Joined November 2020

- Tweets 31,604

- Following 951

- Followers 56,029

- Likes 46,343

4,077 Photos and videos

Pinned Tweet

18 Aug 2025

In-depth reports I have published on S*stack so far...

- Deere $DE (free)

- FRP Holdings $FRPH

- Five Below $FIVE

- Diageo $DEO

- Hermès $HESAY

- Atlas Copco $ATCO.B

- Stevanato $STVN (free)

- Keysight $KEYS

- Zoetis $ZTS

- Judges Scientific $JDG.L

- Medpace $MEDP

- Trupanion $TRUP

- AAON $AAON

Currently looking into two other interesting companies

The library will keep getting longer!

2

11

109

54,991

Leandro retweeted

Jun 13

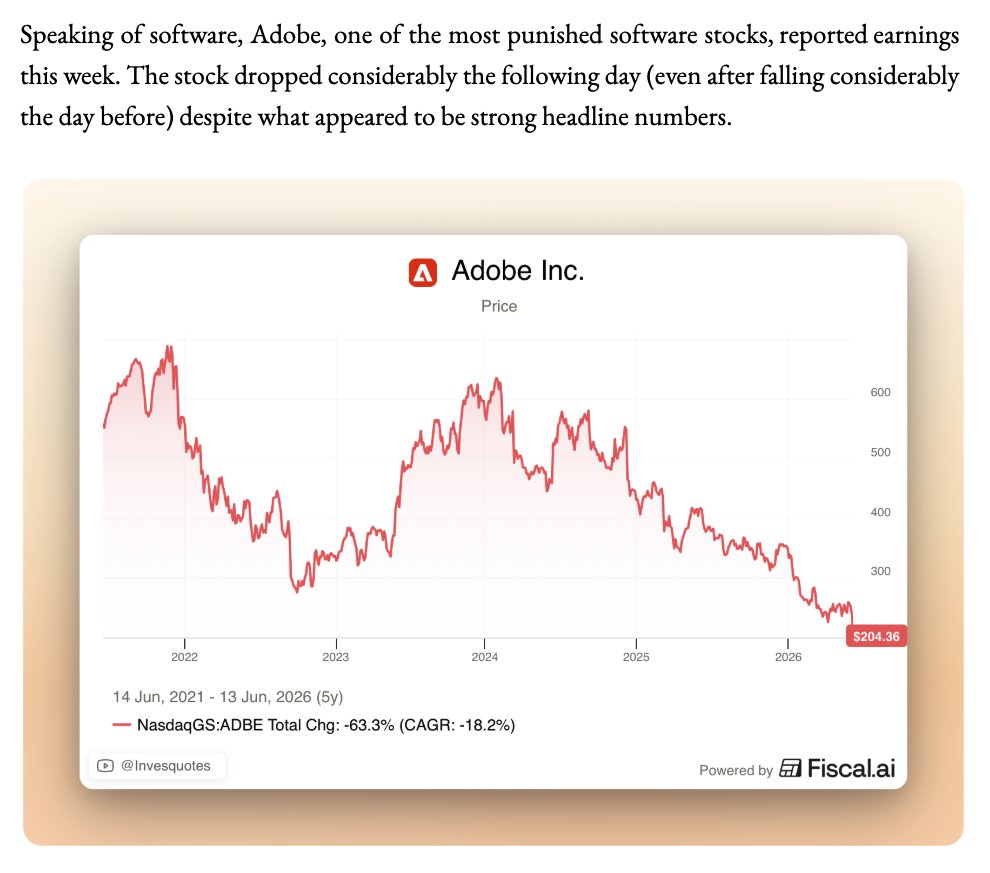

Some expanded thoughts on $ADBE's earnings 👇

From my recent NOTW

5

5

52

9,942

Leandro retweeted

Jun 13

My take from the @AnthropicAI news:

1. Probably good for sentiment in software. If models are already getting capped, then today's environment might be somewhat close to end-state and therefore less concerns around terminal value risk (still TBD)

2. Maybe LT positive for semis because compute has to be built pretty much everywhere to avoid restrictions, but somewhat bearish in the sense that maybe we don't need as much compute in the US (I think it'll be the former)

3. Probably not great in terms of investment sentiment into AI. The government has shown that they can (and will) limit AI when/as needed. Don't think Dario's (and the industry's speech) regarding AI displacing labor was what politicians wanted to hear

The second derivative which invalidates all of the above is that the AI trade is so important for US indices that the President TACO's and we go back to square one (high likelihood if markets go south next week)

Just my 2 cents, thoughts welcome!

