I make big holes to get shiny rocks. From Barcelona to Vancouver 🇨🇦

Joined November 2019

- Tweets 2,959

- Following 528

- Followers 1,914

- Likes 4,432

433 Photos and videos

Pinned Tweet

1 Jun 2025

Of course that’s your contention. You just finished The Big Score, think copper porphyries are a cheat code, and you’re tweeting NPV models like they’re gospel.

Right now, it’s all about "grade-tonnage curves," "cut-off grades," and “strip ratios”… you even printed out a JORC checklist.

Next month, you’ll discover tungsten in Nevada and start saying things like “it’s not about price, it’s about supply chain security” at the bar.

By fall, you’ll YOLO into a junior gold explorer in Alaska, seeing the multi million ounce resource at 2g/t, and forget it’s refractory and sits under a glacier, you’ll tell your buddies thinking you’ve outsmarted Newmont’s geologists.

Next year, you’ll be at a sketchy mining conference in Vancouver, shilling a zinc project with a 7-year mine life and no permits, calling it “a generational buy.”

You’ll throw around “mispriced upside” for a company that hasn’t hit guidance since the 2011 commodities boom.

You haven’t even begun to suffer yet.

You haven’t bought into a “world-class discovery” that turned out to be a twinned drill hole hyped by a shady promo firm, with millions of founders shares issued at a fraction of a penny.

You haven’t emailed IR about a delayed 43-101 report five times, got ghosted, and still averaged down out of pure spite.

You haven’t stared at a flow sheet so long you start muttering “Merril-Crowe” in your sleep.

You think this is about numbers.

It’s not.

It’s about pain tolerance.

Come back when you’ve held a micro-cap explorer for five years, survived two reverse splits, and still called it a win.

Then we’ll talk geo-alpha and investing in Lundin group companies

30 May 2025

Of course that’s your contention. You’re a first-year deep value investor.

You just finished The Intelligent Investor, think net-nets are a cheat code, and you’re tweeting P/B ratios like they’re scripture.

Right now, it’s all about Ben Graham, "margin of safety," "cigar butts," you even printed out a checklist.

Next month, you’ll discover Klarman and start saying things like “risk is not volatility” in casual conversation.

By fall, you’ll hit Greenblatt, run a Magic Formula screen, and convince yourself you’ve reverse-engineered Buffett’s brain.

Next year, you’ll be at an obscure value conference in Omaha, pitching a furniture liquidation business with asbestos liabilities and calling it “unloved but cash rich.”

You’ll use terms like “mispriced optionality” to describe a company that hasn’t turned a profit since 1998.

You haven’t even begun to suffer yet.

You haven’t held a 0.4x book stock that got delisted to the Expert Market and now trades by appointment only.

You haven’t emailed IR five times with no response and still doubled your position out of spite.

You haven’t stared at a balance sheet so long you start dreaming in GAAP.

You think this is about numbers.

It’s not.

It’s about pain tolerance.

Come back when you’ve held garbage for five years, been diluted twice, and still called it a win.

Then we’ll talk deep value.

