100% Fiduciary Financial Advisor | Retired US Navy Submarine Officer | Guided 100s to financial peace of mind | Helping you avoid investing & life mistakes

Joined August 2019

- Tweets 3,876

- Following 449

- Followers 544

- Likes 2,583

77 Photos and videos

Pinned Tweet

31 May 2022

Seven SIMPLE actions you can do (or stop doing) to IMMEDIATELY LEVEL UP your life.

2

8

68

Why is money important to you? Simple question but definitely not easy. Ask yourself this and get clear. If you're married do it with your spouse. You may realize you both think you want things and you actually don't...

For example: Is money more important to buy healthy food for you and your family or to buy a luxury watch because all your friends bought one? (No right answer and no judgement).

Would you rather have that sports car or a big international trip each year for six years?

Do you actually want to own a home or just think it's a "wise" investment even if you hate doing household maintenance?

You have to get clear before your money will work the best for you.

1

101

I recently asked myself a question:

If someone handed me $100 million right now — but I could never go to Hawaii again — would I take it?

Hell no.

I didn't even have to think about it.

That answer told me more about my own relationship with money than any spreadsheet I've ever built. Hawaii isn't a vacation for me. It's where I remember who I am. No number is worth that.

I ask clients versions of this question before we ever talk about portfolios.

Because if you don't know what you'd say hell no to — you don't actually know what you're building toward.

And I can't help you get somewhere if neither of us knows where that is.

1

80

I've been teaching critical thinking for a while now. It's been long enough that my students now use it against me.

One young lady told me she's started disarming logical fallacies with other adults (including other teachers and parents.)

I feel both successful and terrified.

What is it worth and what does it mean to actually teach someone to think freely in an institution that demands compliance?

2

50

i just trained an AI on every alex hormozi book, playbook, blackbook, and podcast episode...

he charges $5000 for his AI assistant and people pay it, i'm giving you the same thing for free

this isn't some shitty GPT with 3 pages of info that hallucinates answers, NotebookLM is the best AI for consuming and recalling information right now, i fed it EVERYTHING:

- $100M offers, leads, money models

- the black books (given to people who donated 200 books)

- all the playbooks and lost chapters

- his best podcast breakdowns and frameworks

the information inside is worth thousands it can answer ANY business problem using hormozi's exact frameworks

it pulls from the exact books and gives you page-specific answers... no generic advice, no made-up bullshit

i should NEVER be sharing this for free, that's why i'll delete this in 24hrs

reply 'HORMOZI' RT and i'll give you access for free (must follow me so i can dm)

2,749

1,656

3,531

520,924

12 Sep 2025

Most people think consistency comes from motivation.

It doesn’t.

Motivation is unreliable. It fades when you’re tired, busy, or stressed.

Consistency comes from systems and habits.

That’s true in fitness. It’s true in leadership.

And it’s definitely true in your finances.

Build the system or habit → remove the friction → let time do the heavy lifting.

