Joined March 2025

- Tweets 676

- Following 18

- Followers 268

- Likes 556

155 Photos and videos

Pinned Tweet

May 4

Tagada.io now supports 12 acquirers (Stripe, Adyen, Checkout.com, NMI, Authorize.Net, Airwallex, N-Genius, CCAvenue, Finix, Tap, Mastercard Gateway, Ovri).

But the interesting part isn't the list.

It's the system behind it allowing the SAME transaction to compare Stripe vs Adyen.

They can have a 4-8 point auth gap depending on issuer and BIN.

This routing is the difference between your profit margin or your chargeback going up.

We offer you 24/7 support and a dedicated Account Manager to walk you through the steps and help you transition.

All you have left to do is to make a decision.

Cal.com/team/tagada

2

11

2,452

12h

We get about 50 DMs a day to ask us the same question over and over

We are all in-house.

We built our own PCI orchestrator, we are not a white label of anyone.

Yes, we work with peptides.

Yes, we accept ISO deals.

Yes, you can set up your post purchase funnel without any integrations.

Yes, we have Apple, Google and Klarna pay.

Drop your questions under, we’ll answer 👇

44

13h

Your landing page can sell the promise and still lose the payment.

A page that converts the click is only half the job. If the checkout shows the wrong payment methods, no local option for the buyer's country, or a fulfillment claim the page made but the checkout cannot back up, the buyer hesitates at the one screen where hesitation costs you the order.

The leak is rarely the headline.

It is the gap between what the page promised and what the checkout delivers.

This is why checkout cannot be treated as the last page of the funnel. In Tagada, checkout is part of the offer system: the Checkout Builder, Payment Flows, and per-checkout payment methods exist to match the buyer you just convinced, down to the networks and local options shown.

Match the checkout to the promise, or you keep paying for traffic that bails on the last step.

28

16h

Calendar retries waste attempts.

R01 declines hit hardest at month-end.

The right window is not when accounts are empty, wait a few days.

R05 (do not honor) has no retry window at all. Did you know this?

The issuer flagged the card.

Blind retries drive your dispute ratio up, not your recovery rate.

No one will tell you this. Our team will.

23

17h

AI agents are customers now.

Stripe Sessions 2026 put wallets on agents: tokenized credentials, pre-set spend limits, API payment flow.

Checkout needs an orchestration layer built for buyers born from code.

Tagada merchats are ready, are you?

1

2

48

20h

Dispute ratio at 0.9%.

Customer reviews say 'unrecognized charge.'

Billing descriptor reads 'CORP SERVICES.'

That merchant is flagged.

Acquirers run all three signals together.

Ratio, review language, descriptor match.

When they align, the risk model moves before you get a call.

This is why you need multiple processors you can trust.

Tagada offers this solution to thousands of merchants worldwide.

Give us a call.

27

21h

A cancel flow designed around friction is turning into a liability instead of a retention tactic.

Regulators are moving back toward strict negative-option rules, and the direction is not subtle: canceling has to be as easy as signing up. Friction-as-retention is on borrowed time.

The merchant cost is bigger than compliance. When you force people to fight their way out, you never learn why they left, and you teach your best customers never to come back.

Tagada's view on subscription infrastructure: cancellation should be visible, not buried. Infrastructure should show you who is leaving and why, and let you earn the save with the product, without hard-coding friction into the flow.

Make leaving easy, then make staying worth it. That is retention that survives a rule change.

2

48

Jun 13

Most attribution tools stop counting at the first order.

That is where subscription math gets dangerous. A customer you acquired for $40 looks profitable on order one and underwater by cycle three, once refunds and cancellations land.

If your attribution window closes at checkout, you are grading ad spend on a number that expires in 30 days.

The order is not the outcome. The retained customer is.

Tagada's view is simple: order one is not the KPI for a subscription brand, what happens across cycles is. It is why our analytics track average lifetime value and rebill revenue, so the number you judge acquisition against is the one that survives past month one.

Judge acquisition on what a customer is worth after the third payment, not the first.

42

Jun 13

Meta's algorithm optimizes on the events you send it. Most subscription brands send exactly one: first purchase.

So Meta does its job and finds more people who buy once. Not people who stay. You pay rising CPMs to acquire your worst cohort faster.

