Founder and CEO of January.com

Joined March 2014

- Tweets 5,208

- Following 325

- Followers 1,326

- Likes 4,738

1,680 Photos and videos

"The smile on her face lights up a room," Doshia says of her daughter. And then, one drug screen later, Selah was taken.

Doshia's not alone: tens of thousands of mothers are coming under scrutiny because of marijuana use.

My latest @RollingStone

rollingstone.com/culture/cul…

4

27

47

20,672

24 Jul 2024

My twin @emcahan bailed on Thanksgiving, claiming a hospital shift

Instead he went to the Ukraine/Russia frontlines to report on superbug chaos. @RollingStone published his story, calling superbugs the "climate change of medicine."

My family freaked out

rollingstone.com/politics/po…

1

2

573

13 Sep 2017

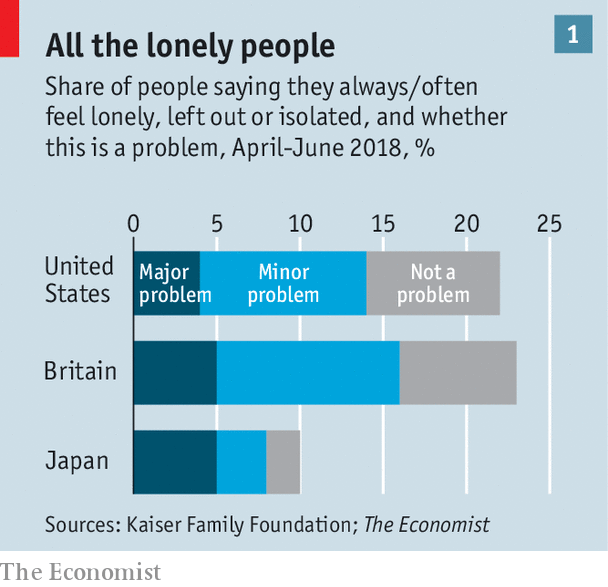

A study found that "having greater social connections is associated with a 50% reduced risk of premature death." wsj.com/articles/the-governm…

1

1

25 Mar 2019

Research on loneliness

Estimated to shorten a person's life by 15 years

Associated with higher cancer mortality risk and higher blood pressure

May accelerate cognitive & functional decline

cc @emcahan ht @abnormalreturns

blogs.scientificamerican.com… economist.com/international/…

2

2

2 Jun 2024

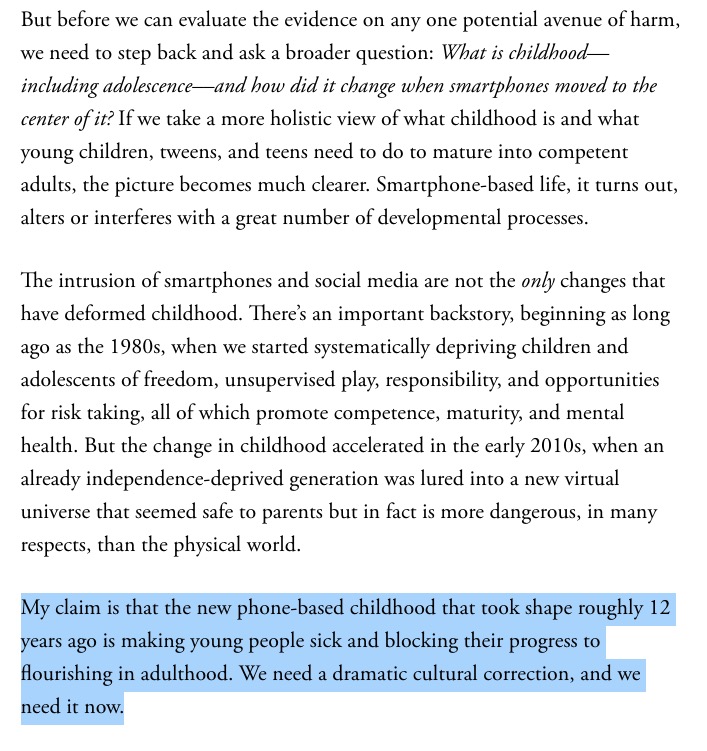

@JonHaidt argues that smartphone-based life "alters or interferes with a great number of development processes…making young people sick and blocking their progress to flourishing in adulthood."

One study illustrated that young people spent 2 hours a day with friends before 2010 & just 67 minutes by 2019.

theatlantic.com/technology/a…

1

371

Jake Cahan retweeted

9 Mar 2024

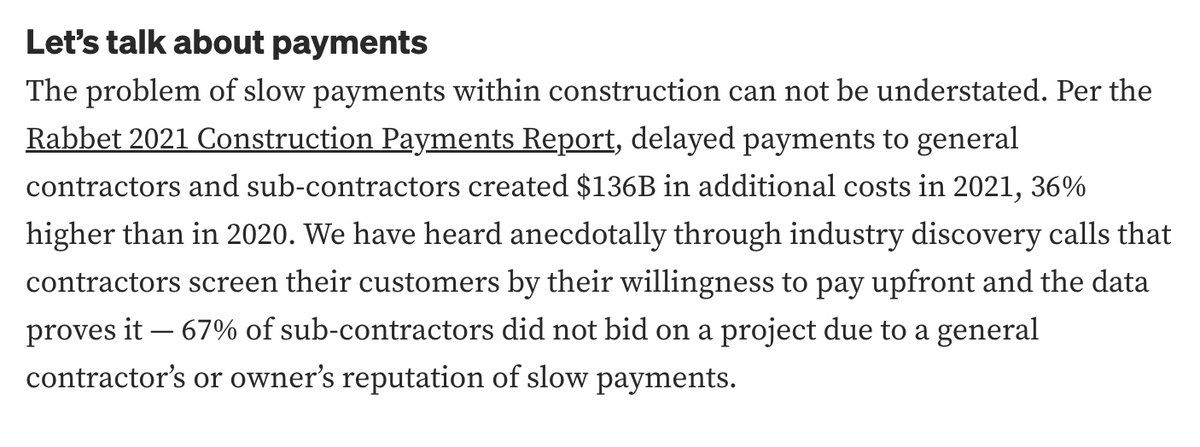

In Lux’s recent letter to LPs (last part pg 3) we note rising CREDIT RISKS (amid consensus of ‘soft landing”)

friend @JakeCahan of January.com recovery rates across their agency networks 📉 20-40% YoY

