CEO - Johnson Financial LLC (Fractional CFO Services) Co-Owner - Boulder Designs by Custom Stone Monuments

Joined September 2016

- Tweets 422

- Following 145

- Followers 117

- Likes 1,310

47 Photos and videos

Brad Johnson (Fractional CFO) retweeted

12 Nov 2025

🍁Enhance your Ranch with custom Farm signage. Let us help you showcase your property with style and durability. 🌲#Ranch #ranchlife #ranchsignage #rockladytx

1

2

64

Brad Johnson (Fractional CFO) retweeted

6 Jul 2025

📢 One Big Beautiful Breakdown of the One Big Beautiful Bill 📢

A monster thread of the most relevant parts of the newest tax law:

11

44

260

58,401

20 Jun 2025

Check out my latest article: 💡 Why More Growing Businesses Are Turning to Fractional CFOs linkedin.com/pulse/why-more-… via @LinkedIn

1

1

61

Brad Johnson (Fractional CFO) retweeted

2 May 2025

Some of the good folks that came to our Dealonomy SMB meetup at Top Golf in Houston today. 🏌️♂️

8

2

20

3,079

Brad Johnson (Fractional CFO) retweeted

21 Mar 2025

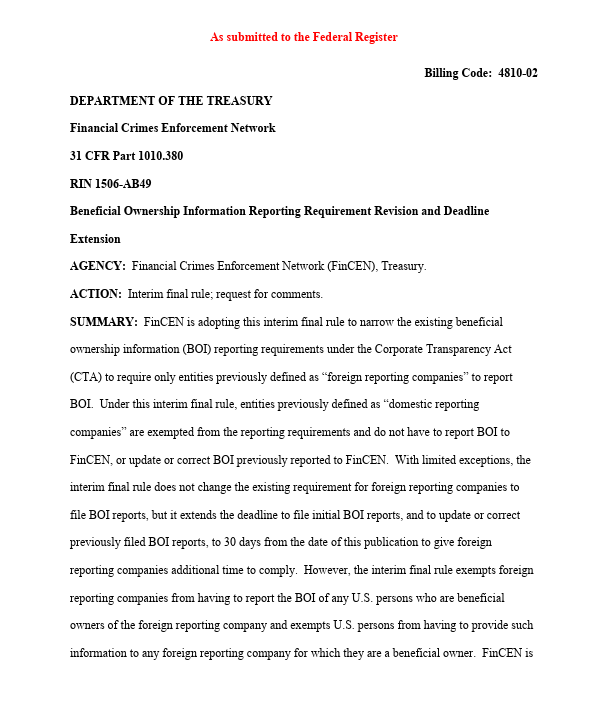

🚨BOI UPDATE!!🚨

Did you miss me? Be honest!

Consistent with the prior announcement from @USTreasury, today FinCEN issued an interim final rule that removes the requirement for U.S. companies and persons to make beneficial ownership filings under the CTA.

Note that the law will still apply to foreign entities, and updated rules to apply to them are still pending.

That said, several congresspersons who supported the CTA have begun heightening their demand for @USTreasury unilaterally revising the rules through procedures that they claim do not comply with the CTA as passed by Congress.

In other words, new challenges that try to enforce the rule as originally issued could be coming!

But for now, suffice it to say, BOI reporting continues to be, at best, dead on arrival for US companies, and at worst, unenforced pending further developments in this wild ride.

I'll keep you posted as more updates come!

12

13

65

9,107

Brad Johnson (Fractional CFO) retweeted

17 Mar 2025

Your friendly reminder that partnership tax returns are due today!!

If you’re behind (like I am), most online filing services (like @turbotax) allow you to file a 6 month extension for free.

Takes about 2 minutes with name, address and EIN.

1

4

17

2,222

Brad Johnson (Fractional CFO) retweeted

14 Mar 2025

Tax Credits vs. Tax Deductions

Knowing the difference, how they work, and which ones are available to you can save you thousands on your tax bill

Tax Credit: A dollar for dollar reduction to your tax bill (Note; Some tax credits are refundable, meaning they can reduce your tax bill below zero and result in a refund. Others are nonrefundable, meaning they can only reduce your tax liability to zero but won’t generate a refund).

Example: If you owe $2,000 in taxes, and you have a $1,000 tax credit, you now owe $1,000 in taxes.

Common Tax Credits: Child Tax Credit, Earned Income Tax Credit, Foreign Tax Credit, Lifetime Learning Credit

Tax Deduction: Lowers your taxable income, which in turn reduces the amount of tax you owe. The actual tax savings depend on your tax bracket.

Example: You have $100,000 in gross income, but you have $30,000 in deductions, your taxable income is now $70,000 and you are taxed on that $70,000.

Common Deductions: Qualifying Medical Expenses, Charitable Giving, Mortgage Interest, Property Taxes

The standard deduction makes tax filing easier for people without many itemized deductions. The standard deduction for 2024 is $14,600 for single filers and $29,200 married filing jointly. Itemizing deductions is only beneficial if your total itemized deductions exceed the standard deduction.

Important to know the difference between the two and how they can impact your financial life.

1

2

5

400

Brad Johnson (Fractional CFO) retweeted

3 Mar 2025

🚨Important BOI Update🚨

We’ll unpack this more when I’m not out at dinner a margarita in…but it looks like @USTreasury announced that the CTA fines and penalties as they currently stand will NOT be enforced.

Further, it sounds like they may be updating the rules to narrow the scope of applicability for foreign owned LLCs, which would obviously relieve a lot of the regulatory burden on American small businesses.

Stay tuned for more as we unpack more from this announcement!

2 Mar 2025

The Treasury Department is announcing today that, with respect to the Corporate Transparency Act, not only will it not enforce any penalties or fines associated with the beneficial ownership information reporting rule under the existing regulatory deadlines…

8

8

76

46,122

Brad Johnson (Fractional CFO) retweeted

26 Feb 2025

Sterling’s Law of Finance Bros:

The more someone talks about Excel keyboard shortcuts and how complicated their spreadsheets are…

The more likely they are to be completely incompetent when it comes to understanding how a business works or structuring a deal.

16

2

88

7,971

21 Feb 2025

Not sure who needs to hear this… but keep plugging. Keep selling. Work smart, work hard, and it will pay off. 💪🚀

1

32

20 Feb 2025

3/21 everyone…3/21!!!

20 Feb 2025

Breaking News 🚨

If you own a business, you have to file a BOI report by 3/21.

Follow @KHendersonCo for more details!

2

65

Brad Johnson (Fractional CFO) retweeted

19 Feb 2025

Talking to business owners, I see this mistake all the time:

They think raising prices will scare customers away. One owner was hesitant—until he saw what happened next… 🧵

1

1

2

274

19 Feb 2025

Talking to business owners, I see this mistake all the time:

They think raising prices will scare customers away. One owner was hesitant—until he saw what happened next… 🧵

1

1

2

274

19 Feb 2025

Higher prices = higher profit margin = less stress.

With more breathing room, he could actually invest in growth instead of scraping by.

1

1

33

19 Feb 2025

If you’re booked solid but barely making money, it’s not a demand problem.

It’s a pricing problem.

Have you ever raised prices? What happened? Let’s hear your experience 👇

(And if this thread was helpful, retweet 🔁 so more business owners see it!)

1

1

30