1,570 Photos and videos

Pinned Tweet

May 30

Tire of losing?

Want to make money in this market without gambling?

Last month I made $27,731.92 by selling options.

123 Total Trades

————————

*107 Trade Winners

*3 Trades Losses

*7 Trades Rolled (into future winners)

*5 Trades Assigned

Results here joshtradeoption.com/post/jos…

I do this every month.

Join me and learn.

You can do this too.

Join along! whop.com/discover/selling-op…

4

1

8

21,524

27m

This 100%

43m

When $SNDK was at $350 people believed that was the top

When $MU was at $350 people believed it topped

When $DELL was at $150 people were convinced it topped

Enough people lost money shorting it

More people lost money selling it early

Leading stocks can go another 200% without you.

80% of your time should be spent on bullish bias. Market’s gravity is up.

Let stocks like $INTC $MRVL $WDC $HUR $MRVL be your reminders.

1

2

680

29m

Oh boy

1

3

1,088

How is $META trading at such a cheap valuation right now?

At ~$567, META sits at a forward P/E around 17. That's near multi-year lows.

Q1 2026 revenue exploded to $56.31 billion, up 33% year over year, with Family of Apps ad revenue up 33 percent and strong momentum in ad impressions plus pricing. The core business continues delivering exceptional margins amid heavy AI investments.

Analyst consensus price target sits near $820, implying over 45% upside.

Am I missing something?

4

6

923

How is $NVDA trading at such a cheap valuation right now?

At ~$205, NVDA sits at a forward P/E around 23. That's its cheapest in nearly a decade and basically in line with the S&P 500.

Q1 FY2027 revenue exploded to $81.6 billion, up 85% year over year, with Data Center hitting a record $75.2B.

Full year FY2026 revenue already topped $215.9 billion, up 65%. Blackwell ramp is just getting started, demand from hyperscalers remains insatiable, and new AI workloads are only accelerating.

Analyst consensus price target sits near $305.

Am I missing something or is this one of the most obvious mispricings in big tech right now?

Are you adding here?

3

1

8

873

Im long $AMZN with commons and call options.

How does the Street have it so wrong here?

- Amazon maintains leadership in cloud infrastructure via AWS with its AI optimized offerings accelerated enterprise adoption.

- Q1 2026 net sales reached $181.5 billion with 17% year over year growth while AWS revenue hit $37.6 billion up 28% the fastest growth in 15 quarters.

- Strong momentum in advertising exceeding $17 billion quarterly and retail unit growth at 15%.

- Operating income expanded to $23.9 billion.

- Price target: $310-350

For me, this is a no brainer buy here.

4

3

719

Im still heavily invested in $NOW with LEAPS and commons.

- ServiceNow holds dominant positioning in enterprise workflow automation.

- Q1 2026 subscription revenue hit $3.671 billion with 22% year over year growth.

- Full year 2026 subscription guidance raised to $15.735 to $15.775 billion implying 21% growth.

- Non GAAP operating margins expanded to 32%.

- Price target: $185-210 per share by 2027.

$NOW where do you land? Bull or bear?

4

4

827

$AAOI

I’m bullish. Are you invested?

Applied Optoelectronics demonstrates robust positioning in the 800G and emerging 1.6T optical transceiver market through vertical integration of InP laser technology and advanced manufacturing processes.

- Q1 2026 revenue reached $151.1 million representing 51 percent year over year expansion driven by hyperscaler deployments in AI accelerated compute clusters.

- Management guidance projects full year 2026 revenue exceeding $1.1 billion supported by a $324 million advanced node order backlog and DOCSIS 4.0 multi year contracts.

- Gross margin trajectory targets 35 percent by year end as product mix shifts toward higher speed coherent modules with improved yield curves from Houston facility expansions.

- Capacity constraints currently limit output to approximately $1.5B addressable demand creating a supply bottleneck that favors AAOI share gains.

- Price target: $220 achieving monthly run rates above $200Mby mid 2027.

2

6

757

Green Monday if this holds?

