I own assets & chill. Investor in grid enhancing technologies. Prototypes are easy, production is hard ⚡️🔋

Joined May 2021

- Tweets 13,019

- Following 281

- Followers 1,409

- Likes 20,280

1,125 Photos and videos

Pinned Tweet

May 3

$EOSE 🧵

Was at a bach party this wknd and coincidentally sat next to someone very interesting in the casino… friend on the trip who worked for a PE firm specializing in financing renewable energy projects…. (with connects to Eos gen2.3)

I know lots of folks are upset with the q4 miss and relative quiet on the order front but let me bring up a few things nobody ever talks about.

Before a single Eos batt gets installed.. the developer buying it has to close project financing. This means getting a senior lender, a tax equity investor, and an offtake agreement all lined up simultaneously.

Every party does their own DD and anyone can kill the deal.

Here's who has a say before a project closes: Senior lender sizes the loan to contracted cash flows, tax equity investor claiming the federal tax credit, independent engineers certifying the tech works, offtaker signs l/term capacity agreement, insurer provider wraps project.

Everyone has to be comfortable. Independently.

The federal tax piece alone is huge.. under the IRA BESS projects can qualify for the 30-40% ITC depending on location domestic content

On a $60M project..thats about $24M claimed in year1. The feds are funding nearly half a project on day1. That’s why it gets built.

The operational cash flows alone don’t justify it. The tax benefits are the engine.

Here's the catch..a tax equity investor will only participate if it’s certified by an independent Engineer.. engineers review field performance, OEMs balance sheet, warranty terms, chemistry etc… then sign off.

That’s the price of admission.. without it.. you wont close.

This is why the “eos tech doesn’t work” has a logical problem.

Mn8 energy is GS backed. The supply agreement is for 750mwh. They have institutional LPs, their own lenders, and a rigoruous DD process… goldman backed firms do not stake their reputation capital on tech they think has no chance to be bankable.

Same with talen.. a $17B IPP. They would not put their CEO name in a PR for tech they don’t believe in IMO.

Talens play is pairing eos w existing generation in PA to serve AI DC. They have the land, the interconnection, and the hyperscaler relationships.

Doesn’t sound like a favor… it’s a calculated infra bet.

And then you have frontier power. UK developer that submitted Eos tech to OFGEM.. the UK regulator in a competitive bid for the cap n floor program. 11Gwh of projects to round two using Eos tech.

Under the program.. ofgem provides a rev floor..essentially the govt backstops the cash flow the lender will underwrite against

The 228mwh firm order isn’t just a sale. It makes eos look much more viable since it’s being considered within regulated lender-backed frameworks …

NYSERDA plays a similar role domestically.. when NYSERDA selects its tech thru competitive solicitation.. it backstops revs that senior lenders will underwrite against…

A govt backed offtake is the cleanest credit in project finance… that is in our pipeline.. 🔑

So why is conversion so slow?

Maybe bc the chain I just described – lender approval, tax equity, independent engineer certification, offtake, insurance can take 12-24 months from contract signing to commercial operation .. then layer in first of a kind BESS chemistry that has never been financed or deployed at scale… 🤔

These counterparties engaging tells me the tech has cleared initial DD hurdles, but scaling risk remains

Nobody signs a 750mwh as a favor.

Cerbs involvement likely improves access to financing counterparties.. but execution risk still exists. But adding a 3rd BOD member isnt a move you make from a company you are about to walk away from.

Talented finance execs tend to do DD before joining as well.

The risks are real. Mfg execution, runway, order conversion- not dismissing any of it. But the project finance complexities are under appreicated. Just trying to close that gap.

20

12

177

32,686

$EOSE

Frustrating.. yes. Not the end of the world.

Projects will be lost delayed.. it’s just part of the game.

