Joined December 2018

- Tweets 1,629

- Following 193

- Followers 2,185

- Likes 881

322 Photos and videos

Pinned Tweet

May 24

I genuinely think India’s power transmission and cable story is a multi year compounding story… and we are still very early ⚡️

Not early in the way people casually use the word in markets.

Early because the real demand shock hasn’t even arrived yet.

India just touched ~250 GW peak power demand for the first time ever this summer.

And this happened BEFORE:

• mass EV adoption

• AI data center explosion

• semiconductor fabs

• full manufacturing scale up

That’s what makes this interesting.

Because India’s per capita electricity consumption is still only ~1,400 kWh.

China is at ~6,500 kWh.

USA is above ~12,000 kWh.

Think about how absurd that gap is.

We are trying to build a $10 trillion economy while consuming barely 20-25% of the electricity China consumes per person.

At some point, that gap HAS to close.

And when it does, India will need one of the biggest electrical infrastructure buildouts in its history.

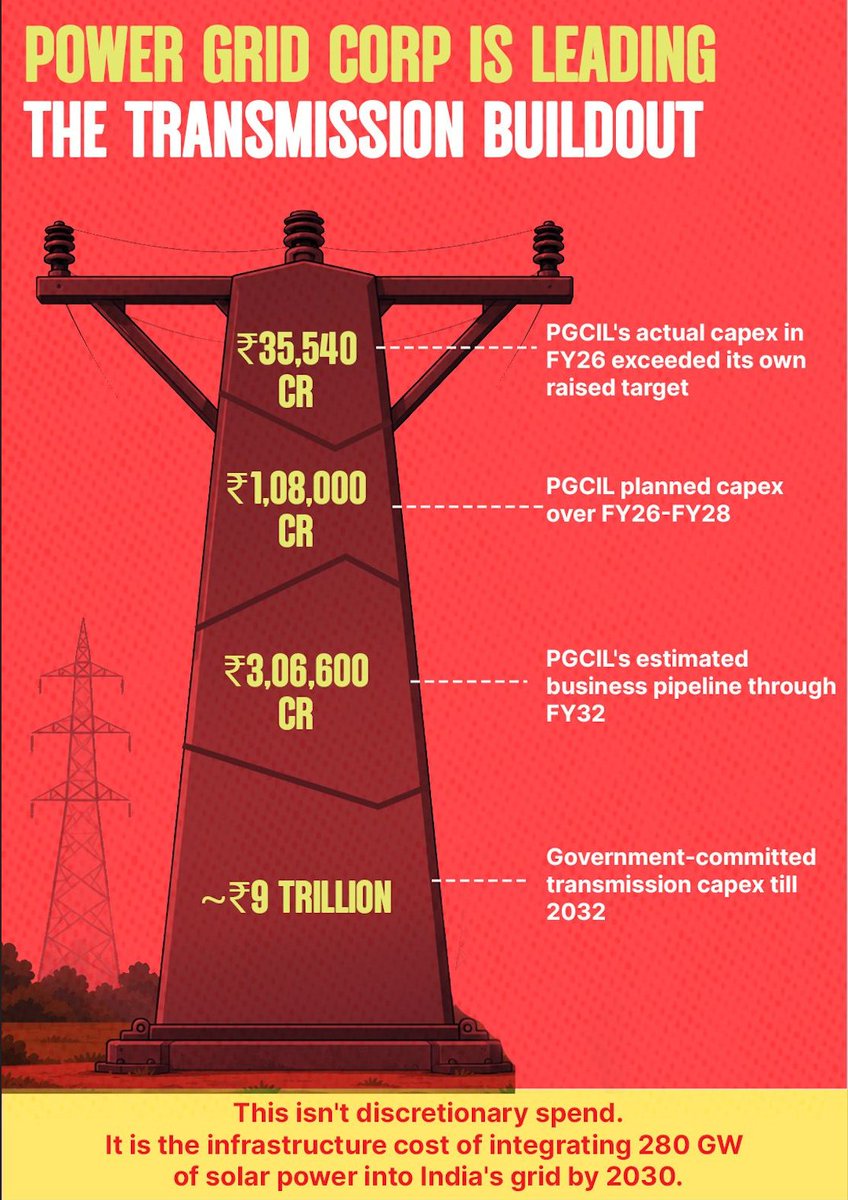

That’s exactly why the government has already committed ₹9.16 TRILLION toward transmission upgrades by 2032.

