We cover Canadian and Australian listed resource stocks with an emphasis on the juniors.

Joined July 2014

- Tweets 626

- Following 248

- Followers 5,747

- Likes 0

228 Photos and videos

KW June 5, 2026 Part 2: Why is Semi-Annual Reporting a Bad Choice?

kaiserresearch.substack.com/…

1

2

313

May 18

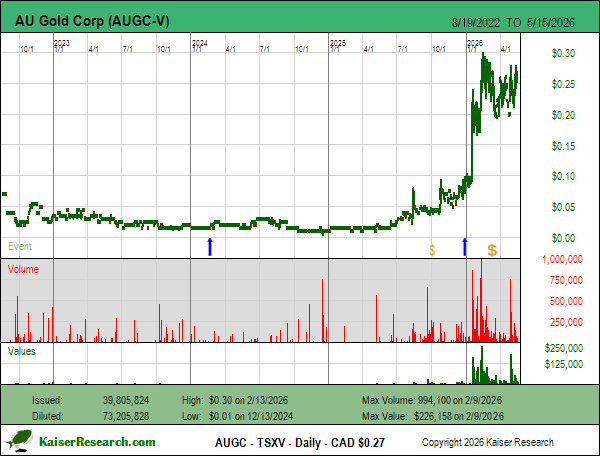

KW May 15, 2026: MIF Observations - AU Gold Corp -kaiserresearch.substack.com/…

@MetalsInvtForum

6

405

May 18

KW May 15, 2026: MIF Observations - Inventus -

kaiserresearch.substack.com/…

@MetalsInvtForum

1

7

400

May 18

KW May 15, 2026: MIF Observations - Silver North Resources Ltd - kaiserresearch.substack.com/…

@MetalsInvtForum

6

457

May 17

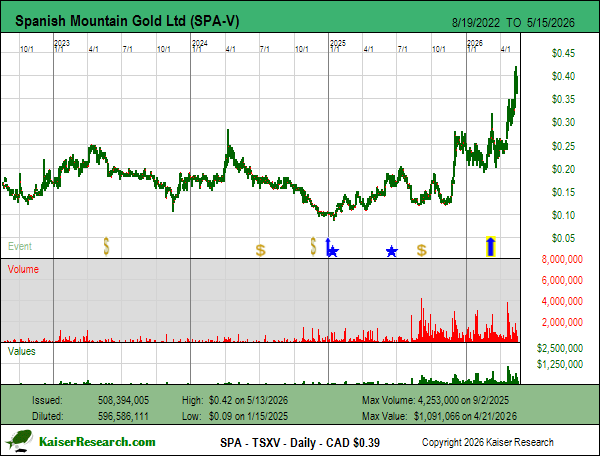

KW May 15, 2026: MIF Observations - Spanish Mountain Gold Ltd - kaiserresearch.substack.com/…

