Joined March 2026

- Tweets 1,567

- Following 37

- Followers 104

- Likes 29

77 Photos and videos

21h

1/9 🧵

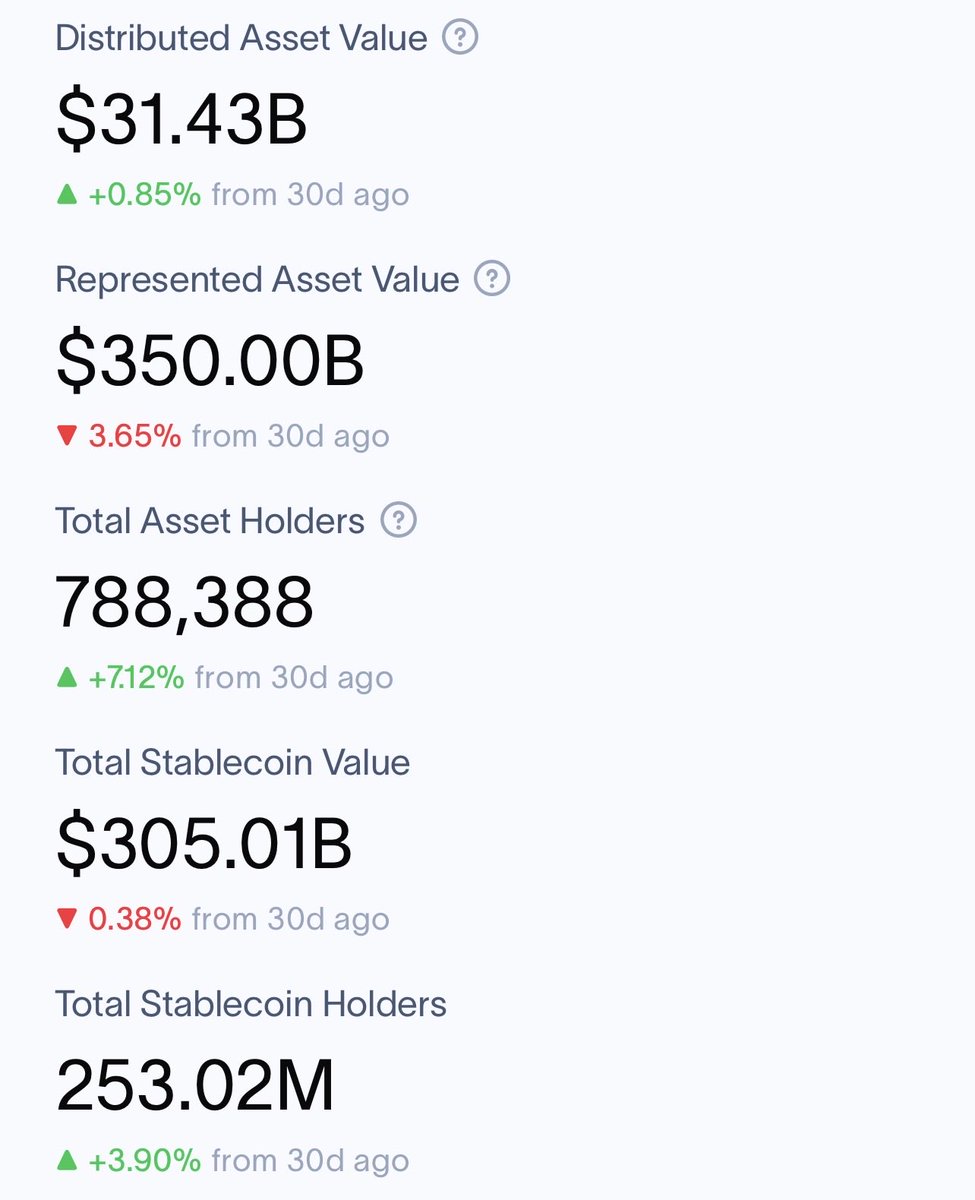

The biggest alpha in private markets isn’t another tokenization narrative.

It’s a global bank turning private company shares into natively on-chain assets with real regulated custody and settlement — live today.

