Joined October 2024

- Tweets 1,385

- Following 80

- Followers 8,099

- Likes 7,788

255 Photos and videos

Feb 7

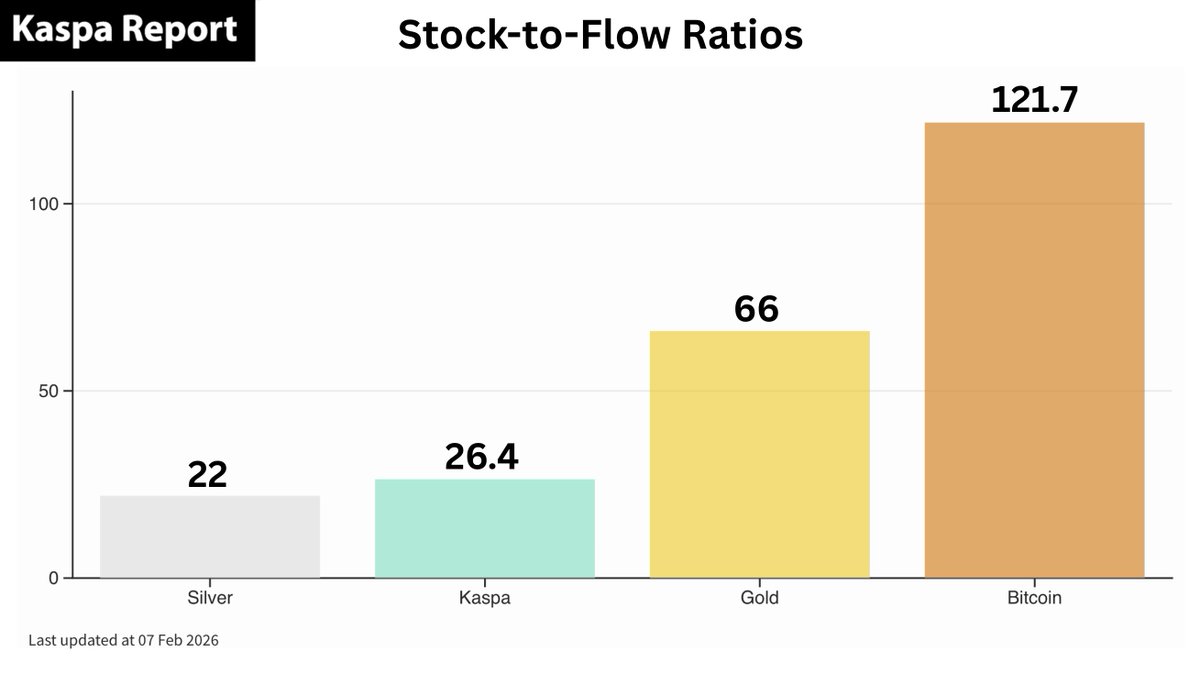

Kaspa’s stock-to-flow ratio has already surpassed silver’s and is on track to exceed gold’s by mid-2027.

2

35

157

6,972

Feb 7

Please excuse the recent lack of posts. The person who manages this account has been dealing with some health issues, which have fortunately improved.

3

29

1,320

Kaspa Report retweeted

12 Apr 2025

Kaspa is Satoshi's vision.

