers 2,573

- Likes 10,691

2,909 Photos and videos

Pinned Tweet

23 Apr 2023

That was fun! Great to talk about work, life and pensions with the brilliant Jack Parsons of the brilliant Youth Group. @JacksonRParsons @TheYouthGroupHQ

youtube.com/live/NYRB6iJ04R4…

1

1

7

2,220

Alistair McQueen retweeted

My Times piece: It is right to worry about Neets, and high youth unemployment and inactivity. But we should not forget about the over-50s, many of whom are also locked out of the job market:

Older workers may be overlooked solution to inactivity crisis

thetimes.com/article/79a8a35…

5

9

11

1,760

Alistair McQueen retweeted

May 27

Blair putting on full display what is in many ways his special ability - to lay out a political argument grounded in his own view of global trends (globalisation in the 2000s, tech in the 2020s). But…

107

102

560

321,970

Alistair McQueen retweeted

May 20

30 years of 30 years of hurt

"Three Lions" was released on 20th May 1996. 30 years ago today! 🦁🦁🦁

34

381

9,872

674,596

Alistair McQueen retweeted

Over 70 million pension records are now connected to the pensions dashboards ecosystem representing around 85% of records in scope 🔌

Connections will continue as we head towards to final connection deadline on 31 October 2026.

2

1

153

Alistair McQueen retweeted

May 18

Pleased to see our @TheIFS work being highlighted by the Pensions Commissioners in @guardian coverage today.

The research was commissioned by @DWPgovuk to inform the Pensions Commission, and looks at how working lives shape pension saving and outcomes.

theguardian.com/money/2026/m…

NEW: A gender gap in the average pension contributions of men and women opens at the time of the birth of their first child, our new research finds.

The @DWPgovuk report for the Pensions Commission provides new evidence on how labour market life-course trajectories link to pension saving and retirement outcomes:

1

3

3

9,552

Alistair McQueen retweeted

May 18

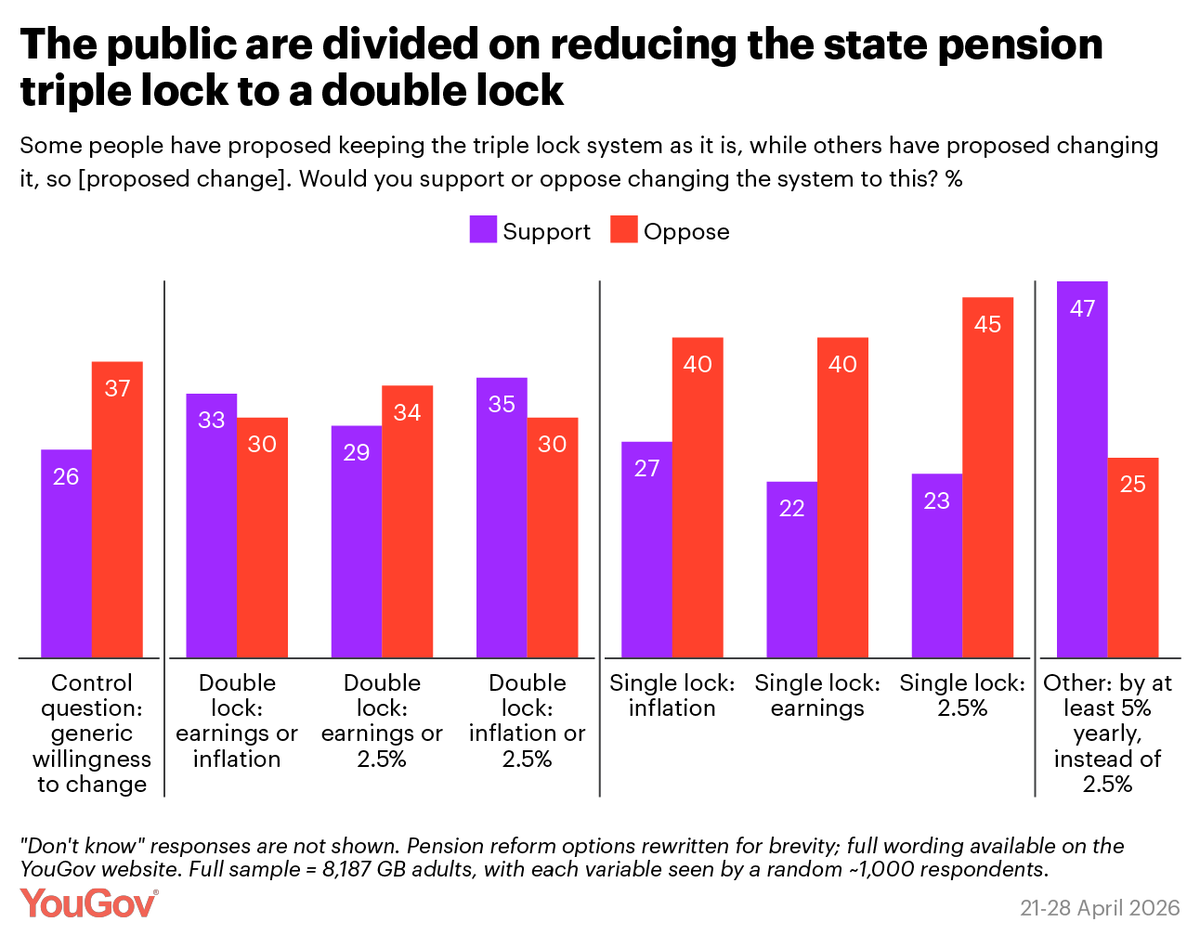

Fascinating polling on the triple lock

The higher popularity of a double lock with inflation or 2.5%

Rather than a double lock of earnings or 2.5%

Does not suggest much confidence in our growth prospects

Net public support for changing the triple lock…

In general (control Q): -11

To a double lock…

Inflation/2.5%: 5

Earnings/inflation: 3

Earnings/2.5%: -5

To a single lock…

Inflation: -13

Earnings: -18

2.5%: -22

Other

Changing the 2.5% to 5%: 22

yougov.com/en-gb/articles/54…

1

1

5

1,454

Alistair McQueen retweeted

May 14

Q1 2026 G7:

🇬🇧 0.6%

🇺🇸 0.5%

🇨🇦 0.4%

🇩🇪 0.3%

🇮🇹 0.2%

🇫🇷 0%

🇯🇵 (not yet reported but estimates are 0.4%)

130

809

2,867

652,137

Alistair McQueen retweeted

May 14

A very strong start to 2026 -significantly above forecasts. GDP/capita rose 0.6% in first three months of 2026 (@OBR_UK expected gdp/capita to grow by 0.8% in 2026 as a whole)

GDP grew 0.6% in Quarter 1 (Jan to Mar) 2026.

Services ( 0.8%) construction ( 0.4%) and production ( 0.2%) all increased.

Read the full article ➡️ ons.gov.uk/economy/grossdome…

ALT GDP growth in the UK January to March 2026 GDP up 0.6% Services up 0.8% Production up 0.2% Construction up 0.4%

193

316

999

144,059

RT @avivaplc: 🎯Aviva has delivered another quarter of strong trading, building momentum in 2026.

Here are the headlines from our first qua…

2

Alistair McQueen retweeted

May 13

HUGE jump in US PPI inflation:

Powered by an eye-popping 1.4% rise in April, nearly triple the 0.5% consensus, the annual rate has hit 6% (crushing the 4.8% consensus forecast).

Core PPI followed suit, surging 1% (vs. 0.3% expected), bringing annual core inflation to 5.2% (consensus was 4.3%).

While the mapping isn't 1:1, these numbers strongly suggest that higher consumer inflation is still coming through the pipeline.