Citi just fired the starting gun. The institutions that move in the next 12 months will own the new rails. Everyone else will pay to access them later.

2

6

66

21h

8/9

Two realistic outcomes in the next 18–24 months.

Best case: DDRs become the default regulated wrapper for private shares. Multi-institution, cross-border transfers happen seamlessly on-chain with bank-grade custody.

Base case: it stays a high-quality niche used by sophisticated issuers only.

Either way, the institutions collecting data, relationships and tech around these rails today will have the structural edge.

The rest will be explaining why they watched from the sidelines.

3

2

29

21h

9/9

Bottom line: regulated on-chain private share infrastructure is no longer a future story.

Citi Kaleido delivered the first live proof point this week.

The alpha concentrates where regulated banks control the new digital custody and settlement layer.

The urgency is real — the adoption curve starts now.

What are you watching most closely: number of new DDR issuers, or actual settlement volume?

Which sector do you expect the next DDR in?

Reply with your take.

#RWA #OnChainRWA #PrivateMarkets #InstitutionalAlpha #MarketStructure

1

36

Jun 12

1/7

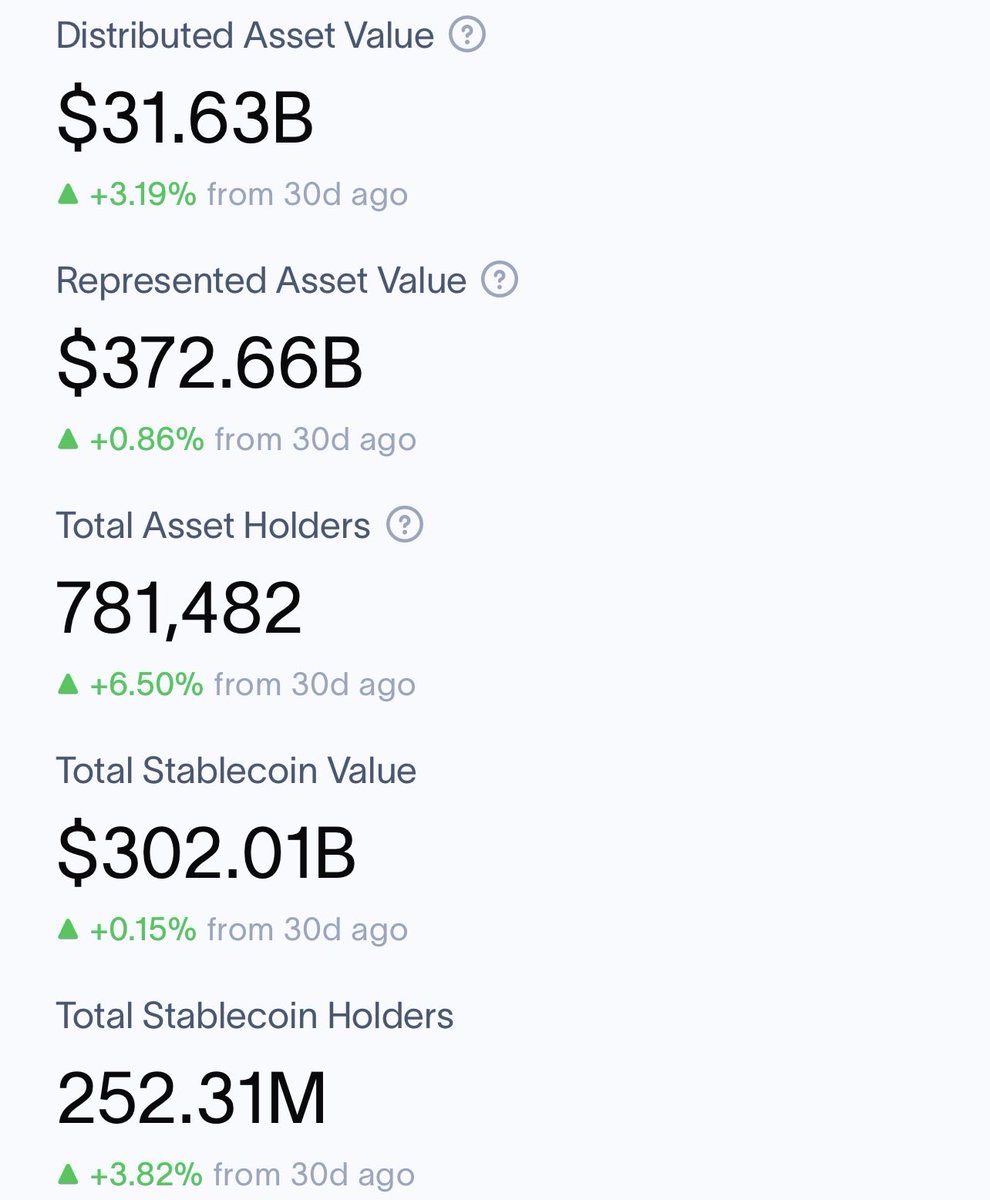

Solana DeFi is no longer just a playground for memes and degen yields.

It is quietly becoming the liquidity hub for real-world private credit.

This isn’t another tokenization hype cycle. It’s a structural shift: real credit is moving from off-chain institutional allocation directly into Solana’s composable DeFi liquidity layers. Data and architecture both confirm it.

