Fast reads on market moves, sector rotation, and strategy signals. Built by IndexRank.

Joined April 2026

- Tweets 91

- Following 18

- Followers 5

- Likes 56

17 Photos and videos

Pinned Tweet

May 12

$CPRX shareholders need to pay attention.

Catalyst just reported Q1 2026 results:

Revenue: $149.4M

FIRDAPSE: $98.9M, 18.1% YoY

AGAMREE: $36.7M, 66.6% YoY

FIRDAPSE AGAMREE: $135.6M, 28.2% YoY

Operating income: $73.2M, 15.6% YoY

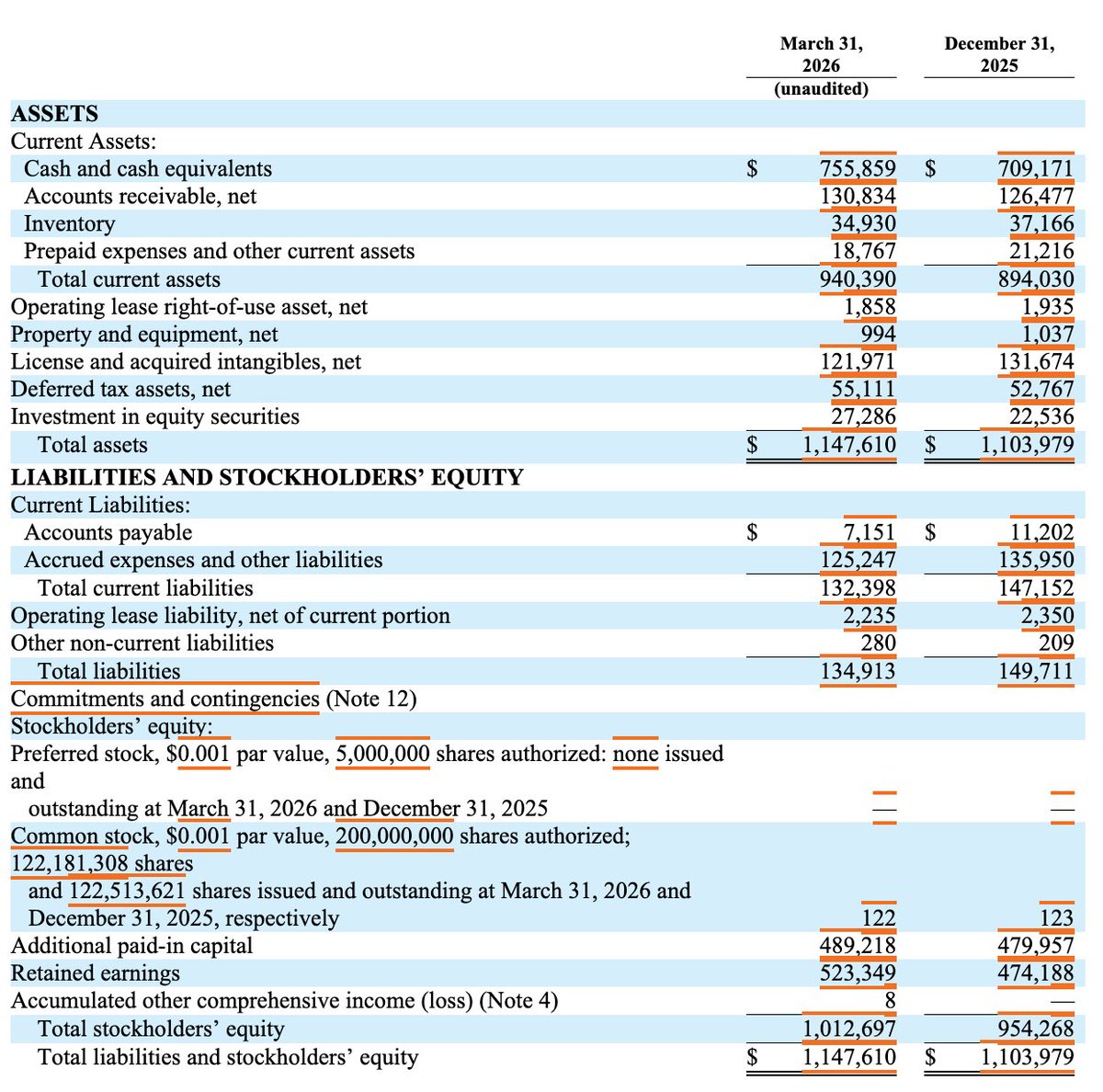

Cash: $755.9M

Funded debt: $0

These are not numbers from a broken company.