#economy #markets #inflation

106

405

1,419

184,657

Alistair McQueen retweeted

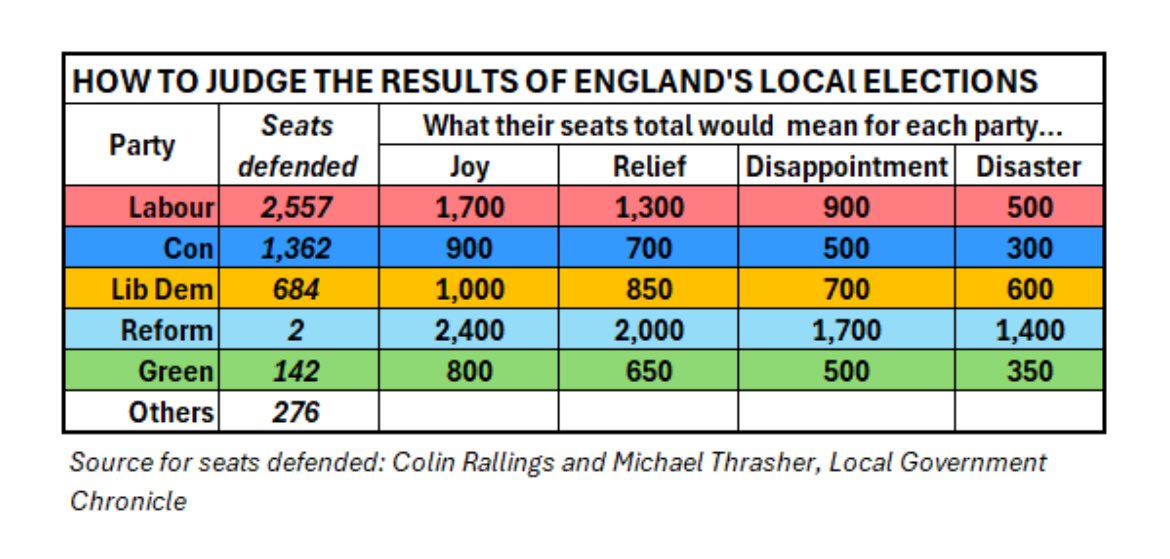

If we go back to this Peter Kellner chart, how should the parties be feeling about these local elections?

Lab = Disappointment

Con = Relief

Lib Dem = Relief

Ref = Disaster

Green = Disappointment

May 1

Peter Kellner has this v useful guide on how to judge the English council election results for each party

85

166

774

242,365

Alistair McQueen retweeted

May 6

“Thanks Martin, I found a lost pension from when I was 22, it’s now worth £45,000!” So can you do what Rose did? Martin shows you how to check…

This is just a snip from the full Martin Lewis Money Show Pensions Special watch it on ITVX

35

232

1,843

731,189

Alistair McQueen retweeted

May 5

Why society needs to rethink attitudes towards retirement and what actually constitutes a working life - words from me in today’s edition of @TheTimes:

thetimes.com/article/7148248…

1

4

1,411

Alistair McQueen retweeted

Apr 30

This one is for the niche audience that wants more charts in politicians’ speeches… offered some reflections on the economic lessons of the shock that we sadly find ourselves in for @ucl inaugural Annual Lecture in Economic Policy ucl.ac.uk/policy-lab/news/20…

12

9

32

6,716

Alistair McQueen retweeted

Apr 29

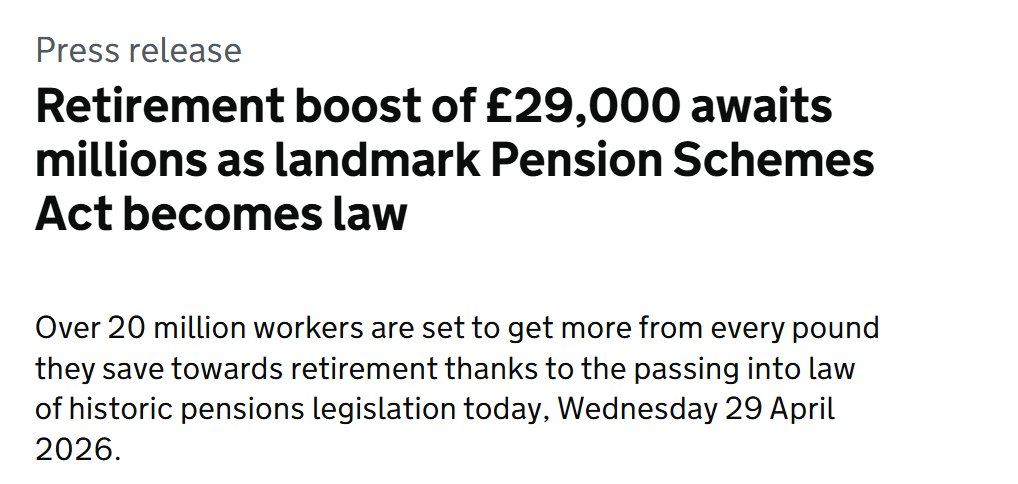

DWP's press release about the Pension Schemes Bill delivering a "retirement boost of £29k" is absurd for obvious and non-obvious reasons.

