El mayor activo de un inversor no es su capital sino su conocimiento. Tratando de aportar algo de valor a la comunidad elinversorinformado.substack…

Joined November 2021

- Tweets 3,466

- Following 366

- Followers 4,030

- Likes 4,516

2,017 Photos and videos

$SPCX SpaceX sale hoy a bolsa a un precio de $135. Lo que he ido leyendo:

🔹4x más demanda, pero SpaceX decidió mantener el precio inicial.

🔹Se ha permitido participar en la salida a bolsa a todo el mundo, incluyendo incluso participaciones en Revolut.

🔹Los modelos de valoración parecen bastante exigentes: multiplicar por 100x los ingresos en 5 años.

🔹Gran cobertura en prensa generalista. Incluso en España, que no es un país muy "bolsero", con comentarios como "me perdí Google, no me pierdo esta", sea a la valoración que sea.

🔹Ya se han lanzado ETF con 2x y 3x de apalancamiento.

Lo que yo veo:

🔹No dudo de que, al inicio, la cotización se dispare por la gran euforia. La mayor parte de las personas que compren no habrán mirado ni la primera página del folleto de salida a bolsa, pero habrán leído que es una empresa que se va a disparar. En 15 días se incluirá también en el Nasdaq.

🔹Muchos "inversores" han comprado para obtener una ganancia rápida. La clave será cuándo vender, ya que una gran parte tendrá eso en mente. "Tonto el último". A este respecto, es interesante ver que han estructurado la salida a bolsa de forma que el periodo de venta restringida se acorta: no tienen que esperar 180 días y pueden vender más acciones si la acción sube más de un 30%.

Para mí, por muy excepcional que sea la empresa —que parece que no tiene ningún competidor en ninguno de sus segmentos cuando lees la prensa—, ha sido inflada a niveles que no tienen sentido.

Apostaría por una fuerte corrección en menos de un año, incluso para una compañía de culto como va a ser SpaceX. En ese momento, veremos cómo aguantan los que no querían perderse el siguiente Google.

(Yo no he leído el prospecto porque no he tenido interés en invertir).

4

951

$BAMI.TO is the only stock in my portfolio standing out today.

They are hosting an investor call tomorrow. Let's see what additional colour they can give.

2

333

$CGY.TO $CGY

Quite a move for a company like Calian. Even with inflation, I doubt defense spending will decrease over the next few years.

I don't see a correlation between threats from Russia (or China) and U.S. inflation figures. It's not as if Canada and other NATO countries have much of a choice...

1

306

⁉️🙏Voy a dedicarle más tiempo a esta cuenta y al substract y a su vez, haré un pequeño cambio de nombre

He pensado en "Inversor Informado Insights", manteniendo el nombre actual pero refleja mejor lo que busco (sobre todo substrack)

¿Cúal os gusta más?

(más detalles debajo)

100%

El Inversor Informado

0%

Inversor Inform. Insights

0%

Informed Investor Insight

0%

Ninguno

0%

0%

0%

0%

1 votes • Final results

1

2

559

Tengo una temporada por delante con más tiempo libre que quiero dedicar a ciertos proyectos, entre ellos esta cuenta.

En el pasado realizaba algunos resúmenes semanales, pero dejé de publicarlos por el poco alcance (no compensaba el tiempo de ponerlos "bonitos") y tengo algunas ideas más que creo que pueden ser interesantes (que también hago de forma privada).

Mi intención es ser más activo aquí, pero también en Substack, desarrollando el contenido de forma más estructurada.

Para ello, y dado que la cuenta evolucionó respecto a la idea inicial, voy a darle un pequeño cambio de imagen. He pensado en cambiar el nombre a "Inversor Informado Insights" De esta forma conservo el nombre original de la cuenta.

A pesar de que no me guste mezclar inglés y español, Insights es la palabra que mejor representa lo que quiero ofrecer. También pensé en empezar a escribir solo en inglés, pero quizá eso sea para el futuro.

Gracias por la opinión!

1

428

Parece razonable si asumimos que hay cero competencia.

Pero hay que aplaudir a Goldman por tener tan buena visibilidad en el negocio. Seguramente estén siendo muy conservadores.

Jun 4

GOLDMAN SEES SPACEX AI REVENUE EXPLODING TO $322B BY 2030

Goldman Sachs projects SpaceX AI revenue rising from $3.2B in 2025 to $322B by 2030, a ~100x increase, forming the core justification for its $1.78T IPO valuation. Total revenue is forecast to reach $474B, with Starlink at $144B and rockets at $8.3B.

AI segment growth is tied to aggressive market assumptions despite current losses and execution concerns around xAI. Overall EBITDA is seen surging to $352B by 2030.