Not generation.

Transmission.

Because the real challenge is no longer producing electricity.

The challenge is moving electricity fast enough to where demand is exploding.

And demand is exploding everywhere simultaneously.

India’s electricity demand is projected to grow ~6.4% CAGR till 2030.

Then comes AI.

India’s data center capacity was ~1.4 GW in 2024.

Another ~5 GW is expected by 2030.

And AI server racks consume 5-6x more power than traditional cloud infrastructure.

Every AI query eventually becomes:

a transformer, cable, switchgear and transmission line story.

Then add EVs.

Then add fully electrified railways.

Indian Railways alone eliminated ~17.8 BILLION liters of diesel consumption after electrification.

Then add renewables.

India wants 500 GW non fossil fuel capacity by 2030 and plans to add ~470 GW solar wind capacity over the next decade.

But here’s where the real bottleneck starts appearing:

The best renewable energy locations are sitting in Rajasthan, Gujarat and Ladakh…

while the actual demand sits in Mumbai, Delhi, Bengaluru and industrial corridors.

So India now has no choice but to rebuild the electrical spine of the country.

Transmission network expansion:

~4.85 lakh ckm → ~6.48 lakh ckm.

Transformation capacity:

1,251 GVA → 2,342 GVA.

This is not incremental growth.

This is an entirely new grid being built in real time.