Payment failures 📈30% YoY

Risk of credit DEFAULTS rising📈

21 Feb 2024

2/

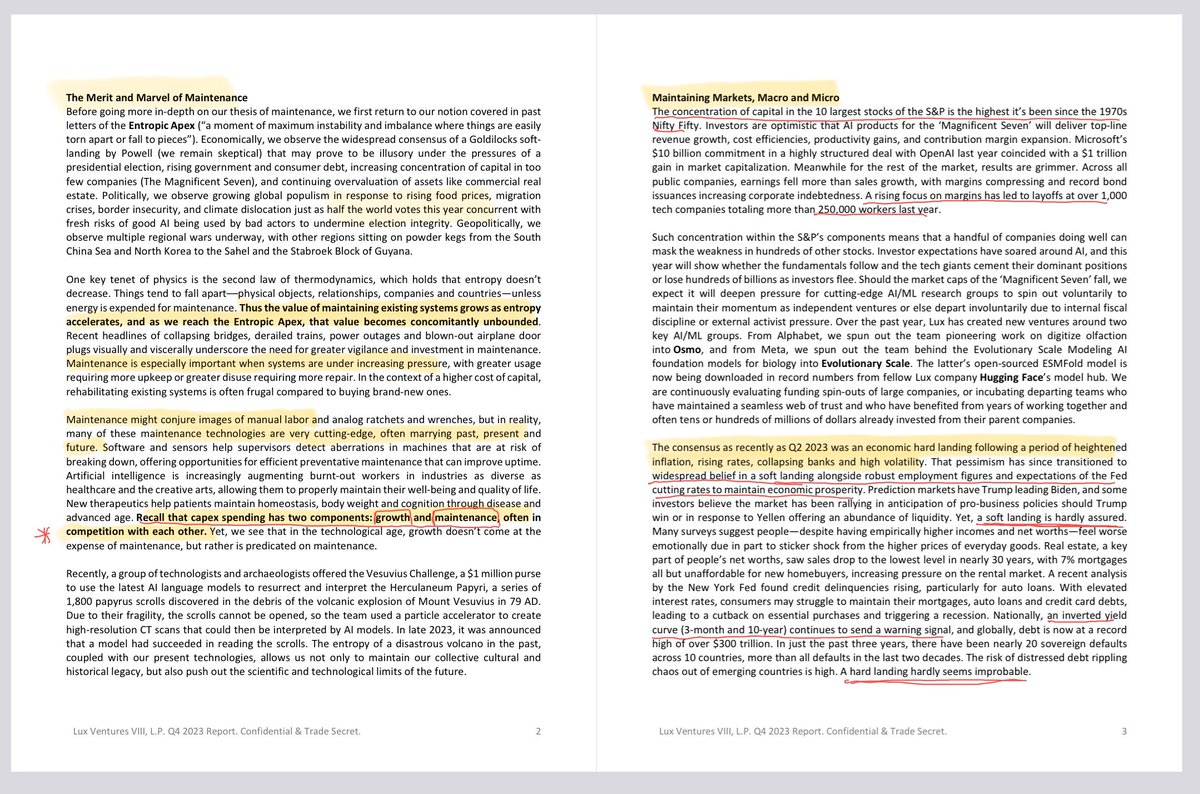

•the merit marvel of MAINTENANCE

• recall capex has 2 parts: growth MAINTENANCE, often in competition with each other…

•…meanwhile contrary to expectations––a HARD LANDING hardly seems improbable

consider:

-the concentration of capital in the 10 largest stocks of the S&P is the highest it’s been since the 1970s Nifty Fifty.

-across all public companies, earnings fell more than sales growth, with margins compressing and record bond issuances increasing corporate indebtedness. A rising focus on margins has led to layoffs at over 1,000 tech companies totaling more than 250,000 workers last year

-such concentration within the S&P’s components means that a handful of companies doing well can mask the weakness in hundreds of other stocks. Investor expectations have soared around AI, and this year will show whether the fundamentals follow and the tech giants cement their dominant positions or lose hundreds of billions as investors flee. Should the market caps of the ‘Magnificent Seven’ fall, we expect it will deepen pressure for cutting-edge AI/ML research groups to spin out voluntarily to maintain their momentum as independent ventures or else depart involuntarily due to internal fiscal discipline or external activist pressure.