The last 30 days have already given a clear signal. If this pathway keeps strengthening, Solana becomes the primary battlefield for tokenized private credit. The window is open right now — watching it form is smarter than chasing it later. 👇

4

3

166

Jun 12

6/7

Two possible outcomes — the data will decide:

If the mechanism strengthens: Private credit origination feeds directly into Solana-native yield markets, creating a parallel, more efficient route for capital formation and liquidity distribution outside traditional channels.

If it stalls: Activity stays concentrated in a limited set of wrappers, generating noise without building broader ecosystem routing effects.

The deciding factor remains the same: whether net inflows and credit-RWA participation continue expanding in tandem.

My clear view: Solana is using real data and clean architecture to seize the high ground in tokenized private credit flowing into DeFi. This isn’t hype. It’s a paradigm shift in how credit capital forms and moves. 👇

2

2

29

Jun 12

7/7

Why this matters right now:

The last 30 days have validated the trend. The next 1–2 months of inflow data will determine whether this story accelerates or fades.

Retail gets access to real institutional yields. Originators get efficient on-chain distribution. Solana gets sustainable, real-world activity. A genuine three-way win — and the window is narrowing.

What do you think?

Will net inflows into these credit products keep accelerating? How big a gap do you see this creating for Solana in the RWA race?

Drop your take in the comments — or share the protocols and indicators you’re watching. Let’s track it together.