They are numbers from a highly profitable, cash-rich rare disease business whose two promoted products were still growing strongly.

The business did not just grow. The core promoted products accelerated.

Now look at the sequence.

May 6: Merger agreement signed with Angelini at $31.50/share.

May 7: Deal announced. Hetero settlement disclosed. FIRDAPSE generic entry pushed out to no earlier than January 2035, subject to customary exceptions.

May 11: Q1 results released.

But no earnings call.

No webcast.

No forward guidance update.

And then the DEFA14A employee communication says Catalyst will enter an investor quiet period and stop holding investor conference calls or attending investor events while it works toward closing the transaction.

So shareholders finally get the Q1 numbers, but they do not get a live management discussion.

That is the problem.

The issue is not only the $31.50 price.

The issue is the process.

The largest patent overhang was resolved.

The core products showed strong growth.

The cash balance increased to $755.9M.

The business remained highly profitable.

And shareholders are now being asked to accept a fixed cash exit before seeing the full proxy, the negotiation timeline, the fairness opinion details, and the Board’s treatment of the Hetero settlement and Q1 outlook.

At a stated equity value of roughly $4.1B, Catalyst’s $755.9M cash balance represents about 18% of the deal value. Economically, the buyer is acquiring a debt-free, cash-rich platform after the core patent overhang was reduced.

By cancelling the earnings call, the Board has not just entered a quiet period.

It has entered an accountability period.

The Board may claim it secured a “premium.”

But a premium over a price suppressed by litigation risk and information asymmetry is not necessarily a win.

It may be a surrender of future value right when the risk was being removed.

This is exactly where Price Discovery and Information Asymmetry collide.

Was $31.50 the result of a true market-tested process?

Were other buyers contacted?

Why was there no go-shop?

When did the Board know Hetero would settle?

Did JP Morgan’s fairness analysis fully reflect the 2035 FIRDAPSE protection?

Did the Board review Q1 expectations before approving the deal?

Why should public shareholders lose the upside of a de-risked asset at the exact moment the risk was being removed?

These are not conspiracy theories.

These are basic governance questions based on the company’s own SEC filings.

The upcoming proxy statement needs to answer them clearly.

Until then, every $CPRX shareholder should read the filings, question the process, and decide whether this Board truly maximized shareholder value.

#CATALYSTPHARMACEUTICALS

#CPRX #CorporateGovernance #ShareholderRights #BiotechInvesting #ValueInvesting #SEC #AngeliniPharma #MergerArb #Activism

2

4

139

Jun 12

SpaceX is about to become one of the biggest public companies in the world.

IPO price: $135/share

Amount raised: ~$75B

Implied valuation: ~$1.77T

This would be the largest IPO ever, more than double Saudi Aramco’s 2019 raise.

But the real story is not just the size.

SpaceX is testing how much public market liquidity is available for mega-scale ambition:

Starlink

launch infrastructure

moon missions

Mars colonization

space-based AI/data-center dreams

This is no longer just a space company going public.

It is a test of whether public markets are willing to fund trillion-dollar infrastructure narratives.

Anthropic filed.

OpenAI is coming.

Oracle is raising capital.

SpaceX is listing.

The next phase of technology is not just about innovation.

It is about who can raise enough capital to finance the future.

48

Jun 11

The AI trade is entering a new phase.

It is no longer just about demand.

It is about funding.

Oracle reported strong cloud growth and massive AI backlog, but the stock fell after the company said it expects to raise about $40B in FY2027 through debt and equity financing.

At the same time, SpaceX is preparing what could be the largest IPO ever:

$75B raise

$1.77T valuation

And this is not happening in isolation.