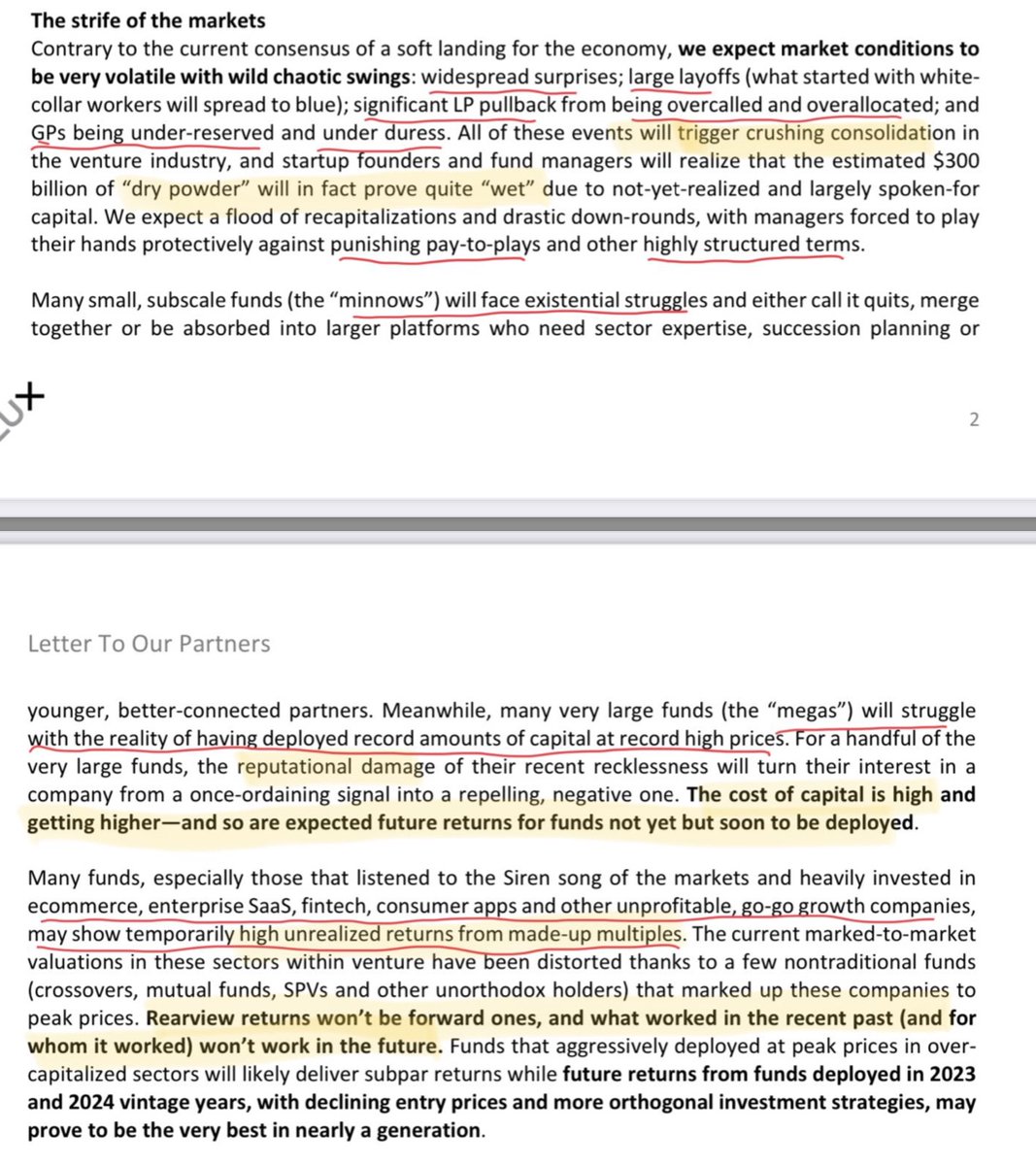

-The consensus as recently as Q2 2023 was an economic hard landing following a period of heightened inflation, rising rates, collapsing banks and high volatility. That pessimism has since transitioned to widespread belief in a soft landing alongside robust employment figures and expectations of the Fed cutting rates to maintain economic prosperity. Prediction markets have Trump leading Biden, and some investors believe the market has been rallying in anticipation of pro-business policies should Trump win or in response to Yellen offering an abundance of liquidity. Yet, a soft landing is hardly assured. Many surveys suggest people—despite having empirically higher incomes and net worths—feel worse emotionally due in part to sticker shock from the higher prices of everyday goods. Real estate, a key part of people’s net worths, saw sales drop to the lowest level in nearly 30 years, with 7% mortgages all but unaffordable for new homebuyers, increasing pressure on the rental market. A recent analysis by the New York Fed found credit delinquencies rising, particularly for auto loans. With elevated interest rates, consumers may struggle to maintain their mortgages, auto loans and credit card debts, leading to a cutback on essential purchases and triggering a recession. Nationally, an inverted yield curve (3-month and 10-year) continues to send a warning signal, and globally, debt is now at a record high of over $300 trillion. In just the past three years, there have been nearly 20 sovereign defaults across 10 countries, more than all defaults in the last two decades. The risk of distressed debt rippling chaos out of emerging countries is high.

A hard landing hardly seems improbable.

3

5

21

15,379

23 May 2022

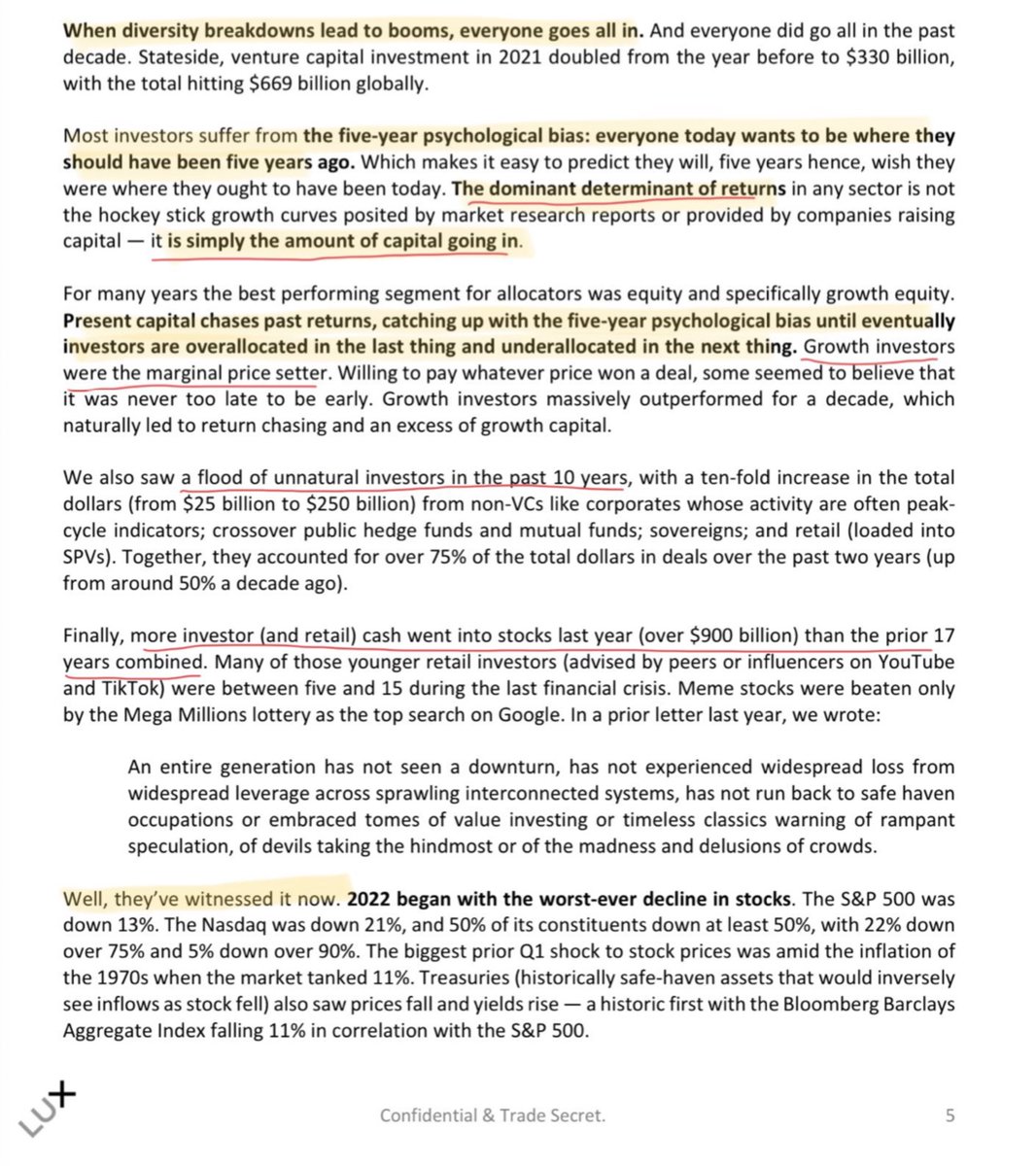

"Most investors suffer from the 5-year psychological bias: everyone today wants to be where they should've been 5 years ago…The dominant determinant of returns in any sector isn't the hockey stick growth curves…it's simply the amount of capital going in" -@wolfejosh's Q1 letter