1

5

102

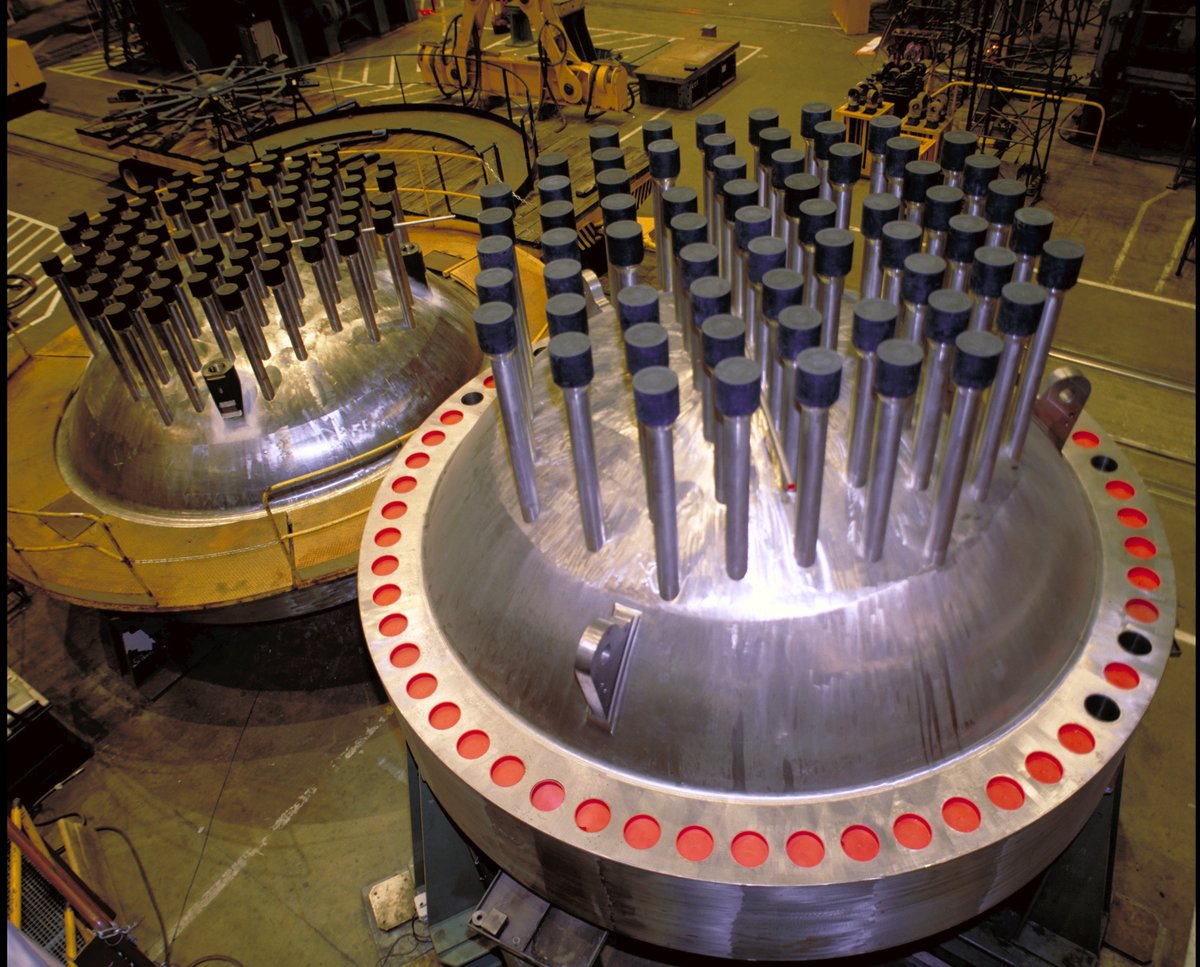

10 Sep 2025

Let's say you're on watch in a submarine’s reactor control space... suddenly lights illuminate and alarms sound. Should you delay the response?

Our nuclear nuclear trained sailors have their immediate actions, procedures, and responses embedded in them as part of their muscle memory and our defense in depth in order to avoid disaster. The stakes are just too high to hesitate.

Your finances are no different.

It feels easier to delay—put off the budget, avoid the portfolio review, kick the decisions down the road. For a moment, the silence feels better than facing the alarms. You may even comfort yourself with "we'll tackle it next month."

But alarms don’t go away. They only get louder. And that haunting feeling in the back of your mind just grows and grows.

The solution? Get the systems solid. Automate what can be automated. Build routines that keep your finances and investments stable—so time becomes your ally, not your enemy. Get a professional to help you get everything running in the background on autopilot.

Don’t wait until your "financial reactor" overheats.

Question: What’s one financial alarm you’ve been ignoring—and when will you (really) face it?

Photo credit to NRC.

1

3

90

4 Sep 2025

When I served on submarines, we had a saying:

“Keep your bearing”

In an environment where a single mistake could risk lives, panic wasn’t an option. Every decision had to be made with clarity, discipline, and long-term thinking—even under intense pressure.

Now, working in investing, I see the same principle play out. Markets get noisy. Headlines scream (and they're always negative). Emotions run high. And yet—the people who succeed are the ones who keep their cool, stick to disciplined processes, and focus on fundamentals rather than noise.