1

3

473

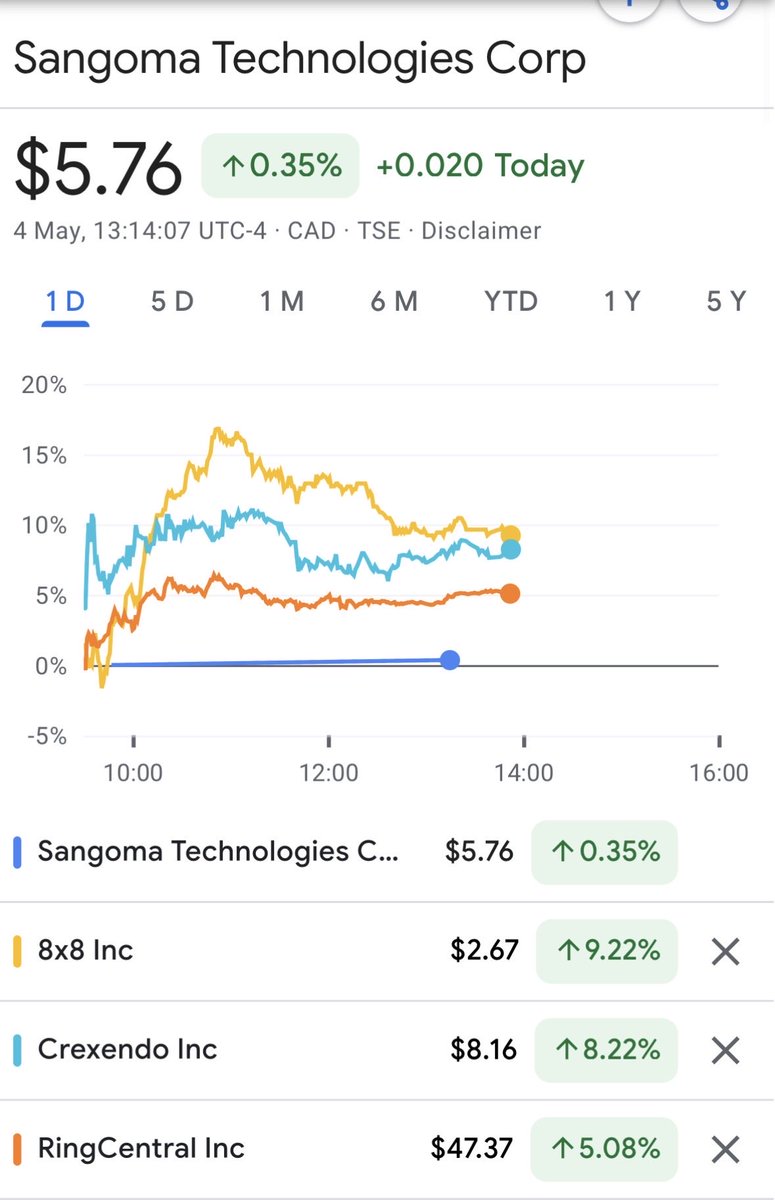

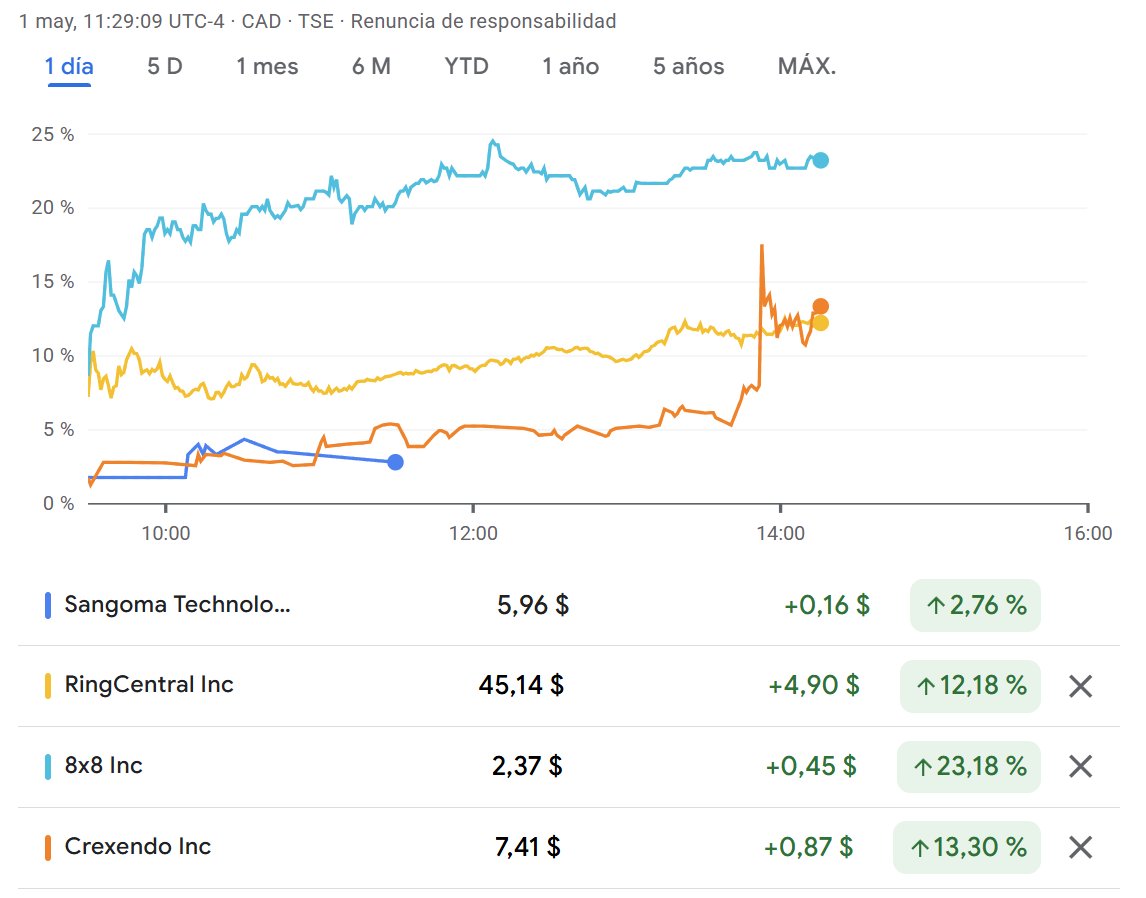

$STC.TO $SANG

Sangoma may try to replicate the success of Red Hat with Linux. For that, they need enterprises to start using PBX for their voice agents, and Sangoma could be the one providing support. It is a long shot, but the possibility is there.

Many businesses use phone systems powered by Asterisk® and FreePBX® without even realizing it.

Sangoma is the primary developer and sponsor behind both platforms, helping support two of the most widely used open-source telephony projects in the world.

2

301

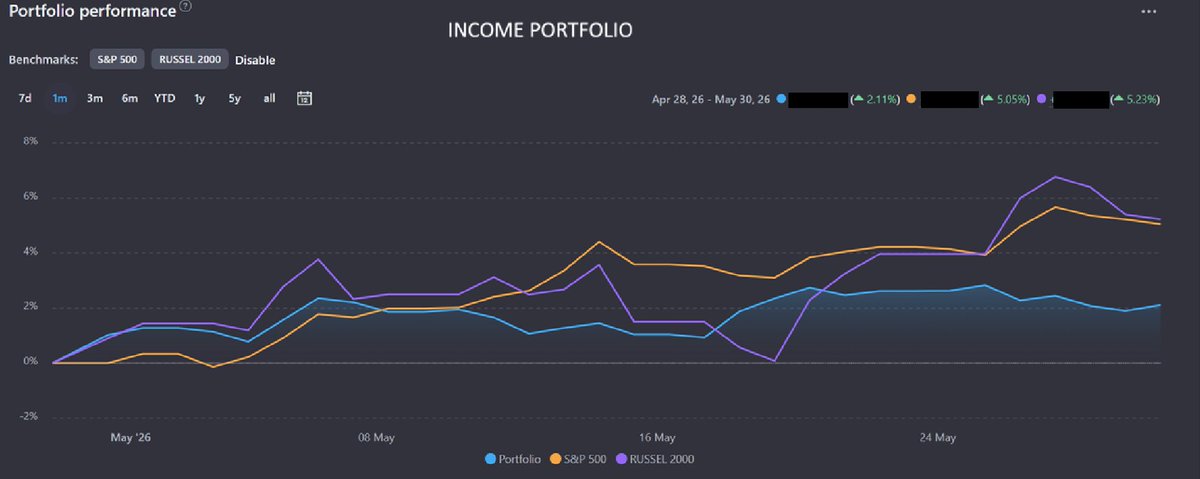

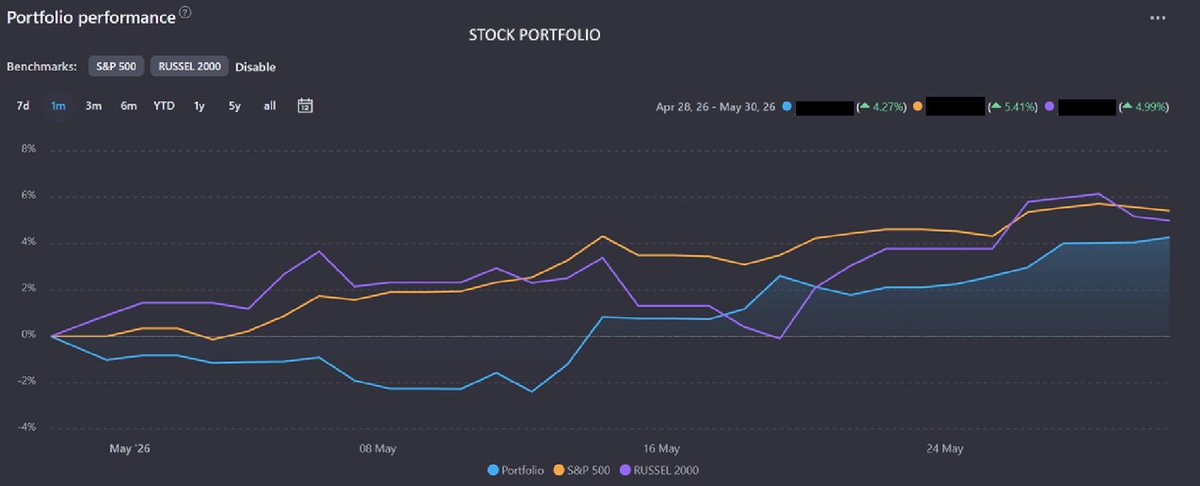

Mayo:

🟢Income Portfolio (incl. Dividendos): 2.11%

🟢Stock Portfolio: 4.27%

🟢S&P500: 5.05%

🟢Russel 2000: 5.23%

YTD

🟢Income Portfolio: 8.42%

🟢Stock Portfolio: 0.01%

🟢S&P500: 9.74%

🟢Russel 2000: 15.41%

CHF como moneda de referencia

Principales movimientos en mayo:

Income Portfolio:

🟢 $TEP ( 12%), $POLR.L ( 6.7% vendida), $FDJU.PA ( 3.9%), $WTES ( 2.9%)

🔴 $SUNN.SW (-4.6%), $CPKR (-3.6%), $JEPE (-1.3%)

Stock portfolio:

🟢 $LODE ( 29%), $CGY $CGY.TO ( 27%), $TEA.AX ( 18%), $TEP ( 12%) $EVO.ST ( 8.3%)

🔴 $DELIA (-29%), "Secreta" (-14%) $PYPL (-13%), $STC.TO (-12%), $NA9 (-10%)