17

24

214

49,819

May 13

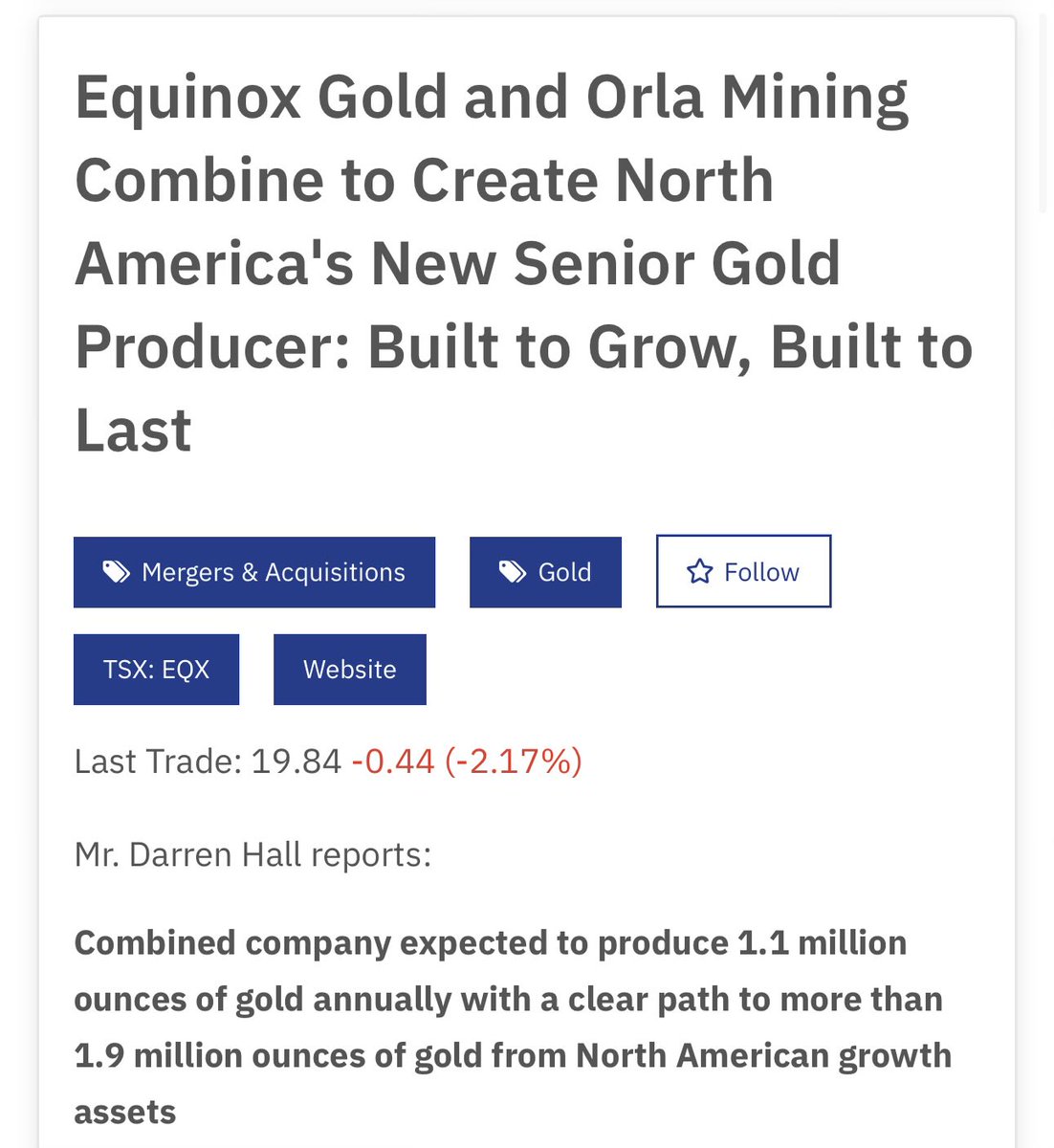

If I had to guess the next Equinox $EQX transaction will be them taking over Gold Candle after it IPOs 🔮

Keeps the narrative of a growing Canadian (and North American now with Orla) producer.

Beaty and Lassonde already in both tickets.

And they’ll grow their exposure to EQX.

May 13

At this pace Ross Beaty will manage to be Chair Emeritus of the largest gold company in the world… all while share price is the same as when gold was 2000$/oz in 2020

But who cares about share price… MCap and ETF flows is all that matter bruhh

3

13

3,304

May 13

At this pace Ross Beaty will manage to be Chair Emeritus of the largest gold company in the world… all while share price is the same as when gold was 2000$/oz in 2020

But who cares about share price… MCap and ETF flows is all that matter bruhh

6 Jun 2025

It's 2035.

Gold is at 15,000$/oz.

EQX has aquired Newmont, Barrick and Agnico, and a bunch of mid-tiers.

It manages 127 mines, barely making a profit.

EQX is 90% of the GDX and GDXJ.

EQX share count is 5 billion shares.

The share price keeps bumping against 10cad/sh.