Anthropic has filed confidentially.

OpenAI is moving toward public markets.

AI infrastructure companies are raising tens of billions.

SpaceX is about to test how much liquidity the market can absorb.

The question is changing.

It is no longer:

“Is AI demand real?”

It is:

“Who funds the next phase of AI?”

Compute is expensive.

Energy is expensive.

Data centers are expensive.

And public markets are becoming the financing layer for the AI buildout.

The AI race is becoming a capital markets race.

41

IndexRank Lab retweeted

Jun 10

TRUMP: IRAN CHOKED BY U.S. BLOCKADE

Trump claims the U.S. naval blockade of Iran is the most effective in history, calling it a “steel wall” that allows nothing through without U.S. approval. He says Iran’s economy has been crippled, with the country unable to fund its military or pay its bills, pushing it toward becoming a failed state. He also notes that some oil exports are still leaving the country.

51

41

420

110,985

Jun 10

Today’s premarket selloff is not just about Iran.

It is Iran CPI AI fatigue.

That combination matters because it hits the two things this market needs most:

stable inflation

and confidence in long-duration tech.

72

Jun 10

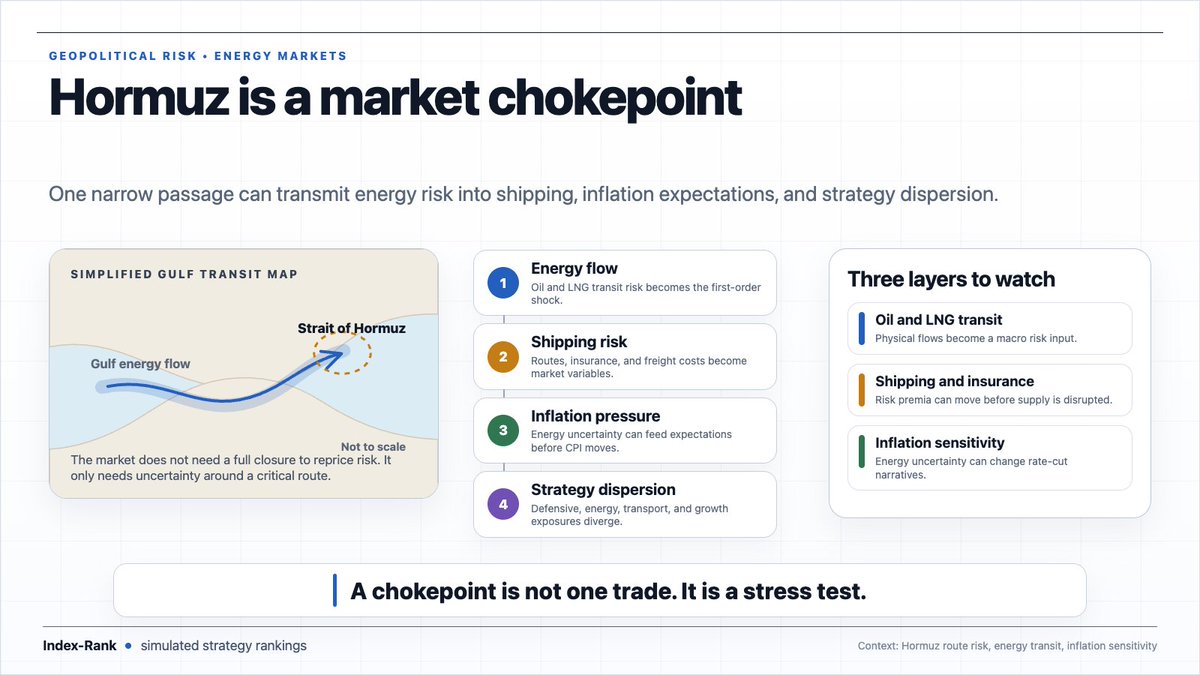

The Middle East risk is back.

The U.S. has launched strikes on Iran after Trump blamed Tehran for an Army helicopter crash near the Strait of Hormuz.

Iran is now vowing retaliation.

This is no longer just an Israel-Iran headline.

It is an oil story.

An inflation story.

