Joined November 2019

- Tweets 227

- Following 61

- Followers 10,876

- Likes 161

17 Photos and videos

Pinned Tweet

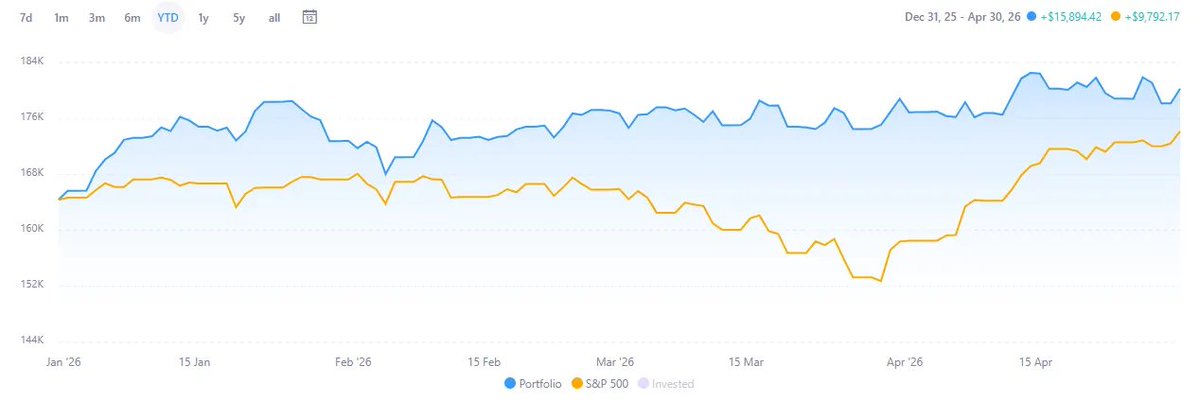

May 4

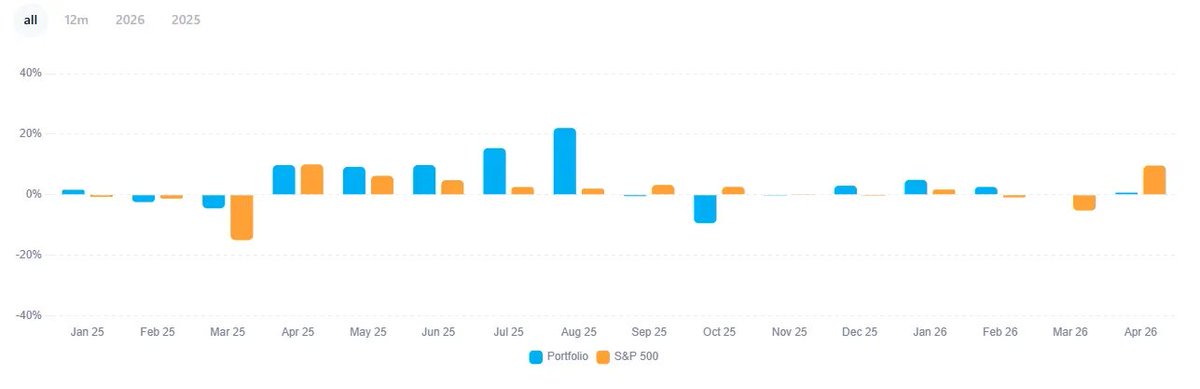

9.49% YTD after returning 64.3% in 2025. April was an incredible ride for the indexes — not so much for us. We didn't suffer much in March because we were defensive, but that also means the recovery wasn't as strong.

Every month I review every position, share management call takeaways, and give an honest read on the macro. No spin, no narrative protection — just what's working and what isn't.

If that sounds interesting, check out Undervalued and Undercovered

2

2

33

14,777

Jun 12

SpaceX seems really undervalued on a vibes-to-price ratio.

Out of jokes, SpaceX has some of the best ingredients for a great IPO. Probably not to produce long-term value, but excited retail that couldn't get enough shares on their brokers will buy the rest at open. Nasdaq inclusion in 15 days could create a short-term catalyst narrative, and if the Iran peace holds, the momentum could carry until insiders start to cash out.

1

2

1,074

Jun 8

Healthcare pick at 25% FCF yield with high DD growth ahead.

$CCLD is a US healthcare revenue cycle management business on the surface. The thesis is not about the RCM software, it is about the acquisition engine sitting on top of it.

CCLD acquires struggling regional billing firms at 0.6-1x revenue and lifts their operating cash flow margins to 20-30% within two to three quarters, by migrating those practices onto its own platform and stripping duplicate cost.

They are not buying these businesses for their profits. They are buying the customers. Churn in this industry sits around 5% a year, so once a clinic has handed over its billing it almost never switches. That makes an acquired customer cheaper to obtain than an organically marketed one.

The market still anchors to the messy 2022-2024 tape (preferred-stock dilution, missed numbers, the restructuring), and the broader software selloff has pulled the stock back to the level it traded at before any of the recent execution was proven.