6

1

42

7,768

Mar 19

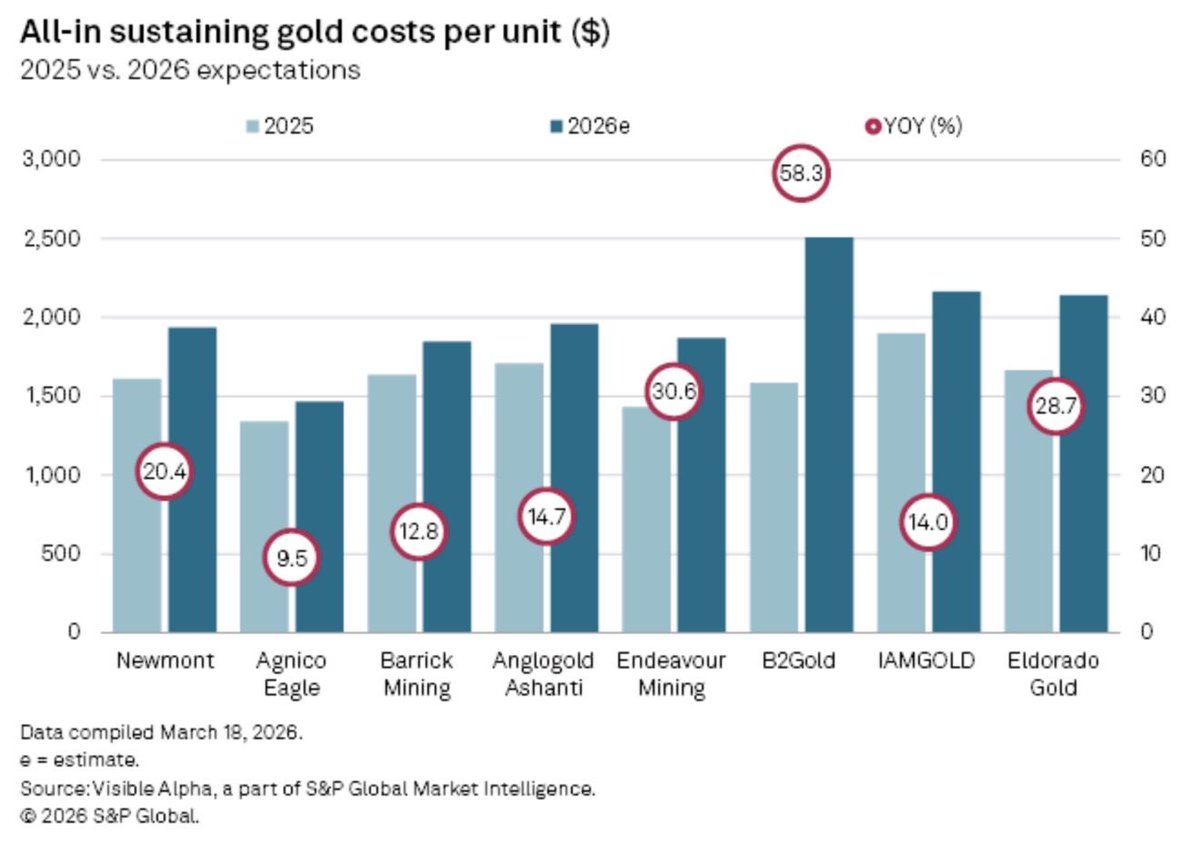

Just a note on rising AISC:

C1/AISC always go up in a rising price enviro. And this doesn’t have to mean inflation. Why is that?

Miners will run reserves at a higher metal price in the following year after a substantial price increase (like that of last year and this year) 1/3

AISC for the top #Gold miners were trending up even before the current oil price shock. Here’s a chart from CapIQ showing 2026 estimates before accounting for the recent oil price volatility.

Gold prices realized in Q1 will be above the average realized price of $4,200 for Q4. Q1 results will be fine but markets looking beyond that. Margins are compressing without higher gold or lower oil and estimates starting to get cut beyond Q1 w/Q/Q roc going negative. Have margins peaked this cycle? Or just temporary blip?

Damage done already. $GDX before today’s open is still up ~2% ytd. As of now, down 7% pre market.

🚜⚒️🌎🥇

1

11

1,044

Mar 19

Running mine plans at a ⬆️price means bringing in metal units that weren’t economic before, thus lowering your avg grade, and ⬆️your production cost *per metal unit* aka C1/AISC.

This doesn’t necessarily have to mean that your production cost per rock unit ($/t) had gone up

1

8

451

Mar 19

Caveat: the increase in input costs we’re seeing now will definitely cause an increase in production costs per rock unit. Not necessarily until now though.

7

365

Feb 6

Sophisticated GlenTinto commentary from the depths of MinTwit

1

1

21

5,341

Feb 4

Oh look at you Magino, all grown up. I barely recognize you from that summer of 2022.

Just don’t let Ausenco build you this time or the 1B$ in NPV lift might end up vanishing in the air.

