Operating and building the home services company that I dream of. Minneapolis west metro.

Joined June 2009

- Tweets 4,100

- Following 812

- Followers 1,215

- Likes 2,098

126 Photos and videos

Jay Sachetti retweeted

Jan 20

I have no reason to believe Bruley is being anything but truthful. And listening to him describe how people are being treated, in an area I know quite well, should anger every damn person in this country, regardless of your political allegiance.

Jan 20

Brooklyn Park Police Chief Mark Bruley: "The last 2 weeks we as a law enforcement community have been receiving endless complaints about civil rights violations in our streets from US citizens. What we're hearing is they're being stopped in traffic stops or on the street with no cause and being demanded to show paperwork to determine if they are here legally. We started hearing from our police officers the same complaints as they fell victim to this while off duty. Every one of these individuals is a person of color ... it has to stop"

23

21

289

31,478

Jay Sachetti retweeted

24 Oct 2025

It’s no surprise that everybody hates their home warranty provider.

As a contractor - we refuse to work for them.

Why?

Their singular objective is to collect homeowner premiums, and pay out as little as possible in claims.

To this end, they hire the cheapest contractors who are instructed to find the lowest cost solution (not the best solution) to your problem.

Which means poorly trained, poorly compensated, and poorly equipped trades people will be handling your warranty claim.

If you are a contractor, run from this type of work.

If you are a homeowner: find a trustworthy, high-quality contractor and hire them directly.

28

6

127

15,676

Jay Sachetti retweeted

3 Sep 2025

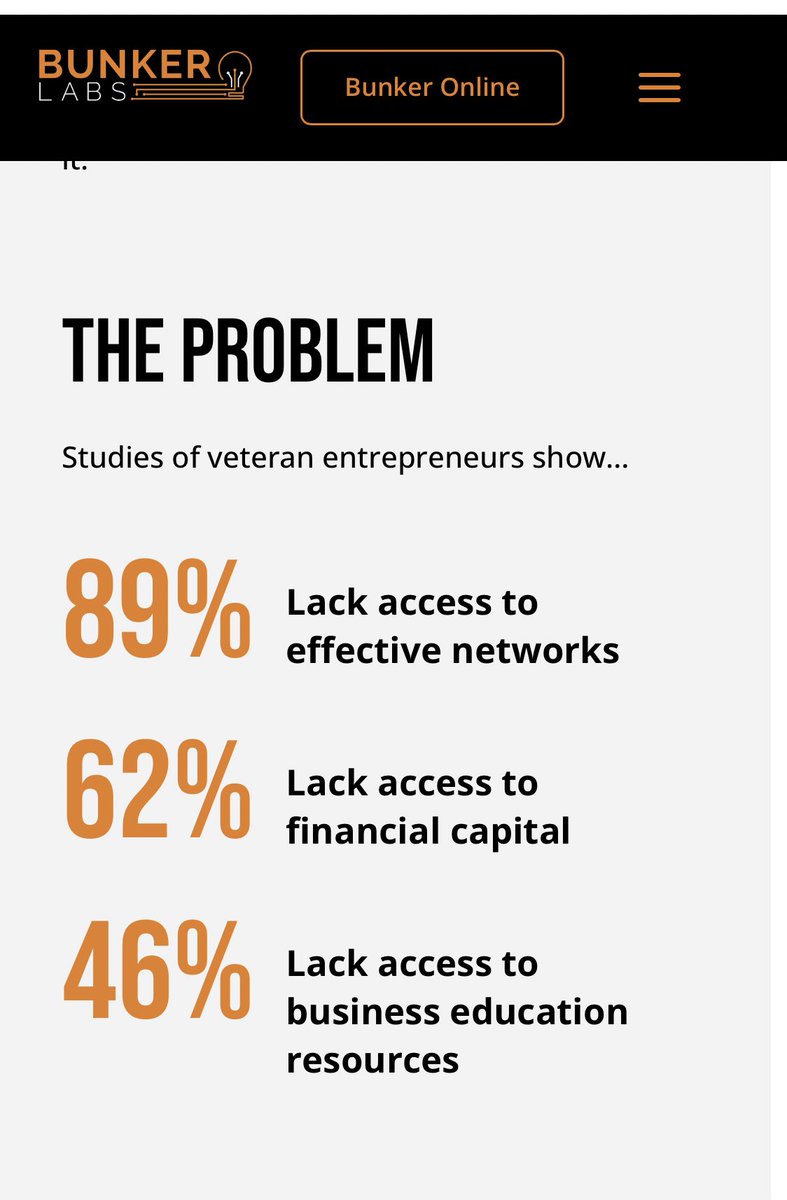

Hire veterans.