First, the obvious part.

- The projected £29k boost is an average, not a uniform uplift, and is based on a whole career. (So today's workers would on average benefit less, as would those who don't have full careers).

- The £29k is calculated using highly uncertain assumptions around several overlapping policies. DWP's impact assessment says "the actual benefits will differ for all savers and may be higher or lower."

- A little over half of the £29k comes from the value-for-money regime. DWP gave this policy a "red, high impact" rating for "analytical risk", noting that "small changes in returns would significantly impact monetization (due to compounding) and future returns are highly uncertain".

But a quirk of the calculation makes suggestions that £29k is a meaningful figure for most workers even less appropriate. The value-for-money regime is assumed to boost average returns by forcing the worst-performing schemes out of the market. That doesn't affect savers in other schemes. So more than half of the "£29k comes from a weighted average of "zero" (most people) and "lots" (some people).

And what does "£29k" mean when we're looking decades ahead? DWP's estimate is in today's earnings terms - so, on assumptions about earnings growth outsripping inflation, the £29k that people would benefit from would buy more than twice as much as £29k does today. On the other hand, this is a boost to the value of pension pots from which withdrawals are mostly taxable. So the boost to retirees' spending power would be <£29k (in today's earnings terms).

I can only presume that someone in DWP's press office keeps insisting that they need a number to sell the story, and "there are good reasons to think that this package of measures will improve outcomes but how much is highly uncertain" isn't a strong enough line.

For context, on DWP's assumptions, the £29k is a roughly equivalent effect to increasing default contribution rates from 8% to 9.5%, but without the pain of paying more. So it's well worth trying to do that - but preferably without pretending that gains of this magnitude are nailed on.

2

7

735

Alistair McQueen retweeted

Apr 28

Very good news tonight. The Pension Schemes Bill has completed its journey through Parliament. Time to celebrate before the really important work begins - implementing the huge reforms it contains to deliver better pensions for savers

Apr 16

We’ve got a pensions bill entering its final stages. This is important stuff - one of the big wins of the 20th Century was ordinary workers having a retirement, and we need to keep delivering that in the 21st. What’s the bill doing?

124

77

258

52,442

Alistair McQueen retweeted

Apr 16

We’ve got a pensions bill entering its final stages. This is important stuff - one of the big wins of the 20th Century was ordinary workers having a retirement, and we need to keep delivering that in the 21st. What’s the bill doing?