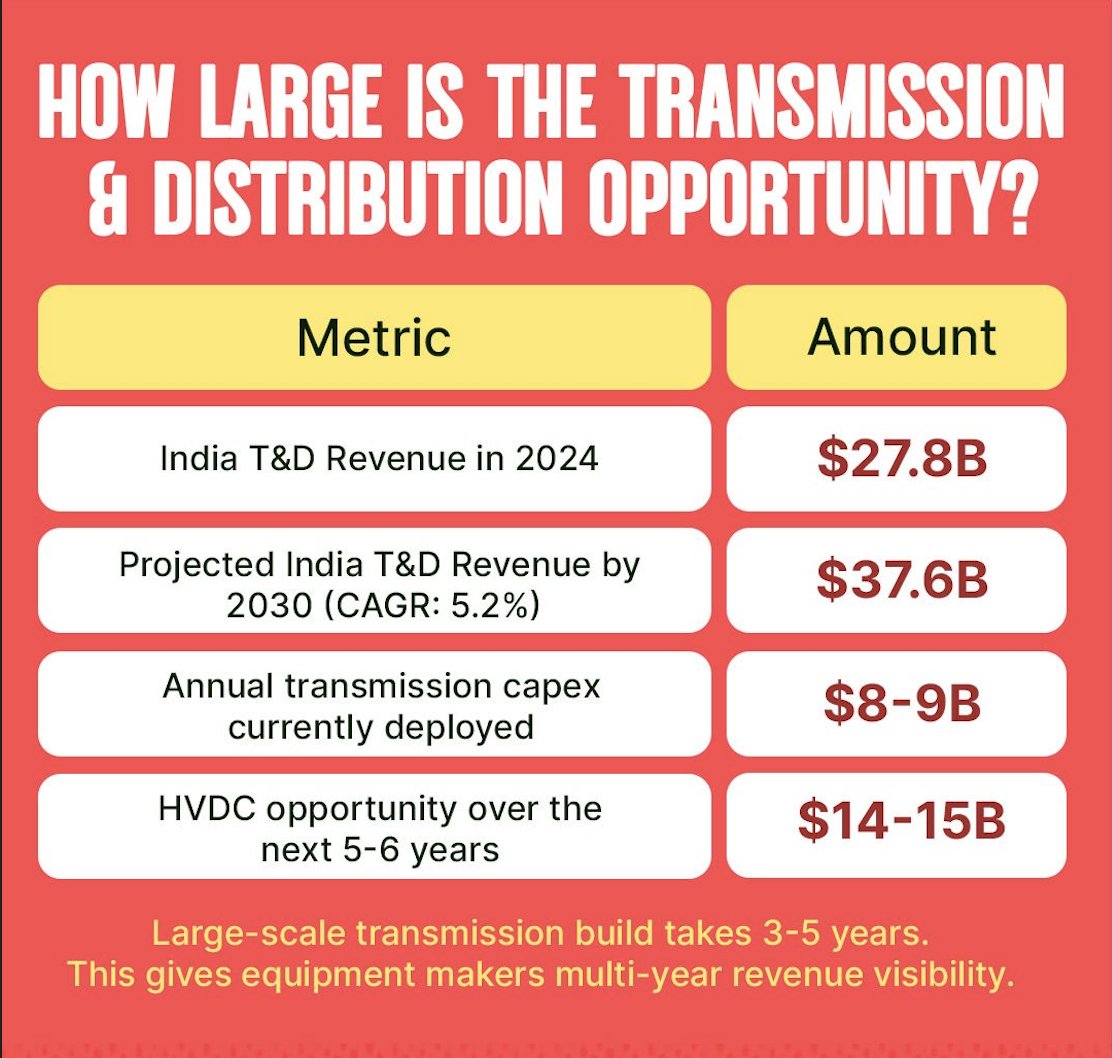

And this is where the cable story becomes massive.

Because globally, high voltage cable capacity is already tight.

Europe and the US are aggressively spending on:

• HVDC corridors

• offshore wind interconnectors

• grid modernisation

• renewable evacuation

Global cable giants like Prysmian, Nexans and NKT already have multi year order visibility because HV/EHV cable demand is exploding globally.

And these are not easy factories to build.

HV/EHV cable plants require:

• specialised machinery

• technical approvals

• years of execution expertise

• very high capital investment

Which means supply cannot suddenly appear overnight.

That’s why utilisation levels across serious cable manufacturers are running extremely high.

And now India is entering the same cycle.

The Indian wires & cables industry itself is expected to move toward a ~₹1.9 lakh crore opportunity over the coming years driven by transmission, renewables, railways, real estate, industrial capex and exports.

And look at what Indian players are doing already:

Polycab already commands ~25-26% market share in India’s wires & cables industry and has been aggressively expanding manufacturing capacity across segments.

KEI Industries is scaling capacity heavily toward EPC EHV opportunities because transmission demand visibility is becoming massive.

RR Kabel is expanding aggressively after strong volume growth and export traction.

Dynamic Cables and Universal Cables are directly exposed to transmission and utility capex where demand visibility is now stretching multiple years out.

This is important because once utilisation crosses ~75-80%, cable businesses stop behaving like commodity businesses…

…and start behaving like pricing power businesses.

That’s the phase which may now begin in India.

Because suddenly every meter of cable matters:

• HV cables

• EHV cables

• underground transmission

• renewable evacuation

• industrial electrification

• data center cabling

This is why companies across the ecosystem are reporting insane numbers:

• Hitachi Energy orders up 365% YoY

• Siemens order book above ₹43,000 crore

• BHEL order book near ₹2.4 lakh crore

• PGCIL pipeline above ₹3 lakh crore till FY32

And then there are cable players:

• Polycab

• KEI Industries

• RR Kabel

• Finolex Cables

• Dynamic Cables

• Universal Cables

Most people still see cables as simple housing wires.

I think the market is slowly realising they are becoming strategic infrastructure assets.

That’s the funny thing about infrastructure cycles.

Nobody gets excited in the beginning because wires, transformers and substations don’t feel exciting.

But neither did telecom towers once upon a time.

Then the entire digital economy ended up sitting on top of them.

People are looking at AI apps.

I’m looking at the electrical backbone underneath them.

That’s where the real supercycle may be hiding ⚡️

4

15

84

8,288

Kalyan Jewellers story is honestly one of the best lessons in how markets can completely lose their mind while the actual business just keeps grinding.

From an all time high near 794 in Jan 2025, the stock crashed almost 40% in a few weeks, wiping out over 20000 crore in market cap. And the irony is the business itself was firing on all cylinders. Revenue crossing 25000 crore, aggressive expansion across India and Middle East, first store opening in the US.

So what actually went wrong. First, a real event. Govt cut customs duty on gold from 15% to 6% in July 2024. This compressed inventory values overnight and Kalyan booked a one time hit of around 120 to 130 crore. Genuine impact, but management was upfront that this was industry wide and fully recoverable by Q4.

Then came the real circus. January 2025 turned into a full blown rumor mill. IT raid rumors that never happened. Fake inventory claims that collapse the moment you look at 450 crore of debt repaid plus 170 crore in dividends, fake books just dont generate that kind of cash. A franchisee revolt story that got massively blown up, when in reality only 3 to 4 partners were terminated over contract breaches. Then the wildest one, bribing fund managers at Motilal Oswal, which MOAMC themselves publicly denied, sending the stock up 7% the very next day. And finally FIR rumors that turned out to be just a civil dispute with one ex franchisee.