6

2

39

9,923

Jun 13

Coming out in a couple of hours!

Quite a few relevant events this week for markets.

12

2,124

Leandro retweeted

Jun 12

3

5

57

9,162

Jun 12

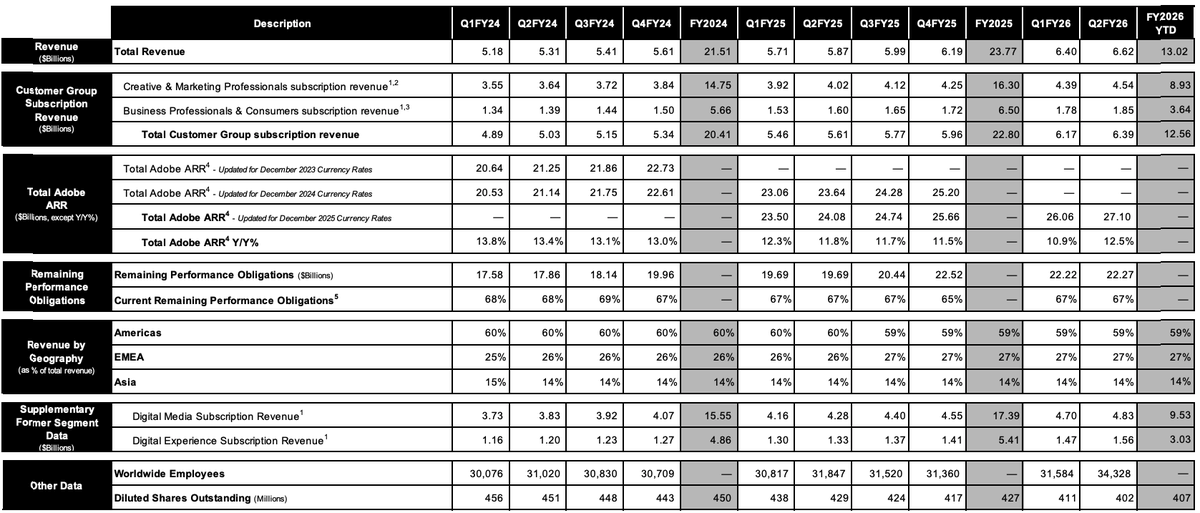

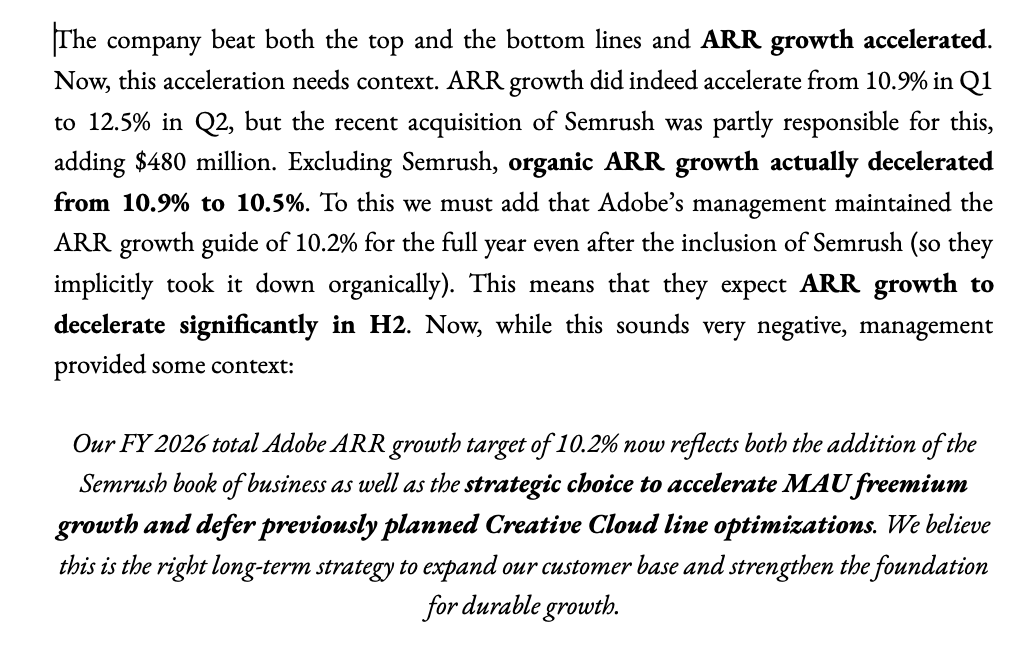

So, Adobe's Total ARR grew 12.5% in CC in Q2. If we exclude $480 million that comes from Semrush, then actual organic growth was 10.5%, a deceleration from 10.9% last Q.

Management left the FY guide unchanged at 10.2% despite Semrush, meaning that they expect more decel

In all fairness, a good chunk of AI-first revenue likely bypasses ARR, but it's definitely not the acceleration that many are promoting here...