Leadership under pressure isn’t just for the military. It’s the same mindset that protects capital, avoids costly mistakes, and builds trust over time.

What do you do to stay calm when things get volatile?

(Picture is my old boat CCC underway for deployment - I was there).

3

39

27,094

3 Sep 2025

Core (reusable) prompts about yourself really are like magic spells...

4

102

2 Sep 2025

"I knew it all along."

That’s the lie hindsight bias whispers in your ear after every market move. When stocks tank, you convince yourself you saw it coming. (Ever notice how so many people saw the 2008 financial collapse coming but yet they are NOT billionaires?) When stocks soar, you swear you knew they were winners.

Here’s the hard truth: most of us didn’t know. We only rewrite the story later to protect our egos.

This bias is dangerous in investing because it turns uncertainty into false certainty. You stop questioning. You stop learning. Worst of all—you stop preparing for the unexpected. You poison your mind.

On a submarine, you don’t get to say, “I knew the dive would go well.” You plan, drill, brief, and train for every possible failure. Markets deserve the same respect.

Once you believe you’re smarter than uncertainty, you’ve already lost.

Hindsight bias blinds you to risk. It seduces you into overconfidence. And it robs you of the humility every great investor needs.

So what’s the countermeasure? A disciplined process. Document your reasoning before you invest. Write down why you buy and why you sell. Write down your thesis and see if it was right, wrong or partially right. Live and learn. When the storm hits, you’ll see clearly whether you made a sound decision—or whether your memory is playing tricks on you.

You can’t escape uncertainty. But you can fight the illusion of certainty.

Disclaimer: This is for educational purposes only and not investment advice.

1

58

31 Aug 2025

Your retirement plan ultimately won’t be tested in a spreadsheet or even some fancy monte carlo analysis (precise assumptions can yield a result that is precisely wrong...)

It’ll be tested at 2am, when the market is down 30%, and your stomach is turning.

Most people think investing is just about math and optimal solutions. It’s not.

It’s about psychology, discipline, and the ability to keep your head when fear takes the wheel.

The best value you may get from a financial advisor? Keeping you from making the mistakes that could cost years or even decades of financial freedom.

Spreadsheets don’t panic. Humans do.

1

2

91

29 Aug 2025

Rebalancing: The Boring Superpower of “Buy Low, Sell High”

Everyone loves to brag about buying low and selling high. But when the market is bleeding red and fear is screaming in your chest, almost nobody pulls the trigger. Why? Because pain, panic, and greed hijack the wheel.

That’s where rebalancing steps in — discipline in disguise. Your stocks soar? Rebalancing forces you to take some risk off the table. It prevents one area from taking over too much, keeping the portfolio in check while the excitement runs high.

Stocks got crushed? Rebalancing has you buy more, scooping them up at a discount — like grabbing clearance Halloween candy on November 1st. Sweet, if you’ve got the stomach. If you love a company at $100 then it's even better when it's 40% off for the claim to the SAME cash flows.

It feels wrong in the moment — but that’s the point. Discipline always feels like swimming upstream.

Rebalancing isn’t flashy, but it quietly forces you to do the very thing everyone brags about: buy low, sell high.

Disclaimer: This content is provided for educational purposes only and should not be considered financial advice.

1

73

27 Aug 2025

Ever notice how every win feels like genius… and every loss gets blamed on “bad luck”?

That’s self-attribution error — one of the most dangerous blind spots in investing.

When markets rise and your portfolio grows, it’s tempting to pat yourself on the back: “I knew it all along.” But when markets fall, suddenly it’s the Fed, inflation, or “those idiots on Wall Street.” The danger? You learn nothing. You claim credit for the tailwinds… and dodge responsibility for the storms.

In the military we had a saying every mistake has your name on it, even if you don't "pull the trigger." That mindset forced us to own the outcome — to adapt, improve, and survive. Even if I was only 20% at fault, that was still 20% I could control and correct.

Investors who ignore self-attribution error fall into a cycle: overconfident after wins, reckless on the next move, and blind to the lessons hidden in losses.