A Fed story.

A market risk story.

The Strait of Hormuz is not just a geopolitical chokepoint.

It is one of the most important transmission channels between war, energy prices, and global inflation.

AI may still be the market’s main narrative.

But if oil starts moving again, macro can quickly take the wheel.

97

Jun 9

The $NUVL rumor is now official.

GSK is acquiring Nuvalent for $10.6B in cash.

Deal terms:

$124/share

40% premium to last close

26% premium to 30-day VWAP

Expected close: Q3 2026

This is not a revenue acquisition.

It is a late-stage oncology platform acquisition.

GSK is buying:

Zidesamtinib for ROS1 NSCLC

FDA decision date: Sept. 18, 2026

Neladalkib for ALK NSCLC

FDA decision date: Nov. 27, 2026

NVL-330 for HER2-altered NSCLC

Phase 1

The bigger signal:

Big Pharma is willing to pay before approval when the asset is scarce, de-risked, and strategically important.

$NUVL shows what still gets rewarded in biotech:

validated targets

near-term FDA catalysts

potential best-in-class drugs

clear unmet need

strategic scarcity

Biotech M&A is back, but buyers are not chasing hype.

They are buying late-stage assets that can change growth trajectories.

71

Jun 9

Rumors are circulating that GSK may be interested in Nuvalent.

Nothing is confirmed yet.

But the logic is clear:

$NUVL has two late-stage precision oncology assets under FDA review:

Zidesamtinib for ROS1 NSCLC

PDUFA: Sept. 18, 2026

Neladalkib for ALK NSCLC

Priority Review

PDUFA: Nov. 27, 2026

For Big Pharma, this is the kind of asset that matters:

targeted oncology

brain-penetrant drugs

near-term regulatory catalysts

potential best-in-class positioning

Whether GSK is real or just rumor, the bigger point is simple:

biotech M&A is coming back, and late-stage precision oncology is exactly where buyers are looking.

285

Jun 8

Iran and Israel are exchanging fire again, putting the Middle East ceasefire under serious pressure.

Trump has told Israel to stop and avoid further escalation.

The real question now: can Washington still control the next move, or are oil, inflation, and geopolitical risk coming back into play?

20

Jun 8

The most important geopolitical story today may be Xi Jinping’s visit to North Korea.

It is his first trip to Pyongyang in nearly seven years.

This is not just a diplomatic photo-op.

North Korea has moved closer to Russia.

China now wants to pull Kim Jong Un back into its orbit.

And the U.S. still wants denuclearization, while Pyongyang is openly calling that an “anachronistic dream.”

The key detail to watch:

Will China’s official readout mention “denuclearization”?

If not, the signal is powerful.

Beijing may be quietly accepting North Korea as a nuclear reality, not as a temporary problem to be solved.

That would reshape the Korean Peninsula issue from a denuclearization problem into a great-power bargaining chip.

China.

North Korea.

Russia.

The U.S.

The old Cold War map is being redrawn in Northeast Asia.

47

Jun 6

The U.S. jobs report just changed the market conversation.

May payrolls: 172K

Consensus: ~80K-90K

Unemployment rate: 4.3%

Wage growth: 0.3% MoM, 3.4% YoY

March/April revisions: 93K

On the surface, this is a strong labor market.

But the market reaction tells the real story:

Strong jobs = less room for Fed cuts.

Less room for Fed cuts = higher yields.

Higher yields = pressure on long-duration assets, especially tech and AI.

There’s also an important detail inside the report.

Job gains were led by:

Leisure & hospitality: 70K

Local government: 55K

Health care: 35K

Meanwhile, financial activities lost 22K jobs and long-term unemployment is still elevated.

So this is not a simple “everything is booming” report.

It’s a two-sided economy:

Services are still hiring.

Government and health care remain resilient.

White-collar areas are softer.

And the Fed now has less reason to rush.

For markets, the message is clear:

The AI trade still needs growth.

But it also needs rates to cooperate.

This jobs report made that second part harder.

19

Jun 5

The biggest geopolitical story right now may be happening inside Washington.