@MetalsInvtForum

8

665

May 17

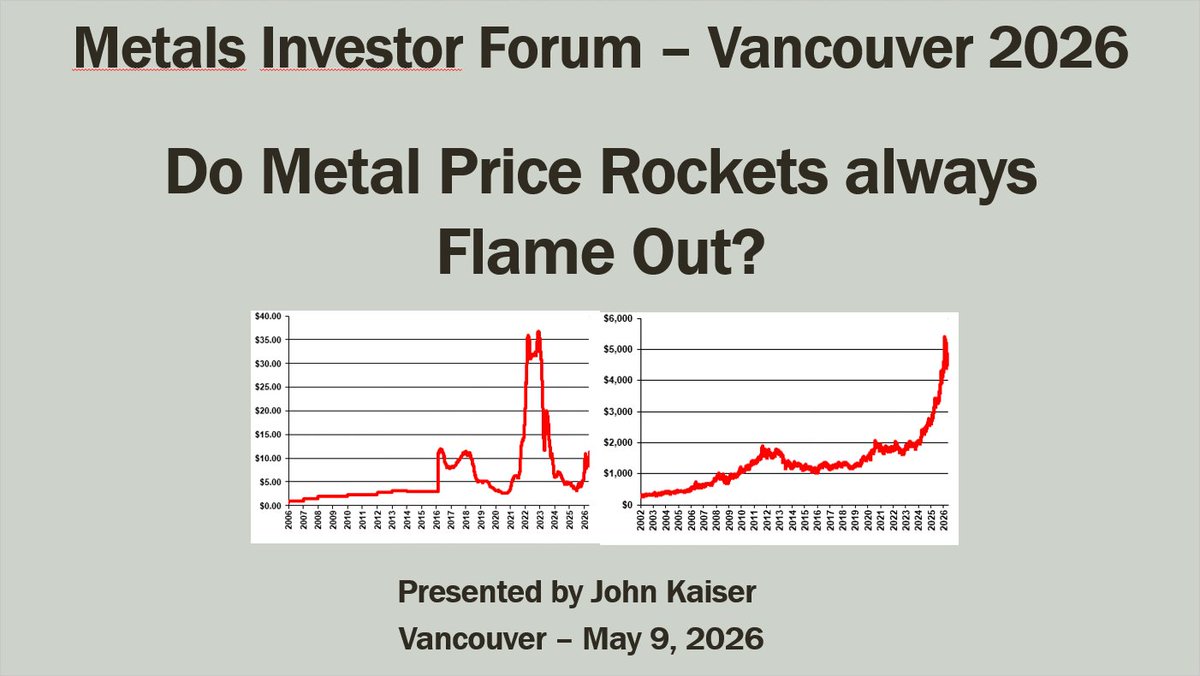

KW May 15, 2026: MIF JK Talk - Do Metal price Rockets always Flame Out? - kaiserresearch.substack.com/…

@MetalsInvtForum

6

423

Apr 28

In 2012 when @bloom_energy was still getting started it did a non-binding offtake deal with Metallica Minerals for 30-60 tpa Sc2O3 as a by-product from its nickel-cobalt Sconi project. That went nowhere and Bloom went on to secure its scandium supply from China by developing a way to recover scandium from titanium dioxide waste streams generated by pigment makers. Bloom Box sales growth did not meet expectations but in 2025 that changed when AI data centers realized they needed a localized supply of electricity that did not come from grids that served civilians.

The world changed for Bloom as it secured deals to supply up to 2.8 GW of Bloom Box capacity for the likes of @Oracle. The stock price has increased tenfold from a year ago and the company today has a market cap of $64 billion. Bloom Energy will release its Q1 2026 financials today and hold a conference call at 2 pm Pacific Time.

investor.bloomenergy.com/pre…

Bloom is a great story but there is a hard question KR Sridhar must answer. How much scandium oxide per 100 kW of Bloom Box is required and where will it come from so that 2.8 GW of Bloom Box capacity can be delivered over the next few years?

USGS estimated 60 tonnes was produced in 2025 from a variety of non scalable by-product sources, much of it from China which now has dual use restrictions on scandium exports.

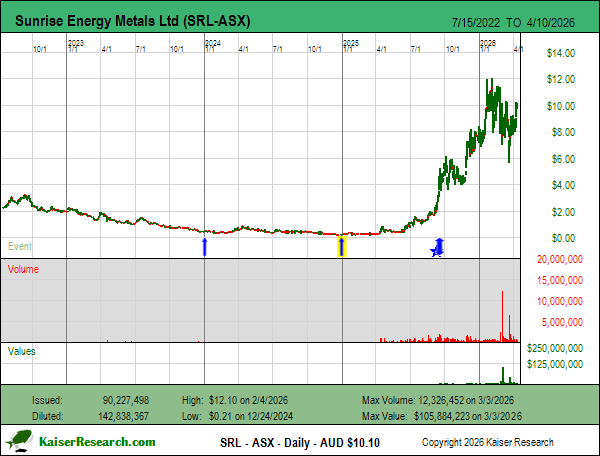

@SunriseMetals has completed a DFS for its Syerston scandium project whose initial version can produce 60 tpa, with a parallel track with 120 tpa output. A solid offtake agreement would eliminate any concern about scandium supply for Bloom, and it would lay the foundation for future aluminum-scandium alloy demand growth. And secure Bloom's future.