8

66

450

13,203

4 Dec 2025

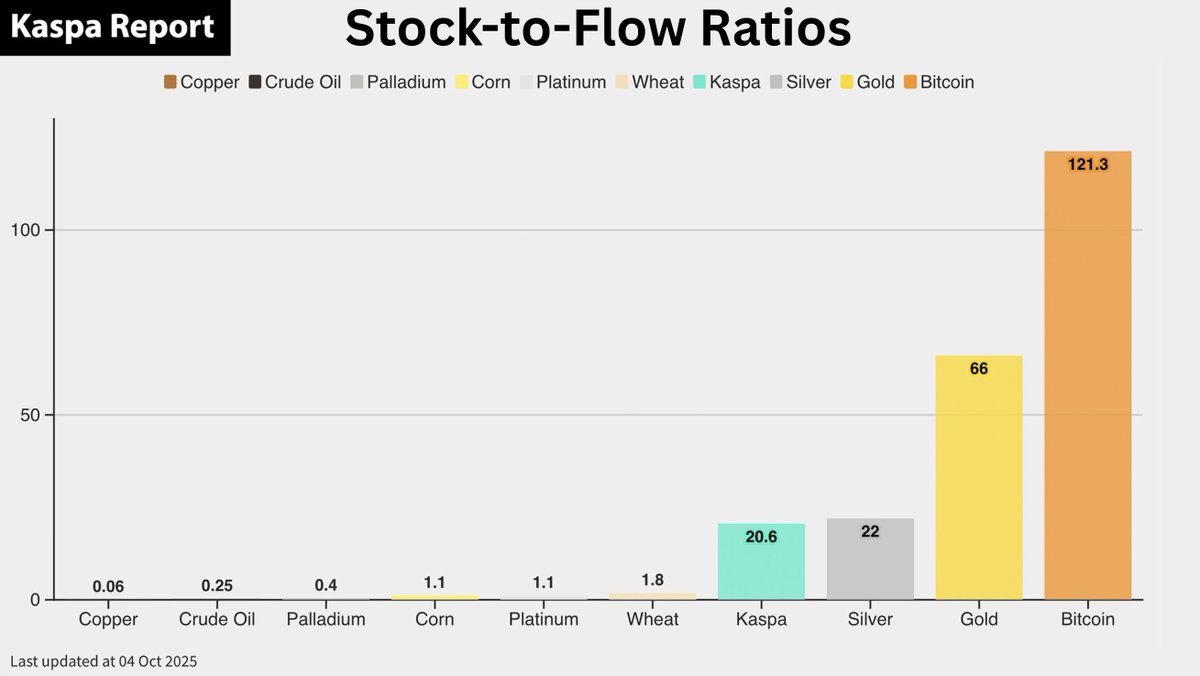

Kaspa's Stock-to-Flow Ratio Just Surpassed That of Silver

At approximately midnight Eastern Standard Time on December 4, 2025, Kaspa’s stock-to-flow (S2F) ratio quietly crossed a historic milestone: it surpassed that of silver.

While a commodity’s S2F ratio does not directly determine its market capitalization, since many other factors influence fiat price action, if KAS were valued at the same aggregate level as the world’s above-ground silver, its price would be roughly $122 per KAS.

If one believes Kaspa to be the most advanced form of money ever devised, offering a ledger superior to silver or any other monetary commodity, then on what basis should we assume its market cap could never exceed silver’s?

Unlike gold and silver, Bitcoin and Kaspa are digital commodity monies that, for the first time in history, provide ledgers where the stock-to-flow ratio can be precisely measured and independently verified by anyone. In contrast, gold and silver rely on trust-based systems and remain vulnerable to coordination failures and information asymmetries.

In this respect, Bitcoin and Kaspa represent superior ledger technologies. They resolve the Byzantine Generals Problem, ensuring consensus without centralized trust.

By the end of this decade, Kaspa’s S2F ratio will exceed that of both gold and Bitcoin.

19

146

547

15,730

4 Dec 2025

Data Sources:

Kaspa Network (via Kaspa REST API server)

Silver Market Capitalization – CompaniesMarketCap

Methodology:

Kaspa’s total coin supply (stock) and current block reward (flow) were obtained from the Kaspa Network via the Kaspa REST API server.

Using these values, the exact time at which Kaspa’s S2F ratio would exceed silver’s estimated S2F of 22 was calculated using GPT-5.

Kaspa’s stock was not adjusted for burned coins; however, even with such an adjustment, the result remains essentially unchanged. With an adjusted coin supply, Kaspa’s S2F will still surpass silver’s on December 4, 2025, immediately following its block reward reduction.