2

14

102

19 Aug 2023

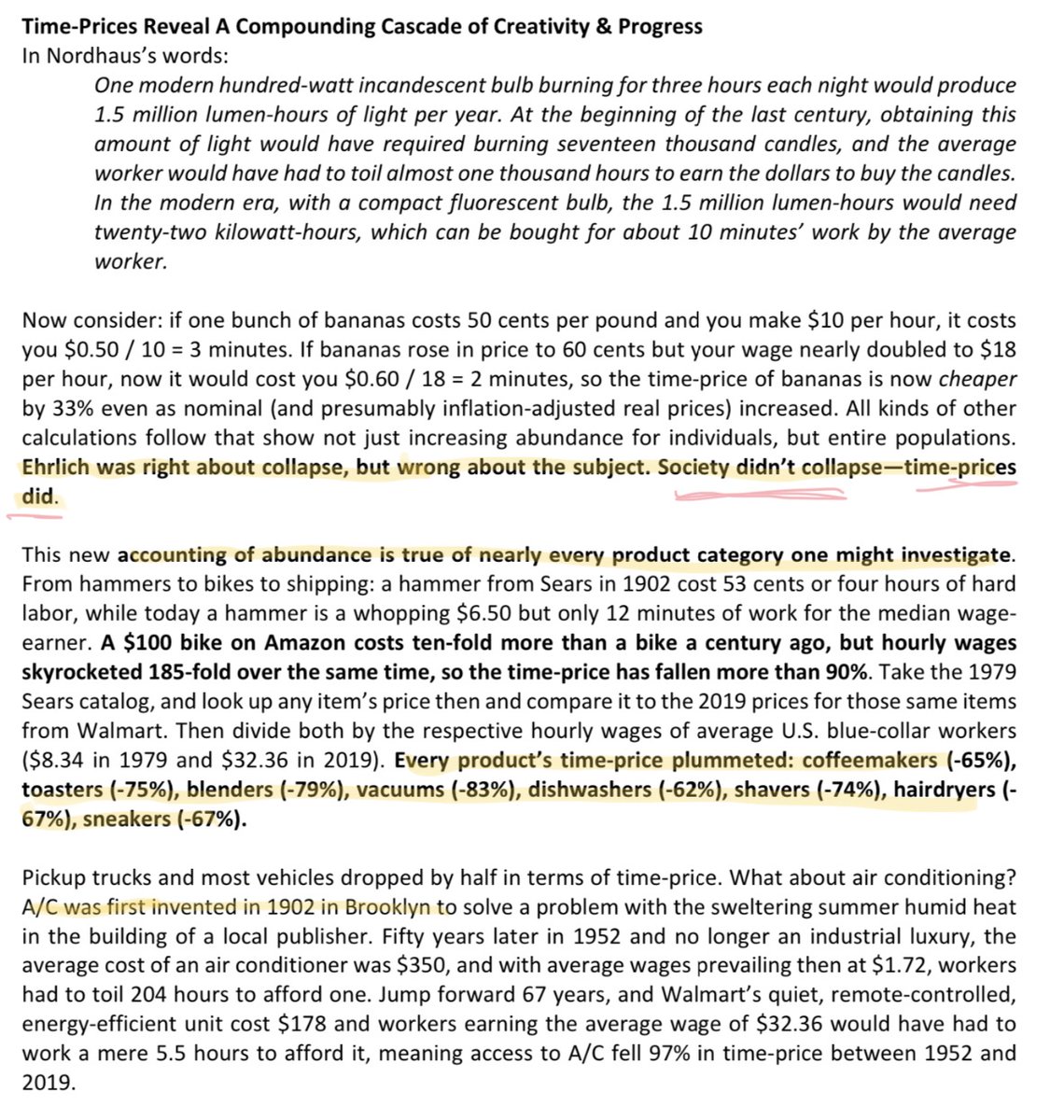

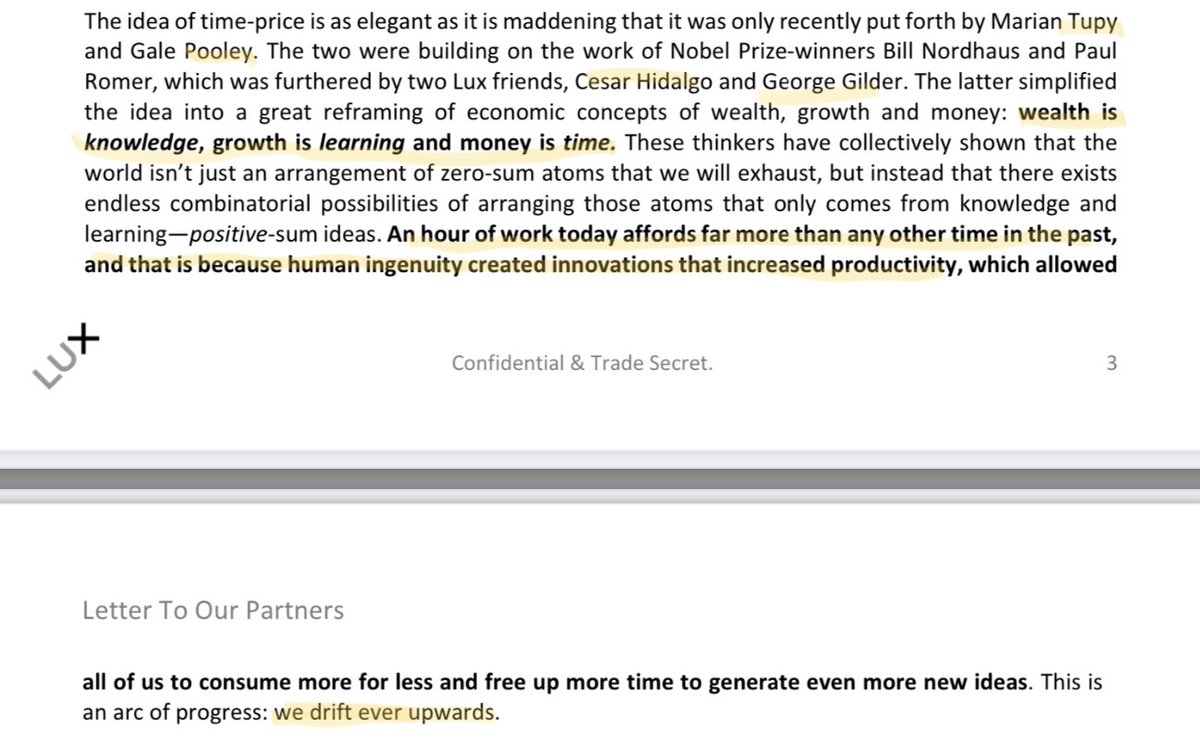

.@wolfejosh writes in his Q2 2023 letter about societal progress, accounting for abundance (via a new metric, time-price), perspectives on what the US can do in light of the CCP, and more! drive.google.com/file/d/14_o…

1

2

7

7,668

9 Mar 2024

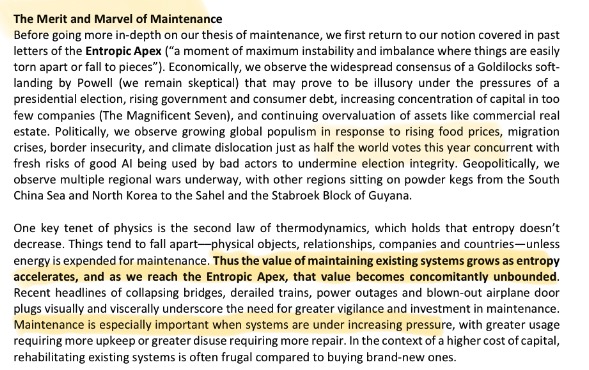

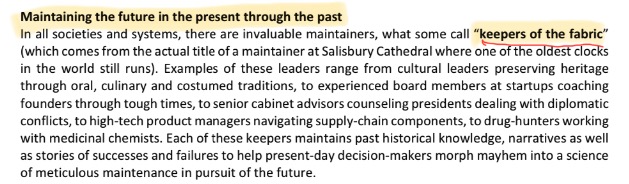

.@wolfejosh writes about the necessity of maintenance today to achieve future breakthroughs in his Q4 2023 letter: "Thus the value of maintaining existing systems grows as entropy accelerates…Maintenance is especially important when systems are under increasing pressure, with greater usage requiring more upkeep or greater disuse requiring more repair." drive.google.com/file/d/11jF…

1

5

3,158

4 Feb 2024

This is the best article I've ever read on the pharma industry. It's a wonderfully accessible read on why drugs used to be discovered at a much faster rate, the different stages of drug development, what's broken today, areas of investment to improve biomedical productivity, and more.

23 Dec 2023

New big blog post covering the history of the pharma industry, why drugs cost orders of magnitude more to develop now than in the 50s, and some suggestions on what we can do to improve R&D efficiency. Written for a general audience.

atelfo.github.io/2023/12/23/…

2

692

6 Dec 2023

I’m so excited to announce our Series B!!