On top of all this, promoter pledge panic. People saw the pledge percentage rise and assumed distress, but most of it was old collateral from the Warburg Pincus buyback back in FY20, and the fresh top up was simply because collateral value fell after the stock itself crashed. Classic chicken and egg.

Fast forward to FY26 and the numbers speak for themselves. Revenue past 35700 crore, PAT at 1350 crore, ROCE near 29%. The capital light FOCO engine is clearly working.

Whats next is what gets me excited. 150 new stores planned for FY27. Zero non GML debt targeted by H1 FY27. A brand new regional brand to take on unorganised local jewellers. Candere already PAT positive and scaling with 50 more stores. Plus non core real estate being sold off to clean the balance sheet even further.

The part most people will miss is the EBITDA vs PAT divergence. EBITDA margin looks weaker because FOCO partners take their share of revenue, but PAT margin expands because interest cost basically disappears once debt is gone. Thats the real story, not the headline EBITDA print.

If FY28 plays out as guided, revenue could be near 50000 crore and PAT crossing 2100 crore, and management has even hinted at reopening COCO stores once the balance sheet is fully clean, which could be the next leg of margin expansion.

Sometimes the best setups happen exactly when the noise is loudest and the fundamentals are quietly compounding underneath. Kalyan feels like a textbook case of that.

1

30

3,891

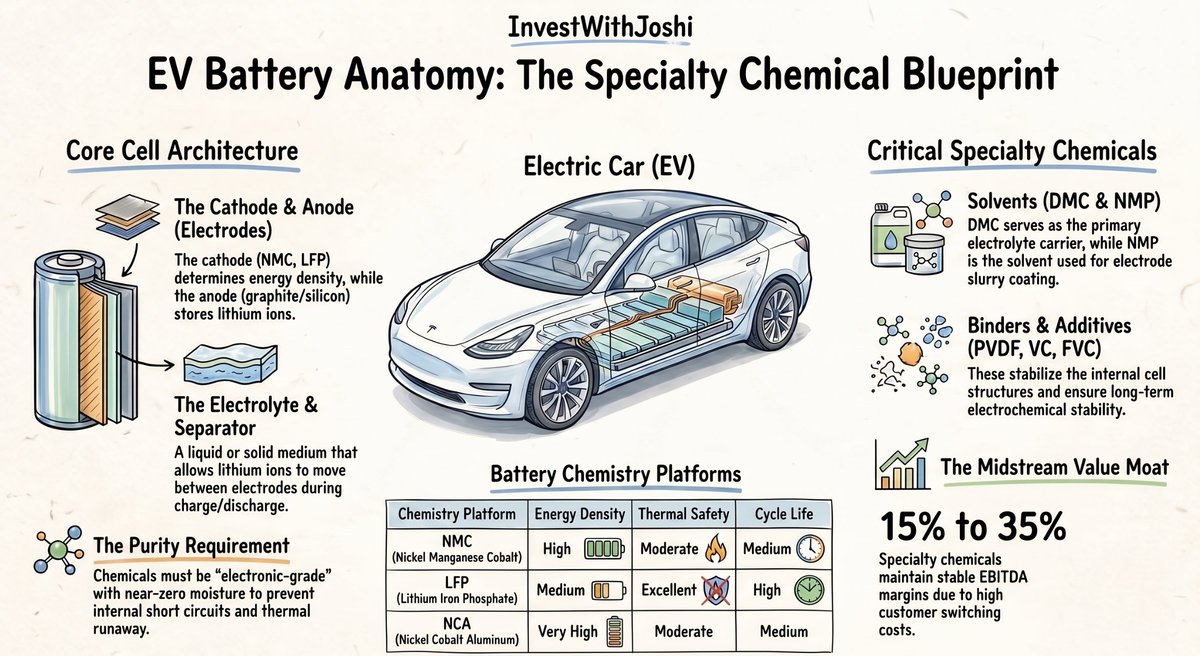

🇨🇳 China doesn't just make EV batteries.

It controls the chemicals that make EV batteries possible.

80% of global graphite supply.

~90% of anode and cathode material manufacturing.

Dominance across lithium, cobalt and graphite refining.