$ADBE

14

2

68

23,832

Jun 11

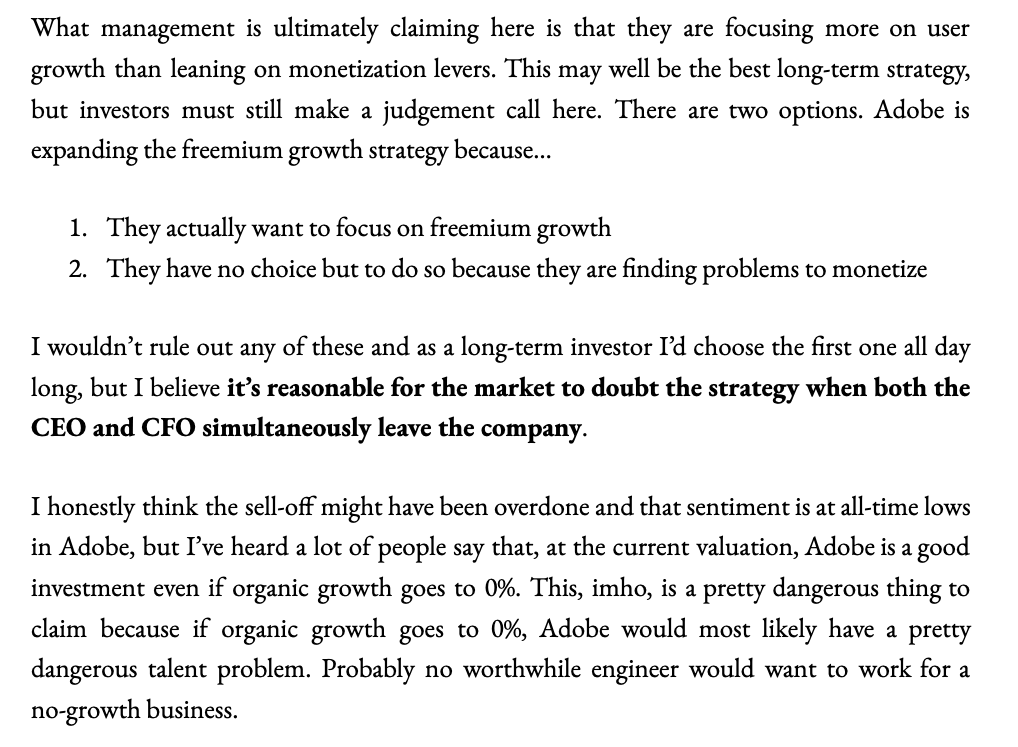

Adobe’s $ADBE earnings look pretty good but…

1) CFO leaving suddenly just like CEO

2) Lack of disclosure around certain metrics important to understand the AI bear case

3) Lack of insider buying

Not great signs overall, but nothing evident yet in the numbers so who knows

25

8

154

37,219

Jun 11

Baffles me how many executive teams think that it's perfectly fine to issue debt to repurchase "very cheap" stock but don't think it's a good enough price for them to buy in the open market

And yes, I get the point that they need to diversify!