At around a 25% FCF yield on current run-rate, with NOLs shielding taxes for years and a clear path to high double-digit growth from M&A alone, this is a serial acquirer being priced for decline.

4

3

41

5,584

Jun 7

Buffett ran his first partnership at 26.

Ackman launched Gotham at 26.

At 19, today I get my chance to start.

I have joined Sapphire Capital EAF as Fund Advisor of PEQUITY U&U Global Opportunities, FIL. The strategy I have been writing about on Undervalued and Undercovered for years now has real money behind it.

49

26

923

622,285

May 29

New metric for AI companies: PBT (Profit Before Tokens).

13

7,955

May 29

New metric for AI companies: PBT (Profit Before Tokens).

Tax expenses are meaningless for these companies. They hacked the tax system. If they blow all their money on tokens, they replace paying taxes.

2

2

24

7,270

May 27

Enviri Corporation ($NVRI), a $3B special situation closing June 1, 2026 where the real opportunity is the stub left behind. Veolia is buying Clean Earth for $3.04B all-cash. Shareholders receive $15 per share plus 0.33 shares of New Enviri (two industrial businesses: steel-mill services rail). At today's NVRI price, the market is paying just 4.5x EBITDA for that stub. Peers trade at 7-8x. Strategic buyers have paid 12.5x for similar rail assets.

Here's why this could be a multibagger:

After four years of crushing pressure on European steel, the cycle is turning. EU 2025 crude steel production hit 125.8 Mt, ~20% below pre-pandemic. Harsco Environmental margins compressed from a 20.3% peak in FY21 to 16.9% in FY25. The market is treating this as the new normal. It isn't. CBAM's definitive phase went live January 1, 2026. EU steel safeguards take effect July 1, with a 47% quota cut and a 50% out-of-quota tariff. ArcelorMittal (HE's largest customer) said in its Q3 2025 release these measures "can provide a solid foundation for our European business to earn its cost of capital."

Inside the stub. Harsco Environmental: a 173-year-old on-site steel-mill services business. 25-year average customer relationship, 85% renewal rate, 50% EAF customer mix (insulated from the BF/BOF terminal-decline narrative). HE absorbed only a fraction of steel-producer EBITDA volatility over the last cycle (HE indexed 92-125 vs steel producers 138-382). Direct precedents: Apollo bought Phoenix Services at ~7.5x. Befesa trades at 7-8x. Mid-cycle EBITDA $200M, vs $172M trough.

Harsco Rail: 50 year average tenure with top customers, 70 country installed base, 39% aftermarket revenue at 2x equipment margins. The drag isn't the business, it's three legacy fixed-price ETO contracts signed pre-COVID running off mechanically (SBB ~92% complete, DB Netz renegotiated, Network Rail in exit talks). Once they complete, working capital reverses and Rail returns to $30-40M EBITDA. Wabtec just paid 12.5x for Dellner Couplers in a similar setup.

The mispricing setup. New Enviri doesn't qualify for the S&P SmallCap 600 or Russell 2000. Index funds become forced sellers on June 1. Special-sit funds that bought for the deal collect the cash and leave. Sell-side coverage halves through a spin and takes 1-3 quarters to re-initiate. A sub-$500M micro-cap with two cyclical businesses and no immediate FCF is not a trendy thing to own.

Downside is structurally protected. Net debt at 2.0x FY26 EBITDA, with $130M of restricted cash returning over 2027-2029 as Rail contracts complete. New CEO is a former M&A attorney; new CFO came out of retirement. This team is telegraphing a sale.

The math. Probability-weighted upside: 289% from the current implied stub of $12.73 per NE share over a 2-3 year horizon. Conservative case still pays 124% at a 6x multiple. Sale Realized scenario delivers 383%.

You're paying for a 4.5x trough EBITDA industrial stub at the bottom of a four-year cycle and getting the regulatory tailwind, the Rail mean-reversion, and a likely sale process for free.

Full deep dive on Undervalued and Undercovered.

2

4

32

8,163

May 25

Payments infrastructure is being reshaped by AI and stablecoins and valuations across the space have gotten much cheaper. I'm looking to connect with other investors and fund managers who are following this closely.

If you're interested in the payments ecosystem and how AI is changing it, I'd love to exchange ideas. DM me or reply here.

2

1

9

4,729

May 22

The biggest IPO wave in years is coming. SpaceX, Stripe, Anthropic. PE and venture capital need to exit. And they will exit into the same passive funds where millions of families keep their retirement savings.

No due diligence. No valuation opinion. Just automatic buying at whatever price the sellers set.

PE, private credit, expensive space and AI companies. All of that is being dumped into passive investors that will not know what's happening until it's too late.

This is generational poverty in the making for honest families that invest with their 401(k)s and trust the system.