Which means every time India sells an EV, someone in China's chemical chain gets paid.

But that's starting to change... 👇

2

6

36

2,837

And BAL isn't alone.

Across India, a battery materials ecosystem is quietly taking shape:

🧪 Gujarat Fluorochemicals → LiPF6 & PVDF

🧪 Neogen → electrolytes & lithium salts

🧪 Acutaas → electrolyte additives

🧪 Tatva Chintan → specialty electrolyte salts

🧪 HEG → synthetic graphite anodes

Different products.

Same theme.

Replace imports.

Build domestic capability.

Capture more of the EV value chain.

1

2

371

The way I see it:

The EV story isn't just about who assembles the battery.

It's about who controls the chemistry inside it.

China understood that years ago.

India is only now starting to build that capability.

DMC.

NMP.

Electrolyte salts.

Graphite anodes.

These sound like boring chemical products.

But they may end up being some of the most important pieces of India's EV supply chain over the next decade.

And that's the part of the story most investors still aren't watching.

3

270

It feels good when management hears the feedback.

In Q4 Muthoot Microfin guided 12-15% AUM growth for FY 27.

In a recent TV Interview they revised the Guidance to 20%. I bet they will still beat this waiting for them to make it official in Investor PPT or Con call.

All the best sir

@Sadafsayeed

Jun 11

#OnETNOW | Crisil upgrades Muthoot Microfin rating

What factors led to this upgrade? "This was long overdue..." Sadaf Sayeed of @MuthootMicrofin explains, also revising their growth outlook

Full interview - youtube.com/watch?v=Tlh65Pr_…

@hershsayta @sajeetkm @Sadafsayeed #StockMarket

1

7

1,414

Crude cooling off 📉

Credit growth hitting a 2-year high 🚀

How can you be bearish now? 💸

1

1

10

1,434

Those predicting India's FY 27 EPS growth in single digit. Good luck 👍

1

2

232

6-month returns for the portfolio companies are looking fairly decent! 📈 Can anyone guess the first and last ones on this list? 👀👇

3

11

1,843

Portfolio returns will vary based on position sizing. The key is not only identifying the right companies, but also executing proper capital allocation.