Thanks @ryanlawler for breaking the news: axios.com/pro/fintech-deals/…

A huge thank you to @beyroutey from @iaventures for leading the round and the rest of our investors for supporting us (@rohanm_ from @BrewerLaneVC , @keithhamlin from @thirdprimevc , @ckwitt3 from @upper__90, and others!) our team for building such a meaningful organization, our clients for working with us to set a new standard, and the consumers we engage with for teaching us and helping us become better.

But, there’s so much left to build.

We’re addressing an increasingly important problem in today’s economy. We’re hiring for many roles now, including a lot of engineers. boards.greenhouse.io/january…

If you know anyone, please reach out!

1

4

28

2,306

Jake Cahan retweeted

27 Oct 2023

26 ways Michael Jordan was described in his 700 page biography:

1. His competence was exceeded only by his confidence.

2.Jordan believed mostly in himself. In Mike he trusted. All others were open to question.

3.Michael puts every ounce of talent to use. Jordan goes all out. He outthinks you.

4.Animation and hyper-competitiveness were simply Jordan's normal state.

5. He had the motivation to be the best at it.

6.He tested himself.

7.He discovered the secret quite early in his competitive life: the more pressure he heaped on himself, the greater his ability to rise to the occasion.

8.He came to practice every day like it was Game 7 of the NBA Finals. That's what set the tone for our team.

9. It took the fewest of words to set him off. He would seize on apparently meaningless cracks or gestures and plunge them deep in his heart, until they glowed radioactively, the nuclear fuel rods of his great fire.

10.Young Michael had begun taking note of the pro game on TV. He was finding rare and special instructors through television.

11. At each step along his path others would express amazement at how hard he competed.

12. At every level he was driven as if he were pursuing something that others couldn't see.

13.He had a clear notion of what he wanted and he wasn't reluctant about expressing it publicly: “My goal is to be a pro athlete.”

14.The coach would recall that Jordan kept sneaking back into succeeding groups for more work that evening.

15.Jordan could sense immediately that he had something the others didn't.

16.They all began to grasp that Jordan's belief in himself reflected a level of intensity no one had contemplated before.

17.He was so committed he wouldn't allow himself to become sidetracked. He knew he wanted to be the best. He was very sure of himself, sure of what he wanted to do, and nothing was going to stop him

18.He was upset with teammates who lacked the necessary competitive drive.

19.He wanted to work on his shooting. And after practice he'd make you help him. He'd keep working on his shooting. He didn't care how long he was out there. Michael loved to play the game.

20. Jordan determined that he wanted to be recognized for having the “complete game."

21.Jordan presented a singleness of purpose that was hard to dent.

22.That's what made him a badass. He wasn't just a talent. It was the understanding of it all, the work ethic, the game itself, the strategy involved. He got it all. He understood all of it.

23. You got to understand what fuels that guy, what makes him great. He took the pain of that loss and held on to it. It's a part of what made him.

24. To his coaches his capacity to be coached was his single most impressive attribute. I had never seen a player listen so closely to what the coaches said and then go and do it.

25. It was quite possible that no one ever did anything better than Michael Jordan played basketball late in his career.

26. No one had seen him coming.

18

209

994

215,110

Jake Cahan retweeted

24 Oct 2023

"if we don’t continually outgrow ourselves, if we don’t wince a little at our former ideas, ideals, and beliefs, we ossify and perish."

~@brainpicker

17 Life-Learnings from 17 Years of The Marginalian themarginalian.org/2023/10/2… via @brainpicker

4

19

126

23,801

10 Jul 2023

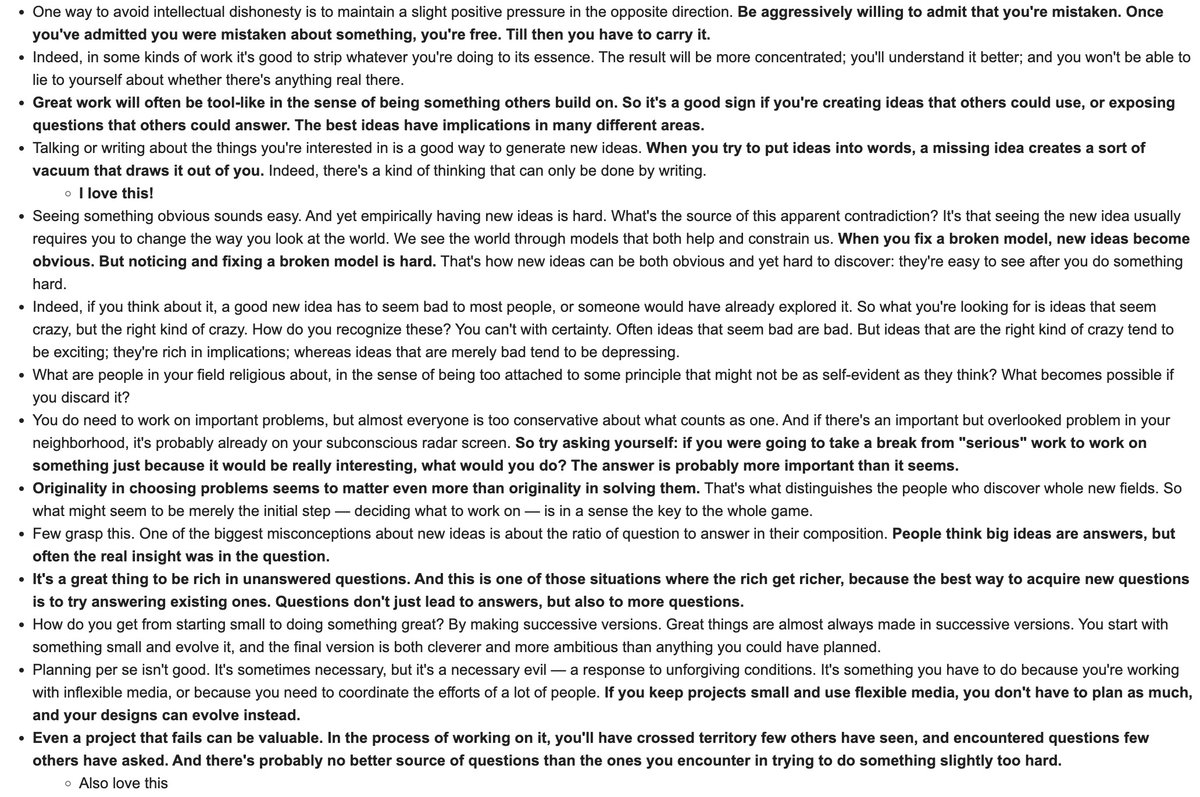

Some -- actually many -- of my favorite lines from @paulg's recent essay on great work paulgraham.com/greatwork.htm…

6

553

8 Oct 2017

One study found that real pension costs rose 69% across 219 cities between 2005 and 2014 economist.com/news/finance-a…

