Professor @Harvard, Director @HarvardBizGov, Senior Fellow @PIIE, teaches Ec10, words @nytopinion, was Chair of Pres Obama's CEA. Some posts may be educational.

Joined April 2011

- Tweets 21,728

- Following 1,915

- Followers 245,783

- Likes 7,122

4,316 Photos and videos

Jun 10

Looking at today's headlines on inflation I want to re-up this.

Is a peculiarity that 100% of the jobs focus is 1-month while majority of inflation focus is 12-months.

If May-25 jobs was 400K & May-26 was 300K the 12-month number would go down but no headline or even line in the article would be "job growth stalled in May".

10 Aug 2023

I mostly avoid media criticism because the reporters that write these stories 100% understand all the issues I'm raising and are consistent over time.

But I wish the editorial choices would move away from a focus on 12-month changes, reversing headlines and subheads.

8

11

59

22,382

Jun 10

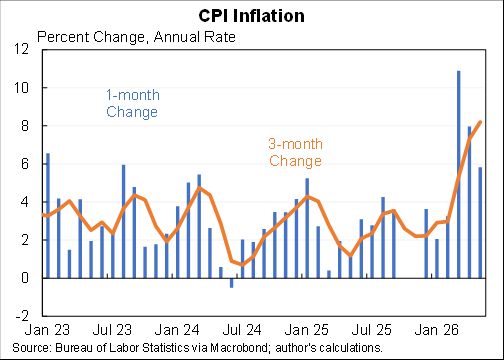

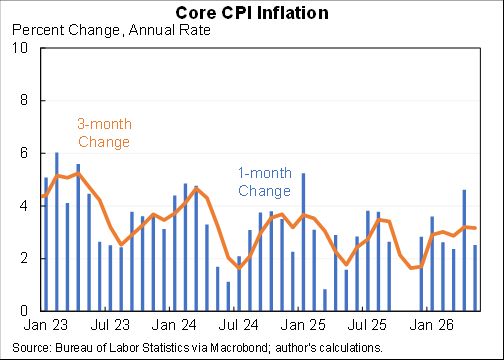

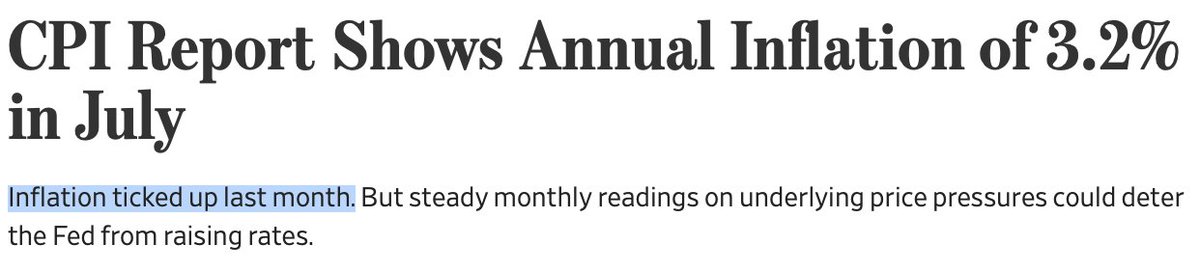

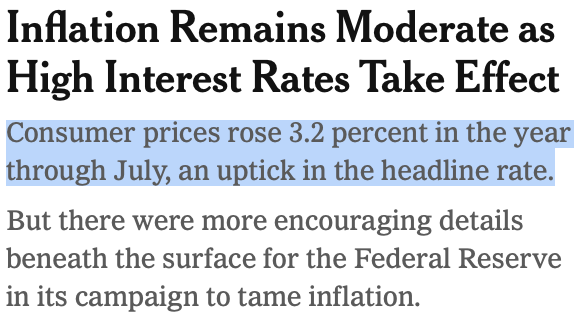

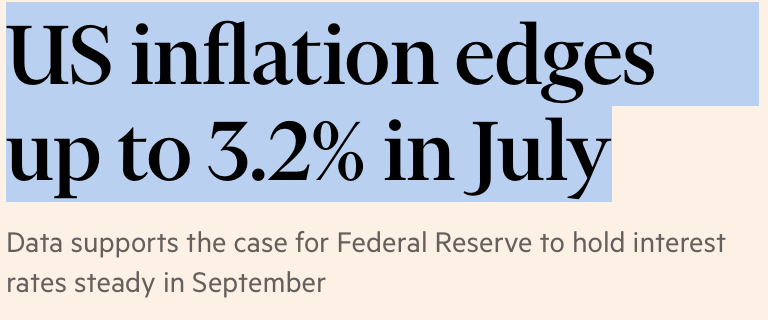

Three things about today's inflation report:

1. 12-month inflation increased (because May-26 > May-25)

2. 1-month inflation slowed (because May-26 < Apr-26)

3. Inflation came in below expectations.

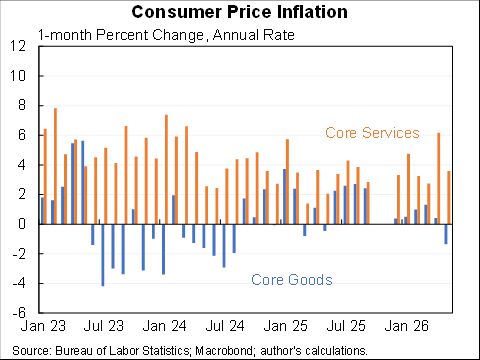

Here is core.

