All great companies started as small companies. CIO @iancassel. if.capital/disclaimer/

Joined September 2018

- Tweets 216

- Following 2

- Followers 8,894

- Likes 330

33 Photos and videos

Jun 12

Expanding the rental fleet - highest IRR business line $KLNG

Disc: Long and wrong a lot

2

17

2,448

Jun 7

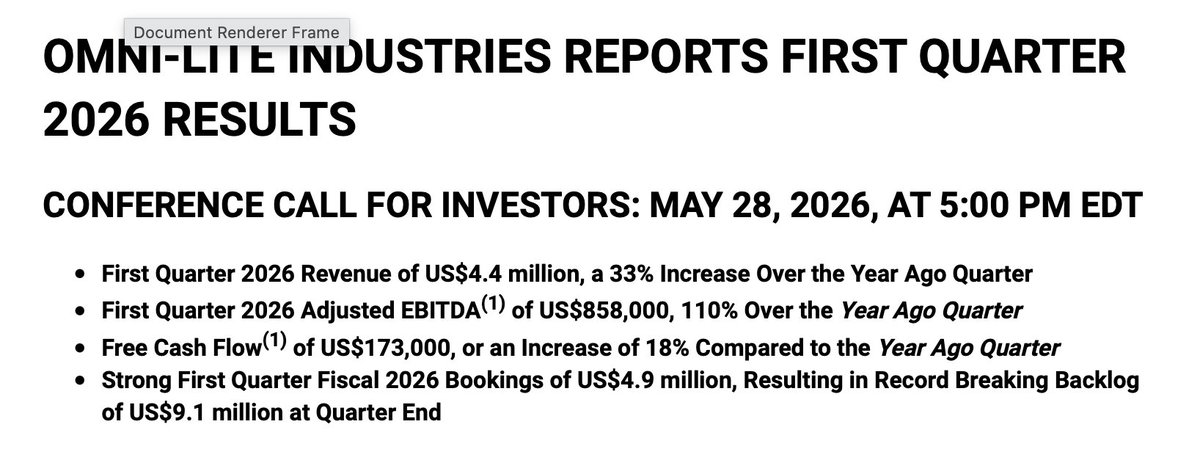

Omni-Lite $OML.V $OLNCF - A serial under performer showing signs of transformation with new board focus on optimization and capital allocation.

$20m EV, $3m cash/no debt, trading at 5x EBITDA with 20% EBITDA margins. Earnings call points to Q1 not being a positive fluke quarter, but expecting continued YoY growth in Q2 and margin expansion into back half of the year as DP Cast price increases flow through the P&L.

2026 a year of organic growth, optimization, and getting the platform in place for potential inorganic growth in 2027 and beyond.

Disc: Long and wrong a lot

3

2

27

3,008

IFCM MicroCap retweeted

May 31

In this great conversation @chriswmayer and @iancassel discuss how they look for similar things but execute differently. @excessreturnpod

microcapclub.com/chris-mayer…

5

24

17,980

IFCM MicroCap retweeted

May 30

This week I wrote about how successful microcap investing is like being the coach of a successful NBA franchise. The team/portfolio that made you made money five years ago is a historical artifact. The team/portfolio that keeps you wealthy is the one you have the courage to keep rebuilding.

microcapclub.com/the-coach-w…

4

5

58

19,833

May 27

Good quarter $OML.V

Disc: Long and wrong a lot

Mar 10

We own a position in Omni-Lite $OML.V

$20m CAD market cap/Profitable. The company provides mission-critical components in the Aerospace and Defense industry across three business units.

The legacy Forging business is a low multiple business that provides fasteners for Boeing and Airbus.

The Casting and Electronics businesses are high multiple businesses that supporting Tier 1 defense programs like, Pratt & Whitney's F35 engine program, Aegist Combat System, SHORAD missile defense and the Patriot platform.

The company will likely see double digit organic growth from new contracts and contract renewals at higher prices that should boost EBITDA margins in 2026.

In the meantime, a CEO search has started to find a leader to drive an acquisition strategy in these segments. Long-time CEO has stepped into an interim-CEO seat, and will then lead one of the subsidiaries once a permanent CEO is found. This is a friendly transition and positive for the company.

We believe the company today is worth more than the sum of the parts, and represents a very low risk, high reward, opportunity at the current valuation.

Disc: We are wrong a lot.

1

1

4

1,752

IFCM MicroCap retweeted

May 27

New Article

The portfolio that made you made money five years ago is a historical artifact. The portfolio that keeps you wealthy is the one you have the courage to keep rebuilding.

microcapclub.com/the-coach-w…

8

11

73

14,856

May 18

9

19

95

19,953

May 17

$SNWV

Peak skin sub disruption caused distributor churn and slower sales cycles the last few quarters. Management says bottom is in.

Q1 3% YoY growth

Q2 guided 10-15% growth

FY 26 guided 16-25% growth

“We've been seeing a great deal of engagement from some large systems right now.”

3

1

15

3,002

May 17

$BILD.V

Management continuing to see consolidation opportunities due to the recent weakness in homebuilding and renovation markets. Recently acquired three additional locations in Florida for at 1-2x EBITDA that also expands them into tile, new flooring category.

2

6

965

May 13

$SNWV

Morgan has done a good job being transparent through peak wound care disruption.

1

5

1,058

IFCM MicroCap retweeted

May 12

Here is a new presentation.

What three centuries of Norse raiders teach us about microcap investing.

microcapclub.com/we-are-viki…

9

7

48

30,649

May 7

Good update with Golconda Gold $GG $GGGOF

$130m market cap/EV

Should do $30m USD EBITDA @ $4300 Au

NCIB should start May/June

In this valuation investors also get the US asset spinoff late 2026/Early 2027 likely worth another $200m for free

Disc: long

youtu.be/oFDSWpotE2g?si=wu9l…

2

9

2,677

IFCM MicroCap retweeted

May 6

New Article

My high school golf coach was 82 years old.

On the day I made the varsity team, he walked over to me before our practice round and said,

"Ian, I'm going to play with you today. And I'm going to play one-handed. I bet I can beat you."

microcapclub.com/investing-i…

7

16

102

44,055

IFCM MicroCap retweeted

May 3

Here is our recent update with Golconda Gold $GG.V $GGGOF w/ 28% owner CEO Ravi Sood.

Disciplined gold producer trading at 4x EV/EBITDA (2026), aiming to triple gold production by 2029 spinoff of US asset in 2027 as standalone US gold producer.

microcapclub.com/update-with…

4

18

6,161

IFCM MicroCap retweeted

Apr 28

New Article - The Last Moat

As AI tools become more widespread and more capable, the informational playing field for for this data flattens. The alpha must go somewhere, and it migrates to wherever commoditization has not arrived yet.

microcapclub.com/the-last-mo…

8

15

103

37,989

Apr 21

$BLM.V hiring for 30-90 day assignment in the Caribbean

Probably get more inquiries if it said "spouse not allowed" 😆

3

900