BREAKING: A senior Iranian official has told Reuters that, under a draft memorandum with Tehran, the US has agreed it will not impose any new sanctions on Iran until a final deal is reached.

🔴 More on aljazeera.com

3

2

1,971

19h

My Canadian friends, this is worth keeping an eye on. @Gubloinvestor

23h

If you have TFSA account in Canada

Keep $10,000 on side. I want to make sure that your $10,000 sees 100% gain in next 6 months.

Stay in touch, i am going to post more about TFSA. We will find winners to make sure we Gain and pay no taxes on Our gains.

5

3

28

14,956

19h

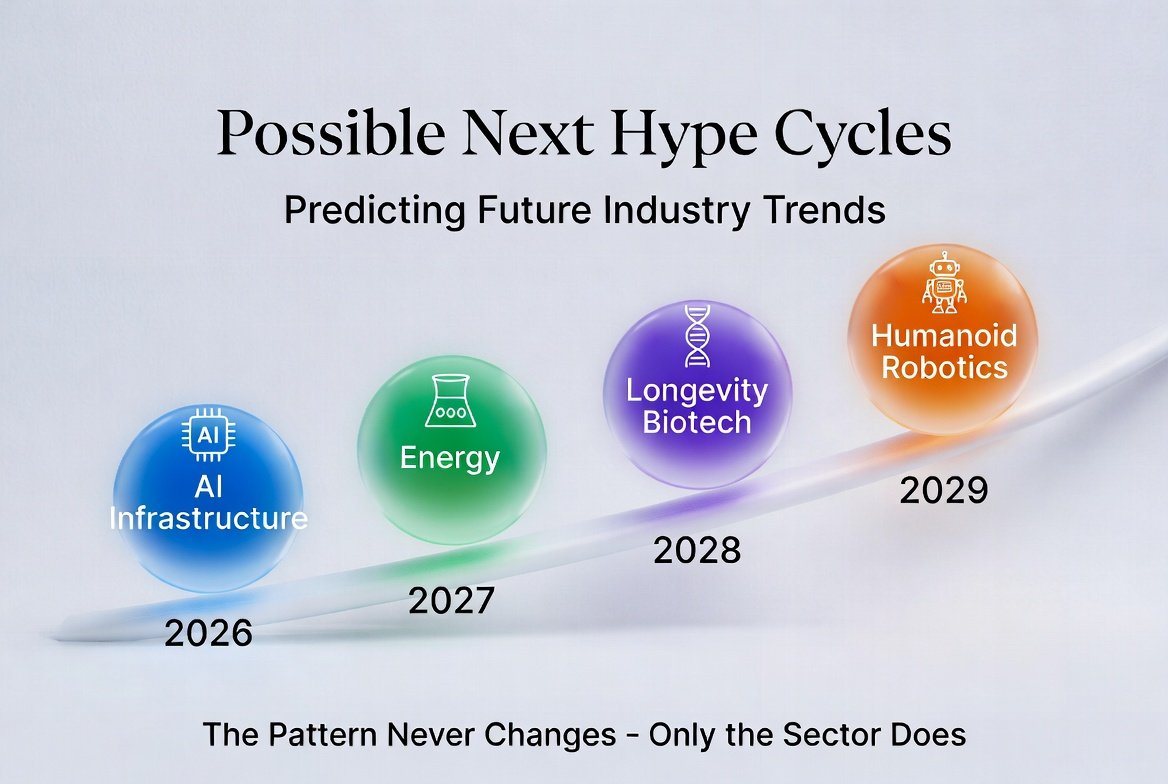

Good analysis here guys! @topsecretstocks does a great job with this kind of approach to analysis!

Hype Cycles - Which one do you think hits next? Drop your pick below.

❤️ Like & 🟦 Save

Markets run on narratives. Every few years a new sector catches fire, valuations detach from reality, retail piles in. The pattern never changes, only the sector does.