#RWA #SolanaDeFi #TokenizedCredit #RealYield #PrivateCredit

#RWAPerps

16

Jun 11

1/7

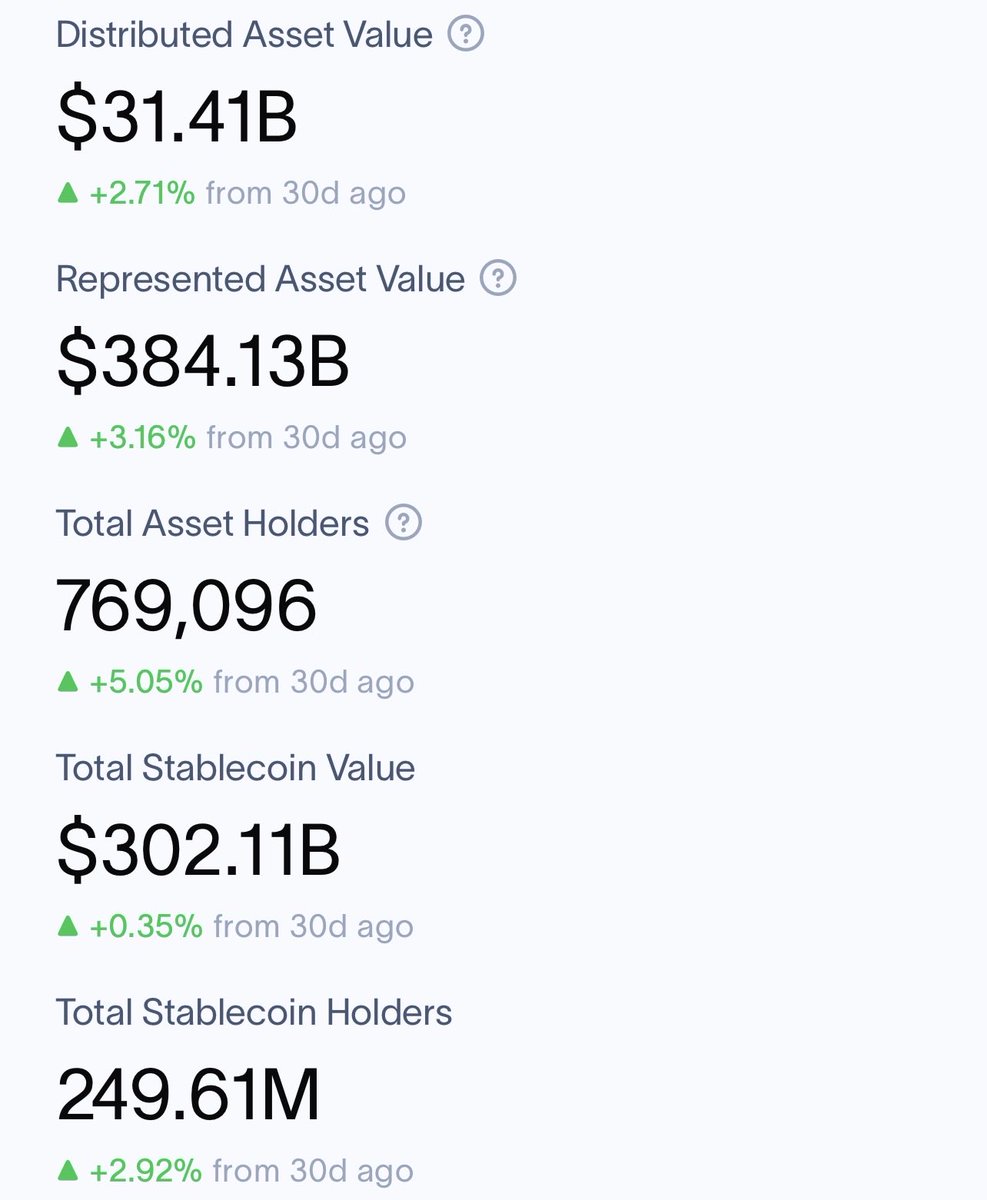

Figure just paid $717 million to acquire Kiavi.

This is not another RWA headline — it is the clearest signal yet that on-chain credit is moving from “tokenize assets after they exist” to originate credit natively on-chain.

Figure takes Kiavi’s origination technology and operating platform. A joint venture with Sixth Street takes the loan book. The result: over $7 billion in annual loan production and more than $100 million in monthly flow now flows directly into Figure’s blockchain-native infrastructure and its Democratized Prime marketplace. Figure already controls roughly 75% of the current RWA tokenization market.

The message is simple: the future belongs to whoever controls credit creation at the source.

1

1

16

Jun 11

6/7

Historically, financial infrastructure upgrades almost always started downstream (distribution, settlement, securitization) while origination stayed in traditional hands.

Early RWA growth followed the same pattern: tokenize existing assets after they were already created.

The Figure–Kiavi deal breaks this pattern by targeting the source of credit production. It looks less like simple asset expansion and more like vertical infrastructure consolidation at the root of the credit system.

1

8

Jun 11

7/7

If this model continues to strengthen, on-chain credit markets will increasingly look like vertically integrated systems where origination, underwriting, funding, tokenization, and trading all operate inside one framework.

If the alternative path wins, origination platforms will keep producing assets at scale while tokenization remains mainly a distribution tool with limited influence over actual credit formation.

My view: The vertically integrated path is winning. The players who control origination will set the rules for on-chain private credit over the next decade.

Do you see more traditional lenders accelerating on-chain integration, or will pure on-chain players start moving upstream into origination? Drop your thoughts below 👇

#RWA #OnChainCredit #TokenizedCredit #PrivateCredit #CreditCreation #Figure #RealWorldAssets

#RealYield #InstitutionalFlows #RWAPerps

7