The fix is not a new creative or a bigger budget. First purchase tells Meta who bought. Renewal tells Meta who was worth buying. Until renewal is part of the signal, you are optimizing on half the picture.

Tagada's position is that payment outcomes belong in the growth loop, not locked inside a billing system. The renewal, the rebill, the refund are the truest signal of customer value a subscription brand has.

Optimize on the second payment, not the first. That is where your real ROAS lives.

1

45

Jun 13

Your checkout should be an operator surface, not a developer ticket.

Our Checkout Builder gives Framer-level design freedom: tokens, components, breakpoints, and live URL preview.

Change the page at the money moment, without waiting on code.

30

Jun 13

Buying is moving closer to the transaction itself.

Agentic checkout, one-click flows, and assistants that complete purchases mean fewer buyers may be sitting in their inbox waiting on your day-25 retention email. An email-only retention playbook loses reach even while your open rates still look fine.

The signal that matters is no longer the open. It is the renewal that went through, the rebill that failed, the refund that quietly predicts churn. That truth lives in the payment layer.

This is why Tagada treats payments as customer data, not just transaction logs. A renewal, a failed payment, or a refund can trigger the next move in the customer loop through TagadaSend, instead of waiting on an email click that may never come.

Start treating a payment event as a CRM event. The inbox is no longer where retention gets decided.

28

Jun 13

Selling subscriptions isn't high-risk. Running them badly is.

Authorize before you capture. Show your billing descriptor at checkout. Send a rebill reminder 3 days out.

Skip any one and the dispute files before you see it.

Commerce-native billing makes these the default.

Try our Authorize First feature see it reducing your charge backs by 80%.

2

1

2

43

Jun 13

Hopefully you made the most of it while it lasted.

What have you shipped during these past 2 days Mythos/Fable was available to you?

Jun 13

The US government, citing national security authorities, has issued an export control directive to suspend all access to Fable 5 and Mythos 5 by any foreign national, whether inside or outside the United States, including foreign national Anthropic employees.

The net effect of this order is that we must abruptly disable Fable 5 and Mythos 5 for all our customers to ensure compliance.

Access to all other Claude models is not affected.

We apologize for this disruption to our customers. We believe this is a misunderstanding and are working to restore access as soon as possible.

Read our full statement: anthropic.com/news/fable-myt…

1

1

58

Jun 13

A captured transaction can be charged back. An authorized-only one can't.

Tagada's Authorize-First holds authorization, delays capture. Customer disputes it: the authorization cancels. No chargeback, no fee, no ratio hit.

Founders who scale, not test, run this on every rebill.

1

2

31

Jun 12

Tagada's payment orchestration layer reads decline codes at the transaction level.

Every failed rebill surfaces the decline reason in your payment flow at the event, not in a weekly report.

The orchestration layer is the nervous system of your business.

1

1

21

Jun 12

Your last 30 failed subscription payments:

A: retry schedule in your billing tool

B: decline-code-specific routing rules

C: not sure what your platform does on failure

Reply A, B, or C. Most operators land on C.

1

16

Jun 12

The math at $100K MRR.

5% monthly failure rate = $5K in failed payments.

Dunning at 25%: $1,250 recovered. $3,750 gone.

Silent recovery at 75%: $3,750 recovered. $1,250 gone.

$30,000/year difference. Same payment pool.

1

1

17

Jun 12

The vocabulary gap is a decision gap.

Dunning operators ask: how do we remind customers?

Silent recovery operators ask: what did the decline code tell us?

First question puts burden on the customer. Second puts burden on the infrastructure.

1

1

16

Jun 12

What you call it predicts what you recover.

Operators saying 'dunning' recover 20-31% of failed payments.

Operators saying 'silent recovery' recover 70-80%.

Same failed transaction. 3x outcome. The vocabulary gap is the ops gap.