Here are the major ones from the last 30 years and what might be coming. 🧵👇

3

3

8

5,833

19h

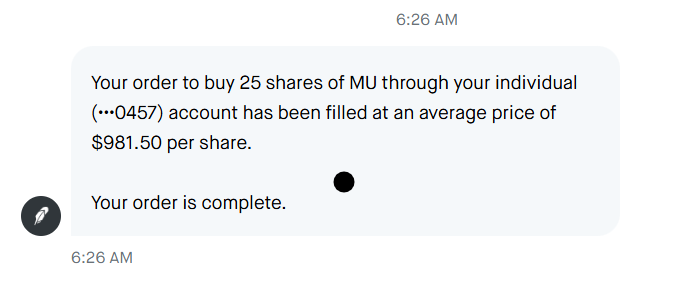

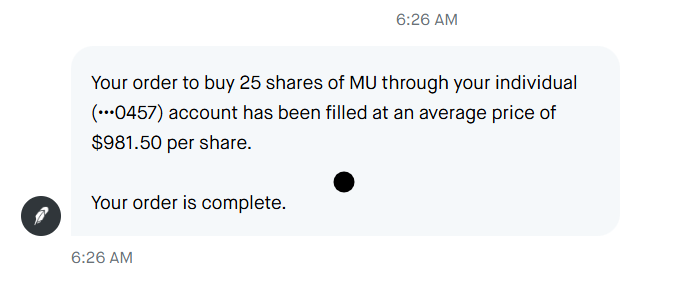

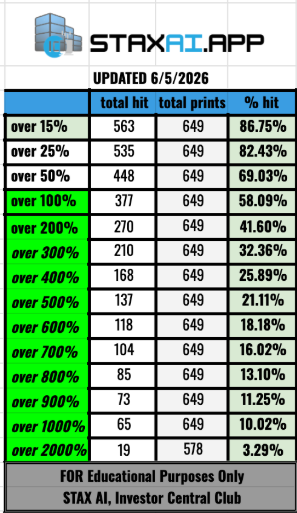

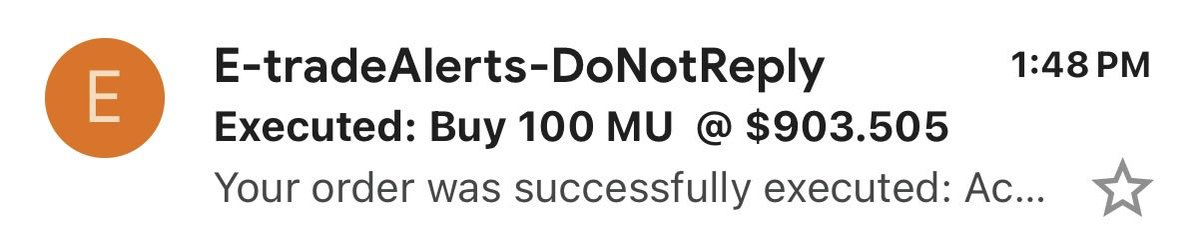

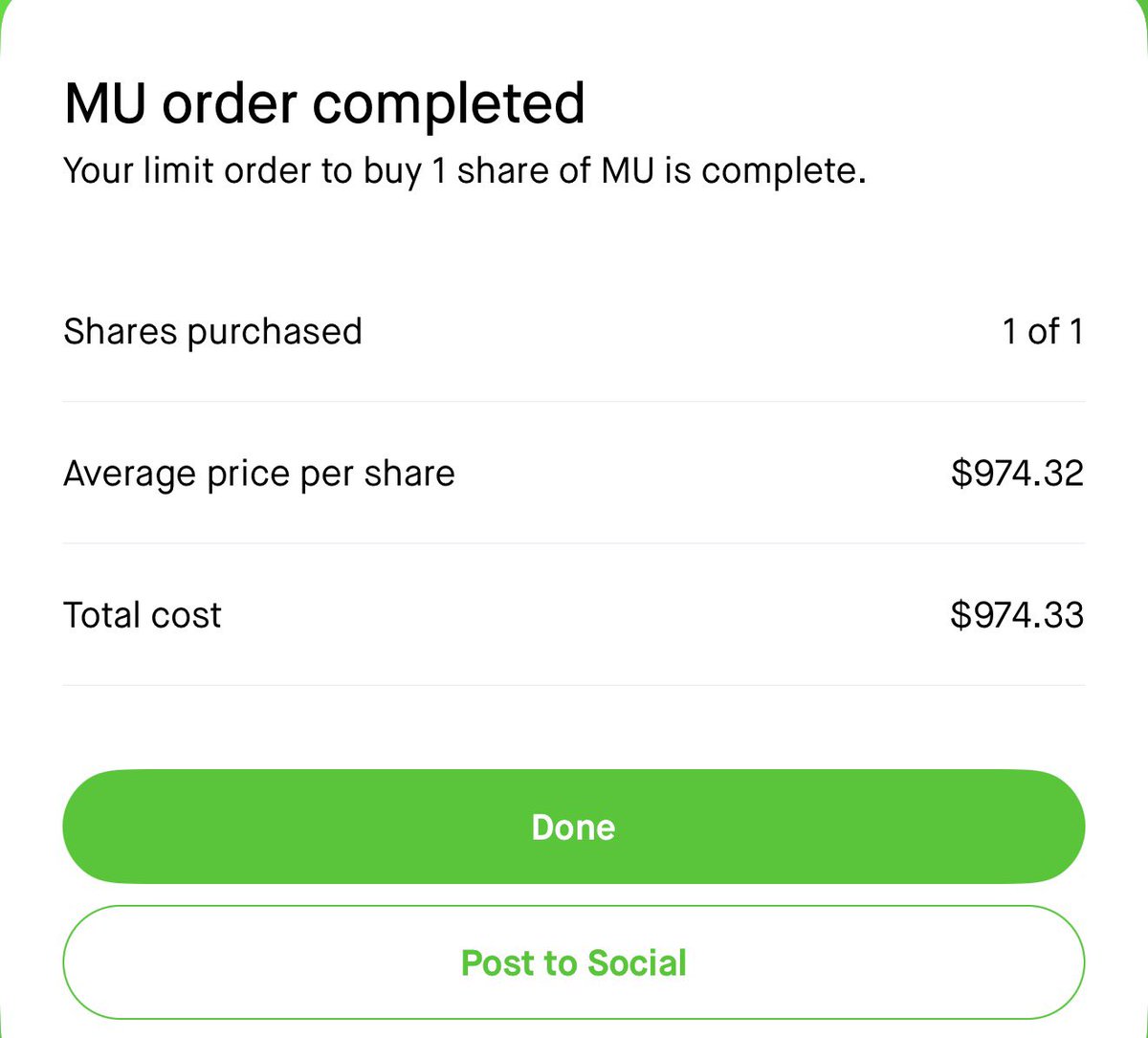

Who’s with me? $MU

Bull Thesis for MU (Micron Technology)

Micron is positioned at the center of the AI infrastructure buildout as the leading supplier of high-bandwidth memory (HBM) and DRAM essential for AI training and inference.

Strong demand has led to sold-out production capacity through much of 2026 and 2027, with record revenues, gross margins near 60%, and exceptional free cash flow in recent quarters.

AI-driven memory demand represents a multi-year structural shift rather than a traditional cyclical boom, supported by hyperscaler capex increases and HBM4 qualifications at premium pricing.

Micron's execution, technology leadership, and pricing power should drive continued earnings growth.

Price target: $1,400–$1,750 within 12–18 months, reflecting expanded multiples on sustained high profitability.

15

2

130

52,550

Jun 13

We bullish if this pans out?

Jun 13

Pakistani Prime Minister: The United States and Iran have reached the final text of the peace agreement

5

14

3,271

Jun 13

Brick by brick!!! $MU is a great deal here. I added tonight too.

@DollarCostAvg has it right!

4

26

4,851

Jun 12

I appreciate my friend @Gubloinvestor for sharing this. He's great and one of my best friends on here.

Jun 12

My friend @JoshTradeOption is must follow for all the great dip buy. One of the best on here for options and dip buying opportunity.

3

5

2,896