1

4

21

2,080

27 Nov 2025

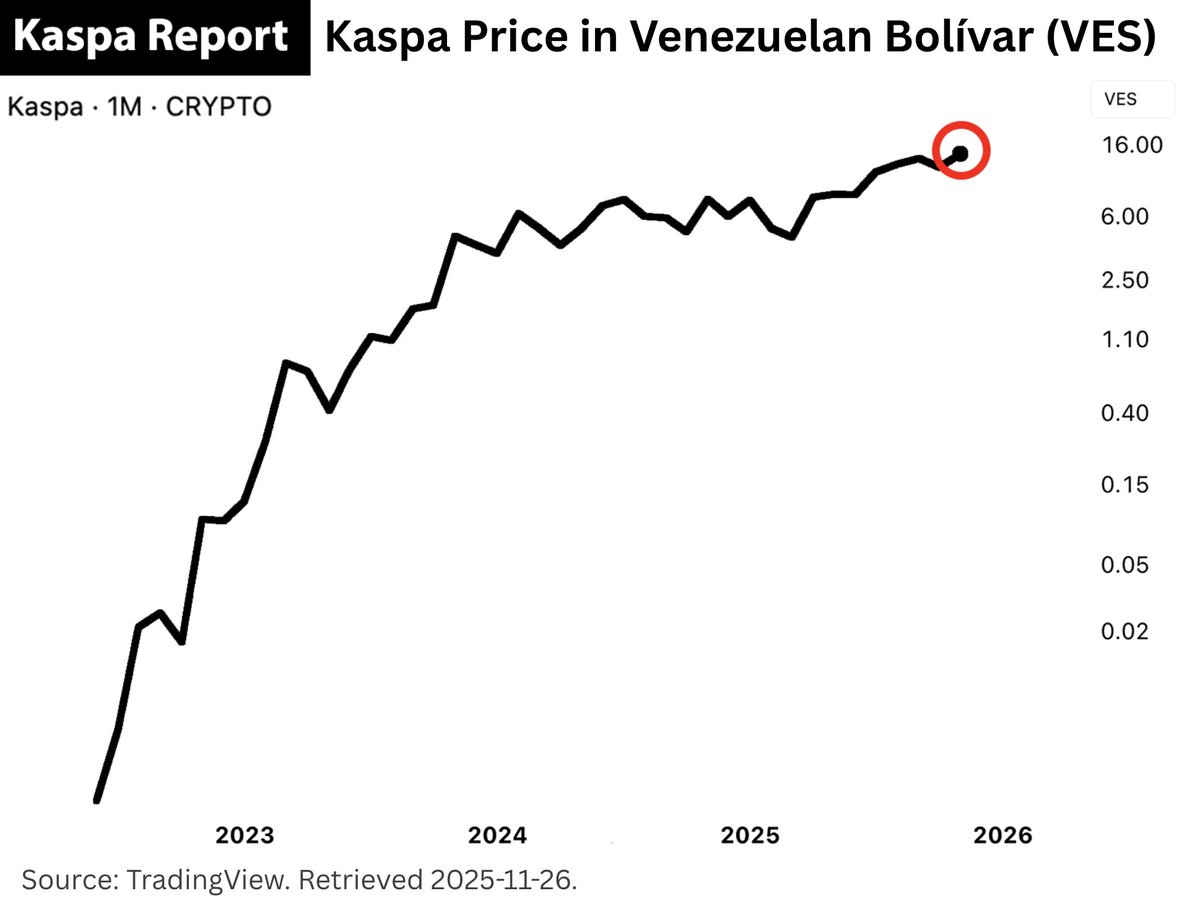

Kaspa hits new all-time high against the Venezuelan bolívar.

Although the Venezuelan bolívar (VES) is among the world’s fastest-devaluing fiat currencies, all fiat currencies will generally tend to depreciate against Kaspa in a similar way over time.