3

367

Jun 12

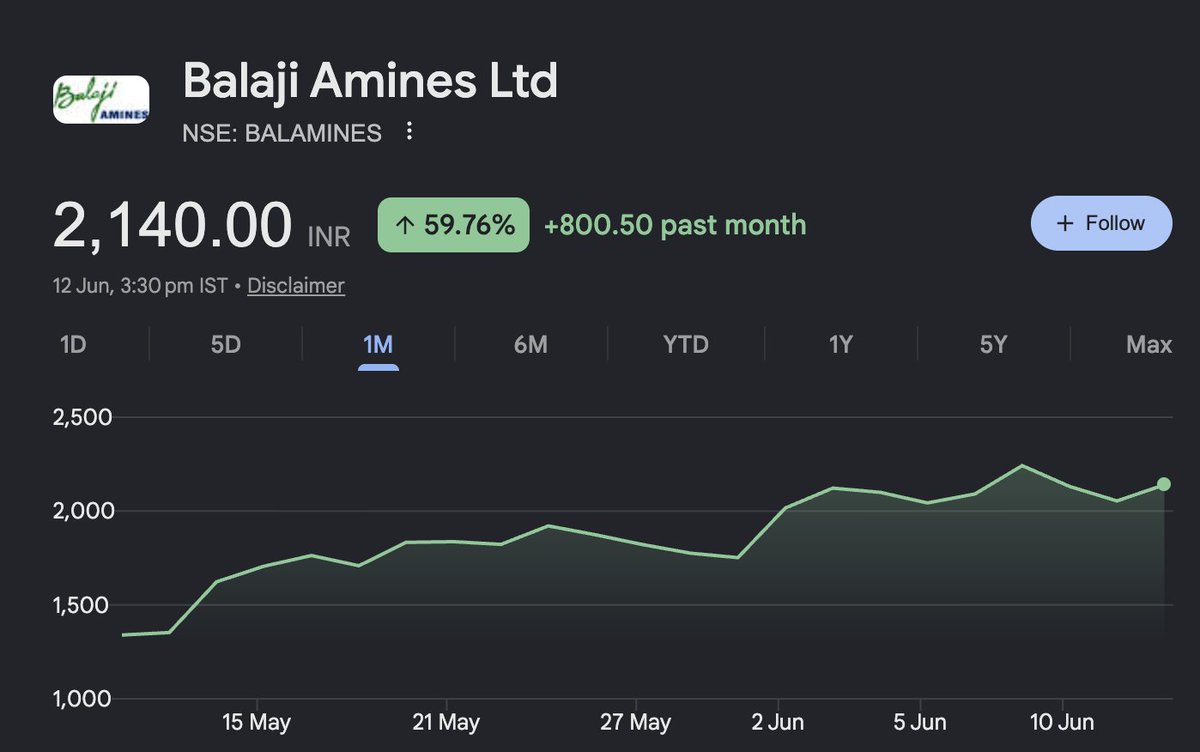

Balaji Amines sits right at the sweet spot of The Coal Gasification theme in India

With its 1L TPA Dimethyl Ether (DME) plant commissioned, it’s a sole commercial mover for 8% LPG blending.

Huge raw material optionality as cheap domestic methanol scales up via national gasification targets.

May 20

Big milestone for Balaji Amines 👏

The company has officially commissioned India’s first commercial-scale DME (Dimethyl Ether) plant with a capacity of 1,00,000 TPA.

Why does this matter?

DME can be blended with LPG and has the potential to reduce India’s dependence on imported fuel over time. A strong step towards cleaner energy alternatives and energy self-reliance 🇮🇳

Interesting to see an Indian chemical company not just talking about new-age chemicals but actually building capabilities ahead of the curve.

Also worth noting BAL is positioning itself aggressively in EV battery chemicals alongside this development.

Sometimes the biggest opportunities are created quietly, one plant at a time. 🚀

#BalajiAmines #DME #CleanEnergy #EV #ChemicalSector #IndiaGrowth

1

11

95

12,286

Jun 12

Good to see INR stabilizing after RBI's reforms.

The Rupee may have already bottomed. Here's my thesis 👇

Even as foreign investors were dumping Indian stocks through early 2026, they were quietly buying Indian government bonds at the same time.

FIIs were not leaving India because they had lost faith in the economy. They were rotating out of expensive equities into safer sovereign debt. This is exactly why the RBI reforms hit so fast.

The Rs 8795 crore that flowed in within days of the announcement was not new money suddenly discovering India. It was money already sitting at the gate, waiting for the friction to disappear.

What India Just Did

1⃣ Zero withholding tax on G-Sec interest and zero capital gains on government bonds, retroactive from April 2025. You already know this. But what most people are missing is everything below.

2⃣ Long dated bonds of 15, 30 and 40 year maturity are now fully open to foreign investors with no quota or cap. This sounds technical but the implications are massive. Global pension funds and sovereign wealth funds are sitting on trillions of dollars and they are legally required to hold very long dated assets to match their own long term liabilities. China spent 20 years building infrastructure to attract exactly this class of investor and still only has 2 to 3% foreign ownership in its bond market. India just opened the same door in one policy move.

3⃣ The RBI is absorbing the full currency hedging cost on fresh NRI dollar deposits until September 2026. Indian banks can now offer NRIs 5.5 to 6% on dollar deposits versus 4.2% on US Treasuries. That gap is close to a free lunch. The implication most people are not talking about is what happens when $40 to $45 billion of those NRI dollars convert into rupee deposits domestically. Indian banks have been running a dangerously wide credit-deposit gap, loan growth at 16% with deposits lagging badly. These inflows synthetically close that gap by an estimated Rs 1 lakh crore. Banks face less pressure to hike deposit rates. Borrowing costs across the whole economy quietly fall without the RBI cutting the repo rate even once.

4⃣ State owned companies are being incentivized to borrow dollars overseas at subsidized rates and convert them domestically. This pumps dollar supply directly into the Indian interbank market and supports the Rupee from the supply side.

5⃣ Indian exporters must now repatriate their foreign currency earnings within 9 months instead of 15. More dollars entering the system sooner. Simple but effective.

6⃣ NRIs and Overseas Citizens of India can now invest higher amounts in listed Indian stocks without needing to register with SEBI. This matters more than it looks. For decades the SEBI registration requirement acted as a genuine deterrent for diaspora capital. India has an estimated $2 trillion diaspora wealth pool sitting globally. Even a marginal increase in the fraction of that money flowing into domestic equities is a structural demand tailwind. This is slow burning but directionally it reduces India's dependence on institutional FII flows for equity market stability.