2

277

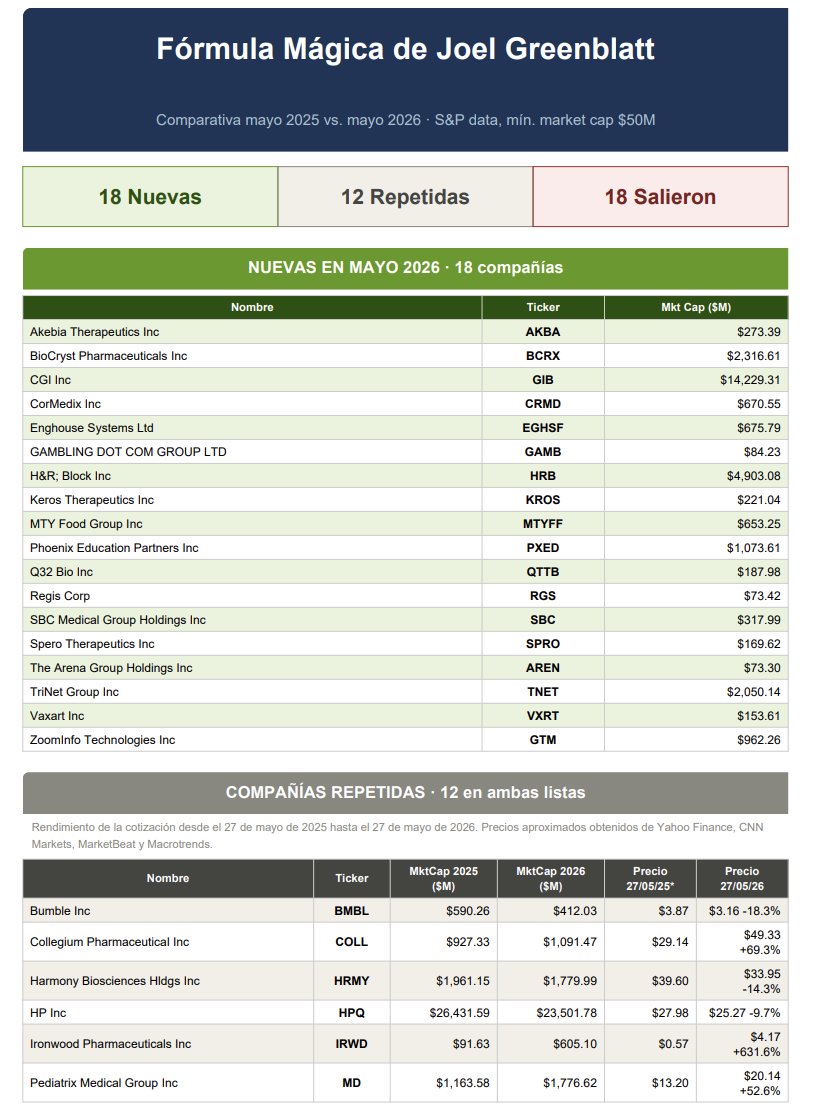

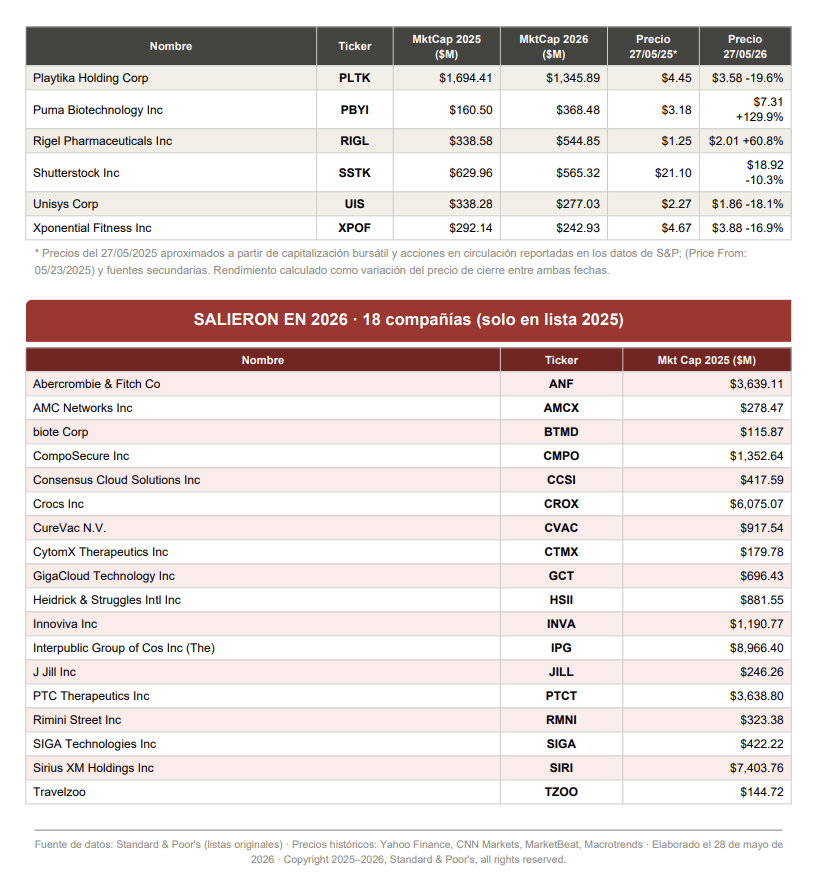

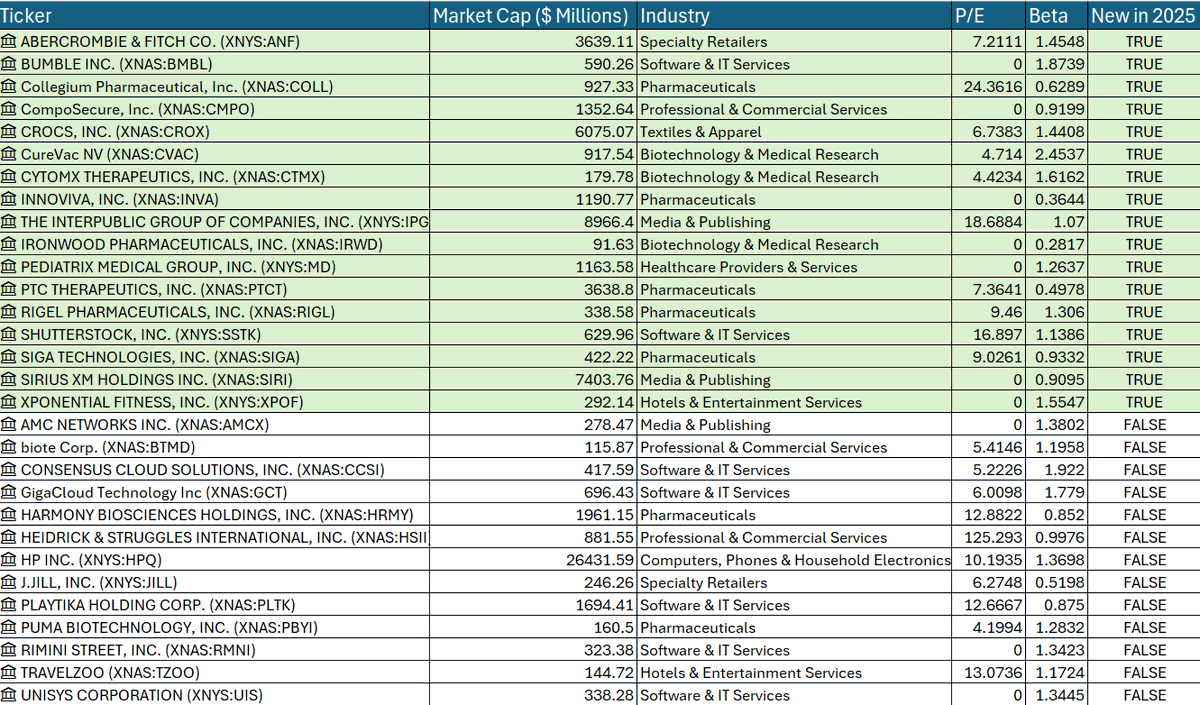

Un año después, vuelvo a comparar la lista de acciones de Joel Greenblatt, de su fórmula mágica. Esta vez, con la ayuda de Claude:

🔹18 acciones nuevas

🔹12 repetidas

🔹18 salen

Entre las nuevas:

🔹 $MTY.TO MTY Food

🔹 $GAMB

🔹 $GIB CGI INC

🔹 $RGS Regis

🔹 $CRMD Cormedix

27 May 2025

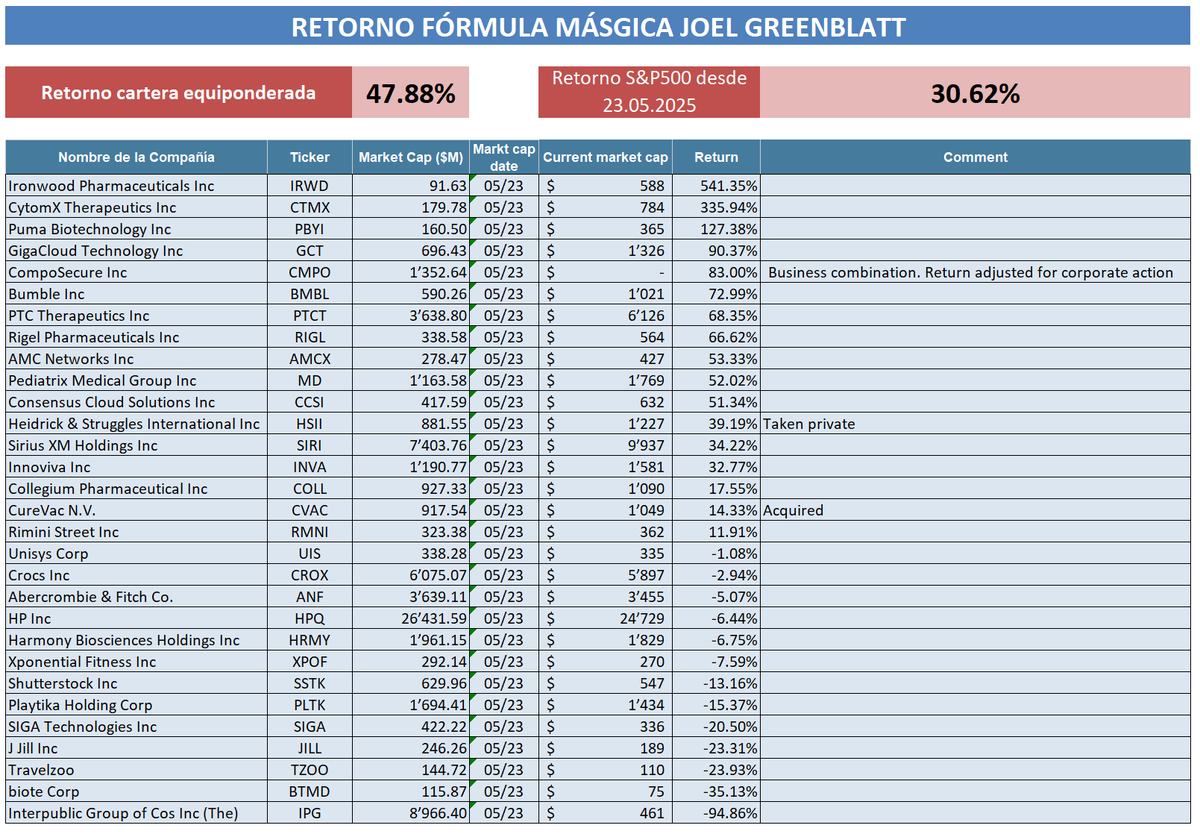

De vez en cuando le echo un vistazo a los nombres de la lista de Joel Greenblatt. Comparándolo con la captura que tenía de 2024, estos son nuevos nombres en verde, entre otros:

$SIGA

$CROX Crocs

$BMBL Bumble

$ABF Abercrombie

$MD Pediatrix Medical

1

5

1,435

Income Portfolio

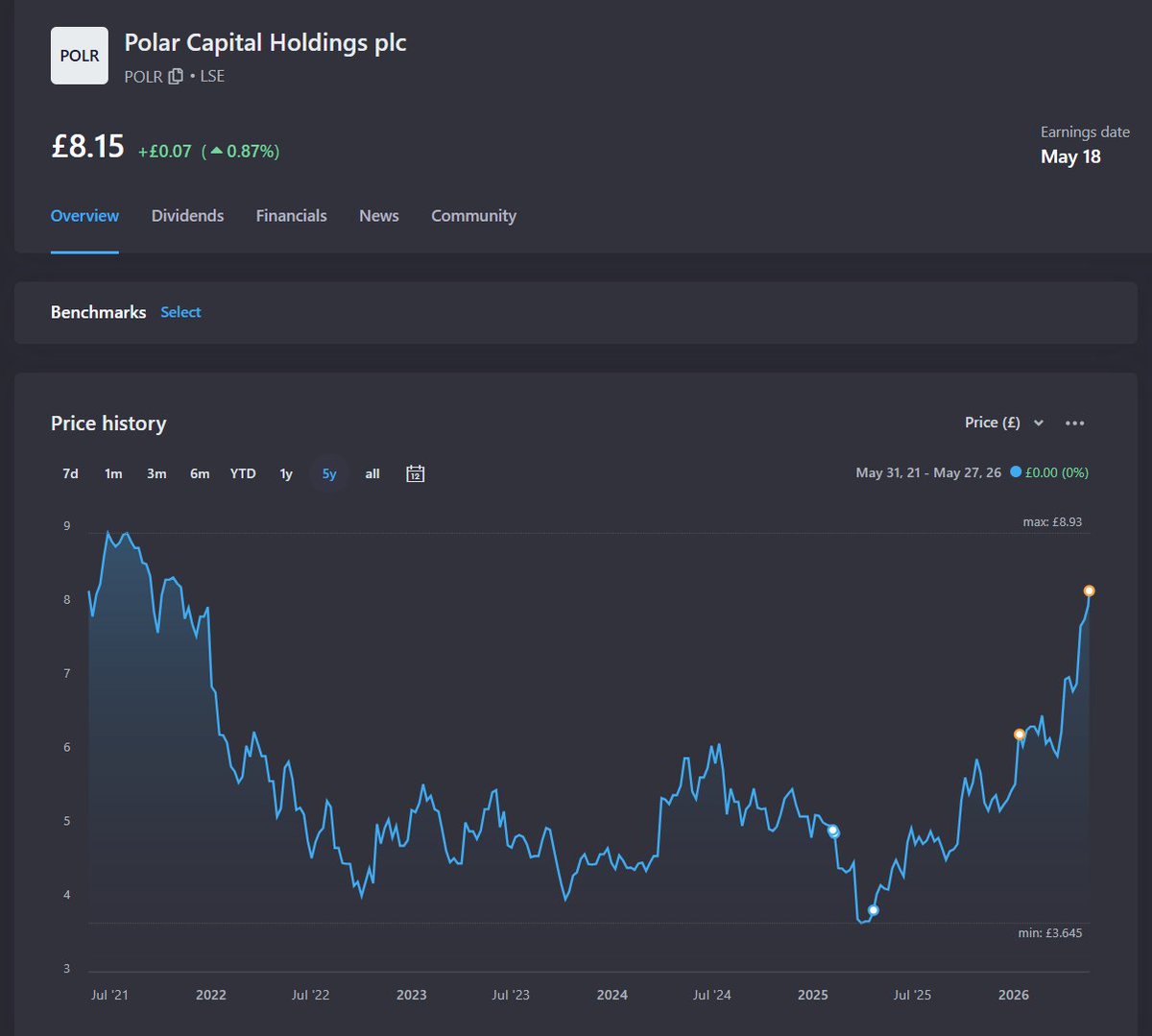

Cierro toda la posición en Polar Capital $POLR.L #POLR

🔹YoC: 10.25%

🔹Yield actual (con la venta): 5.6%

🔹Retorno capital: 53.35% (43% considerando FX)

🔹Dividendos cobrados: 10.26%

🔹Rendimiento total: 63.6% (52.7% considerando FX) en algo menos de 1.5 años.

El capital obtenido lo he reinvertido en $JEPE JPMorgan Europe Equity Premium Income Active por dos motivos principales:

🔹Proteger capital, ya que en una corrección fuerte de mercado sufriría menos (analizando otros fondos de JPM con más historial como $JEPI).

🔹Mayor retorno por dividendo, en torno al 10% esperado.

Si hay una corrección de mercado, es posible que vuelva a rotar ya que Polar es una gestora que me gusta mucho, pero dada su gran exposición a tecnológicas y la situación de mercado, creo que es prudente salir ahora. Pero la gestora lo está haciendo bien con incremento de AuM por aportaciones netas en el último trimestre y buen rendimiento de sus fondos.

En la anterior reducción había distribuido el capital a Sunrise $SUNN.SW (ha bajado bastante pero aun con un 5% de rendimiento más un 8% de dividendo cobrado) y $FDJU.PA, sigue plana pero con el dividendo cobrado, y sigo teniendo buena expectativas este año. Esas dos acciones me ofrecían una mejor alternativa para proteger capital.

1

4

534

Impresionante. Solo con un pequeño guión de un video que tenía sobre el libro de 100 baggers.

El fragmento del guión: "En primer lugar, no existe una industria o sector único de donde nazcan estas compañías. Lo cierto es que esas 365 compañías analizadas están en todo tipo de sectores como por ejemplo el industrial, donde compañías como Boeing o Deere & Co consiguieron ser 100 baggers en 20 y 35 años respectivamente, sector financiero, con State Street y Bank of New York Mellon, consiguieron el ansiado título en 17 y 23 años respectivamente o textil, con L Brands o VF Corp multiplicándose por 100x en 7 y 26 años respectivamente"

May 21

Yo sé que no es perfecto, pero me parece una jodida pasada lo que se puede hacer ya con una IA con una simple foto y un prompt. Esto ha sido a la primera, y ni me he esforzado.

