Founder & CEO | CIO @gullbridge Innovation-obsessed. Improve lives through transformative financial and infrastructure solutions. | Not Financial Advice

Joined April 2021

- Tweets 3,167

- Following 1,226

- Followers 621

- Likes 4,569

56 Photos and videos

Jun 4

Concentration creates opportunity.

Diversification creates endurance.

The real challenge is knowing when to use each.

8

Joseph Mozube retweeted

May 11

Michael Burry says that we're witnessing history in the stock market, and not in a good way.

272

241

3,576

342,198

May 8

Passive flows and AI capex cycles are reinforcing mega-cap dominance in a way the dot-com era didn’t fully have.

BREAKING: Michael Burry says the market today feels like 'the last months of the 1999-2000 bubble'

52

May 8

Rising asset prices themselves are easing financial conditions, which then fuels more inflows into the same winners. That loop can extend trends far beyond what fundamentals alone justify.

We truly are witnessing history right now.

It's clear that the period we are in now will be referenced for decades to come.

The S&P 500 has added $10 trillion in 29 days, semiconductor, AI stocks are surging 100% in weeks, and the Trump Administration is up 550% on Intel.

When we began emphasizing the need to own assets to win in this market over 12 months ago, this is exactly what we meant.

While inflation is back and the labor market has weakened, it simply does not matter right now.

In fact, the return of inflation has only intensified the scramble for yield and hard assets that can preserve purchasing power.

Look at the data: just 5 stocks have accounted for ~50% of the S&P 500’s total gains since April 1st.

These same tech giants driving the market higher are gaining even more momentum amid rate cuts, deregulation, and historic inflows into equities.

Asset owners are experiencing one of the greatest wealth expansions in modern history while everyone else is being left behind.

Our 12 month thesis has materialized.

42

Apr 8

People love to judge trades by how they end up. Cute. As if the outcome isn’t just the sloppy aftermath of the process. Before $BRAI was even a position, it was a diagnosis. A freshly listed name in full-blown price discovery, no real structure underneath it, just pure chaos wearing a suit.

In those setups, price doesn’t walk, it sprints like it’s late for therapy. It overshoots, it gets delusional, it prices in fantasies that balanced money would never touch. So you stop pretending you can call direction. That’s for amateurs with Bloomberg terminals and hope in their hearts. You start measuring stability instead. How long before this thing starts smelling like bullshit?

The moment the market stops behaving like a market and starts twitching, the odds of a hard reversion go through the roof.

The trade? Just the polite way of saying: “I see what this is.”

Long term, you don’t get consistent by hunting more setups. You get consistent by being less wrong about the conditions. Everything else is just noise and ego.

Apr 8

Our CIO breaks down the $BRAI trade, from price expansion to structural exhaustion. Markets don't fail randomly, they become unstable first. Understanding that shift is the edge.

Read the full note; rb.gy/of743r

1

92

Apr 8

The opportunity wasn’t in some naive little prediction about direction. That’s for the retail crowd with their charts and hopium.

No. It was in spotting the instability before it became obvious.

When price pushed beyond the structural support, that’s when you knew the game had shifted. Continuation no longer depended on real strength. It was suddenly about weaker participants piling in, hoping they weren’t the last ones left holding.

At that point, momentum is irrelevant. It’s all liquidity. Pure liquidity.

Read more; rb.gy/vb8106

67

Feb 27

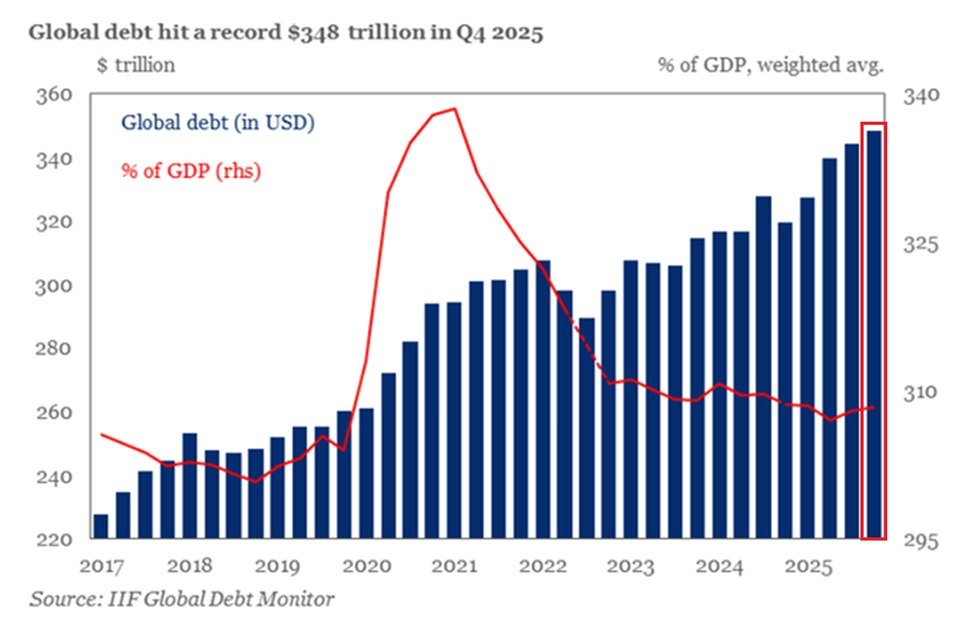

The absolute number is massive, but markets care more about interest burden relative to GDP. Debt becomes destabilizing when growth slows and refinancing costs rise simultaneously.

BREAKING: Global debt surged $29 trillion in 2025, to a record $348 trillion.