Eos as an investment continues to be extremely binary. Been waiting on one domino to fall for quite awhile… 👀

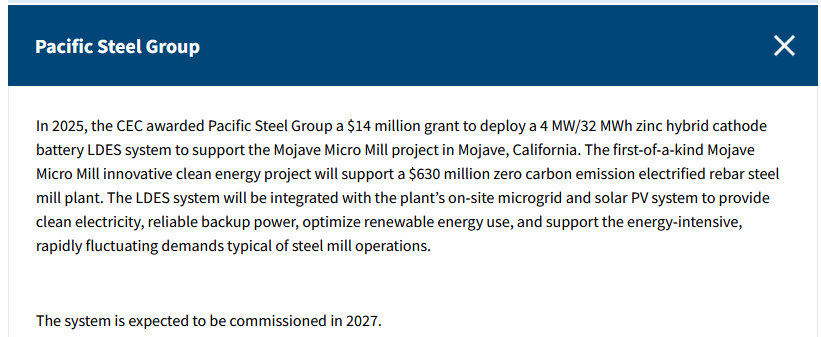

$EOSE @PoweredByEos would you care to explain what happened to the Pacific Steel project?

irtools.co.uk/88/story/e06ae…

6

23

3,004

JordanSolace retweeted

22 Dec 2013

I just want to be successful thats all..

637

12,297

62,558

Jun 14

The Jets of basketball no longer.

Kings of the castle 👑

Congrats #knick fans

All those years.. painful years. Finally worth it 👏

New York x Empire State of Mind -Extended Version youtu.be/i6HP81dJoHk?is=KIXx… via @YouTube

446

Jun 12

Not only this… but just think about all the spacex money that will flow into the economy… bars, restaurants, travel, materials etc

Shit will be next level

2

10

1,917

Jun 12

$SPCX

Ideally wanna see this thing close up 15-35%.. anywhere below that.

Do not want to see spcx up north of 60/70% on day one.

The latter is likely what will see though. Who the hell knows

2

1

781

Jun 11

$EOSE $CSIQ

AI bottleneck is still electricity.. but the invoice shock could be real…

Tokenomics 🧵

$NVDA Blackwell vs hopper…

65x more tokens/sec per GPU, 50x more tokens per MW, and the cost per million is 35x cheaper

Intelligence is collapsing in price.

Cheaper tokens do not reduce power demand but they actually recruit more…

At $4per M tokens the AI consultant is used more sparingly but at .12/M its tap water.

Agents will be looping, reasoning models burning 50k thinking per query, and AI running on everything.

Jevons paradox in real time.

But Efficiency will save the grid! Not necessarily.

First: the FLEET lags the frontier. Rubin specs do not matter when data centers are full of hoppers and a100s running for another 4-6yrs.

Fleet avg will improve much slower than the spec sheet.

Two: The systems around chips are getting hungrier.

Rack power has gone from 15kW to 135kW to 600kW planned for rubin. 40x in a decade.

And the Datacenter PUE has been flat since 2015. The efficiency was harvested years ago. 🔑 🔑

That’s why IEA, Goldman, BNEF all still see data center demand doubling even though the chips have gotten WAY more efficient. … even tripling in demand going out to 2030s

Now the supply side… transformer lead times are abut 3yrs and getting longer, the US interconnect queue is 2x the size of the grid right now.. and average wait times could be north of 5yrs

There is a massive gap between what Data centers need and what actually gets built by 2028… lets call it a ~20GW gap

Meanwhile China sees this and invest in their transformers and has 40% of the grid being under 10yrs old when the US has half the lines >20yrs old

The US is doing an AI build out on an Reagan era grid..

Nvda also sees this.. they are basically redesigning the data centers around the transformer shortage replacing the multi stage AC distribution with a VDC backbone and batteries

The demand? Anthropic data shows AI usage concentrated in coding, engineering, law, etc.. while food service, construction, agricultural and many other sectors lag.