What the Projections Say

SBI Ecowrap estimates $55 to $65 billion in total inflows through FY27. If even a majority of this materializes India flips from a projected Balance of Payments deficit of $65 to $70 billion into a surplus of $5 to $10 billion. The Rupee stabilizes around 92 to 93 organically, without the RBI draining its reserves to defend it.

The Part Most People Are Still Missing

The government quietly granted the Bank for International Settlements, essentially the central bank of central banks, a special tax exempt status. This sounds like a footnote. It is not. Bloomberg's Global Aggregate Index, the most tracked fixed income benchmark in the world with trillions in passive capital benchmarked to it, requires Indian bonds to be settleable through Euroclear. Euroclear needs the BIS to be able to participate without tax friction. India just solved that. Analysts estimate Bloomberg inclusion brings in another $7 to $20 billion in purely passive, permanent capital. India already got into JP Morgan's index in June 2024 and FTSE Russell in September 2025. Bloomberg is the final gate and it just got unlocked.

The Risk Worth Taking Seriously

Full openness cuts both ways. India has dismantled its capital control shock absorbers. If the Fed pivots hawkish or global sentiment turns, the same passive funds flowing in can be algorithmically forced to sell Indian bonds at scale. That kind of outflow would have been structurally contained two years ago. It will not be now. India traded its defensive wall for a seat at the global table. The next 12 to 18 months will be the real verdict.

The Bottom Line

India stopped playing defense and started playing offense for global capital. The Rupee at 96.90 may well have been the peak pain. The early data is already saying so.

2

372

Jun 12

Lgta h ye tweet zyada logon tk pahuch gai 😬😬

Let's talk about Zaggle once again at ₹200 and ~₹2,700 Cr mcap and why i feel this is a great deal at this price.

Long post so hold your horses and like it if you find some value from this.

The stock has been absolutely hammered, so first let's understand what went wrong.

It all started with the QIP at ₹523.2/share during the peak of the bull market. Looking back, management was actually spot on in raising capital at those levels. They built a solid cash reserve and institutional ownership went up to ~23%.

Fast forward to today and FIIs have been exiting aggressively.

Not only did the holding percentage fall, but the number of FPIs holding Zaggle dropped from 74 to 52 in the March 2026 quarter. That means 22 foreign institutions completely exited.

DIIs also cut their stake from ~14% to ~7%.

Now the interesting part.

Who's still holding?

• Promoters increased stake from 44.13% to 44.29% through open market purchases

• Ashish Kacholia continues to hold 2.23%

• ValueQuest Scale Fund still holds 1.71%

So why isn't the selling getting absorbed?

From what I could gather, there are four major concerns.

1⃣Negative cash flows and low ROCE

2⃣Dice acquisition

3⃣AI fears

4⃣Management being everywhere on TV

Let's go one by one.

1. Cash Flows and ROCE -

Most people look at the numbers and conclude that Propel is the problem.

They're not entirely wrong.

Propel generates only ~₹45 Cr of net revenue while locking up a lot of working capital, which suppresses cash flows and ROCE.

The obvious question becomes:

Why not just shut it down?

Because that's where things get interesting.

Around 90% of spends on Propel happen through prepaid network cards. The economics from these card swipes are highly profitable, but accounting rules classify that revenue under Program Fees and not Propel revenue.

So if Zaggle shuts Propel, they don't magically become a cash rich business overnight.

They end up killing the engine that drives a huge chunk of Program Fees revenue.

Propel is basically the entry gate into the ecosystem.

A company comes for rewards management, gets deeply integrated into the platform and then Zaggle starts cross selling products like Zoyer and Save.

What most people miss is that cash isn't permanently stuck.

It's largely a timing issue.

Unlike businesses where receivables are trapped for years, Zaggle gets its money back in roughly 60 days.

And here's the beauty.

As growth slows down and the business matures, cash flow automatically improves.

At a 6% margin, the business can sustain roughly 45% annual growth without creating incremental cash stress.

At a 7% margin, that number moves closer to 55%.

So when Propel eventually matures, cash flow positivity should naturally follow.

Mere hisaab se this concern is a lot bigger on paper than it is in reality.

2. Dice Acquisition

Initially, the acquisition was supposed to happen at ₹123 Cr.

That looked expensive.

Eventually, they got it done at ₹68 Cr.

What did they actually buy?

The codebase.