Will Bloom Energy come clean on its scandium needs and what it is doing about it?

3

3

15

1,023

Apr 26

KW Apr 25, 2026: Without Sunrise will Bloom Energy Sunset?

On April 28 a company Newsweek added to its list of most trustworthy companies will be asked, how much scandium does it need for its Bloom Boxes and where will it come from?

kaiserresearch.substack.com/…

1

7

673

Apr 23

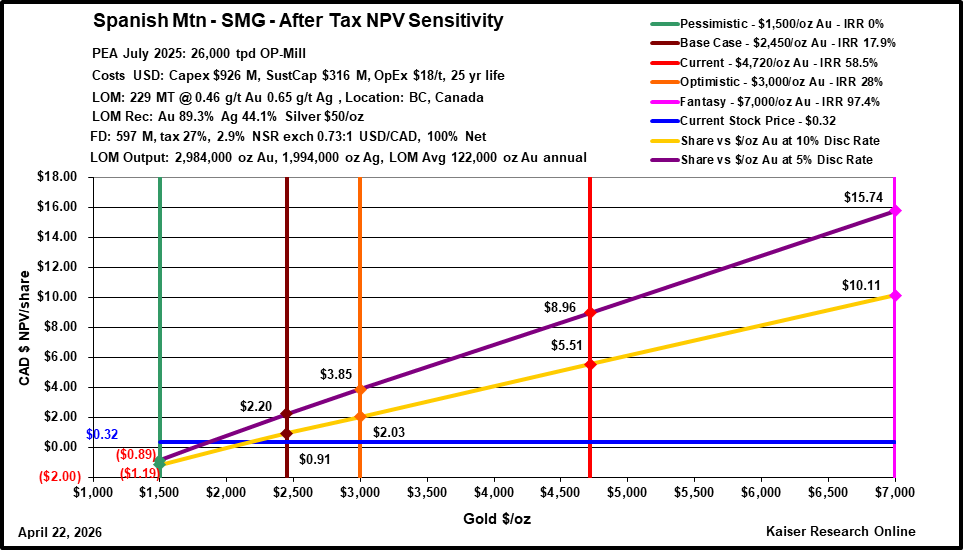

Apr 22, 2026: Wheaton endorses Spanish Mountain with a big royalty deal - If Spanish Mountain Gold Ltd deserves to be in the $0.75-$1.50 range based on $3,000 gold, what should it be at $4,720 if we dare believe such a level is possible in the long run? - kaiserresearch.substack.com/…

1

2

12

969

Apr 15

Mining Stock Education Interview with Bill Powers - kaiserresearch.substack.com/…

2

2

22

2,481

Apr 15

KW Apr 12, 2026 Part 3: A Kingdom for a Sword - Scandium - kaiserresearch.substack.com/…