Theoretical capability > observed usage is almost everywhere. Huge backlog. And we dont even have robots yet … 🔑

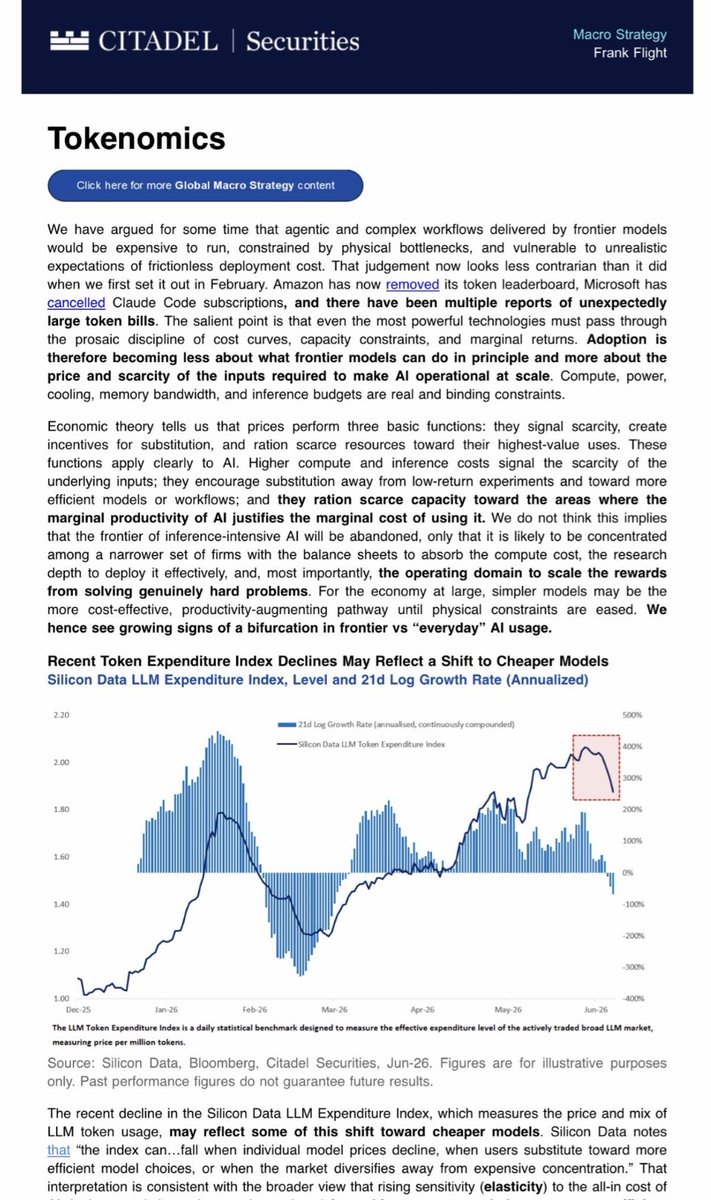

Now the tokenomics note… from citadel

Companies seem to be shocked by the bill they are paying for tokens. Msft cancelled Claude code subs and amzn pulled its token leaderboard

The deploy AI without looking at the bill era may be ending .

Citadel’s chart- LLM spend per token doubled Dec25 to Jun26 as everyone rushed to expensive reasoning models… then rolled over hard.

Growth swung from 400% annualized to negative in weeks

But the ambiguity is that index is measured in dollars not tokens…

A falling index = demand saturating… OR usage exploding while everyone substitutes to cheaper models that got good enough.

Less flying vs cheaper flying. The chart alone can’t tell you which.