Con sonidos y todo.

Es que es brutal.

Si haces vídeos en Youtube, los efectos y la calidad pueden ya aumentar una barbaridad.

Y no sólo para Youtube, también para dar formación

1

5

1,479

Stock portfolio

Ventas parciales en Sangoma ($STC.TO / $SANG) y Tasmea ($TEA.AX), que eran de las principales posiciones. Ahora representan el 8.05% y el 10.5% de mi cartera, respectivamente.

Considero también reducir Calian, que ahora representa el 23.8% de la cartera (aunque con los resultados que presentaron esperaba incluso una mejor reacción del mercado).

Breve comentario:

🔹Sangoma: Vendo el 50% de mi posición a C$5.2. Llevo más de 3 años en la empresa, y he ido ampliando al ver el buen desempeño de la nueva directiva. Sin embargo, como ya comenté, no me gustaron los últimos resultados por el nuevo cambio en la estrategia, reconociendo que hay mucha competencia en la parte de aplicaciones. La nueva estrategia (bundle) debería hacer que el producto de Sangoma sea competitivo en precio, pero no veo claro a corto plazo cuál va a ser el catalizador. Ya había comentado que en este año fiscal esperaba ver el crecimiento en los números, y no está siendo así. Sigo confiando en la directiva, que me parece honesta y transparente, pero tengo que ajustar el tamaño de la posición, ya que puede ser un gran (y mayor) coste de oportunidad mantener casi el 20% de la cartera en Sangoma, como he llegado a tener. Vendo realizando una pérdida. Con la valoración actual, sigo viendo muy poco downside, así que la decisión viene más por gestión de cartera y coste de oportunidad (como comento abajo, parte reinvertido en $BAMI.TO)

🔹Tasmea: Vendo el 50% a A$ 6.03. Por méritos propios, la empresa ya representaba más del 20% de la cartera. Sigo confiando en la empresa a largo plazo, pero después de hacer un x3 en la posición, conviene recoger beneficios y reducir riesgo. En Tasmea sólo realicé una compra inicial y el resto ha sido reinversión de dividendo.

La posición de efectivo ahora está en el 5%. Parte del efectivo de las ventas fue a cubrir el margen que había utilizado para comprar recientemente $BAMI.TO y otra empresa. Esperaba ajustar la cartera después de la presentación de resultados de Calian y Sangoma, con la idea de reducir Calian primero. Pero viendo los resultados, me he inclinado por reducir Sangoma, realizando pérdidas. La venta de Tasmea es más para ajustar pesos.

2

617

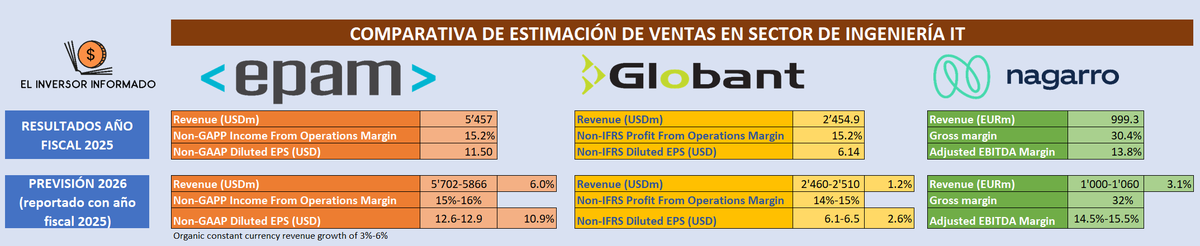

Previsiones sector ingenieria IT reportado con Q1:

🔹 $NA9 Nagarro: Sin cambios en sus previsiones respecto a lo reportado con FY25

🔹 $GLOB Globant sin cambios de previsiones

🔹 $EPAM Recortó la guía de ingresos en su rango medio, de 6% a 5.3%, con menor crecimiento orgánico (de 3%-6% a 2.5%-5%.), aumentando EPS esperado

Nagarro. Previsiones para 2026:

🔹Ventas: Aumento del 3.1% en su rango medio

🔹Esperan mejorar tanto el margen bruto como el EBITDA ajustado.

La acción cayó un 10% 🩸

$NA9 #NA9

14

2,102

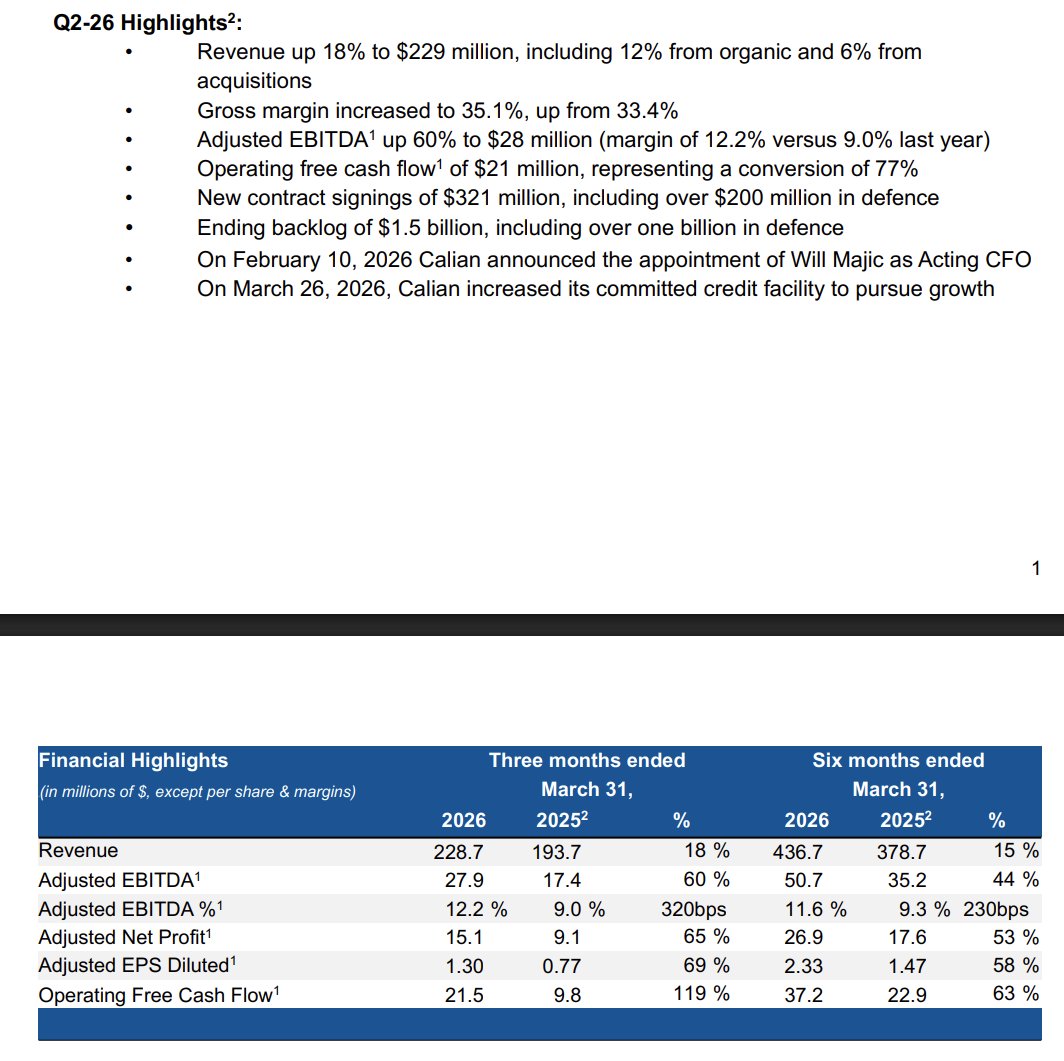

$CGY $CGY.TO

Calian has presented a strong Q2, with strong organic growth (12%), margin expansion, and good cash generation.

Let's see how the market opens, but I don't think the market is properly reflecting the company's current performance and future expectations.