We’re not doing enough to help these incredible men and women transition back to civilian life.

Especially those with leadership experience.

They’ll supercharge your business.

21

5

154

14,752

Jay Sachetti retweeted

4 Aug 2025

Friendly reminder if you bootstrap a startup to a million in revenue, you'll probably make more than 99% of venture backed founders.

91

56

1,305

100,917

Jay Sachetti retweeted

19 May 2025

A simple rule of thumb in acquisitions - your net cash flow will likely be half of what the sellers was for 1-2 years.

If SDE was $500k, your cash flow will be $250k, etc.

23

2

187

56,754

31 Mar 2025

What are the latest and greatest educational resources and coursework that I can point people to in the ETA space?

Books make the list. MBA schools. @SMB_Attorney had an email-led course and @Sam_Rosati might have something, but I can't find either.

@Schornack @ParsleyETA

3

2

417

Jay Sachetti retweeted

22 Mar 2025

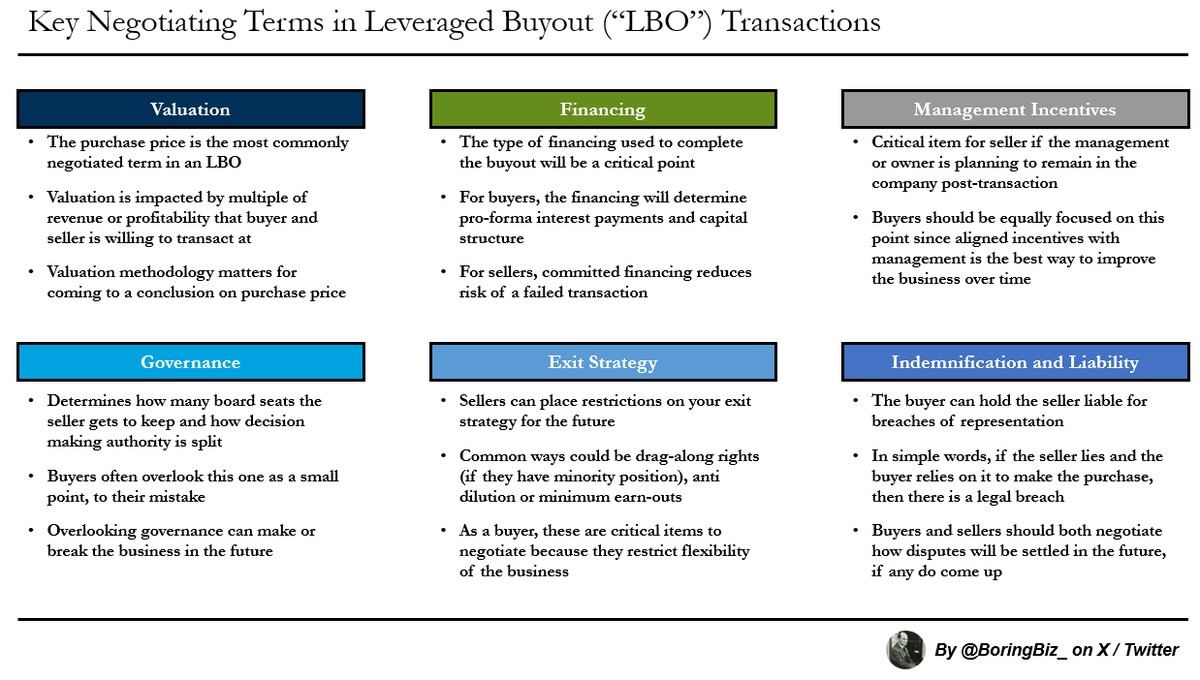

Primer on Key Negotiated Terms in a Private Equity LBO

2

39

511

60,141

Jay Sachetti retweeted

12 Mar 2025

Used EOS in my eCommerce business, which grew to over $44M in revenue before being acquired in 2020. It was a game-changer for accountability, alignment, and proactive goal-setting after years of firefighting. Some thoughts on what worked, what didn’t, and advice for Hampton. 🧵

2

2

1

1,898

Jay Sachetti retweeted

19 Feb 2025

The least important thing business owners have in common is company size.

