Nothing I say is financial advice

Joined October 2024

- Tweets 120

- Following 520

- Followers 132

- Likes 669

2 Photos and videos

Inverted Mikey retweeted

The 2Y to 10Y curve has flattened below 40bp, a 14 month low.

The lower this goes the worse it is for credit expansion at banks.

That’s bad for tech stock but it’s great for Main Street and lower mortgage rates.

I can’t find any math that interferes with a protracted period of power flattening.

It will produce a special K economy where Main Street thrives and Wall street gets reigned in.

Women have received 80% plus of the Jobs since Trump 2.0 and experienced a greater reduction in woman’s unemployment which will lead to higher wages.

This is wonderful and as the treasury follows flatter on its path to equilibrium male jobs that are more interest rate sensitive will join the Main Street party.

1

3

12

2,424

Inverted Mikey retweeted

@tracyalloway @TheStalwart @hendry_hugh

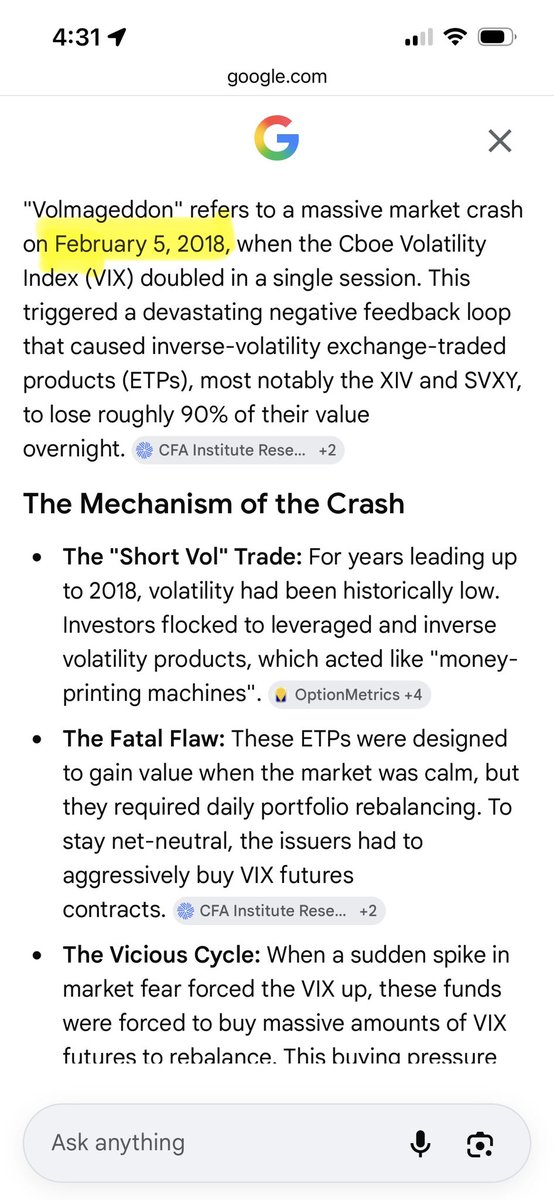

SP500 Volmageddon was Feb 5, 2018

Bitcoin Volmageddon was Feb 5, 2026

BTC Vega doubled from 46 to over 90 in 2 days and the day prior to MSTR earningS in part because people were worried that the poorMSTR performance would force Saylor to announce that he would tactically sell Bitcoin to be able to support an “undervalued” price of MSTR. That was 1 quarter early.

From the chart, I posted NDX Vega divided by S&P vega is essentially at the highest in eight years and that’s a large part due to the fact that too many people are hedging their technology massive overweight from historic norms through VIX and the cost of hedging VXN despite the inclusion of Walmart, Gilead and Pepsi in the NASDAQ 100 has risen to more than a 50% premium versus a typical 20% premium and that premium is now at an 8 year quarterly closing level and rising. VXN/VIX is a pressure gauge of a system that has so much leverage and volatility suppression through ETFs, structure, note, funds, algorithms swing traders and contingent traders.

This is a pressure gauge that’s about to exceed its historical limits.

The 2008 highest quarterly close was 7 above today’s close.

Excessive policy easing via the reversal of QT to QE and other forms of stimulus had added to the momentum of the volatile suppression dynamic, which is now achieving an eight year high but 17 points more will take this back from 2018 back to 2003 23 years ago and near the low of the dot com era.

Unlike the peak in 2000 when Greenspan fed stood there and let tech stocks fall 57% in 10 months without cutting one basis point, our past chairperson of the fed Jerome Powell, reduced quantitative tightening by 150% and lowered the Fed funds rate by 175 basis points.