$CGY.TO $CGY

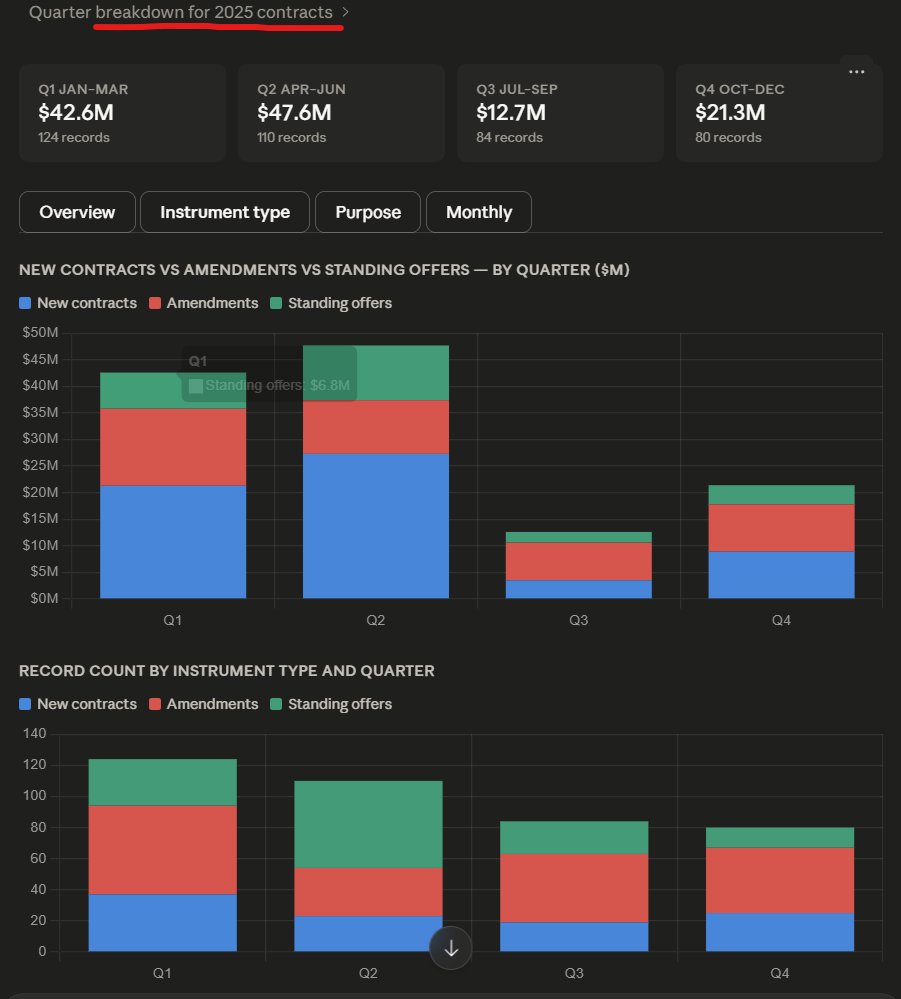

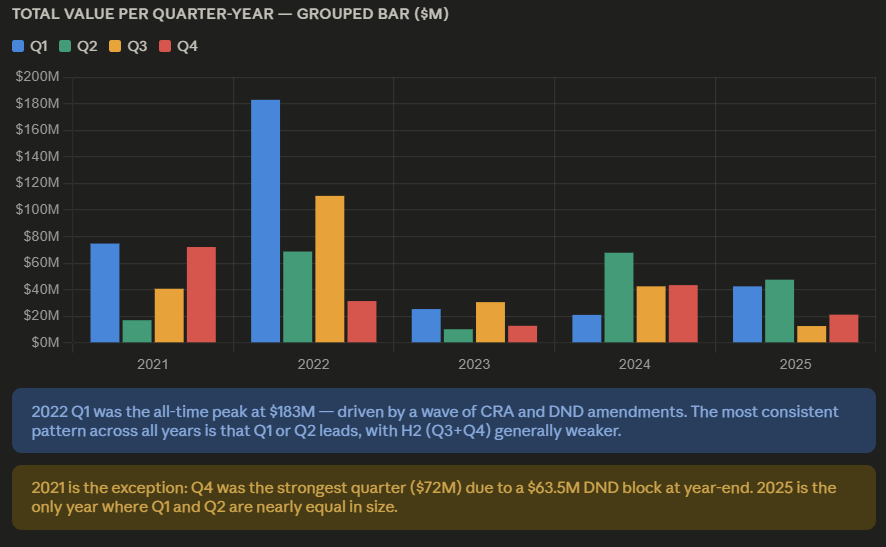

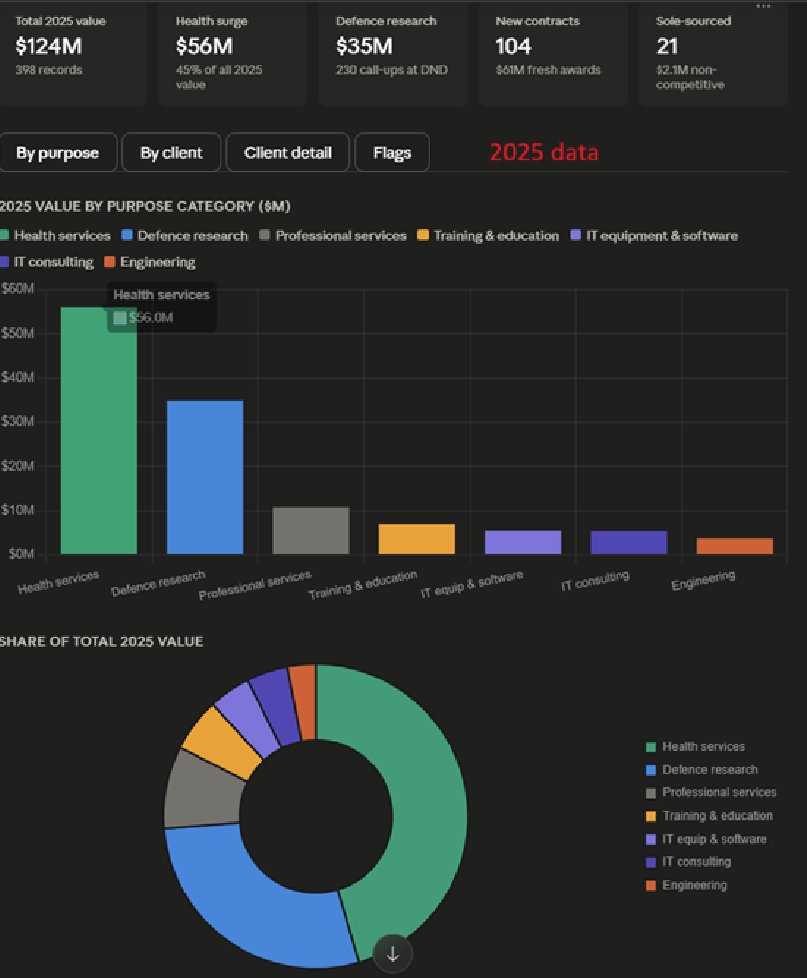

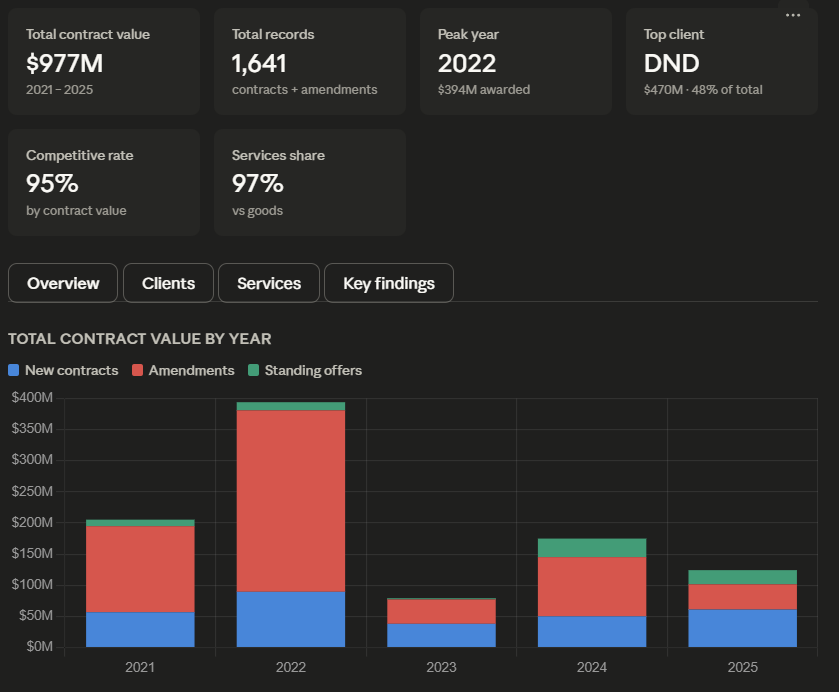

I was looking in more detail at Calian's contracts in Canada. Using the information available in "open government", which has a delay of 4-5 months in publishing (contracts >10k), there is some interesting information I wanted to share (using Claude to analyze the 1,641 contracts in the last 5 years).