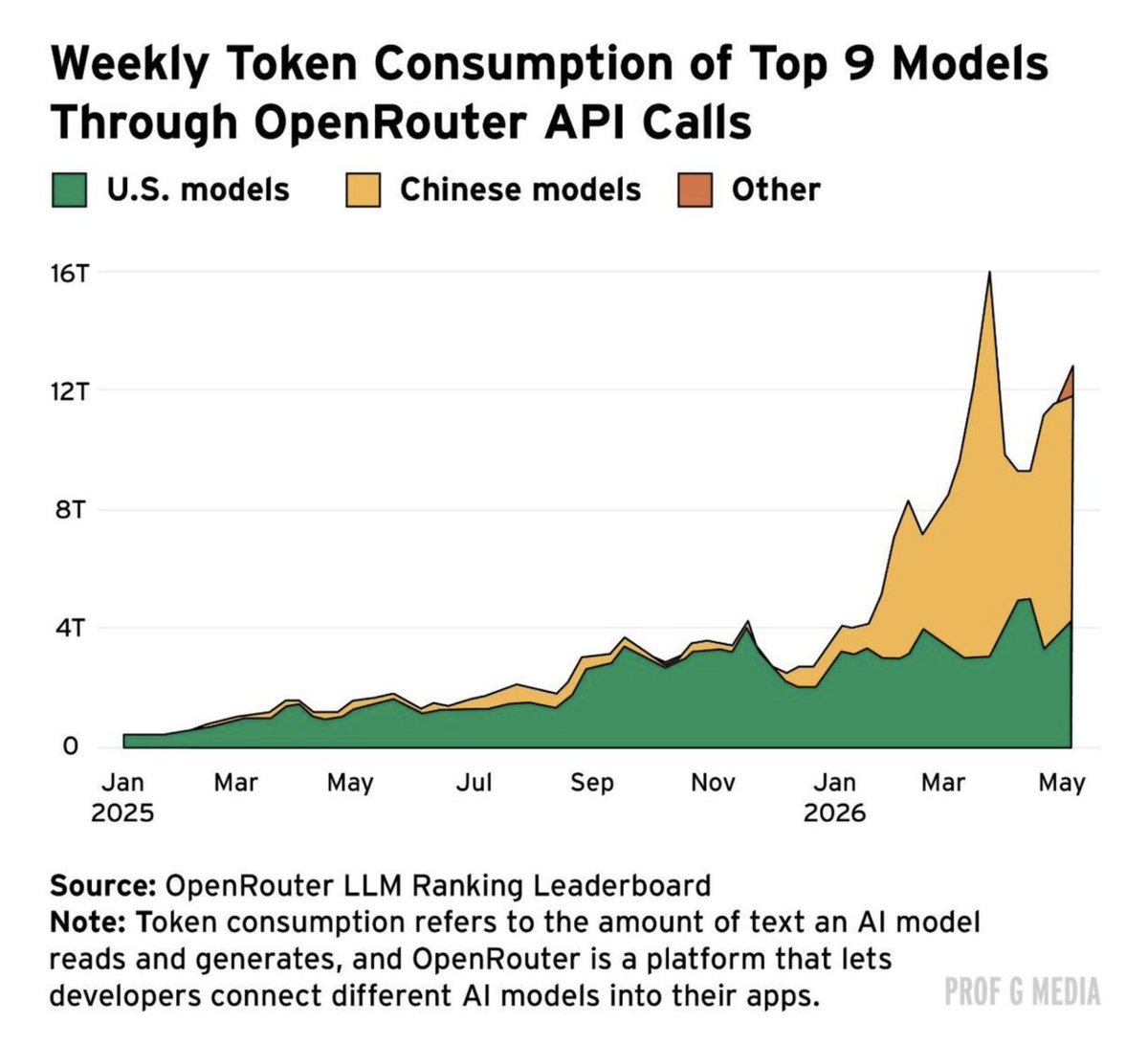

The volume data leans one way:

OpenRouter throughput grew ~4x YoY to 20T tokens/WEEK by April 2026- during the exact period spending wobbled.

Agentic coding tasks average 1-3.5M tokens each.

That’s substitution- not saturation.

The variable to watch isn’t volume or efficiency alone but it’s the ratio

Power demand = tokens / fleet efficiency

As long as volume grows faster than fleet efficiency improves demand will keep climbing no matter how the headlines frame it

So you can think about it two ways..

1- own the power bottleneck

2- expect a fork in the road bc frontier demand will be price elastic and many will just shift to cheaper models bc they are sensitive to price

Both can be right… frontier spend can slow while the tokens and megawatts compound

The thesis only breaks if the models plateau or the backlog runs dry in terms of AI use cases

But with agents barely deployed and robots not even here yet… I don’t think we are close

Watching token volume closely and hyperscaler token disclosures

Jun 10

Citadel dropping a "Tokenomics" piece with lots of common sense in it:

"Adoption is therefore becoming less about what frontier models can do in principle and more about the price and scarcity of the inputs required to make AI operational at scale. Compute, power, cooling, memory bandwidth, and inference budgets are real and binding constraints".