In two days, the House voted to:

1. Curb U.S. military action against Iran

2. Advance Ukraine aid and new Russia sanctions

Different theaters.

Same signal.

Congress is trying to reassert itself in U.S. foreign policy.

Iran matters because the Strait of Hormuz, oil prices, and inflation are back at the center of global risk.

Ukraine matters because Russia is testing whether Western fatigue is real.

The market story of 2026 has been AI, chips, and capital markets.

But the geopolitical story is becoming just as important:

Can the U.S. still sustain a coherent global strategy when domestic politics is pulling foreign policy in multiple directions?

That question will show up in oil, rates, defense stocks, shipping, currencies, and risk premiums.

16

Jun 4

U.S. pre-market weakness today looks less like a growth scare and more like an AI expectations reset.

Broadcom posted strong numbers, but the stock is falling because the market wanted more than “good.” Revenue grew 48% YoY, AI semiconductor revenue jumped 143% YoY, and Q3 guidance was strong, yet investors were looking for a bigger upside surprise and a clearer raise to the 2027 AI chip outlook.

That disappointment is spilling over into semis and Nasdaq names. This does not look like an AI demand collapse. It looks more like valuation, positioning, and “too-high expectations” being repriced after a powerful rally.

Macro is adding pressure too: elevated oil keeps inflation risk alive, ISM services showed sticky price pressure, and that makes the Fed less likely to turn dovish quickly.

So today’s move is basically:

AI profit-taking semiconductor repricing oil/inflation/Fed risk.

After the open, the key tells are AVGO’s recovery attempt, Treasury yields, oil, and market breadth.

35

Jun 4

Broadcom’s Q2 was not an AI slowdown story.

It was almost the opposite.

$AVGO just reported:

Revenue: $22.2B, 48% YoY

AI semiconductor revenue: $10.8B, 143% YoY

Free cash flow: $10.3B

Adjusted EBITDA margin: 69%

And the real signal was guidance:

Q3 revenue: ~$29.4B, 84% YoY

Q3 AI semiconductor revenue: ~$16B, 200% YoY

That means Broadcom’s AI chip revenue is expected to jump nearly 50% sequentially in one quarter.

Management also said AI semiconductor bookings were over $30B in Q2, versus $10.8B shipped.

So why did the stock fall after hours?

Because in this market, “great” is no longer enough for AI infrastructure names.

Investors are pricing in perfection.