Historically, later in the easing cycle of policy, its effectiveness is less because the curve is steeper.

We are about to see based on quantum economics the failure to contain volatility suppression, and we’re gonna get a NASDAQ Velma Gedhun, even as the S&P volatility stay suppressed because people are mistakenly using that as a hedge or as a liquity harvest theta

Policy makers made cyclicals appear like the tech sector was non cyclical and appear as a growth sector due to systematic policy support of the long end of the yield curve and financials by Jerome Powell, and as they hand off the chairmanship to Warsh who now has almost an empty shed of policy and will not be able to suppress VXN volatility versus the S&P.

We’re gonna unleash enormous tech selling which will triggering massive capital gains taxes, a stronger dollar, disinflation, and a violent bid that starts off slow in the long end of the curve, which will squeeze out the volatility and mortgages exacerbating the problem and my great volumes will migrate from tech to housing and you can’t unsee divided by VXN/VIX once you look at it.

I was at Hugh Henry’s Acid Capitalist finance summer camp last summer an amazing teaching environment, and hopefully I’ll be joining again. It’s an amazing event that pays for itself in, my view multiple times over.

I was screaming at the top of my lungs in the local St.Barths theater in front of the audience, begging people to focus on this data set, which was at zero and now the cost of hedging and the NASDAQ is more than 50% more than the S&P and there is very little in the terms of tools or weapons or policy that can suppress this much longer and this data set in 2001 was 230 and so as NASDAQ volatility rises mechanically institutions will be reducing exposure because they won’t need that level of exposure. Given the level of volatility. You just do the dot product of Capital at risk times volatility to get your targeted return and you’ll just reduce capital and put it into treasuries, which will exacerbate the problem because so many people are funding their tech intrusion unwind sets up the greatest bull market ever just Nov 2008.

3

14

929

It is fascinating that nobody other than @PolarityRadio is discussing VXN/VIX. On track for the highest daily close in 8.5 years! Acceleration of leverage unwinding right in front of us

1

1

6

1,691

Highest daily close for VXN/VIX since October 2018. Lowest daily close for the

US10Y-US02Y spread since April 2025. Smells like acceleration @PolarityRadio

45

Inverted Mikey retweeted

Are you watching? 👀

USD/JPY

“Japan just burned through $73.6 billion trying to prop up the yen.

It didn’t work particularly well.

The USD/JPY pair has been hovering around 159 in late May 2026, repeatedly knocking on the door of the psychologically critical 160 level.

With the Bank of Japan’s next policy meeting set for June 15-16, the next two weeks look like a pressure cooker…”

@Crypto_Briefing

13

38

158

6,779

Inverted Mikey retweeted

If GOOGL cannot recapture yesterday's low that's gonna be an island.

Was not expecting that.

10

9

119

8,246

Getting closer. Revenge of low beta loading @PolarityRadio

Jun 2

CBOE DSPX (dispersion) is now the 3rd highest reading of this index ever, second only to Tariffs in Apr 25 and Covid in 2020.

DSPX measures the IV of the SPX to the IV of single stocks and marks the degree to which they differ from each other.

This says people expect single stocks to move a whole lot more that than the index.

You may have caught on that the previous highs were during crisis periods. In both Covid & Tariffs there were very clear winners and losers and that drove volatility expectations.

Here its AI or bust.

ALT CBOE DSPX 3rd highest reading ever.

46

Inverted Mikey retweeted

Jun 2

CBOE DSPX (dispersion) is now the 3rd highest reading of this index ever, second only to Tariffs in Apr 25 and Covid in 2020.

DSPX measures the IV of the SPX to the IV of single stocks and marks the degree to which they differ from each other.

This says people expect single stocks to move a whole lot more that than the index.

You may have caught on that the previous highs were during crisis periods. In both Covid & Tariffs there were very clear winners and losers and that drove volatility expectations.

Here its AI or bust.

ALT CBOE DSPX 3rd highest reading ever.

14

37

210

21,054

Bitcoin no longer reacts to these headlines. Sign of things to come?

Jun 1

TRUMP SAYS HE THINKS IRAN DEAL COULD HAPPEN OVER NEXT WEEK: ABC

78

On track for the highest close in VXN/VIX since October 2018…@PolarityRadio

3

3

1,004

Inverted Mikey retweeted

22

20

34

4,922

Inverted Mikey retweeted

42

15

30

6,084

Inverted Mikey retweeted

12

9

19

5,476

Inverted Mikey retweeted

35

13

26

4,931