Whether you have 3 employees, 30, or 3000, you are in the same club.

Because responsibility for other people’s employment forever changes you.

• Laying awake worrying over payroll

• The hell of having to lay people off

• Knowing that real families depend on your decisions

It creates an invisible kinship much deeper than a job title. It’s a fundamental shift in worldview.

Taxes. Regulations. Healthcare costs. Government policies.

These all become important in ways not obvious for people who don’t sign checks on the front.

It is not about the size of your company. It is the weight of responsibility.

23

8

120

4,926

Jay Sachetti retweeted

18 Feb 2025

Your "side hustle" cleaning business isn't failing because of the economy.

It's failing because you thought IG reels of people wiping windows would magically fill your calendar.

The gold rush of easy LSA leads is over.

Welcome to the real world. Time to get your hands dirty.

Remember that guy Kevin who started a cleaning business because some dude with perfect hair told him to on YouTube? Yeah, he just went back to his corporate job.

Not because the business model is broken….I’ve been running my remote cleaning business @MaidThis for 11 years.

But because he thought "passive income" meant watching leads roll in while he played Fortnite.

The reality? Local service businesses require actual... service. And local... presence.

Those Instagram cleaning gurus sold you a dream where all you needed was:

➜ A fancy logo

➜ Some automation software

➜ A TikTok account

➜ The audacity to charge premium rates

But they conveniently left out the part about:

➜ Door knocking

➜ Networking events

➜ Community involvement

Here's the brutal math: 80% of new cleaning businesses won't make it 24 months.

Not because the market is saturated, but because most founders think "building a brand" means posting motivational quotes over stock photos of vacuum cleaners and flipping on digital ads.

The survivors? They're the ones who:

1. Network at local chambers of commerce

2. Join BNI groups

3. Build real relationships

LSA (Local Service Ads) used to be the cheat code. Now it's just part of a broader marketing mix.

Digital marketing changes CONSTANTLY.

If you started a business based on a single lead source and that lead source goes away…you need to innovate or go bust.

TL;DR:

➜ Your cleaning business isn't failing because of market conditions

➜ It's failing because people believed in digital fairy tales

➜ Real local businesses require actual local presence

➜ The ones who will put down the phone and go out to meet people will win

8

2

48

9,527

Jay Sachetti retweeted

15 Feb 2025

SBA loans have low default rates, right?

Bob sat in his cramped home office, surrounded by stacks of maintenance contracts and crew schedules.

Three years ago, he'd been a rising executive at a Fortune 500 company, pulling in $205,000 a year plus bonuses.

Now he was the proud owner of "Premium Landscape Solutions"—purchased with a big ass SBA loan that had seemed like such an obvious move.

SBA loans have low default rates, right?

Youtube made buying a business so OBVIOUS and the business broker had made it sound perfect....an established landscaping company with recurring maintenance contracts, reliable crews, and a strong reputation in an affluent suburb.

"A steady business with great cash flow," he'd read, "and room to expand into high-end landscape design!"

The numbers supported his pitch: Healthy margins, and a seemingly reasonable purchase price.

With the SBA covering 90%, James only needed to put down $130,000—a fraction of his savings after 10 years in corporate America.

Bob already had ideas of other companies he could buy!

He remembered his wife's concerned expression when he'd explained his plan to "escape the corporate rat race."

She'd supported him, of course, but her eyes had betrayed her worry.

Their youngest had just elementary school and she was pregnant with their second.

Her salary had supported everyone while Bob "pursued his dream" of being an entrepreneur....

...because SBA loans have low default rates, right?

The spreadsheets he'd created showed they still could—the business would generate enough income to maintain their lifestyle and then some.

He'd even used his Six Sigma training to map out process improvements that would boost efficiency by at least 30%.

Then one day - he actually had to run and own the business.