The age of passive investing might be in its final days. Most people don't know the risk they are taking.

2

4

47

4,947

May 19

RAVE Restaurant Group ($RAVE), a pure-play restaurant franchisor trading at 6.7x EV/EBITDA. $12M net cash, 32% of market cap. Peers at ~18x average. Even stagnant Jack in the Box trades at 10x.

Here's why this could be a multibagger:

After 24 consecutive years of unit decline, this company just turned the corner. Five consecutive years of buffet unit growth, and the latest quarter showed exactly what the next leg looks like:

13 restaurants under contract to open in the next 3 quarters. 5 already under construction. 4 opened YTD. 17 expected in 2026 on a base of 82 units. Pipeline of 30 signed franchisee agreements. A Director of Construction hired in Q4 to remove the last bottleneck.

That math = high-double-digit annual unit growth. While other national pizza chains are announcing closures of hundreds of stores, $RAVE is opening.

The format is also winning on same-store sales. SSS went from -2% troughs in mid-2024 to 8% peaks in CY Q3 2025 while Chipotle turned negative and Sweetgreen dropped 8%. $8 dine-in pricing with servers. Insulated from the squeezed-middle problem hitting every fast-casual peer.

Even ignoring all of that: 8.5% LTM FCF yield, zero debt, >90% FCF conversion. Net cash alone covers 32% of market cap. The downside is structurally protected.

The reason the mispricing exists is the same reason it could be a multibagger.

While the market wrote off another microcap with no coverage and a 24-year scar, this management team was investing in growth — second franchise salesperson, Director of Construction, ad-fund recapture, reimage program driving 20% sales at pilot stores. The Q3 print is the first concrete confirmation that those investments are now converting into openings under construction.

Base case: 38% 3-year IRR at a 12x exit. Bull case: 44%.

You're paying for a profitable franchisor at 6.7x EV/EBITDA and getting a high-double-digit unit-growth pipeline — for free.

Multibagger upside — and the inflection has already been confirmed by the latest results.

Full deep dive on Undervalued and Undercovered.

2

1

44

8,622

May 18

Good results from Smart Eye ($SEYE): strong growth off an unreported base (as usual), EBITDA-positive but still cash-flow negative. Seeing Machines is in a much stronger position in my view, yet SEE has a similar market cap to Smart Eye. That makes zero sense to me.

To use an analogy: $SEE is like Apple with iOS. Their software works better because it’s built for specific hardware. Smart Eye is more like Android—it scales well, but performance can be weaker because device makers have to adapt the software to their own hardware. SEE’s approach is structurally superior: they can command higher pricing and are better positioned to expand into adjacent markets.

2

5

3,437

May 16

We need to embrace the probabilistic side of investing. Creating complex models does not affect the outcome, you will just fool yourself into having more conviction than you should.

To be a good investor you just need to find a couple of drivers that are not completely priced in, why they are not priced in, and what needs to happen for them to be priced in. It's that simple.

1

10

2,596

May 14

Something I've been thinking about with $SPCB — if revenue on multi-year agreements is recognized upfront alongside costs, the P&L becomes misleading in both directions.

In the early years, profits look inflated because most of the revenue from the contract is booked upfront. But in the later years, you see a sharp decline in both revenue and profits — not because the business is deteriorating, but because the accounting already recognized what was earned.

That means the numbers you see on the P&L in any given year don't really represent what the business is actually making. A strong year might just be front-loaded recognition, and a weak year might just be the tail end of a contract that was already profitable.

If this is how it works, you can't take any single year's earnings at face value. You'd need to normalize across the full contract life to understand the real economics. Does anyone following this name have a view on this?

2

1

8

3,470

May 13

Looking for people invested or that have researched $SPCB. I am currently in the process of researching the company and would like to get different perspectives on it.

6

1

9

4,833

May 13

A cheap tech duopoly just posted 259% YoY royalty growth at a single-digit forward FCF multiple.

Seeing Machines ($SEE / AIM: SEE). The inflection is finally here. Q3 KPIs surpassed expectations. The GSR ramp up is no longer theoretical, the path to above 2m units per quarter seems almost inevitable. The company is now set to be cash flow positive, ready to refinance the loan and pursue further growth.

Aftermarket continues to lag (delays, not cancellations). A new contract was announced yesterday and the pipeline looks strong heading into next quarter.

Valuation: even assuming minimal contribution from Guardian 3 it's around 10x FCF. Include the aftermarket division and it drops to a single-digit multiple.

That's cheap for a duopoly business with substantial growth ahead.

Today I'm publishing the full thesis update a 1-hour CEO interview.

1

3

22

6,637

May 11

I’m invested in offshore oil, but I also own some renewable developers because they’re so cheap. There are so many takes on whether renewables are actually viable or not. It’s such a political topic that it’s hard to find unbiased sources.

Any recommendations?

1

5

2,033