4

448

Apr 15

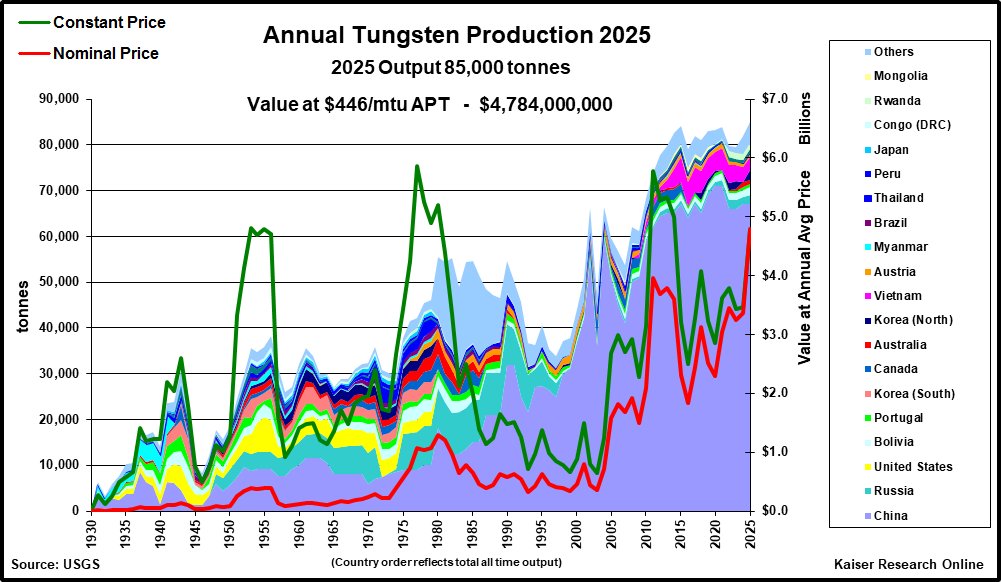

KW Apr 12, 2026 Part 2: A kingdom for a Sword - Tungsten - kaiserresearch.substack.com/…

3

384

Mar 28

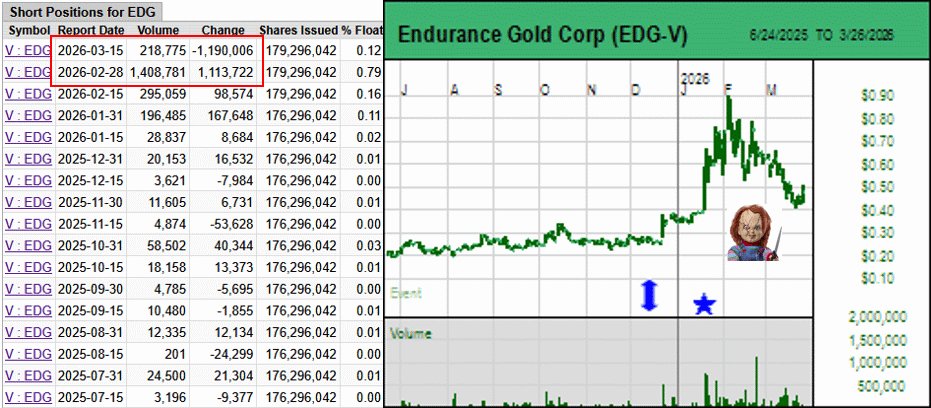

Endurance needed to overcome Canada's Chucky Doll System - Or why Making Canadian Resource Juniors Great Again is so difficult: kaiserresearch.substack.com/…

1

10

772

Mar 26

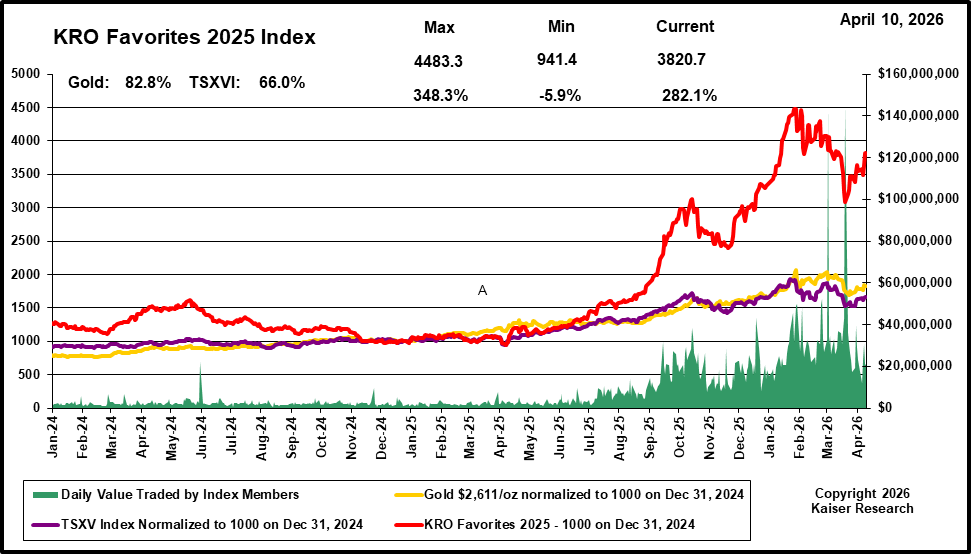

KW Mar 24, 2026: Repairing a Scary Exponential Gold Chart - kaiserresearch.substack.com/…

1

12

776