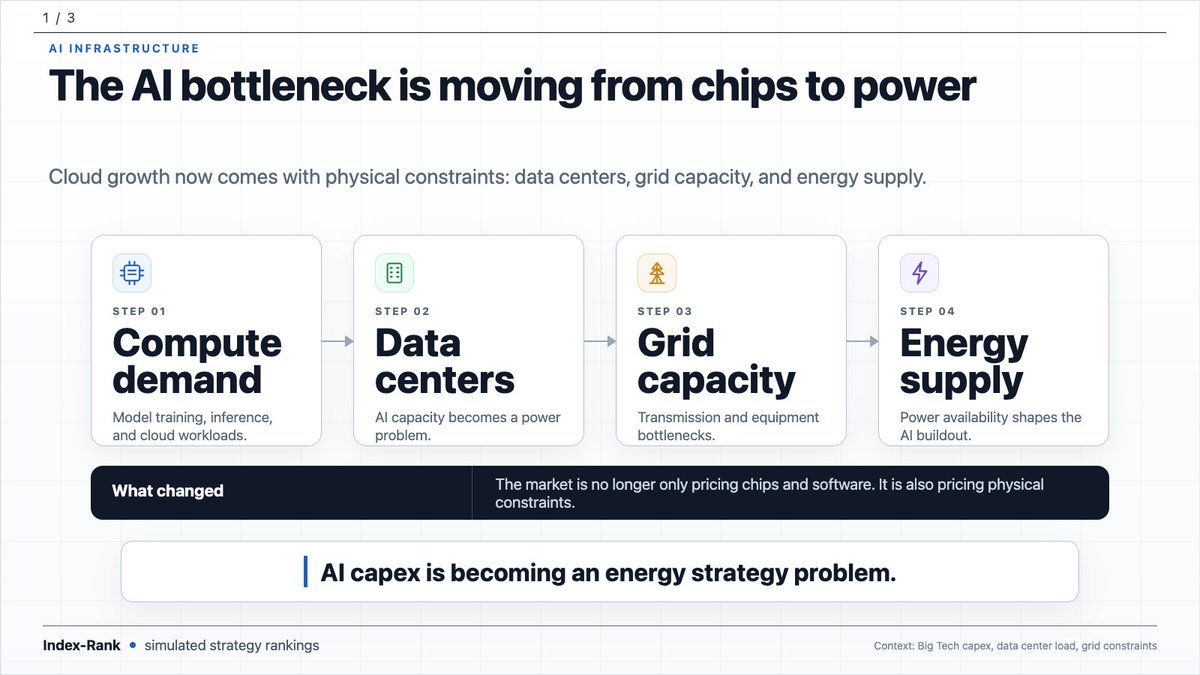

Yesterday, the story was Anthropic preparing for public markets.

Today, it’s Broadcom showing the physical layer behind that story:

custom AI accelerators, networking, gigawatts of compute, and multi-year supply commitments.

The AI race is moving from models → chips → power → capital.

That may be the real takeaway.

120

Jun 2

Yesterday, Anthropic confirmed it confidentially submitted a draft S-1 to the SEC.

Now Alphabet is raising up to $80B through equity offerings to fund AI infrastructure and global compute.

This is not a startup trying to survive.

This is Google’s parent company, one of the greatest cash machines in history, tapping the equity market to keep scaling AI.

The signal is clear:

AI is no longer just a software race.

It is a capital markets race.

A compute race.

An infrastructure race.

Anthropic is preparing for public markets.

Alphabet is raising $80B.

SpaceX is in the IPO pipeline.

OpenAI is reportedly preparing its own move.

The next phase of AI may be decided as much by balance sheets and capital access as by model quality.

22

Jun 2

$CPRX shareholders should read the May 28 PREM14A carefully.

The filing does not make the $31.50 Angelini takeout easier to accept.

It makes the process questions sharper.

The most important part is the 24-hour capitulation.

April 26:

The Catalyst Board authorized J.P. Morgan to counter Angelini at $34.00/share.

April 27:

Angelini came back with a “best and final” $31.50/share offer.

Within roughly 24 hours, the Board moved from authorizing a $34.00 counter to accepting a path toward $31.50, exclusivity, and a deal conditioned on settling the Hetero litigation.

That is not ordinary price discovery.

That looks like a process that ended right when shareholders needed it most.

Now look at the Hetero sequence.

The proxy shows Angelini’s proposals were repeatedly tied to resolving the Hetero litigation.

The proxy also says Catalyst expected to announce the transaction and the Hetero settlement together, no later than May 11, to coincide with Q1 earnings.

That is not a minor detail.

Hetero was the key patent overhang on FIRDAPSE.

Once resolved, the market should have had a chance to price the de-risked asset.

Instead, shareholders received a fixed cash exit at $31.50 before true post-settlement price discovery could occur.

The Board may call this a premium.

But a premium over a price still burdened by litigation risk and information asymmetry is not the same thing as maximizing value.

Now compare the deal value to the company’s own projections.

Stated equity value: ~$4.1B

Q1 cash balance: ~$755.9M

Rough net EV: ~$3.34B

March 2026 projections disclosed in the proxy:

2026 EBIT: $323M

2030 EBIT: $692M

2034 EBIT: $885M

That implies roughly:

10.3x 2026 EBIT

4.8x 2030 EBIT

3.8x 2034 EBIT

So Angelini is buying a de-risked, cash-rich rare disease platform at a valuation that looks increasingly hard to justify once Hetero risk is removed.

This was not a broken business.

FIRDAPSE was growing.

AGAMREE was ramping.

Cash was building.

The largest patent overhang was being resolved.

And public shareholders are being asked to give up the 2030s upside for $31.50 in cash.

The proxy also discloses an incentive structure shareholders cannot ignore.

Directors and executive officers holding about 5.5% of outstanding shares entered voting agreements to support the deal.