We've had every mayor AI CEO warning about this for over a year. The bottleneck is now real-world infrastructure buildout.

Time to unleash US' inventiveness into building out power infrastructure and manufacturing. Otherwise, China will just leave us behind and the world will be running on their models...

BTM ultra-expensive data centers are not gonna cut it imo... Time to expand the grid and add cheap renewables to the mix, otherwise we will not be competitive long term.

2

1

20

2,491

JordanSolace retweeted

Jun 11

On June 4th I posted “Coming into today, I was concerned over the increasing near-term bubble like behavior in the which the SOXX was up a staggering 95% from the market closing lows on March 30th through yesterday June 3rd which drove a 19% rally in the S&P.” There were numerous signs of near-term froth and I believed they would need to be worked off.

However, coming into today, the morning of June 11th, the S&P is now down 4.5% from its recent closing high while the SOXX is down 12.3%. While the SpaceX IPO tomorrow in which a staggering ~$75B will be raised in the largest IPO in history may cause some of their large cap peers to be sold, I think that should be the final negative catalyst in the near-term.

I also wrote on June 4th, “I remain bullish over the long-term given 1) S&P earnings are expected to increase 25% this year driven by the advent of Agentic AI, 2) I believe oil prices will come down, and 3) new Fed Chairman Warsh is likely to push back against calls to raise rates.”

$ORCL results last night once again pointed out how the spending on AI continues driven by the token generation required by Agentic. Capex was guided to $90-95B including pre-payments for FY27 from $56B in FY26. While not good for Oracle cash flows or their hyperscale competitors which are locked in a capex war, it is great for the beneficiaries of that spend in semiconductors. I believe starting to add back positions in this sector once again makes sense and that the sell-off in the overall market is near an end.

I believe this is the pause that refreshes.

39

52

570

49,964

Jun 10

$EOSE

Acknowledging the choppiness.. the challenging PA lately.. Spacex IPO supply, other equity raises, potential momo rotation, macro headwinds (Iran/rates)

I’m reducing names and adding cash & to high conviction positions… Eos is one of them

The core bet: Eos books an anchor order by Q3 call. Exit Q2 on a $300m run rate w zero production from L2 & continue making margin progress

With a 4gwh nameplate I don’t see how they keep a backlog under $1B

Apply whatever multiple you want to sales, margins (if they exist or not), EBITDA (negative/0/ ) … the delta between what I think happens, the sell side, and broad mkt sentiment is drifting very wide again

Anchoring too:

Form 4s above mkt price

Felt increases - directional indicator of factory utilization (it’s not zero)

AG insurance

New CFO

The multiples assigns to comps

Cerbs equity contribution to FPusa

Cerb lockup to year end 🔑

Don’t see Cerb exiting before year 3 with 3 seats on BoD and more entanglement post FPusa. Continued lockup tells you where the conviction is…

Am I spooked by 800M shares.

No.

800 authorized doesn’t equal 600 FD which doesn’t equal the current outstanding float ~330m

Until the day when the current float equals the FD count the mkt may give you the chance to exit at valuations that make no sense based on the FD count.

Especially in this mkt environment we live in today.

The delta between current outstanding shares & FD might exist for a long time anyway.

The mkt is nowhere near pricing eos for what it can become… at $1B in revs with $45kwh ptc/itc

$200 ASP

$150 COGS

$200M in opex

30x EBITDA multiple your north of $15

Fully diluted

On 4 lines $2B same math. Same credit. Same opex growth rate you are north of $30

It is as binary yesterday. Still binary today.

Takes one PR to change narrative.

6

11

121

6,992

Jun 5

$EOSE

Keep in mind.. a rights offering is fundamentally different and much more complex than a standard offering from an IB

That shit is boilerplate.. banks have set templates and can turn it around in 48hrs price it overnight. Done.

With the RO… you need a record date, subscription date, convert ratios, over subscription terms

Dealer mgmt, rights transferability and trading mechanics on the exchange

What happens to unexercised rights that are ITM.. ?

