EViews accelerates econometric estimation, forecasting and time series analysis so you can spend more time analyzing data than configuring it.

Joined January 2011

- Tweets 1,241

- Following 57

- Followers 2,324

- Likes 84

21 Photos and videos

EViews retweeted

24 Sep 2024

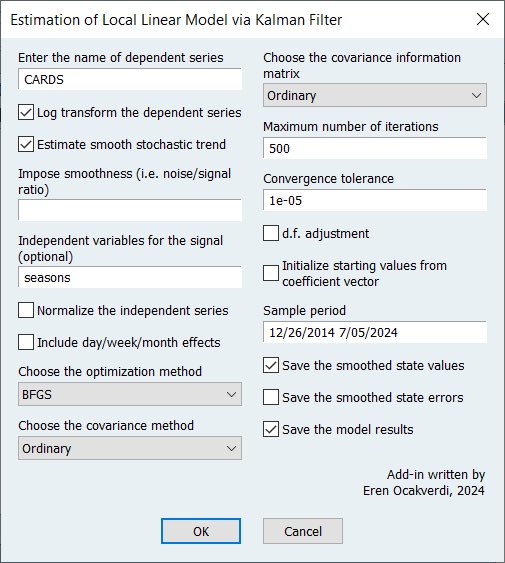

I have written an EViews add-in that implements the local linear trend model. My post on EViews’ official blog outlines the use of this add-in along with an application on weekly credit card expenditure data.

blog.eviews.com/2024/08/esti…

2

7

38

9,271

23 Sep 2024

New blog post on estimating local-linear trends with the Kalman Filter.

blog.eviews.com/2024/08/esti…

2

379

5 Aug 2024

New Blog Post detailing handling Lunar/Chinese New Year in seasonal adjustment routines.

blog.eviews.com/2024/08/seas…

1

2

486

15 May 2024

EViews 14 Beta patch released with the inclusion of Facebook Prophet (not documented yet), and the addition of rational expectations to models.

1

1

3

1,114

EViews retweeted

12 Feb 2024

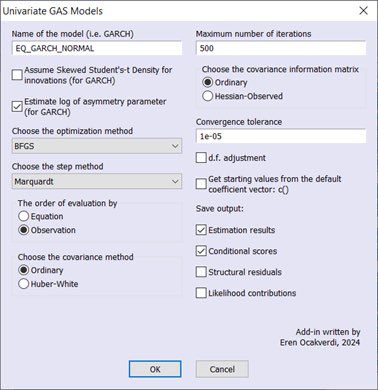

I’ve written an EViews add-in that implements the Generalized Autoregressive Score (GAS) method for GARCH-type volatility estimations. My post on EViews’ official blog outlines the use of this add-in along with an application to daily returns of USDTRY.

blog.eviews.com/2024/02/gene…

1

9

33

15,340

EViews retweeted

Last Chance to register!

This hour-long webinar led by Prof Lorenzo Trapani will cover Automated ARIMA Model Selection with EViews.

Register here -> pulse.ly/6wf8hca69q

1

3

558

29 Nov 2023

New guest blog post using a Large Bayesian VAR to replicate Cascaldi-Garcia's 2022 paper on Pandemic Priors. blog.eviews.com/2023/11/from…

4

14

2,181

22 Sep 2023

EViews registration servers are up and running. If you are having difficulty refreshing your license, please try flushing your DNS on your computer.

3

582

20 Sep 2023

New Blog post on Factor-Augmented MIDAS for nowcasting GDP.

blog.eviews.com/2023/09/nowc…

3

7

667

18 Sep 2023

EViews registration and Student Lite / University access will be unavailable for maintenance on 2023-09-21 at 09:00 PST / 16:00 UST for a couple of hours.

1

534

30 Jun 2023

The excellent Dr. Malvina Marchese is providing a free online seminar on using EViews on July 18th. Sign up here. instats.org/seminar/introduc…

6

609

22 May 2023

New guest blog post on estimating State Space models with GARCH errors.

blog.eviews.com/2023/05/stat…

2

5

635

EViews retweeted

Register now -> pulse.ly/6o0a9b54qa

ARDL models with EViews: Application to Bank Stress Test Models

Led by Prof. Christophe Hurlin

1

3

673

11 Apr 2023

New EViews 13 patch available, with some important VAR/VEC fixes.

eviews.com/download/ev13down…

1

1

4

688

EViews retweeted

Registration is still Open for Prof. Alain Hecq's one day course in Mixed Frequency Models using EViews.

Register Now -> pulse.ly/riw31fmi08

Running on April 25 this session will introduce tools to effectively leverage information released at different frequencies.

1

3

527

EViews retweeted

Register -> pulse.ly/ljseypg805

Do you work within Forecasting or use Forecasting in your research?

Led by Prof. Andrea Carriero of QMUL, this is the perfect course to bring you up to date with the latest methods in the forecasting profession.

@IHSEViews

2

5

772

22 Mar 2023

New EViews 13 patch released today, including support for the latest EIA database API.

1

4

476

EViews retweeted

The ongoing R vs Stata wars is my candidate for most overrated dispute in higher education.

I've now use the following programs in papers: R, Stata, SAS, HLM, SPSS, HLM, EViews, Limdep AND Excel.

I used all but R in the 8 years post-phd.

My grad program used Gauss/Markov.

9

7

101

31,817