The challenge for you:

Next time you review your portfolio, ask yourself was that success skill… or just a strong tailwind? (Both? Neither?) Was that failure really bad luck… or a poor decision I can fix?

Intellectual honesty is the sharpest weapon in an investor’s arsenal.

Disclaimer: This post is for educational purposes only and not financial advice. Investing in equities and other securities involves risk, including the potential loss of principal. Always seek guidance from a qualified financial professional before investing.

74

26 Aug 2025

Would you buy a stock at $100?

What about the same stock at $80?

Feels like a deal, right?

That’s anchoring bias messing with your brain.

The first number you see becomes your reference point—even if it has nothing to do with the company’s real value.

The same trick happens at the store: “Was $299, now $199.” It feels like savings, but maybe you just got played.

In both investing and spending, anchors quietly steer our choices. And here’s the kicker: once you spot it, you’ll start seeing anchors everywhere.

Next time ask yourself:

“If I didn’t know the ‘before’ price, would I still see this as worth it?”

Where have you seen anchoring bias hit you hardest—investing, shopping, or somewhere else?

2

61

24 Aug 2025

You worked your butt off. You saved diligently.

You invested wisely.

You did everything right for 30 years…

…and your retirement could still get wrecked if the first few years go wrong.

That’s the danger of sequence of returns risk.

Two retirees, same savings, same market, same “average return”:

Jan hits strong markets early → retires comfortably.

Dave hits a downturn early → forced to sell at a loss → wealth never recovers.

Same averages. Very different outcomes.

It’s not about beating the market. It’s about surviving the order of returns in those critical early years.

That’s why your withdrawal strategy, cash reserves, and risk controls in the first 5–10 years of retirement are absolutely critical.

Have you thought about what happens if the market tanks right after your last day of work?

58

23 Aug 2025

📘 If your annuity reads like a financial derivatives textbook…

…it’s probably not built for you.

Insurance companies aren’t charities. Complexity in contracts usually hides:

High costs

Big commissions

Painful surrender penalties

Agents deserve to be paid — but you deserve transparency. Always ask:

How much of this goes to commissions?

Why does this product need to be so complex?

If the answers aren’t simple, neither is the motive.

52

21 Aug 2025

Some fortunes are made by betting big on a single stock… but many retirements are ruined the same way.

Take $META (Facebook) over the last 5 years. This is a mature company with a strong brand and balance sheet. Yet look at the ride:

🚀 Huge run-up

📉 A 75% collapse in 2022

📈 Nearly a 10x rebound from its low

If you held through that, congratulations. But that’s not genius — that’s stomach, discipline, and almost certainly some luck.

Concentrated positions can pay off. But they demand nerves of steel, perfect timing, and the ability to watch years of gains vanish (on paper) without bailing. Human psychology works against us here: the urge is to sell right before the recovery.

For most people, having their future tied to one or two companies isn’t worth the risk. Diversification may be boring, but boring is what helps you stay wealthy once you get there.

Are you overconcentrated in any stocks today?

1

1

76

21 Aug 2025

I love working with people who take charge of their own finances. The discipline, the curiosity, the willingness to learn — it’s admirable. Some DIY investors even outperform the pros. I was one of them for many years, and I can talk shop with DIYers for hours.

But here’s the question I always ask:

What happens if you die suddenly, or become incapacitated?

Are your loved ones as enthusiastic about DIY investing as you? Will they really want to rebalance portfolios or stress over markets during the hardest moment of their lives?

Too often, spouses don’t even know the family’s full financial plan. That can leave the people you love most vulnerable to confusion, mistakes, or even scams when they’re already grieving.

DIYers work hard to build wealth. A fiduciary on retainer can quietly follow your finances in the background and be ready to step in, protect your legacy, and guide your family if tragedy strikes.

A great plan is only great if it can survive you.

1

50

29 Mar 2025

People just don’t get it. Even people who use it don’t get it.

1

5

154

22 Mar 2025

75 days ago, this was just a goal.

Now it’s a reminder of what consistent effort can do.

No shortcuts. No magic. Just discipline and grace for the days I almost broke.

75 Hard 2025 in the bag 😎

5

139