1

1

3

15 Jul 2018

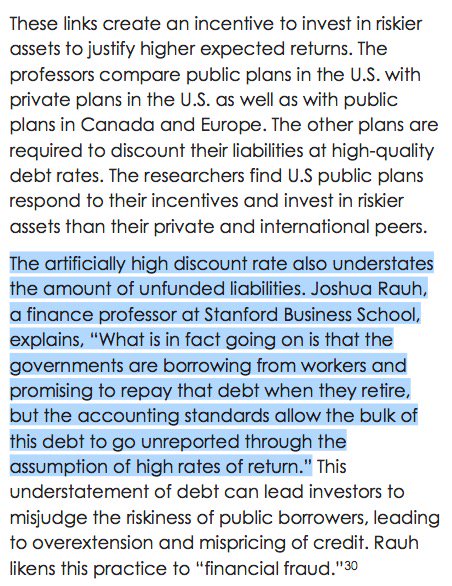

.@mjmauboussin describes how US accounting rules around setting discount rates based on expected returns incentivizes pension funds to invest in riskier assets & the consequences, which are likened to "financial fraud." bluemountaincapital.com/wp-c…

1

2

17 Jun 2023

Stanley Druckenmiller: "To actually pay for the entitlements we promised in the future, you’d have to raise all taxes 40% today forever or cut all spending 36% today forever." youtu.be/NERglanBMIk?t=450

This concern echoes what he's shared 7 years ago: x.com/JakeCahan/status/71903…

10 Apr 2016

"If you present valued what we have promised to seniors in Medicare & Social Security & Medicaid, the federal debt..would be $205 trillion"

2

3

15

2,827

14 Jun 2023

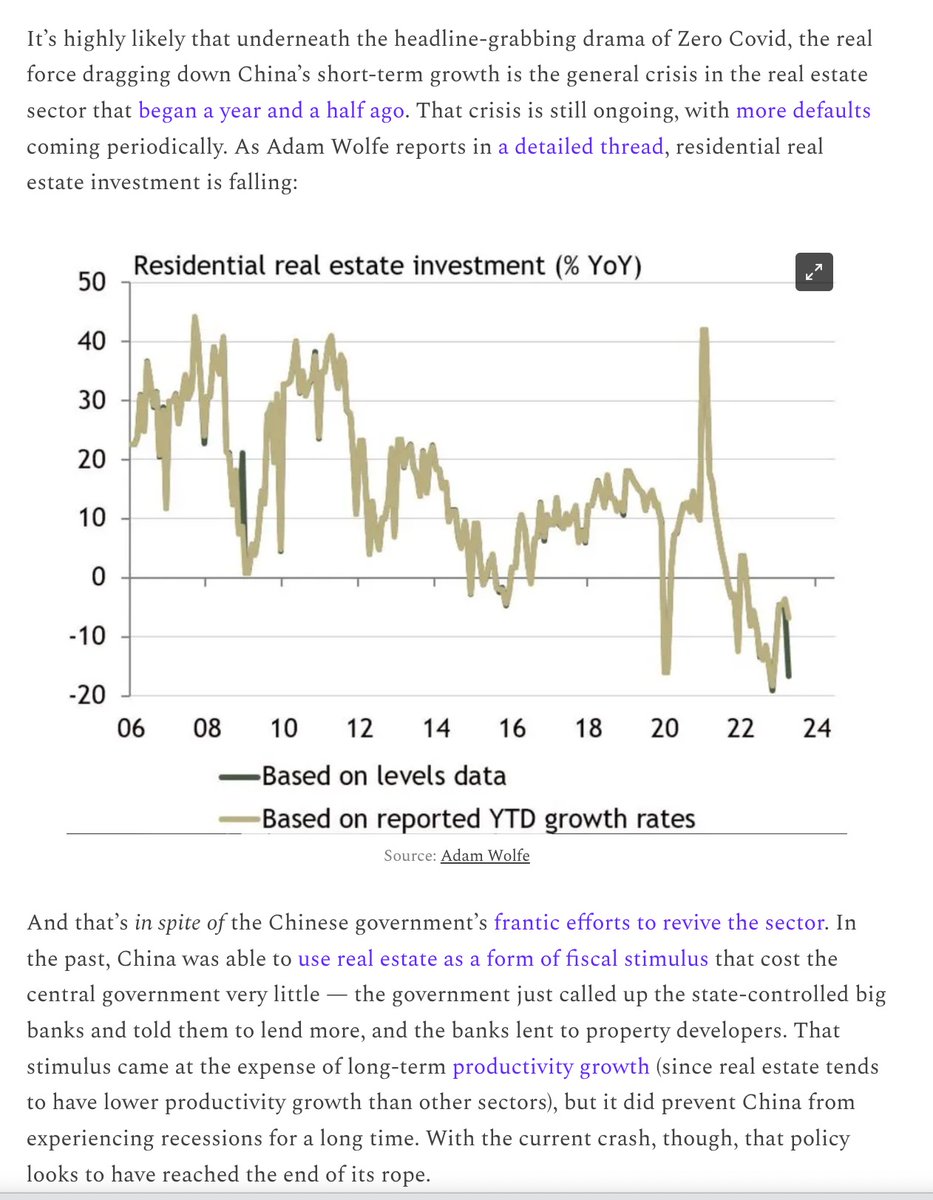

.@Noahpinion's fascinating take on China's material real estate problems: noahpinion.blog/p/real-estat…

"China was building a bunch of real estate that nobody was really using as real estate. Instead, they were increasingly using it as an investment vehicle."

