1,199 Photos and videos

Hexer 🧠 retweeted

Jun 13

The US government, citing national security authorities, has issued an export control directive to suspend all access to Fable 5 and Mythos 5 by any foreign national, whether inside or outside the United States, including foreign national Anthropic employees.

The net effect of this order is that we must abruptly disable Fable 5 and Mythos 5 for all our customers to ensure compliance.

Access to all other Claude models is not affected.

We apologize for this disruption to our customers. We believe this is a misunderstanding and are working to restore access as soon as possible.

Read our full statement: anthropic.com/news/fable-myt…

12,537

25,757

87,949

89,734,416

Now it is

Mar 30

If Claude Code was OSS, the community could help fix this.

If you could use your Claude Code subs in other harnesses, we could help much more with diagnosing.

Instead, we just deal with the consequences of the black box: worse code, no insights, endless pain

31

1) what

Feb 24

We rebuilt Next.js in a week. No, really.

The team ported the framework to run natively on Workers to prove what’s possible with edge-first architecture. Dive into the technical hurdles we solved to eliminate Node.js dependencies.

cfl.re/4ciNc3L

38

Hexer 🧠 retweeted

22 Sep 2025

Generating Alpha in All Market Conditions: A Quantitative Approach to Tokenomics-Driven Pairs Trading

1/7

A quantitative, market-neutral strategy can generate alpha irrespective of market direction. The thesis is to construct a pairs trade based on fundamental tokenomic divergences: long a deflationary asset with revenue-driven buybacks, and short an inflationary asset with significant insider token unlocks.

2/7

The long position targets protocols with "Real Yield." These projects allocate substantial protocol revenue to programmatically buy back their native tokens. This mechanism creates a deflationary force by reducing circulating supply and providing constant, structural buy-side pressure, directly linking protocol success to token value.

3/7

The short position targets protocols with predictable inflationary headwinds. Empirical analysis of over 16,000 token unlocks reveals a clear pattern: ~90% of events create negative price pressure. Unlocks designated for teams are most detrimental, correlating with an average price drop of -25%.

4/7

An archetypal pair would be Long HyperLiquid ($HYPE) vs. Short Arbitrum ($ARB). Hyperliquid utilizes ~97% of its substantial trading fees for automated $HYPE buybacks. Conversely, Arbitrum's tokenomics include a multi-year linear vesting schedule for insiders, creating persistent, predictable supply pressure

5/7

Execution requires specific instruments. Perpetual futures offer capital-efficient long/short exposure without expiration. A cross-margin account is strategically imperative; it pools collateral across all positions, allowing unrealized profits from one leg to offset losses on the other, thus preserving the hedge and preventing premature liquidation of a single leg.

6/7

A systematic framework for implementation and risk management:

• Position Sizing: Positions must be dollar-neutral at entry to eliminate market beta.

• Entry/Exit Signals: A rolling z-score of the pair's price ratio can identify statistically significant deviations for trade entry and mean-reversion exits.

• Risk Mitigation: A stop-loss must be applied to the spread itself, not the individual asset prices, to protect the core thesis from invalidation.

7/7

This strategy exploits a quantifiable market inefficiency: the asymmetric pricing of slow, cumulative deflationary pressure versus sharp, predictable inflationary shocks. The objective is to achieve a high Sharpe Ratio, indicating superior risk-adjusted returns that are fundamentally uncorrelated with the broader digital asset market.

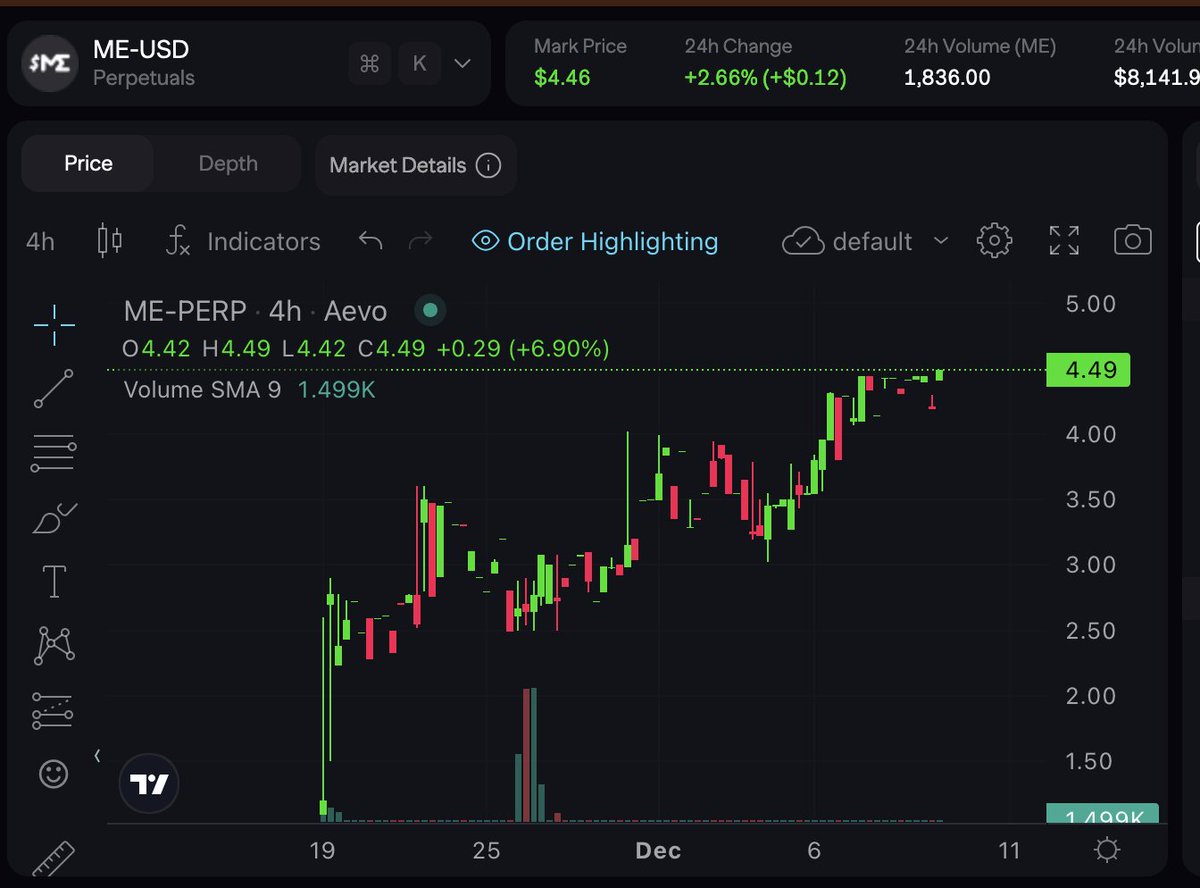

big thank you to @hansolar21 I mainly traded isolated margin till the point I first saw his perp account on @Lighter_xyz and then I realised portfolio optimisation is so much easier with cross margin if you understand Market Neutral Positions, up 6 figures since and sharpe ratio at 5, since I trade market neutral

1

3

15

743