The customers.

The engineering talent.

As someone working in tech, I can tell you one thing.

People massively underestimate the cost of building software from scratch.

The cost isn't just salaries.

It's failed iterations, delays, bugs, hiring mistakes and execution risk.

The market's bigger concern is the additional engineering workforce impacting margins.

My rough estimate is that the net employee addition is around 50 people.

Even at ₹20L average CTC, we're talking about ~₹10 Cr annual cost.

That's roughly a 40 to 50 bps drag on margins in worse case.

Nothing dramatic.

And if Dice revenues continue growing, even that drag could largely disappear.

Again, not thesis breaking.

3. AI Will Disrupt SaaS

We've been hearing this for years now.

Meanwhile software companies across the US continue to grow.

AI will change workflows.

AI will change how software is built.

But AI killing SaaS altogether doesn't seem to be playing out.

Not losing sleep over this one.

4. Management on TV

I know many investors dislike this.

Personally, I think this is a relatively new management team trying to defend the narrative around the company.

Would I worry if promoters were selling while giving interviews every week?

Absolutely.

But promoters are actually buying from the market.

So for now, I don't consider this a major red flag.

Now let's look at the numbers.

FY26:

Revenue ₹1,908 Cr

EBITDA ₹185 Cr

PAT ₹139 Cr

Management is guiding for roughly 40% revenue growth.

Since they haven't missed revenue guidance post listing, let's assume they deliver.

FY27 could look something like:

Revenue ~₹2,700 Cr

Even if margins contract by ~30 bps,

EBITDA margin ~9.4%

EBITDA ~₹253 Cr

PAT ~₹184 Cr

At the current market cap, FY27 PE comes to roughly 14x.

PEG comes to around 0.4.

That's honestly quite attractive.

And once Dice integration is behind them, operating leverage should start kicking in from FY28 onwards 🚀

Can the market disagree?

Of course.

Can the stock remain cheap for longer?

Absolutely.

But at ₹200, the risk reward looks significantly better than it did at ₹523.

One last thing.

Whenever a stock falls, people immediately say FIIs and DIIs sold, kuch toh soch samajh ke hi becha hoga.

Maybe.

But if they were always right, would they have participated in the ₹523 QIP in the first place?

That answer, I'll leave to you.

1

9

2,200

Jun 12

Kl tak jo log 100% cash pe baithe the aaj achanak se wo 100% invested ho jaenge 🫡

17

968

Jun 12

We went from sell everything to sell your house and bet everything on equities in less than 24 hrs crazy times man 😂

2

21

1,661

Vaibhav Joshi retweeted

Jun 11

Trump: I’m attacking Iran. I’m not attacking Iran. I’m attacking Iran. I’m not attacking Iran.

Markets:

1,352

13,124

74,023

3,985,908

Jun 11

I made most of my returns by playing contra bets. I bought great companies that the market was bashing for useless reasons that were not fundamentally degrading the business.

I was lucky enough to catch Meta at a ~$129 average. People were beating the hell out of Meta because of the Metaverse cash burn. Other FAANG companies were also quite cheap back then.

Then I shifted to Chinese stocks through ADRs listed in the US market. Alibaba worked, but JD.com didn't.

Indian markets were also full of opportunities pre-2024.

PSU banks were in that bucket when they were extremely cheap and people were just busy with HDFC and other private sector banks.

Avalon Tech around ₹450 was another one. Everyone was busy praising Kaynes and totally beating down Avalon without looking at the forward trajectory.

Yatharth Hospitals was a great buy at ₹430–450 when people were bashing it because the Income Tax Department was holding their IPO money, while the business itself was doing absolutely great.

Satin, Raymond, and Paramount turned out to be great contra plays.

SG Finserve was another one where people were unhappy just because management gave conservative guidance. Bro, if you only invest by looking at guidance, I feel sorry for you.

There are countless examples.

Moral of the story: there are n number of ways to make money, but if you buy at dirt-cheap valuations where the business model and growth remain intact, or are just temporarily hampered, there's a very good chance you'll make great returns.

Focus on starting valuations, growth, and the possibility of PE expansion. That's where you'll potentially find multibaggers in your journey.

Disc: All the stocks mentioned above are stocks I have held or may still be holding currently. This is not buy or sell advice in any way. Use this for educational purposes only. I am extremely biased, so never make investment decisions based solely on my views.

3

1

16

2,137