The people around the transaction evaporated, the business influencer made their $899 on the course, and it was time to start interacting with reality.

Reliable crews turned out to mean "reliable until something better came along."

Weather created havoc with scheduling—every rainy day meant lost revenue he could never recover.

Equipment broke down constantly; the previous owner hadn't mentioned that half the mowers were on their last legs, and Bob had never repaired anything in his life.

Each season brought its own challenges: spring's overwhelming demand, summer's brutal heat and crew shortages, fall's race against time to complete projects before winter, and winter's nerve-wracking lull.

His corporate experience, which he'd thought would give him an edge, often proved a hindrance.

Crews didn't care about his "strategic vision" or process optimization initiatives.

They just wanted their paychecks on time and another few bucks an hour.

His attempts to implement professional management systems were met with resistance or blank stares.

Bob had so many ideas to make thing better.

He just didn't have the team, cash, or energy to make them happen.

The business didn't need a former executive; it needed someone who could handle endless equipment repairs, manage weather-dependent scheduling, and deal with increasingly demanding clients who expected country club results on a suburban budget.

The business wasn't failing—he made his $7,200 monthly loan payment without fail.

Because SBA loans have low default rates, right?

But his personal income had dropped to less than a third of his former salary, and he was working 2X as much.

The crews got paid, the suppliers got paid, the bank got paid, and James got whatever was left over.

Thoreau's words haunted him during his long drives between job sites:

"The cost of a thing is the amount of what I will call life which is required to be exchanged for it."

Almost a decade of loan payments stretched ahead of him—seven more years of missed family dinners, canceled vacations, and constant stress about weather forecasts and equipment breakdowns.

He knew he probably wasn't going to miss a payment, because SBA loans have low default rates, right? He remembers the broker telling him that.

The worst part wasn't the money or even the hours—it was the creeping realization that he'd traded his life's prime years for a cage of his own design.

He was stuck in an endless cycle of crew management and customer complaints, too financially committed to walk away, too proud to admit he'd made a mistake, and too exhausted to figure out an exit strategy.

Bob's story would never appear in the glowing SBA default statistics that lured him in, yet he paid a devastating price measured not in dollars but in missed bedtime stories, mounting health problems, and the quiet death of his professional dreams.

While the brokers, business influencers, and loan officers had made their money and moved on to their next deal, Bob remained trapped in a cage of his own making....too financially committed to escape and too exhausted to find a way out.

In pursuing the promise of entrepreneurial freedom, he had only succeeded in trading his corporate shackles for a heavier set—ones that bound not just his career, but his health, his family life, and his future to a business that owned him far more than he would ever own it.

But it's all ok, because SBA loans have low default rates, right?

Be careful out there amigos.

83

21

304

141,212

Jay Sachetti retweeted

12 Feb 2025

Guys/gals, I can't tell you enough how much it pays to just get in the game.

If you have to go small on your first deal to get in the game, then go small.

Those "off market" deals that you couldn't find when you were just a "searcher"? They will find YOU once you're in the game and are an "operator."

Infinitely easier to raise equity and debt capital once you're already in the game as well.

Do whatever it takes to get in the game.

28

5

161

33,350

5 Feb 2025

This reminds me of some time that I spent with @KrissBergTweets that really helped me release guilt of the past.

If you’re carrying burdens, know that you’re not alone and that you deserve to give yourself grace.

Lead with love! Including for yourself.

5 Feb 2025

I had a semi-spiritual experience this weekend that I want to share with you all.

The past two or three years have been pretty challenging for me. Aside from the direct professional & personal challenges, it’s been extra rough to go through it all pretty publicly. Radical transparency is a fun wave to ride when things are going well. But it is definitely less fun when things are not going well.

On top of that, I was fortunate to bring together an incredible group of investors. Investors in our funds and crowdfunding campaign are nearly 1,000 people that I hugely admire, many of whom are friends. And I got to spend the last almost three years sending this incredible group of people a steady stream of disappointing updates. Not to mention over 100 founders who’ve had to deal with the version of me that’s consistently been stretched thin nearly to the breaking point.

I felt like I spent the last three years, essentially in a form of managed decline, where I wake up every day and bring a ton of energy and effort, good decision-making and skills just to make things get a little less worse, a little more slowly than they otherwise would have.