6

15

60

12,460

Jun 10

Headline was still VERY high, just not EXTREMELY high like it was in March and April, as gasoline had a sizeable rise for a third straight month.

3

2

15

4,731

Jun 10

Overall this confirms that the prices consumers pay were not just high but also rising quickly. But the incremental new information was also encouraging in the surprise to the downside in core. Not much here that should force the Fed to hike anytime soon.

6

8

32

8,359

Jun 9

AGI is officially here.

6

6

230

87,586

Jun 9

The first time I've seen you approve of anything Anthropic!w

1

1

18

8,469

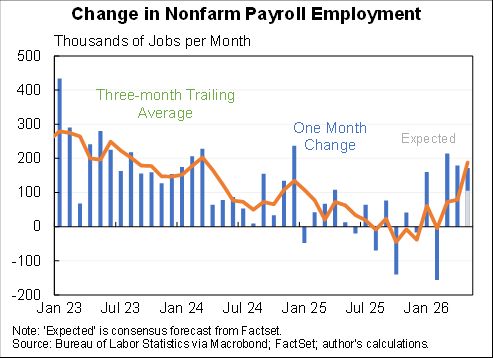

Jun 5

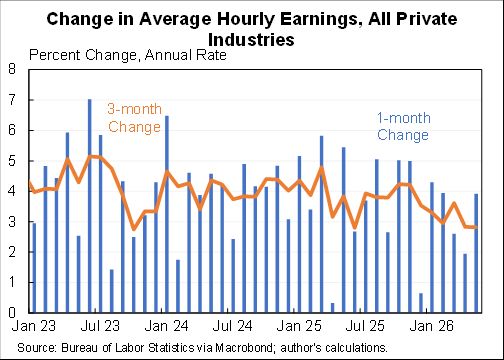

Another strong month for job growth. 172K in May with upward revisions for previous months that brings the three month average to 188K.

Unemployment rate stable at 4.3% while broader measures (U-6 and employment rate) both improved.

7

15

69

9,427

Jun 5

Meanwhile, average hourly earnings continue their slow easing--something you see even more clearly in better labor data like Atlanta tracker and ECI. Suggests that labor market is still in a somewhat loose place consistent with gradually easing underlying inflation.

5

3

17

4,565

Jun 5

In crude terms two big things happening: (1) tariffs/Iran and (2) AI boom (including direct effects but also indirect like higher stock prices helping to support consumption).

Both of them lead to higher inflation but they cancel out when it comes to the labor market.

3

3

22

4,123

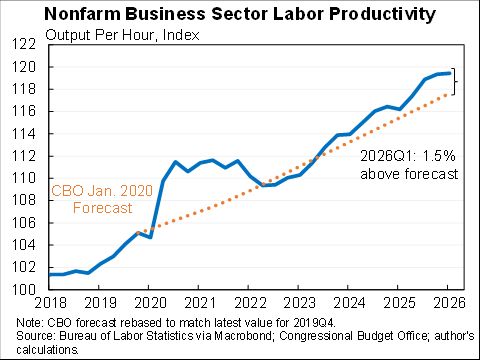

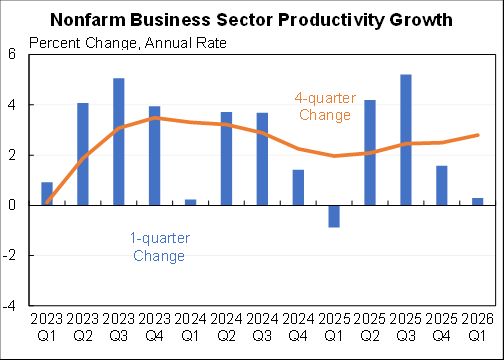

Jun 4

The macro data giveth and the macro data taketh. Productivity for Q1 revised down. Still a respectable pace over the last five quarters (2.1% annual rate--five quarters because shifting means Q1 & Q2 last year were two sides of the same coin).

5

2

42

7,316

Jun 4

And ahead of the CBO pre-COVID forecast. My read of the scanty micro readings on actual use and productivity are consistent with about 0.5pp of additional productivity, cumulative, due to AI.

3

22

4,939

Jun 4

For the cycle as a whole we're comfortably above post-1973 except dotcom (which shows up partially in two of these bars).

FWIW, if I had to pick a number for the next decade I would pick 2.3%. That is way above CBO, about inline with people I've surveyed, but way below SV view.