This marks the biggest annual increase since the 2020 pandemic.

The surge was particularly driven by governments, which added $10 trillion, with the US, China, and the Euro Area responsible for roughly three-quarters of the increase.

This brings the global government debt to $107 trillion, an all-time high.

Furthermore, non-financial corporate debt rose to a record $101 trillion, with AI-related investment a major driver of corporate borrowing.

Meanwhile, the total debt of emerging markets rose to a record $117 trillion, with a Debt-to-GDP ratio of 235%, also an all-time high.

The global debt crisis is reaching unprecedented levels.

51

Feb 27

If this thesis plays out, watch T-bill yields, reverse repo balances, and dollar liquidity metrics, those would reflect stablecoin-driven Treasury demand before broader bond markets react.

Feb 27

Standard Chartered forecasts the stablecoin market could expand from $304 billion today to $2 trillion by 2028, increasing demand for U.S. Treasury bills.

50

Joseph Mozube retweeted

Feb 24

If the economy is growing but jobs are not, it usually means companies are increasing output without hiring more people.

7

1

2

5,048

Feb 21

Periods of structural change usually feel hardest in real time. Volatility rises, correlations shift, and traditional playbooks stop working, but those environments historically create new leadership rather than eliminate opportunity.

Feb 21

I truly believe we are entering one of the hardest periods of time to invest.

There is change and disruption happening across every industry and every financial market.

And the rate of change is accelerating.

There are few safe places to hide your capital, which increases the amount of decision an investor has to make.

More decisions means higher likelihood of making mistakes.

It will be interesting to see how this all plays out.

Best of luck to all of you.

30

Feb 20

Alternative trade frameworks could shift revenue timing without reducing fiscal pressure, which matters more for long-duration bonds than equities.

Feb 20

Goldman: "This won’t be the end of tariffs… the administration will almost certainly roll out alternative legal frameworks. Net result is probably slightly fewer tariffs, materially more trade uncertainty, and some incremental deficit concerns. Net-net, that’s mildly supportive for equities and mildly negative for bonds… but largely priced for both."

41

Feb 20

Purchasing power erosion

Feb 20

47% of Americans surveryed said they had withdrawn money from retirement accounts due to inflation, per Allianz.

1

28

Feb 18

You need real guts, steel-plated, ice-cold guts, to look the numbers dead in the eye, stare at the valuation like it’s the only thing that matters, and completely ignore the crowd losing their minds around you. Everyone’s panicking, screaming, running for the exits? Doesn’t move the decimal. Doesn’t change the math. Toughen up. The herd’s noise is irrelevant.

30

Feb 18

Everyone wants upside until volatility shows up, then suddenly nobody wants inventory risk.

Feb 18

Goldman: "Following last week's moves, the market continued to see large intraday swings given liquidity is not set up well here. Rallies encounter fresh gamma supply, while dealers move shorter gamma on further sell-offs. Tension remains with the panic index hovering ~8.6."

1

36

Feb 18

People aren’t frustrated because work exists, they’re frustrated because productivity keeps rising while real security doesn’t. That gap is where trust in institutions starts leaking.

Feb 17

They convinced you

working until 65 is normal,

mothers don’t need long maternity leave,

45 hours a week isn’t “working hard,”

good citizens pay 50% tax on their income.

It’s okay to tax food, clothes, cars, houses everything.

While you struggle to pay rent and put food on the table for your family, elites go to islands to do their pedo stuff and won’t get arrested even if there is video evidence.

22

Feb 18

If it runs, it won’t be because people suddenly discovered Amazon exists, it’ll be margins, AI leverage, and capital discipline. Narrative follows numbers, not the other way around.

Feb 17

Prediction:

$AMZN is going to go on a generational run from 2026 - 2030 as the market realizes it’s one of the most defensible businesses in the world.

Price right now $200.

Check back in 4 years.

33

Feb 18

Automation helps margins, it rarely rewrites commodity fundamentals overnight. Otherwise oil, copper, and lithium would’ve already gone to zero years ago.

31

Feb 17

Credit default swaps tied to major technology firms barely existed a year ago. Net notional exposure now approaches ten billion dollars. That type of hedging demand does not materialize from thin air. Someone somewhere started asking uncomfortable questions before the crowd did.

Oracle absorbing roughly six billion dollars of CDS protection should make anyone pause. Not Nvidia. Not Microsoft. Oracle. Ask yourself why. Balance sheet composition explains part of the picture. Aggressive debt-funded infrastructure expansion creates a timing mismatch between capital expenditure and monetization. Cloud capacity, AI compute buildout, data center leasing, grid commitments, none generate cash on day one. Debt service does.

Markets rarely punish ambition immediately. Liquidity delays consequences. Credit markets remove that delay brutally. Equity investors chase narrative; bond desks price survival.

Everyone screams about GPUs, model breakthroughs, trillion-parameter fantasies. Meanwhile electricity demand from hyperscale data centers keeps climbing toward levels comparable to mid-sized cities. Northern Virginia data center corridor alone already consumes multiple gigawatts. ERCOT projections show Texas data center demand potentially tripling by decade end. Yet somehow energy cost rarely trends on financial media feeds. Curious.

Utility regulators across several U.S. regions quietly flagged grid stress from AI-driven load growth. Not conspiracy. Public filings. Regulatory hearings. Rate case adjustments. Energy cost flows straight into operating margin whether analysts want to discuss that or not.

Feb 17

Tonight begins a conversation most investors avoided for months. AI excitement dominates headlines, yet credit markets quietly price something very different. That divergence rarely stays quiet forever.

Here's my insight; rb.gy/oedcir

1

29