Alamos Gold Announces Island Gold District Expansion to 20,000 TPD, Creating One of Canada’s Largest and Lowest Cost Gold Mines with Attractive Economics, including 69% After-Tax IRR and $12.2 Billion NPV at $4,500/oz Gold $AGI.TO tinyurl.com/2558zsle

2

14

2,780

Jan 16

I’ll sure be wrong on this, but I feel we dump to 5.50-5.40 before 6.25$ (both are at the same distance from current price). We’ve seen 3 ATH with declining strength over the last 2 weeks.

If we do, I’ll load up. I’d wish to load around 5.20 though.

#copper

3

13

1,568

13 Dec 2025

Forgot to say this yesterday, happy 40$ to all those who celebrate! 🥳

$GMIN.to

GMIN has overtaken ARTG’s MCap. Crazy to see it close to 9B$ in MCap, still remember when it was a sub 200M$ junior.

The value that is created by building mines (and gold going up 140% 🙄)

Time for ARTG to play catch up.

6 Oct 2025

$GMIN.to officially a 10x since my first tweet. (11x really but who's counting🥸).

Still holding 70% of the shares I've ever bought of the company.

Feeling good in a gold bull and one of the best teams executing.

h/t to @ManelMolina11 for putting it in my radar in Jan-Feb 2022

1

19

2,513

Jordi retweeted

8 Dec 2025

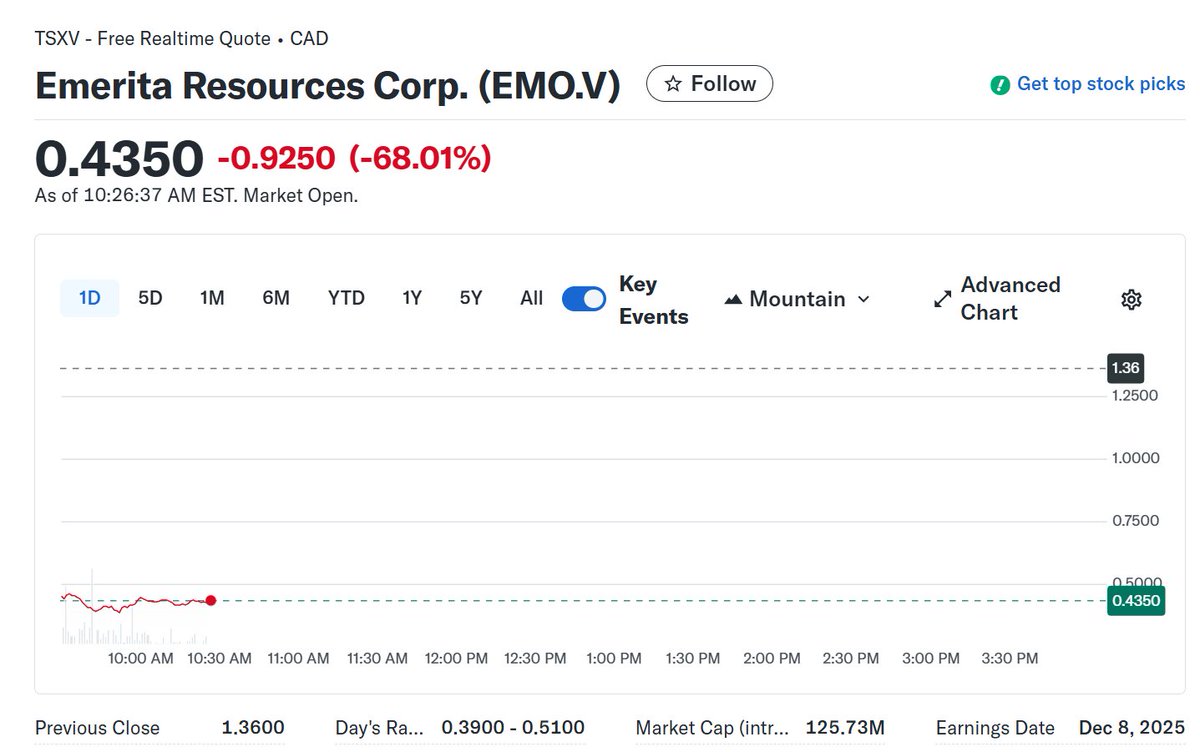

Today marks one of the most important moments of my investing life.