Interestingly, Kaspa’s power law model fits much better when Kaspa is priced in the Venezuelan bolívar: there is less deviation from the line of best fit than when priced in U.S. dollars or in fiat currencies effectively pegged to the U.S. dollar.

That tighter fit arises from two confounding factors that largely cancel each other out. First, the Venezuelan bolívar is suppressed against the U.S. dollar because Venezuela has restricted dollar access. Second, Kaspa is suppressed against the U.S. dollar by certain exchanges. These exchanges use many tactics to suppress Kaspa’s price, but chief among them is trapping long KAS exposure in USD stablecoins through Kaspa perpetual futures.

These two unrelated factors tend to suppress each currency against the dollar by a roughly similar magnitude, causing them to offset each other and leaving the KAS/VES price time series with a better power law fit.

This shows that the choice of unit (currency) for the dependent variable (Kaspa’s price) can materially affect the power law model’s explanatory power (e.g., R² value). It strengthens the case for using on-chain, hard-to-manipulate metrics to measure Kaspa’s monetary value.

Inactive supply is harder to manipulate and better reflects Kaspa’s use as a store of value—a core function of money—making it a more reliable indicator of Kaspa’s monetary value than any single fiat currency price time series.

8

49

308

10,125

26 Nov 2025

The holder of Kaspa’s largest address has created a supply shock. This holder’s continued accumulation of KAS is unsustainable, especially as demand from other market participants rises.

Kaspa’s supply shocks are likely to be extreme, due to its rapid emission schedule, completely inelastic supply, and strong tendency for rapid adoption as both a store of value and medium of exchange.

24 Nov 2025

Wallet #1 Continues Aggressive KAS Accumulation

Over the past several months, the holder of Kaspa’s largest address (ending in m7n4uk5a, labeled “Wallet #1” in the animation) has been aggressively accumulating KAS.

This holder’s demand for KAS is so strong that even if every miner sold all newly mined KAS exclusively to them, it still wouldn’t meet their demand. They must therefore acquire some of their KAS from existing holders, not just from new supply.

Notice that Wallet #1’s net accumulation surged in the aftermath of the October 10 market crash. While some existing holders sold or were liquidated, Wallet #1 was aggressively accumulating.

30

96

489

28,183

26 Nov 2025

Kaspa fulfills Satoshi’s vision: truly decentralized, peer-to-peer money that settles almost instantly.

1

3

52

1,353

Kaspa Report retweeted

14 Mar 2025

Abandon the idea of taking profit from Kaspa at a specific price target, since doing so would mean exchanging superior money for inferior money. Instead, transform your understanding of money: aim to spend only what you need and use KAS to store remaining value.

22

61

397

22,630

24 Nov 2025

Wallet #1 Continues Aggressive KAS Accumulation

Over the past several months, the holder of Kaspa’s largest address (ending in m7n4uk5a, labeled “Wallet #1” in the animation) has been aggressively accumulating KAS.

This holder’s demand for KAS is so strong that even if every miner sold all newly mined KAS exclusively to them, it still wouldn’t meet their demand. They must therefore acquire some of their KAS from existing holders, not just from new supply.

Notice that Wallet #1’s net accumulation surged in the aftermath of the October 10 market crash. While some existing holders sold or were liquidated, Wallet #1 was aggressively accumulating.

22

73

348

42,497

24 Nov 2025

If you enjoy the Kaspa Report, give us a follow. If you’d like to support our work with KAS, you can support us here: kaspa.report/donate

1

3

17

1,923

23 Nov 2025

It’s hard to overstate the impact Kaspa will have in a world whose ability to reach consensus on truth is so impaired.

1

11

88

2,361

Kaspa Report retweeted

2 May 2025

Kaspa solves problems that most of the world hasn’t yet realized need solutions.

14

46

275

7,749

20 Nov 2025

I respect Asher’s analysis in the quoted tweet and the time he took to look into this, but I believe that what this chart shows is just that we are in the miner-capitulation phase of the cycle.