1

2

17

5,188

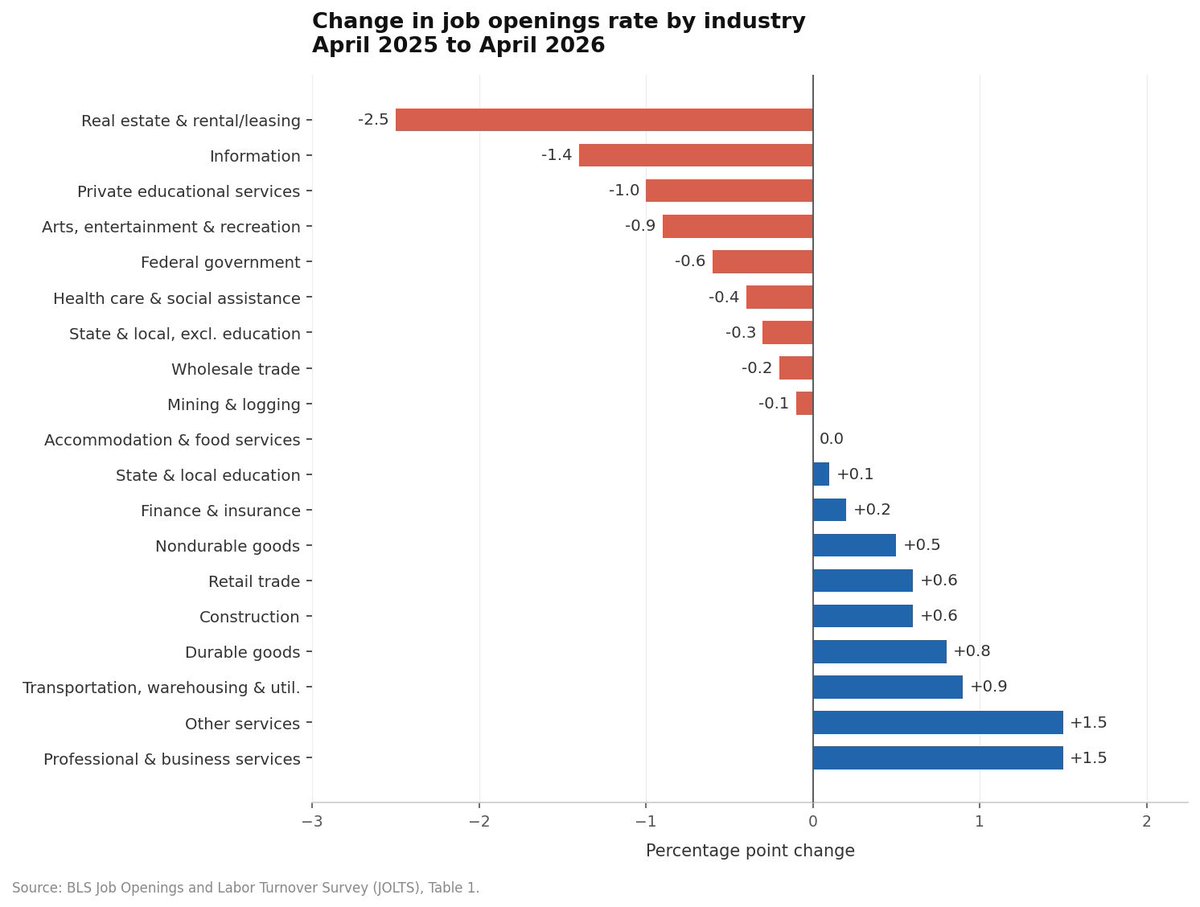

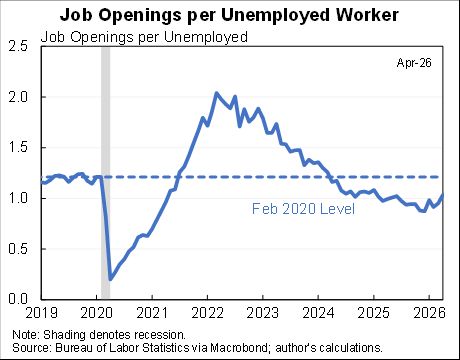

Jun 2

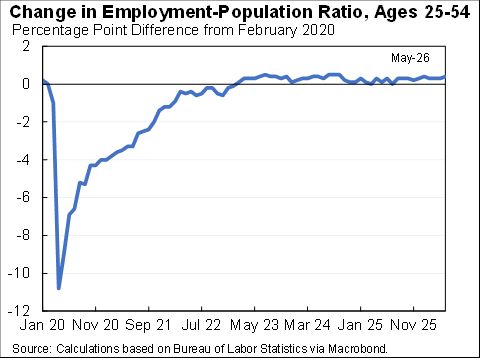

The labor market has been steadily tightening, albeit just a notch--and maybe in absolute terms it is still loose.

Unemployment rate stable/edging down while job openings stable/edging up.

Ratio of V/U has risen from a low of 0.87 in December to 1.03 in April.

3

7

44

8,851

Jun 2

Finally, the hiring rate bounced down in April but was from a temporary bounceup in March. The real read is it remains low. As do job separations.

1

6

3,794

Jun 2

Bottom line: We have a lot of inflation. Much of it transitory supply-side like tariffs and oil. The other big questions are: (1) will it build into expectations and (2) will there be demand-side, labor-market tightness. This says be just a little more worried about the later.

7

1

12

3,760