Got to get it set up at every broker. DTC clearinghouses .. FINRA approving comp structure for dealers etc. SEC review takes longer bc of unique structure

Point is… shit is much more challenging & complex and all bc Eos wants shareholders to be involved… and be able to exchange rights as well

This will take time.

Having said that the team should be working 18 hours days. Get it done

2

43

3,367

Jun 4

Agree with a lot of this

In order to get wealthy you need to be an entrepreneur & take concentrated bets

To stay wealthy… you need to leverage global macro hfs & diversify.

His point on liquid alts > privates… something I’ve come to agree with in recent years

1

3

1,443

Jun 3

$BRKB $GOOG

Another signal.. AI capex cycle isn’t currently 99.

Berkshire putting $10b in Goog at a 6% discount to the mkt. Not a rescue, distressed deal, but near mkt on a company trading > 5yr avg.

Brkb doesn’t do hype. It does cash flows.

The most conservative capital allocator of our time (granted we need to get a feel for Abel’s risk tolerance relative to Warren) blesses the AI infra buildout is another stamp…

And from googs POV- first equity raise since 05. A company that prints cash decided the AI buildout is moving to fast to self fund.

The $80b raise isn’t a sign of weakness.. it signals the opportunity is larger than the ability to capture with current cash flows

When goog needs outside capitals it probably means we have more legs & the cycle isnt imminently ending…

May 30

$SPY ☕️

My am thoughts on the US Equity mkts.

Everyone calling this an AI bubble has the same problem: they’re using 2000 as the only template. I think that misses the bigger point.

This mkt has bubble like pockets/sideshows, no doubt. But at the index level, this looks much more like a cash flow funded capex cycle confirmed by earnings than a 2000 equity funded speculation cycle.

🧵 on why equities go higher from here and what the real risks are…

Capex argument: In 2000, corporate America was spending 3-4x FCF on capex. Today- outside the hyperscalers were under 1x. This isn’t an equity funded speculation. It’s cash flow funded investment that has taken place so far… it’s been accretive to earnings.

That’s not the classic 2000 bubble setup. 🔑

The data displays capex broadening…Capex started a tech story, but it is becoming more diffuse across the index. That matters because real investment cycles broaden earnings in a way that buyback led cycles do not. Critics used to call buybacks lazy.. now they call capex dangerous? The goal post will always move in a bull mkt.

Margins: One of the most underappreciated charts in this mkt is the unit labor cost in nonfarm business sector (ULC). The growth rate of ULC has collapsed and is in bottom quartile when we look at this metric over its history… a very favorable non recessionary read in the last ~50yrs.

For much of corporate America, labor is the biggest cost. When it’s contained alongside 3% inflation and positive GDP.. margins do not just hold… they expand…

Earnings… the key to everything. They are real broadening. The SP 493 earning growth was 10.5% in mid April and is now revised up to 17.5% by end of May. Equal weight earnings are finally growing post the 3yr contraction clip from 2022-2024. The last few quarters go to show how a narrow AI trade can start broadening out…Small cap earnings in energy, financials, materials & real estate are inflecting after a ~3yr period of contracting.

Semis.. They are not cisco.

The $CSCO $NVDA comparison doesn’t hold.

Cisco built fiber that sat dark for years waiting on demand that didn’t exist.

Todays compute is being consumed immediately… we are short compute relative to demand.. 🔑 not future hoped for demand. $NVDA trades at 25x NTM growing revs 85-95% YoY. $AAPL trades at 30x growing closer to zero.

Semis can correct. IPOs can be insane. Some AI proxies for private co’s will have deep corrections. That does not equal a 50% index crash.

And look at $SOXX …

Price performance has lagged earnings growth. When you buy a sector up 100% and its earnings have grown faster than price.. history says that asset outperforms over the next 12 months 2/3rds of the time going back to the 60s

The duration of the chip cycle may be extending from 3yrs to 7…the sell side is always structurally behind… semi estimates are always too low on the way up and always to high on the way down. Always… 💯

The Fed… They aren’t the enemy here.

Here is what people miss. Oil shocks historically make the fed less likely to hike.. not more. Less likely is not absolute…

Since the 1980s, oil driven spikes have not passed through to core inflation the vast majority of the time.