After more than three years following and dissecting the $EMO.v case with countless calls, discussions, and nonstop attacks from pumpers, everything ends here.

-68%, the Big Short is closed

30

9

237

639,439

5 Dec 2025

How it started / How it's going:

Cannacord recommended a turd to retail when it was right on the edge of collapse, got their fees, and loaded some EMO shares onto a tonne of baggies... and towards the next one like nothing happened

$EMO.v

3

4

37

13,509

5 Dec 2025

Spanish Court pays for Xmas presents this year!

Let's send this turd to cash value 🥳🥳

Props to the owner of the EMO short thesis @The_Godas !! This is all you buddy, enjoy!

Hoping for sub 30cts 🤞

2

2

17

1,807

5 Dec 2025

🐐

10

1,352

19 Nov 2025

Narrator: "it did, in fact, teleport to 10$"

Quite a bit of money left on the table by selling on Monday tbh.

Although not having Ana's will tied to my net worth is enough of a payoff for now.

17 Nov 2025

Sold $SGML

Had kept the position with different sizing since early 2023. Remember Tesla was about to acquire it? Yeah since before that pump

Managed to end in the green despite the stock still being down 80% from the '23 highs. But this has been the worst ROI adj. for headache of 2025, without a doubt.

The contractor leaving, the mine not producing, liquidity in the Co is nonexistent, an offtake that's incoming since May... and worst of all the way Ana just tries to sweep everything under the rug and not even disclose it.

I'm pretty confident the mine will restart and continue to operate well. But I could easily see it back at 6$ in a couple weeks. Maybe I hate myself enough to buy in again at that price, maybe I've learned the lesson and don't want to be involved with bad mgmt anymore, we'll see!

It could also teleport to 10$ if a good off-take is announced given how spod has been trading these past few months. That was my thesis when trippling down during summer. I just didn't expect Ana to be so ret*rded and the contractor leaving..

Anyhow, pretty lucky Ganfeng's chairman saved the week.

2

15

2,832

17 Nov 2025

Sold $SGML

Had kept the position with different sizing since early 2023. Remember Tesla was about to acquire it? Yeah since before that pump

Managed to end in the green despite the stock still being down 80% from the '23 highs. But this has been the worst ROI adj. for headache of 2025, without a doubt.

The contractor leaving, the mine not producing, liquidity in the Co is nonexistent, an offtake that's incoming since May... and worst of all the way Ana just tries to sweep everything under the rug and not even disclose it.

I'm pretty confident the mine will restart and continue to operate well. But I could easily see it back at 6$ in a couple weeks. Maybe I hate myself enough to buy in again at that price, maybe I've learned the lesson and don't want to be involved with bad mgmt anymore, we'll see!

It could also teleport to 10$ if a good off-take is announced given how spod has been trading these past few months. That was my thesis when trippling down during summer. I just didn't expect Ana to be so ret*rded and the contractor leaving..

Anyhow, pretty lucky Ganfeng's chairman saved the week.

2

22

5,733

14 Nov 2025

Good discussion yesterday on what crushed AISC expectations at Kamoa-Kakula since FID.

The conclusion: higher sustaining Sust Capex than expected (~ 0.15$/lb, power back-up and debottlenecking plan), higher opex due to logistics and power volatility (~ 0.45$/lb), and higher royalties (~ 0.10$/lb, due to higher Cu price, so no biggie here). All in all 0.70$ more expensive to produce one pound of copper.

To be clear I was using the 2019 and 2020 reports as the baseline. The 2023 report had slightly higher OPEX assumptions, although still lower than reality.

13 Nov 2025

Mining is hard.

Even a very successful mine construction like Kamoa-Kakula: building Phases1-3 on-time, on-budget and ramping up to 550ktpa Cu at crazy speed (let's forget about the geotech event and the UG pool it has become lately), had a 50% increase in OPEX from expectations at FID to reality in the first few years of operations.

Adjusting for inflation AISC was meant to be ~1.5$/lb. Average of the first 3y of operation (2022-2024) was ~2.2$/lb!!

Who wants to make an educated guess (or speculate) as to why KK had such an OPEX jump?

And I'm leaving out 2025 for the obvious reasons.

Again, on-time, on-budget, ramp-up to plan (and even beating plan), production beat, but somehow it cost 50% more to extract each unit of metal than was planned. Pretty crazy if you ask me.

5

21

6,370