Between doing that grind every day, and having to recount the process to an audience of more or less everyone I admired… it really, really wore on me psychologically.

The thing that I realized this weekend was that I was carrying around with me a heavy almost-invisible weight of something like embarrassment or shame from this process.

Despite the fact that nearly every time I would catch up with someone - one of our investors, or supporters, or just anybody who was aware of the situation at all - they would go out of their way to comment on how they admired, appreciated, and approved of how I had clearly done my best to navigate a really challenging situation.

I’m talking about folks going out of their way just to let me know this fact alone, not just as a pleasantry because we happen to be talking to one another. So by all accounts intellectually, I should have understood that that people get it, that people can understand that being professional and making the best of a really challenging situation is not something to be ashamed of. It's something to be proud of.

And intellectually I could agree with it, I just didn't believe it in my bones.

Somewhere deep down I felt ashamed. And I carried that with me implicitly into my world view; into what I thought I could do next, into how I felt about myself and where my life could go from here.

But this weekend I had the right combination of a long drive, some time to myself, and a couple of good audiobooks.

The nudge that triggered it was a statement from Martha Beck: "oftentimes, the internal beliefs that cause us the most suffering are ones that we intellectually know are absolutely false and yet we believe them anyway." I asked myself, "What kind of beliefs like that I might be holding?" And just immediately this feeling of shame came into complete focus.

In an instant I was able to clearly see this contradiction in myself and to both notice the implicit shame I was feeling and to see how silly and unfounded it was. I saw how that feeling was clouding and infecting almost everything in my life with a tint of negativity and pessimism.

All at once I was able to drop that belief and see the reality that I, in fact, should feel immensely proud of the effort over the last few years. And that’s what I felt... proud. Really damn proud. It felt like maybe about a 50-pound weight vest just melted off with me all at once.

So I just wanted to share that in case somebody else needed to hear the same nudge.

2

6

509

Jay Sachetti retweeted

5 Feb 2025

If I were to start a home services company today I wouldn't start a cleaning company, and neither should you. Here are my reasons:

(this isn't one of those things where every bad reason is a good reason)

8

5

59

17,743

Jay Sachetti retweeted

29 Jan 2025

If you're serious about buying a business in 2025

Join us at SMBootcamp Live on April 30th-May 2nd in Downtown Tampa, Florida

Learn more and apply below:

1

2

4

2,230

Jay Sachetti retweeted

29 Jan 2025

🚨🚨Attention Minnesota/Upper Midwest searchers or other business buyers/sellers🚨🚨

February 12: Hosting an ETA/M&A happy hour in Chanhassen 4-6 pm.

Already expecting 20 searchers/service providers.

DM/email me and will send you the invite.

1

6

642

Jay Sachetti retweeted

2 Jan 2025

ETA and your search slowed down Q4 2024? Quality listings down? Discouraged?

Standby and get ready to pounce in the next few weeks. Here’s why:

In addition to all our buy-side work, we do tons of sell-side work and, unless a seller is under LOI, sell-side biz owners’ work towards a sale plummets as the leaves change from green to brown.

By Thanksgiving “the kids and grandkids are in town.”

By early December there’s the trip to Italy.

Christmas? Forgetaboutit.

“Let’s just revisit in the new year.”

Well the new year is here. Brokers/bankers finalizing CIMs. Sellers back in the saddle after mentally confirming desire to sell over yet another stressful holiday season operating the business.

Listings about to pop. Stay strong.

5

1

21

4,002

24 Dec 2024

This Christmas, spread love and joy!

Here’s a Christmas story from the world of SMBs…

We did our holiday party last week with food and presents. Faces were smiling, laughter could be heard, and all were content… except for one.

2

3

185

24 Dec 2024

To my surprise, our office manager had gathered the team again on Monday morning. I was confused… why?

She talked about how strong this team is when we stick together and support each other.

Then, that now-grown girl finally got her Barbie.

1

1

105

24 Dec 2024

She beamed like the sun as her story inspired us. And not an eye was dry.

This Christmas and holiday season, let’s be thankful for all that we do have and strive to make a difference for others — no matter how small that may seem.

Merry Christmas! 🎄

2

80