1

3

185

Jun 12

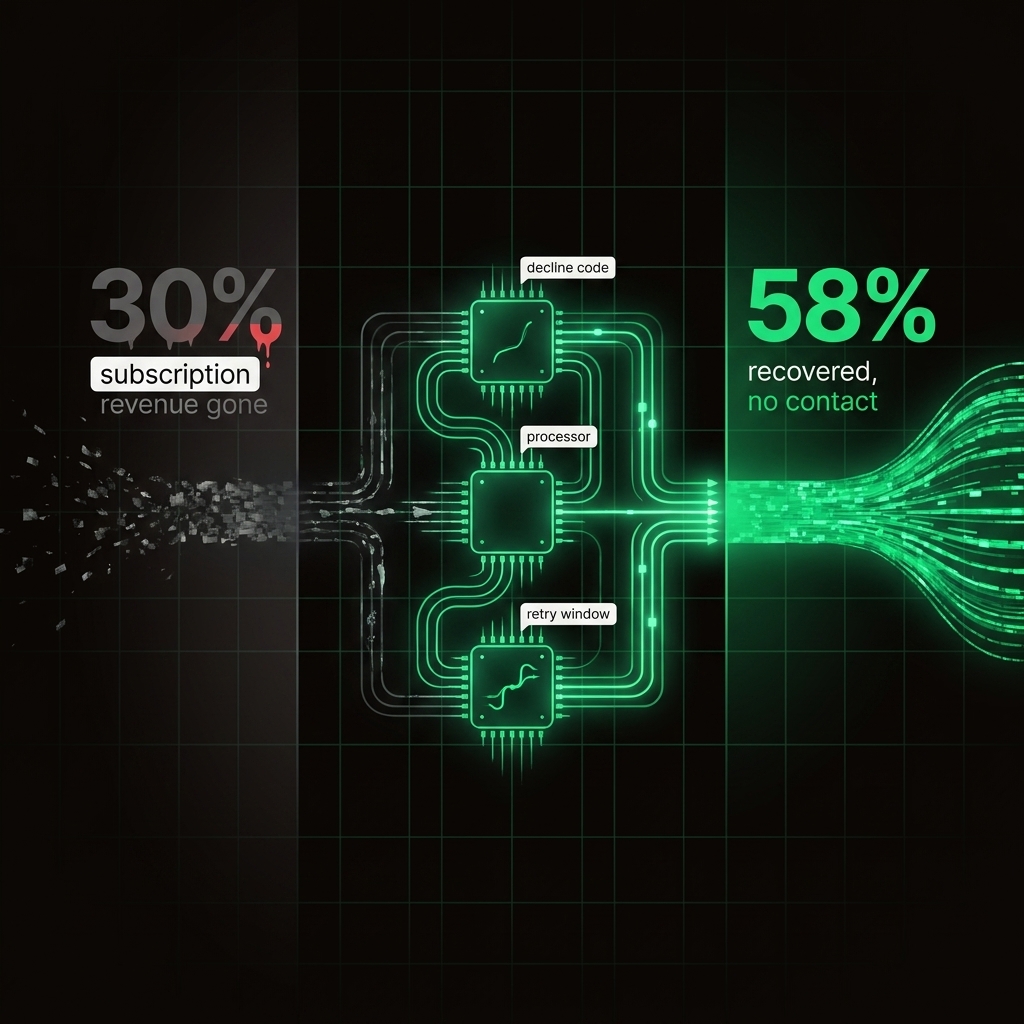

The 3 codes behind 80% of failed rebills:

R01: insufficient funds (timing, retry wins)

R05: do not honor (issuer flag, retry damages the relationship)

R14: account not on file (card update needed, no retry fixes this)

One engine. Three responses. One calendar.

1

1

16

Jun 12

Silent recovery runs AI-native decline-code engines.

Failed payment → decline code parsed → card-specific retry fires → no customer email unless contact improves recovery.

70-80% recovery rate. No cancellation spike from alarming emails.

Sources: finsi.ai, churnbuster.io.

1

1

14

Jun 12

Here's where dunning loses the most.

Decline code R01 (insufficient funds): timing problem. Retry earlier.

Decline code R05 (do not honor): issuer flag. Retry makes it worse.

Dunning sends the same email to both. The card issuer already told you what to do.

1

1

56

Jun 12

Dunning operators run 2020-era tooling.

Failed payment → email sequence → retry on day 3, day 7, day 14.

The mechanism is calendar-based. The decline code is ignored.

20-31% recovery is what you get when every failed payment gets the same response.

1

89