2

23

3,821

Jun 10

Enjoyed the conversation a lot but why do tech investors always feel the need to come up with a metric that theoretically simplifies business quality?

The prior rule of 40 (growth margin) was terrible in its own right because it more or less claims that you can freely interchange growth and margin, which is certainly not the case. Would you rather own:

1. A 30% growth business generating 10% margins

2. A 0% growth business generating 40% margins?

I know what I’d rather own and it’s not even close, but both screen as rule of 40 companies. The case is even worse when one considers that margins tend to be adjusted in many cases.

The new rule of 40 discussed here (proportion of AI revenue AI market share) doesn’t even have a profitability metric because most AI-native business are not yet generating profits (who knows what the future holds, though)

Don’t know what to think about it, but either way, enjoyed the conversation

My conversation with Alex Sacerdote, founder of Whale Rock Capital Management.

Alex runs more than $17B and has been one of the best performing tech investors for years, though he keeps a low public profile.

As you'll hear, he is singular in how he thinks about investing through technology cycles.

For over 25 years, he has built his entire investment framework around a single idea, the S-curve.

We discuss:

- The AI L-Curve

- When to buy into an S-curve and when to sell out

- The de-commoditization of data center hardware

- Why he went net short software

- His two models for tech adoption

- Finding alpha

Enjoy!

Timestamps

0:00 Intro

9:55 AI's L-Curve

19:31 Whale Rock's S-Curve Playbook

26:14 Spotting Inflection Points

32:02 Finding AI Winners

40:04 AI vs Software

48:13 The Hardware Renaissance

58:04 Why Investors Miss AI

1:05:18 Whale Rock's Research Machine

2

33

7,955

Jun 10

14%

8%

2%

4%

Honorable mentions:

23%

6%

SPY -4%

So far so good, but they are all still cheap.

May 28

I am buying these 4 companies today.

I believe they offer very attractive risk-adjusted returns and have gotten caught up in misleading narratives.

Time will tell!

In the usual place.

1

26

7,734

Jun 10

There were fewer incremental positive news for Stevanato when it was at $27 than today when it sits at $17, which is kind of crazy if you think about it

- Orals penciling out to be 30% of the GLP-1 market (with fewer uncertainty than several months ago)

- Biologics advancing through the pipeline and starting to show up in the numbers

- Cartridges transitioning to RTU

- Management making the claim that higher dosages don't necessarily cannibalize lower dosages because they grab their fair share of value

- Probably the two most bullish investor conferences ever for the company

$STVN

2

33

3,891

Jun 10

Everyone is talking about the AI mega-trend (and for good reason) but few are talking about the healthcare/biologics/injectables mega-trend that will be with us for a pretty long time ( GLP-1s)