67

21

91

67,057

Alistair McQueen retweeted

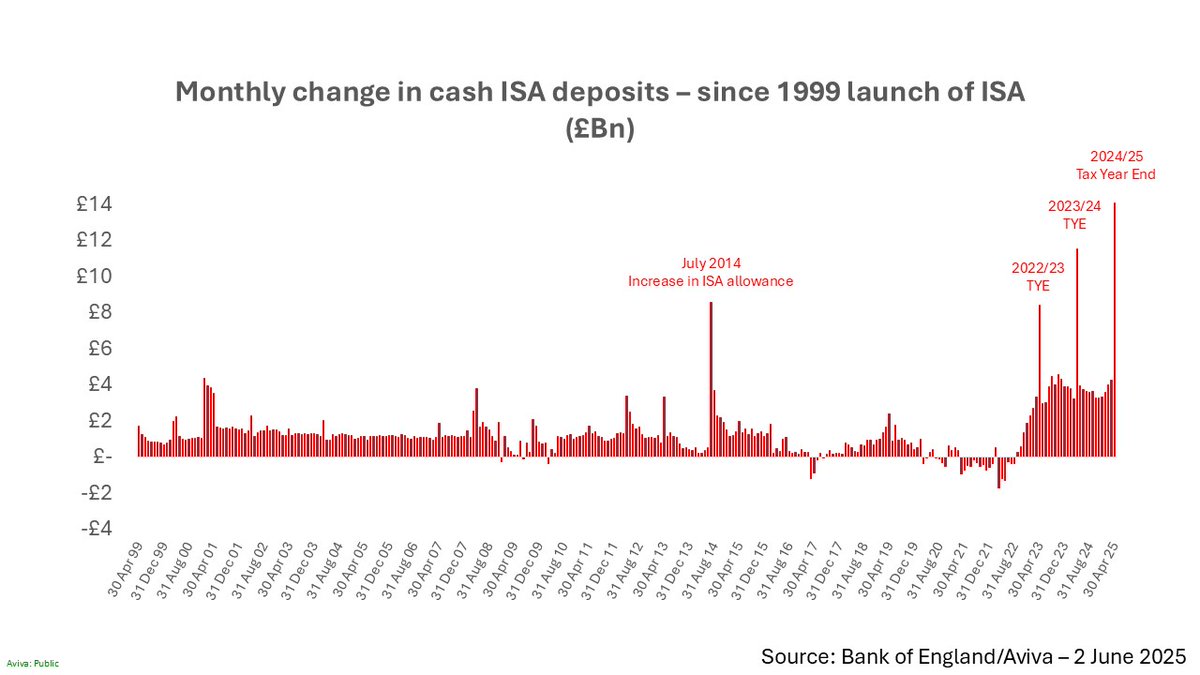

Mar 31

Cash ISAs (Individual Savings Accounts) pay #interest, free of Income Tax. Find out how they work, how to open one and if they're right for you by clicking onto the link within our @MoneyHelperUK tweet below. ⬇️

#Savings #IncomeTax #TalkMoney #CashISA

Mar 31

If you’ve got cash savings, using a Cash ISA before the tax year ends could help you keep more of your interest tax-free. It’s worth checking your options before the deadline.

👉 ow.ly/g1RF50Yy1T5

#CashISA #Savings #TaxFree #MoneyManagement

1

1

153

Financial inclusion – We’re all in this together

moneymarketing.co.uk/opinion…

1

3

123

Alistair McQueen retweeted

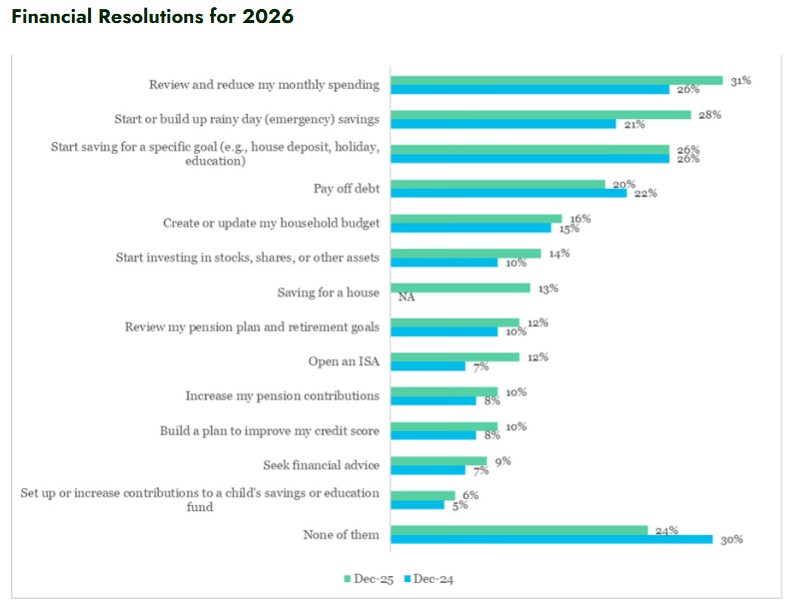

#Pension contributions move up the priority list for 2026, @PensionsUK_ ..The start of a new year is the perfect time to reset financial goals. While everyday needs often take priority, it is encouraging to see people increasingly willing to take action... tinyurl.com/58apyyua

1

948