‼️Key point: the C$200m signed in Q1 (Q2 for Calian, January-March) represents 4x the size of 25Q1, or 2x the size of 25H1.

🔹In 2025 they won C$123.7m in contracts, out of which C$61m were new contracts and C$40m amendments. Most of the contracts were awarded in Q1 (C$42.6m) and Q2 (C$47.6m) 2025. The point that Calian has signed C$200m in 26Q1 alone makes that announcement more important/meaningful.

🔹By "purpose", the most relevant category in 2025 was health care (C$56m) and Defence Research (C$34m). Nevertheless, health care is also mainly related to defense (65%-70% globally), so we can say most of Calian's contracts in 2025 were related to defense, so it is a fair comparison (but we are being conservative). If we look at government clients, Calian got contracts mainly from National Defence valued at C$60m and the Canada Border Services Agency C$40m.

🔹It may also be relevant to say that C$64.7m in contracts were awarded in March/April. So we should not expect to get similar communications (of that size) for the rest of the year.

This may give us a better understanding of the size of that announcement. Not sure the market has fully priced that in.

If anyone is interested, I can share the dynamic tables to look at in more detail.

1

6

2,457

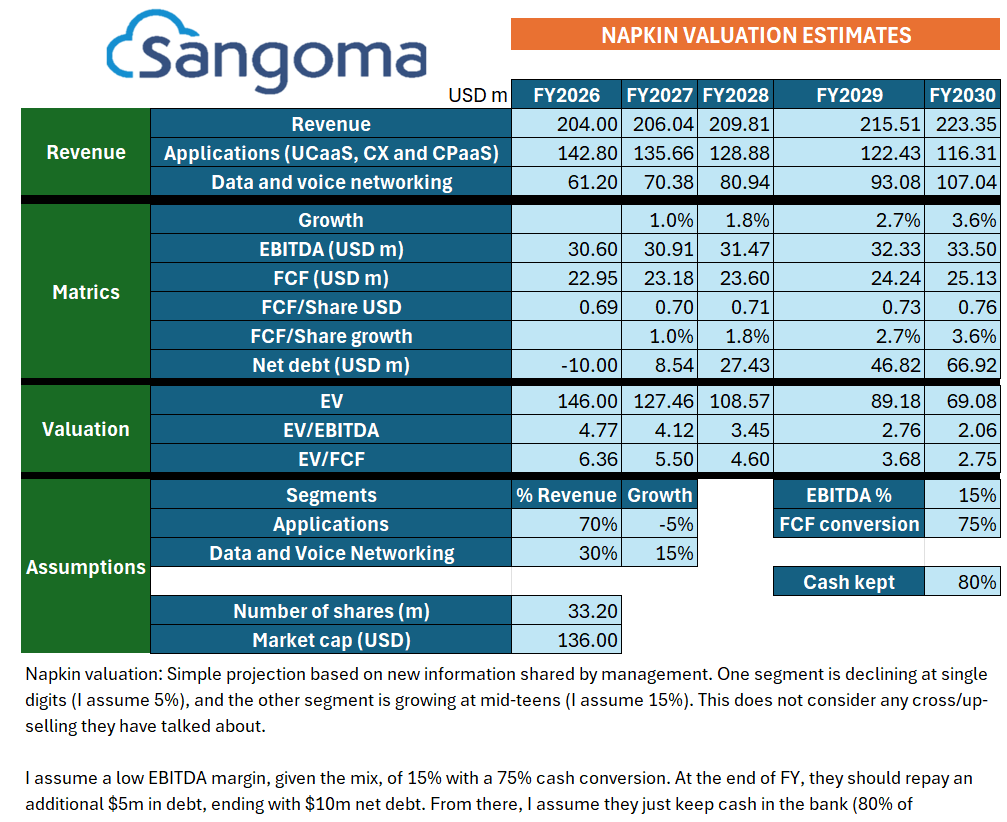

$STC.TO $SANG

In general, I'm not happy with the results Sangoma presented yesterday for Q3 FY26.

It is good they adjust to market changes, but we are again seeing a new pivoting of the company, now focusing on data and voice networking, where they see higher growth.

Few points:

🔹They have reduced the FY26 guidance just a few months after confirming it. They are blaming the international part of the business and the current macro situation. They have better visibility, but I guess the pressure on prices, due to high competition (which they were already accounting for), may have a greater impact.

🔹They now provide a breakdown of 2 segments. One is declining at single digits (Applications, high competition), which represents 70% of revenue, and the other, Data and Voice Networking, is growing at mid-teens, representing 30% of the business.

🔹They have opened a strategic review, but I completely disregard this comment. To me, this is just a distraction if they have not had any concrete proposal and are just exploring.

🔹On the positive side, they have indicated that they have seen positive developments on previous deals, mentioning that a previous deal of $150k MRR has increased to $200k MRR in a few months.

🔹The issue with why revenue is not yet showing the impact of previous deals continues to be execution. The deal they closed in Q2 (350 locations, with $150k MRR, now at $200k MRR) is just 15%-20% implemented. Delays are coming from clients' locations.

🔹Financially, the balance sheet remains strong, and they keep printing money while keeping costs under control. Lower margins are due to the revenue mix (which I don't mind as long as they have high growth).

I have confidence in the management, as they have done a great job with the transformation, but there always seems to be a reason to blame the lack of growth, with another pivoting now. They keep focusing on creating shareholder value, which is good, as insiders own a large portion of the company (from memory, close to 25%).

Based on the new information shared about growth, I have run a napkin valuation with very conservative assumptions (no acquisitions/buybacks, low EBITDA margin). I don't assume any up-selling like the example they mentioned.

I get an EV/EBITDA of 4.8x for FY26 and 4.1x for FY27. For the low expected growth (base and conservative approach), it seems fairly valued and market had already discounted this (let's see how market opens)

But I don't see any clear catalyst in the short term for the company. Management keep indicating int he call they are many indications of growth, but it does not materialize. I will review the position, and I may look at cutting the position size.

Happy to hear other views.

3

5

403

$CGY.TO $CGY

I was looking in more detail at Calian's contracts in Canada. Using the information available in "open government", which has a delay of 4-5 months in publishing (contracts >10k), there is some interesting information I wanted to share (using Claude to analyze the 1,641 contracts in the last 5 years).

‼️Key point: the C$200m signed in Q1 (Q2 for Calian, January-March) represents 4x the size of 25Q1, or 2x the size of 25H1.

🔹In 2025 they won C$123.7m in contracts, out of which C$61m were new contracts and C$40m amendments. Most of the contracts were awarded in Q1 (C$42.6m) and Q2 (C$47.6m) 2025. The point that Calian has signed C$200m in 26Q1 alone makes that announcement more important/meaningful.

🔹By "purpose", the most relevant category in 2025 was health care (C$56m) and Defence Research (C$34m). Nevertheless, health care is also mainly related to defense (65%-70% globally), so we can say most of Calian's contracts in 2025 were related to defense, so it is a fair comparison (but we are being conservative). If we look at government clients, Calian got contracts mainly from National Defence valued at C$60m and the Canada Border Services Agency C$40m.

🔹It may also be relevant to say that C$64.7m in contracts were awarded in March/April. So we should not expect to get similar communications (of that size) for the rest of the year.

This may give us a better understanding of the size of that announcement. Not sure the market has fully priced that in.

If anyone is interested, I can share the dynamic tables to look at in more detail.

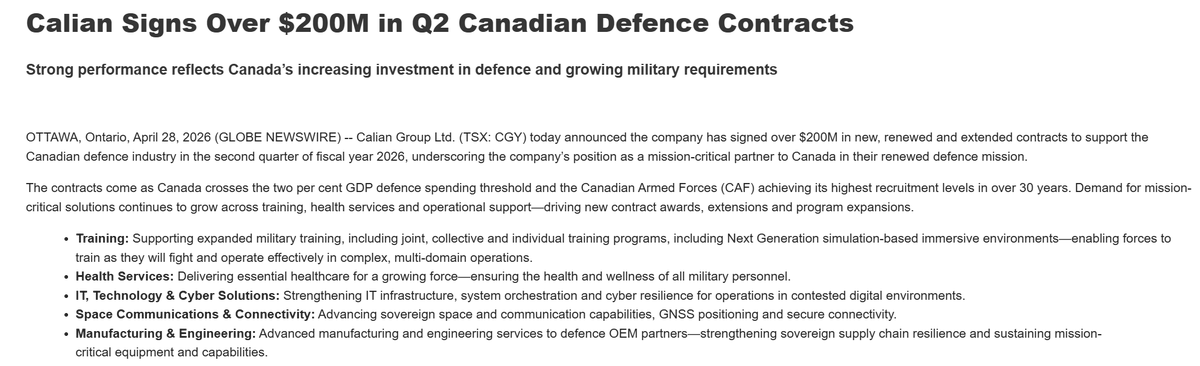

$CGY.TO $CGY

Calian signs over $ 200m in Q2 Canadian Defence Contracts:

🔹Previous backlog $1.4bn (est. revenues in 2026 of $ 850m)

🔹This contract is with Canadian military. Canada represents 56% of revenue (but not clear how much of that is from Defence in Canada alone, but goverment contracts overall are lower than that, 52%)

So quite good news for Calian.