Core cpi ex shelter was 2.3% YoY in April.

Shelter is a supply problem.. you don’t fix a supply shock by raising rates. Yes.. durable goods orders are in the top quartile of their historic range and a hike could come later this yr.. historically that setup correlates with a ~65% probability of a hike.. but ask the question.

Do we care? A fed hike driven by durable goods is a growth confirmation hike.

Equity mkts will brush that off. It’s the inflation panic hike that kills mkts. 3-4% inflation with positive GDP and the 10yr appropriately priced for growth?

Honestly sounds like the sweet spot.

Inflation above 4.5% is when you worry. Not here.

1

7

1,144

Jun 2

$EOSE

Just wanted to point out a *potential* pattern given the Cerb involvement…

A setup…

June24/24-> Cerb closes eos deal when the stock is ~$1

Distressed spac play with institutional money just starting to underwrite the thesis

Over the next twelve months- Eos grinds from $1 to $7. Not a moonshot but a slow deliberate accumulation phase.

Cerb not flipping.. building with Eos and giving them breaks on covs.. 🔑

Adding BOD members…

June 16/2025-> Cerb comes back with the first refi & convert deal. And then locks up the shares for another year…

You don’t lock up if you believe what is coming is worth more than your exit. 🔑

What followed?

Eos goes from $6.50 to $18 in the following ~120 days.

Lockup wasn’t a footnote.. maybe it was the signal

Q4 2025-> stock sells off hard. Bears are vindicated. But the sell off is not structural

Idiosyncratic execution issues, lack of redundancy, and software integration challenges. All of which have been resolved or have drastically been improving

Cerb doesn’t flinch.

May13/26 they lock up again until year end.

Third time they have formalized there commitment. $8.70 well off peak.

Every time Cerb has signed on the dotted line the stock has trended materially higher. 👀

Sophisticated capital with full access to info continues to stay fully locked in.

Q4 selloff shook out weak hands. Operational & execution issues are real but likely temporary.

Battery storage thesis intact.

Cerb just told you again where they think this is going.

I’m not here to tell you what to do.

But when the same institutional partner with a full view of the books voluntarily restricts their own liquidity three separate times, that’s a data point worth noticing…

3

7

122

6,140

Jun 2

$EOSE New whitepaper.. ☕️

Basically says the quiet part out loud. The battery is no longer the “hard part” of energy storage. The hard part is everything else

Tax equity delays, missed ITC bonuses… interconnect restudies that push first cycle 6-9 months.

These risk are eroding project returns.. and they are operational not technical

Sophisticated storage buyers aren’t just buying equipment.. they need to think like energy infra owners. Obsess over the finance structure, tax optimization and 20yr O&M economics

Eos response 🔑

Restructure around the project lifecycle not the product…

Delivery, mfg, field ops all report to COO. The goal is to catch risk before they even hit the factory floor so they say…

Eos highlights a recent install that went from factory to fully commissioned in 5 weeks.. they claim it’s about half the time relative to other tech out there.

Pretty crazy imo

I like the part about borrowing from cross industry disciplines.. my current firm does a ton of that and we have been growing like wildfire… the new hires bring a diverse set of experiences & fresh ideas that have helped. 👍

The bigger trend this points to as storage scales is this… the competitive moat is shifting from chemistry to execution

Who can compress time to revs, navigate tax structures, and run a 20yr service relationship

Investors need to start asking questions like what is your time to first cycle, what’s driving it… that’ll tell you a lot about how mature the organization is… not just the tech

4

6

76

5,911

Jun 1

$EOSE

The AI trade started with chips.. value is beginning & will continue to flow down the stack

Compute is still the obvious bottleneck.

Power is the next one.

$FLNC just got embedded in the $NVDA/siemens factory blueprint which is huge… 👏

They have hyperscaler contracts coming..

Eose should be reading the same script.

Zinc is insurable and cycling daily at Viejas. Maybe even twice (dual discharge)

The terminal value of the power bottleneck is massively underpriced.

2

2

55

4,138