FDA already piloting AI to accelerate drug approvals

3

1

36

4,216

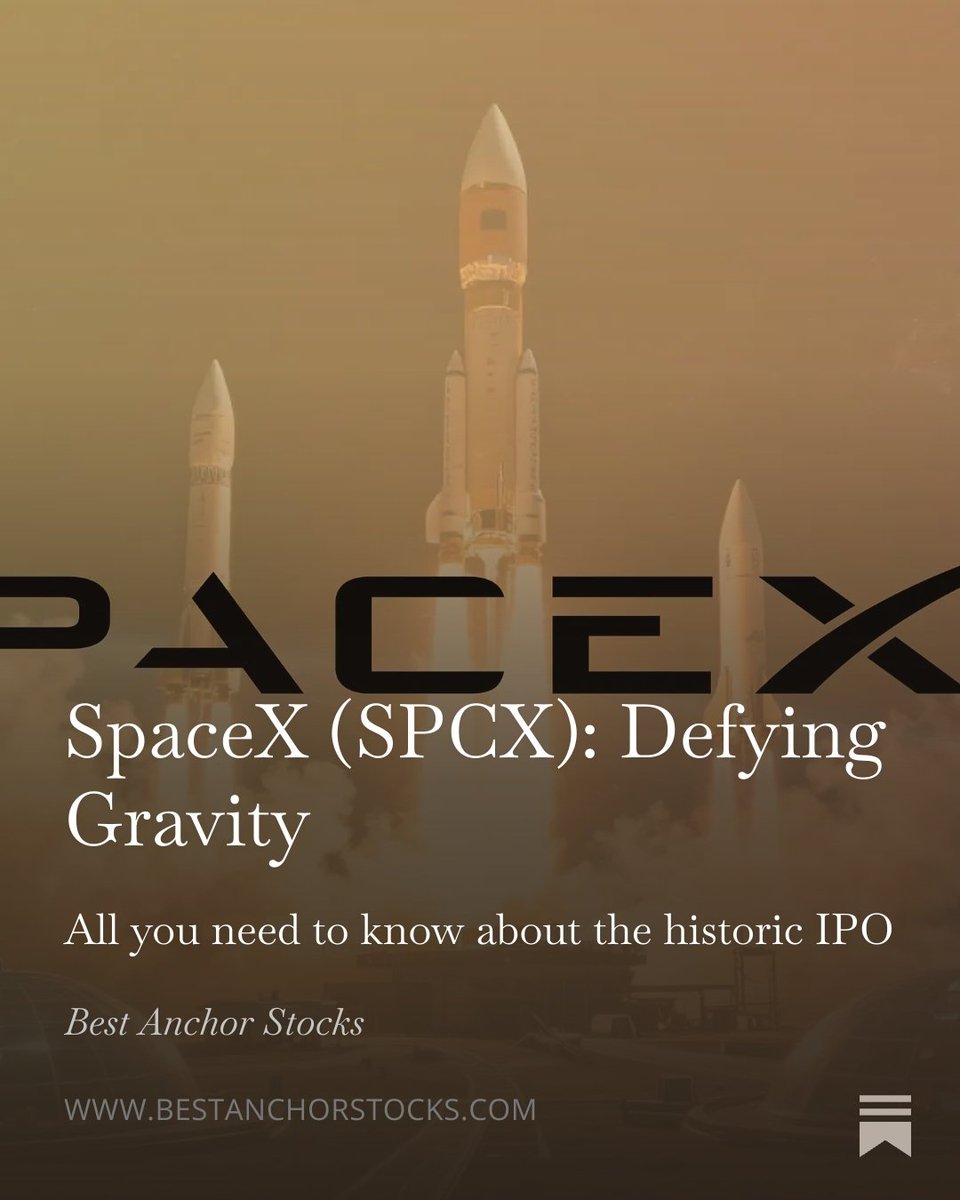

Jun 10

Just published something on SpaceX $SPCX

We go over a wide variety of topics and should help you understand the business better (even if you are not thinking about going to the IPO!)

Find it in the usual place!

3

11

2,647

Jun 9

If Nintendo manages to “save” FY 2026 with price-hike pull forwards Zelda Ocarina of Time remake I think the SW2 ecosystem is going to become massive pretty fast.

FY 2027 comes with:

- Pokemon

- 3D Mario (likely)

- Xenoblade Genesis

And with a higher-priced SW2

$NTDO.NE

6

36

6,669

Jun 9

1/ Some weeks ago I launched a new recurring series where I share companies on my watchlist — before they potentially make it into my portfolio.

4 issues in; 4 free picks shared thus far!

Here's a quick summary of each 👇🏻

2

22

4,225

Jun 9

5/ Belimo (SWX: BEAN)

A Swiss industrial making HVAC actuators and control valves — two products, focused exclusively, with 20-30% global market share.

Exposed to liquid-cooled data centers, semiconductor fabs, and pharma manufacturing.

Great business, but rich valuation.

1

6

1,626

Jun 9

6/ 4 very different businesses. Different geographies, different models, different situations.

That's the point of On The Radar, to show what the funnel looks like!

New issue every two weeks. The first pick in each is always free! Subscribe here: bestanchorstocks.com/

1

6

1,497