5

3,123

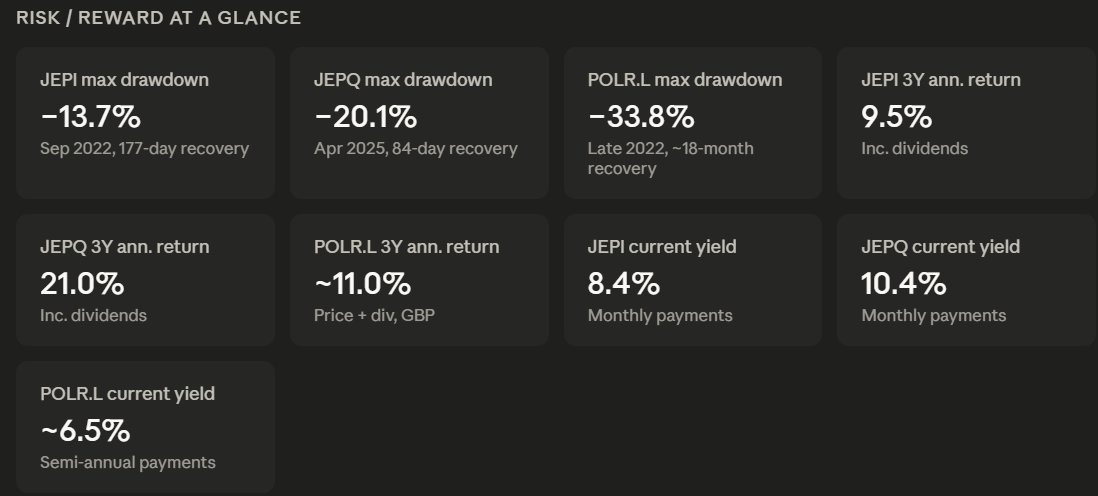

$POLR $POLR.L #POLR

Polar Capital is c. 6% up today following a rating upgrade from Deutsche Bank, raising their price target to GBP 10 (now GBP 7.5).

This is an AM I have been following for a long time and entered last year. They are doing well with an increase in AuM due to market performance, but also due to net inflows.

This position is in my Income Portfolio, returning now a 6% yield, far lower than when I bought it.

I reduced part of my position at GBP 6.22 as it was quite sizable back then, representing now 7.4%.

Given the current market situation (all-time highs with a not very stable geopolitical situation, oil prices, etc.), I think this stock (price) can suffer severely in a market correction. So I will be looking to rotate the full position.

In my Income Portfolio, I don't focus just on yield, but also on protecting principal. If I can redeploy the capital gains into a higher-yield security while reducing the risk, that's a preferable option.

I was using Claude to calculate the max. drawdown of Polar and potential alternatives, showing the following:

Max. drawdown:

🔹 $POLR.L -33.8% in 2022 (18-month recovery)

🔹 $JEPI -13.7% (177-day recovery)

🔹 $JEPQ -20.1% (84-day recovery)

Current yields:

🔹 $POLR.L 6.5%

🔹 $JEPI 8.4%

🔹 $JEPQ 10.4%

Based on that information, which I need to validate, but it is a quick way to validate my "impressions," in the current situation $JEPI may offer a better risk/return profile. I keep generating income (slightly higher) and I protect the principal.

In a market correction, Polar will suffer more than twice as much. At such a moment (market correction), is when we could rotate again to Polar (or another AM), which may have a higher yield back then and wait for market recovery.

$POLR $POLR.L Very positive news if confirmed! I was wondering whether this publicity in Bloomberg (article from February) would result in an increase in AuM on that fund. Maybe it contributed with delay :)

I reduced my position at GBP 6.22, but it still represents 7% of my Income Portfolio.

financialpost.com/pmn/busine…

1

440

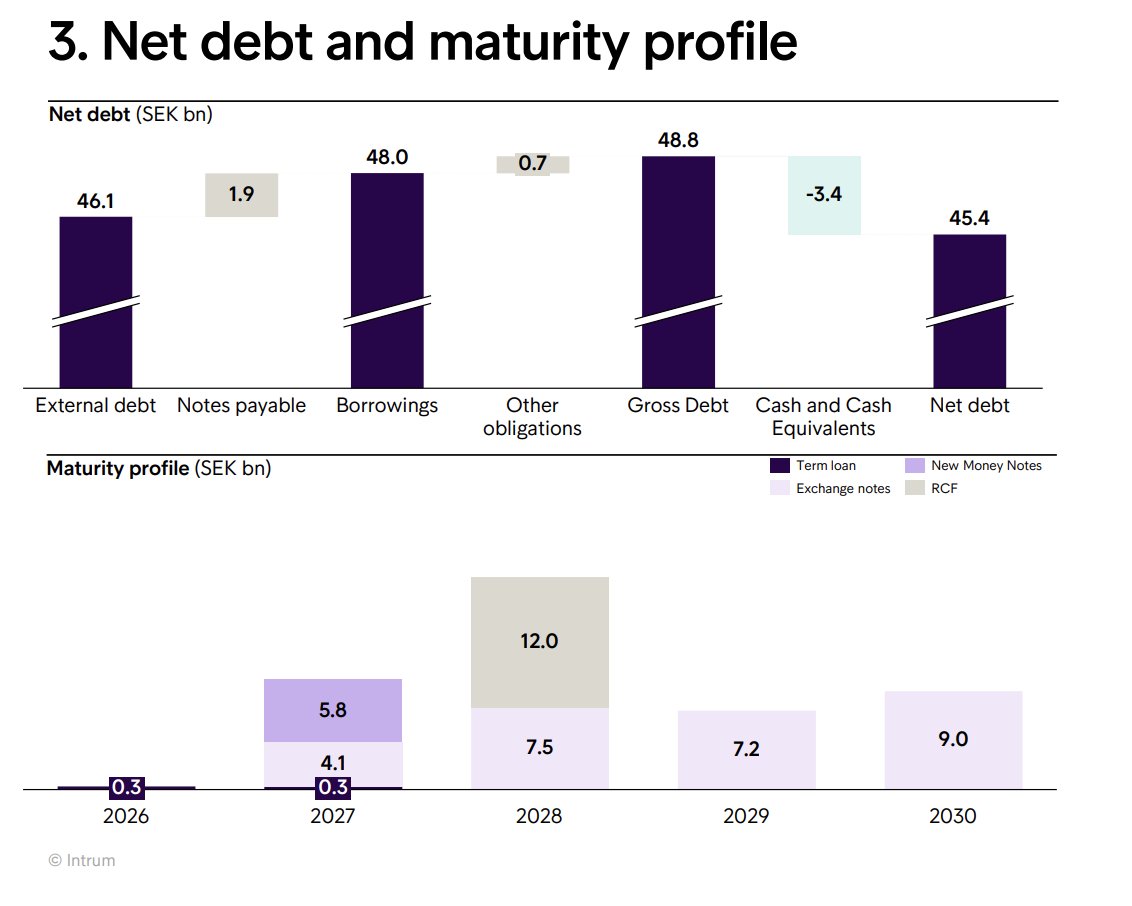

$INTRUM.ST Intrum AB

European debt collector. They have released their Q1 today, showing an improvement in profitability. Nevertheless, their debt load is still a concern.

The stock has opened at -30%, mainly driven (in my view) by their announcement of raising SEK 7.5 billion in capital (market cap now, after the drop, SEK 4bn).

Those aren't good news for current shareholders, but it really reduces their financial risk.

Management has confirmed they will subscribe to the capital increase, and they made significant stock purchases in September 2025 at SEK 45-50.

I don't own the company, but I'm following it. It is still too difficult for me to assess the downside risk, so I'm not investing.

The stock has recovered and is now trading at -14%.

3

619