Unvested options and RSUs vest and cash out at closing.

Richard Daly’s golden parachute table shows roughly $34.1M.

Patrick McEnany’s vested in-the-money options alone show roughly $42.2M of cash consideration.

The proxy does not prove motive.

But it does show a clear incentive mismatch.

Public shareholders were waiting for post-Hetero price discovery.

Insiders had large, immediate cash-out economics at closing.

That is exactly why governance matters.

The question is not whether $31.50 is above the pre-rumor share price.

The question is whether $31.50 reflects the value of Catalyst after Hetero was resolved.

Why accept $31.50 one day after authorizing a $34.00 counter?

Why enter exclusivity before shareholders could see post-settlement market pricing?

Why lock in a cash exit before Q1 results and before the market could digest the 2035 FIRDAPSE protection?

Why should the upside of a de-risked asset transfer to the buyer at the exact moment the risk was removed?

This is not an accusation of illegality.

It is a governance question.

And the final proxy needs to answer it clearly.

#CPRX #CorporateGovernance #ShareholderRights #BiotechInvesting #ValueInvesting #MergerArb #Activism

1

1

1

71

Jun 2

Anthropic just confirmed it has confidentially submitted a draft S-1 to the SEC for a proposed IPO.

Not a public S-1 yet.

Not a guaranteed listing.

Share count and pricing are still TBD.

But it’s now official: Anthropic has started the IPO process.

SpaceX is already in the IPO pipeline, Anthropic just joined, and OpenAI is reportedly preparing its own move this year.

The real question isn’t just “who goes public first?”

It’s what this wave of AI mega-IPOs means for public markets, AI valuations, and the next phase of the AI race.

31

Jun 1

Japan Company Watch #1 — KEYENCE

06. The Debate

KEYENCE is one of Japan’s highest-quality industrial companies. The business is asset-light, global, cash-rich, and extremely profitable.

But the valuation already reflects that.

As of June 1, 2026, the stock traded around ¥80,220, with a market cap near ¥19.4T, a trailing P/E around 43.5x and a dividend yield below 1%.

Risks: industrial capex cycles, semiconductor/auto exposure, FX, fabless supply-chain execution, and the need to keep scaling high-quality sales talent globally.

My read: KEYENCE is clearly a great business. The harder question is what growth rate justifies the price.

Sources: KEYENCE FY2025 results, Annual Report, Business Model, Capital Allocation Policy, Sustainability disclosures, StockAnalysis.

28

Jun 1

Japan Company Watch #1 — KEYENCE

05. Recent Numbers

FY2025 was still strong.

Net sales: ¥1.1693T, 10.4%

Operating income: ¥595.8B, 8.4%

Net income: ¥445.2B, 11.7%

Overseas sales were the key driver. FY2025 overseas growth was 13.5%, or 12.9% on a local currency basis. Americas grew 13.3%, Asia 16.7%, and Europe & Others 8.4%.

By FY2025 Q4, overseas sales were 65.7% of total sales.

This is the key question for investors: can KEYENCE keep transplanting its direct-sales model overseas?

19

Jun 1

Japan Company Watch #1 — KEYENCE

04. Moat

KEYENCE’s moat is a loop:

customer problems → direct sales insight → product planning → high-value standard products → same-day shipping → more adoption → more customer data.

The company is also fabless. Production is outsourced to subcontract plants, while KEYENCE stays deeply involved in materials, production technology, planning and quality control.

This keeps capital intensity low while preserving quality.

The result is unusual: an industrial hardware company with software-like economics. In FY2025 Q4, gross margin was 83.5% and operating margin was 53.6%.

19

Jun 1

Japan Company Watch #1 — KEYENCE

03. Business Model

The magic is not only the product catalog. It is the operating system.

KEYENCE uses direct sales instead of relying mainly on distributors. Its sales engineers visit customer sites, observe production problems, propose applications and feed potential needs back into product planning.

That creates a data advantage.

Most industrial companies sell what they already make. KEYENCE learns what factories struggle with, then designs standard products that can solve similar problems across many industries.

Sales is not just distribution. It is R&D intelligence.

18