ht @WallStCynic

1

3

18

21,393

28 May 2023

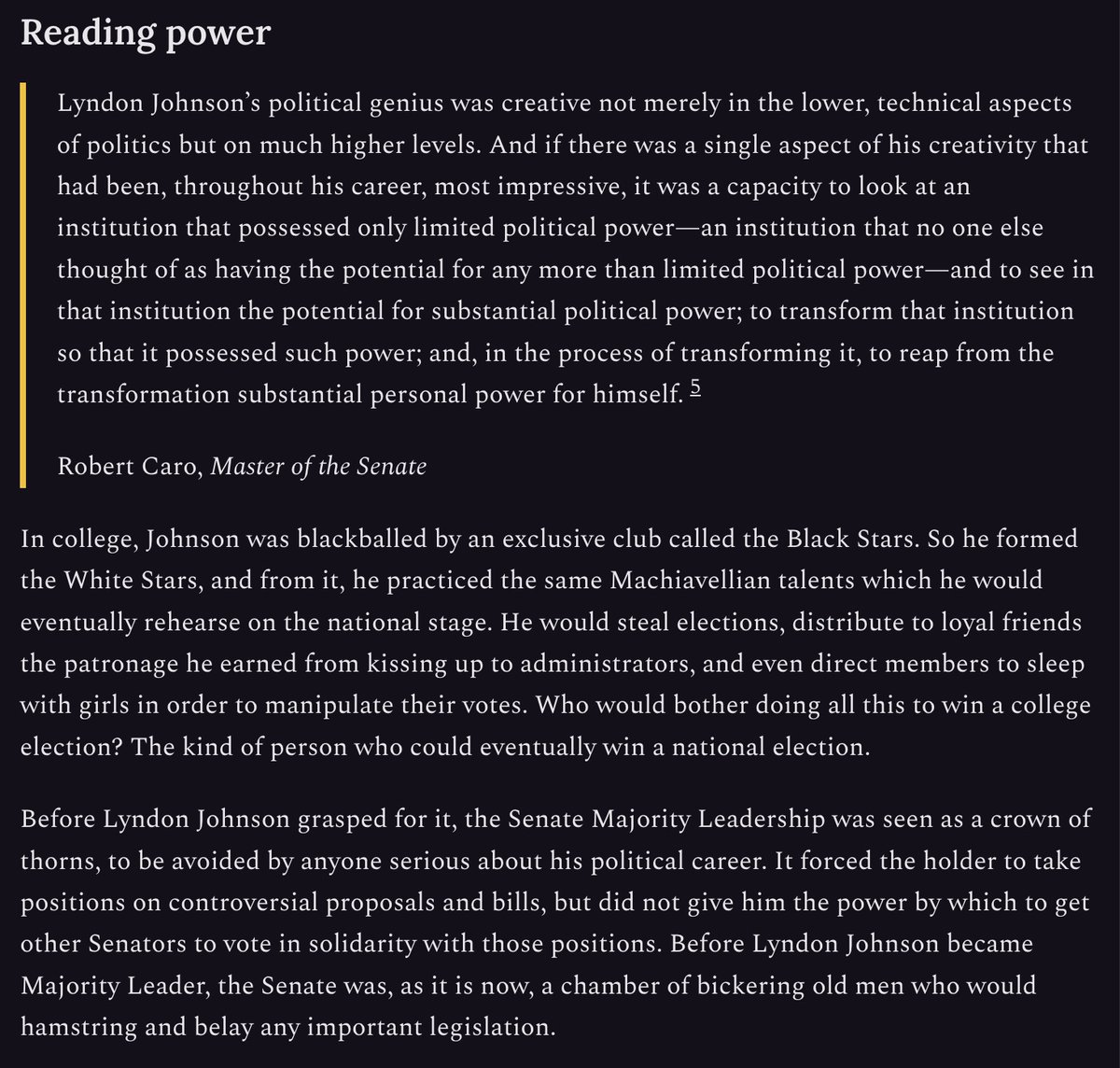

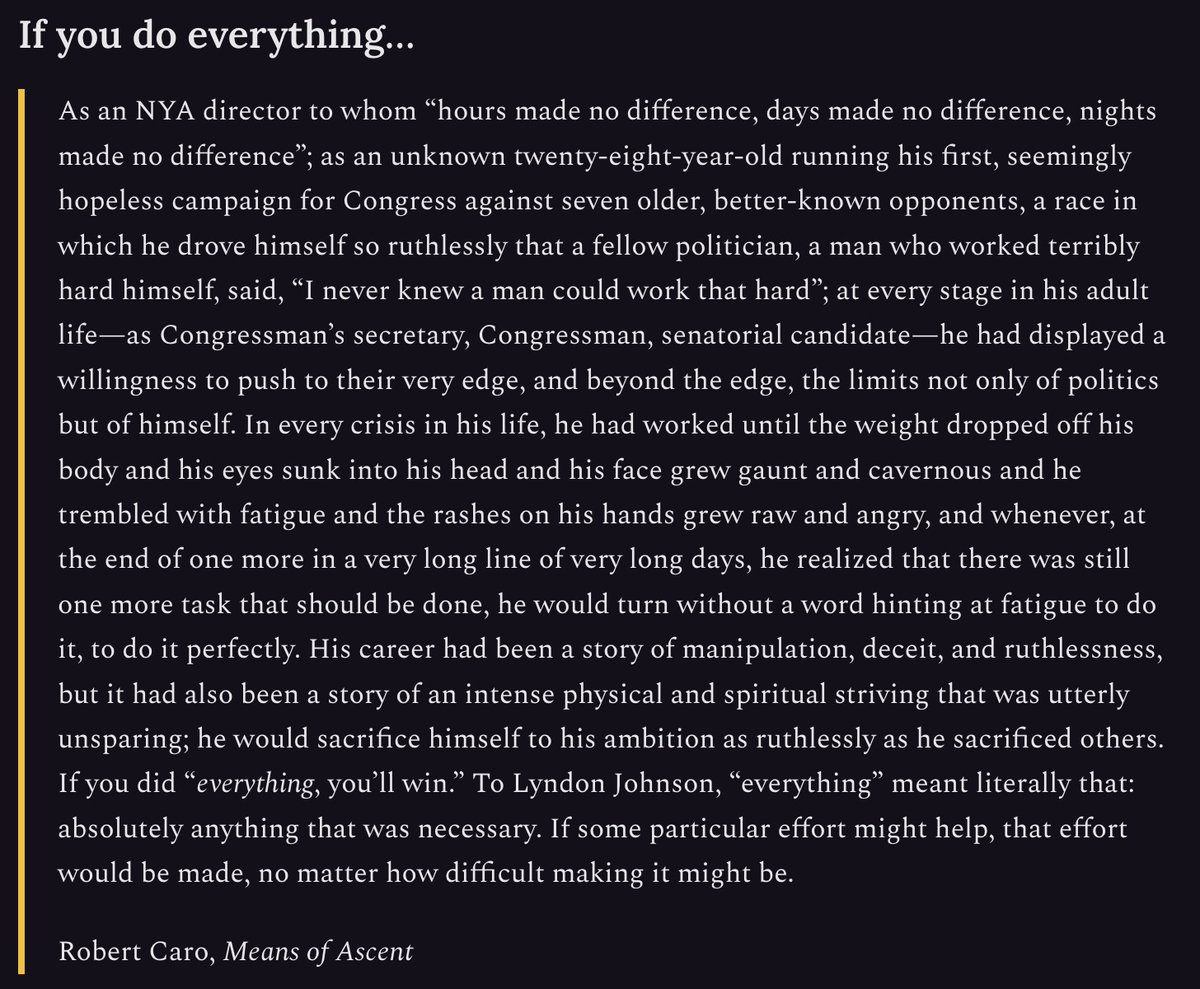

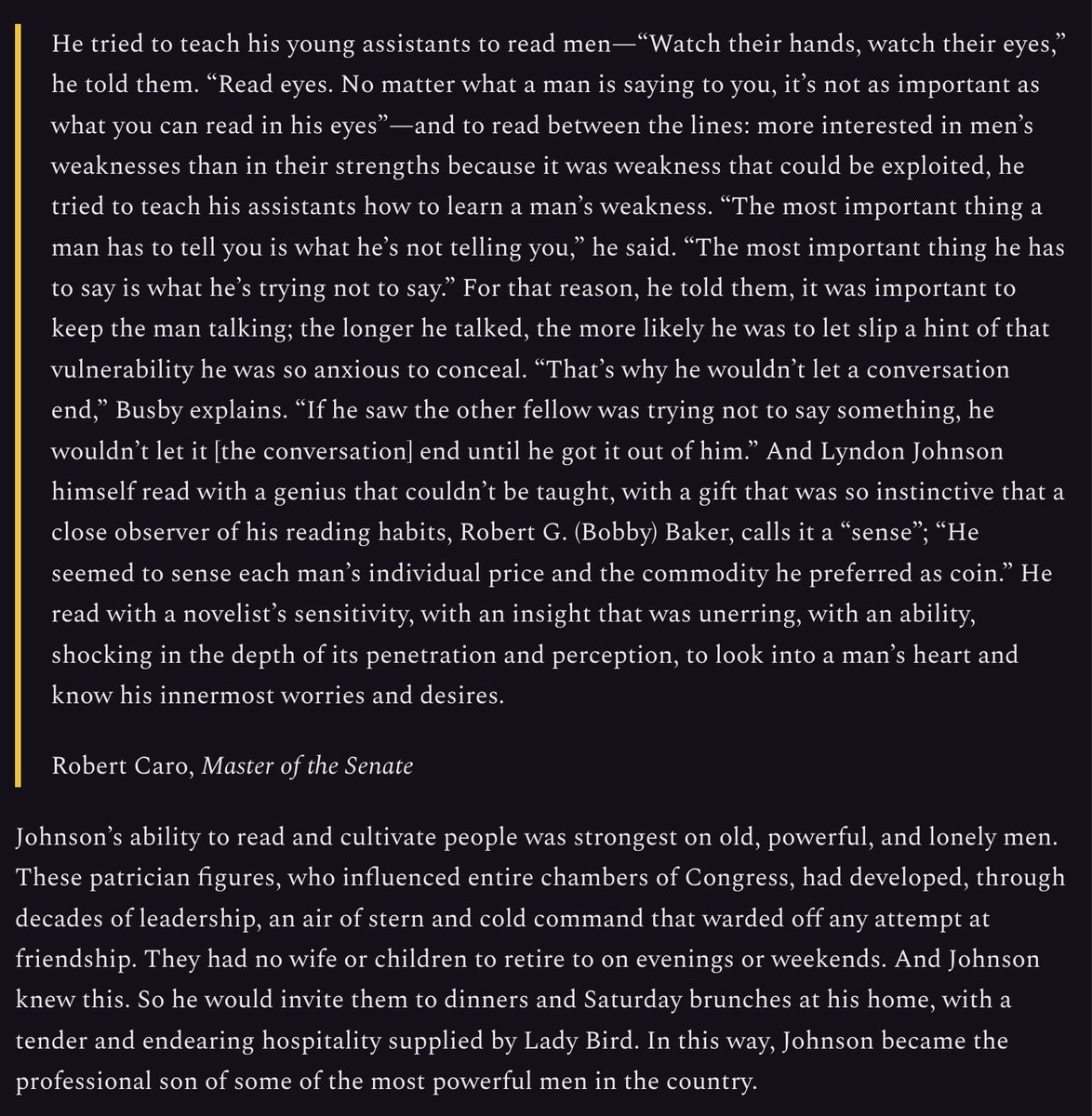

I loved @dwarkesh_sp's summary of Caro's biographies on Lyndon B Johnson, covering power, political intrigue, ambition, indomitability, and more. I strongly recommend it! ht @arbesman dwarkeshpatel.com/p/lyndon-j…

1

11

3,039

14 May 2023

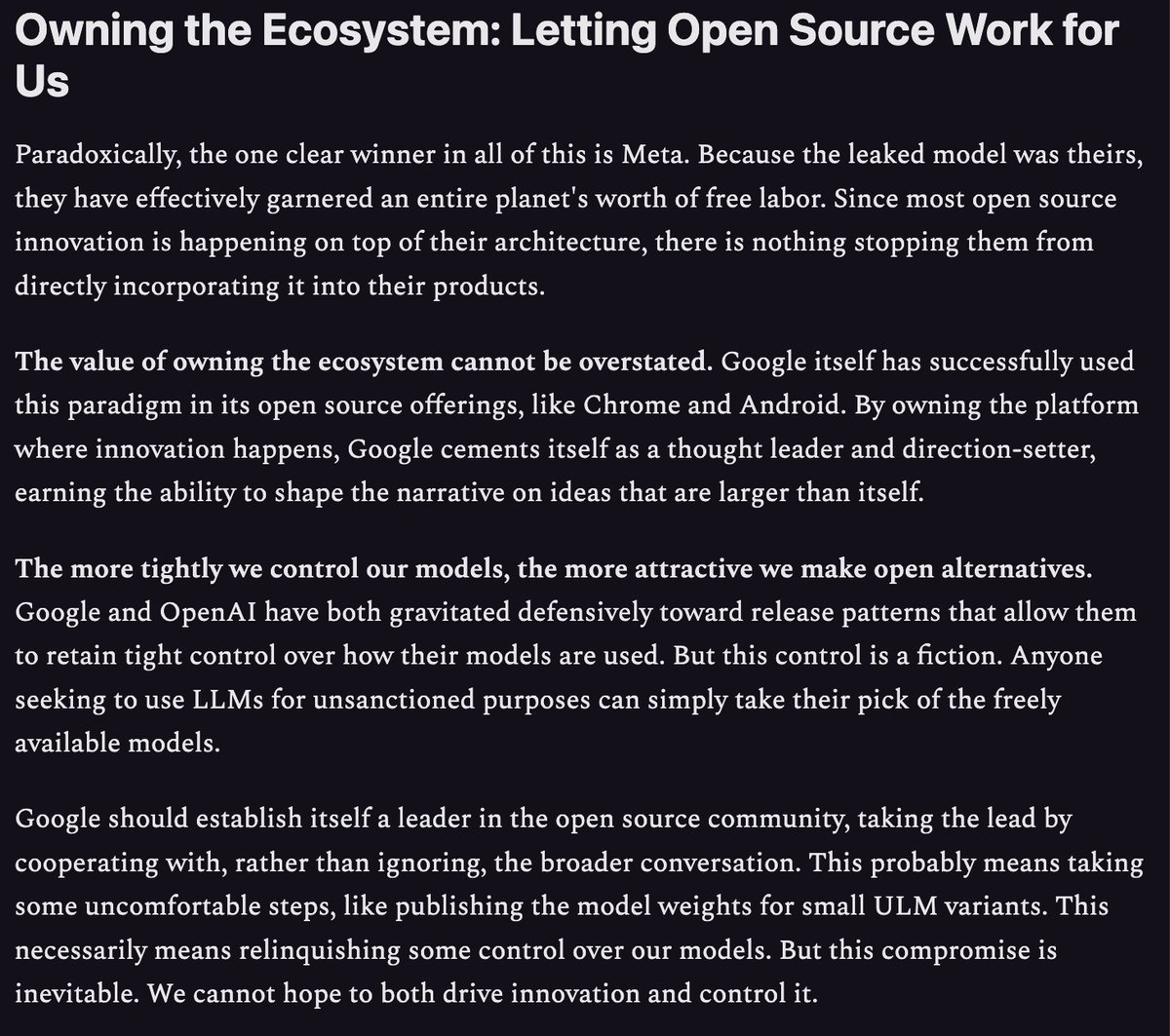

"The more tightly we control our models, the more attractive we make open alternatives" -- from leaked internal document from Google semianalysis.com/p/google-we…

1

276

15 Jan 2023

"The best thing that founders can do is subtraction." - @tobi in an awesome interview with @farnamstreet where he talks about focus, fighting bureaucracy, professional CEOs vs founder-led companies, and more youtu.be/hUug8tEWtoY?t=856

355

14 Jan 2023

Great article on Clausewitz & strategy ht @WTCM3

"Strategy is about picking the right battles. Tactics are about successfully executing those battles."

"Strong determination in carrying through a simple idea is the surest route to success."

gsb.columbia.edu/articles/id…

250