Although it’s a subtle point, one shortcoming of the chart and its analysis is the assumption that the U.S. dollar, as the unit of measure for miner revenue, is globally determinative.

Not all miners track mining revenue in USD. In some countries, local fiat currencies experience inflation far faster than the dollar, which means that KAS mining revenue denominated in those currencies has dropped by less than this chart suggests.

For instance, in Venezuela, the price of KAS in local currency is higher now than when the Kaspa network’s hashrate was at its peak, indicating that the chart may not accurately reflect miner incentivization there. While I’m not asserting that mining KAS in Venezuela is more profitable, I am highlighting the problem with assuming USD-denominated revenue is globally determinative of mining incentivization.

Mining will increase if KAS is increasingly used as money, because mining is the mechanism by which energy is converted into money within the Kaspa economy. Therefore, if Kaspa’s use as money continues to grow, as rising inactive supply clearly indicates, mining and hashrate will tend to rise as well.

Relatedly, I am working on a report that attempts to quantify the extent to which exchanges are suppressing Kaspa’s fiat price. It is important to understand that mining incentives are being artificially held down at the moment, and this is not due to any design defect of Kaspa.

In effect, this suppressive action by exchanges “steals energy” from miners and distributes it, in its converted form, to market buyers of KAS. Exchanges are therefore subsidizing the cost of KAS for buyers at the expense of miner profitability. The good news for Kaspa’s security is that such suppression can only ever be temporary, as a supply shock will eventually disrupt it.

From a theoretical standpoint, exchanges suppressing Kaspa’s price are behaving as inefficient economic actors. Over time, market forces will eliminate these inefficiencies, and the suppression will necessarily end. A time will likely come when some of the same actors currently pushing Kaspa’s price downward will, after accumulating enough KAS, attempt to drive price upward — and when that happens, the incentive to mine will return with full force.

We are currently in the phase of the cycle where both the coin and mining are “cold.” Once the coin “heats up” again (price rises), hashrate will follow on a lagging basis. We can be reasonably certain that the price of KAS will rise by looking at multiple metrics: inactive supply continues to increase (i.e., KAS is increasingly being used as a store of value), transactional volume is generally trending upward, and basic supply-and-demand dynamics support higher prices.

Kaspa’s supply is completely inelastic and new supply falls rapidly, so when demand rises (or even if it merely stays constant or decreases more slowly than new supply) price will move higher.

With that said, we already know real demand for Kaspa is extremely high; see my recent post analyzing the KAS accumulation of Kaspa’s largest address (x.com/KaspaReport/status/199…). A supply shock will eventually occur, and Kaspa’s price against fiat currency will likely rise sharply, marking the beginning of a new bull cycle and a renewed rush to mine.

Kaspa’s hashrate won’t just reach new all-time highs; it will tend to increase faster than Bitcoin’s over time. Kaspa’s much higher block creation rate reduces mining reward variance and improves the efficiency with which miners convert energy into its stored monetary form, KAS. This, along with block parallelism / the avoidance of stale blocks, makes mining KAS more attractive than mining BTC and, over the long term, will cause the Bitcoin network to leak hashrate to Kaspa. In essence, because Kaspa is a better distributed ledger and a superior commodity money, Kaspa’s hashrate will tend to rise faster over time.

Since 2024, the scarcity effects of Bitcoin’s halving made BTC temporarily more valuable relative to KAS. As that effect fades, and because Kaspa’s stock-to-flow ratio rises much more rapidly than Bitcoin’s, the pendulum will swing strongly back toward Kaspa, and KAS will become more valuable when measured in Bitcoin terms. When Kaspa becomes more valuable relative to Bitcoin, Bitcoin miners will tend to switch to mining Kaspa.

As Kaspa surges in value against Bitcoin, Bitcoin miners perceive an opportunity to mine KAS and convert it into BTC for an excess return compared with mining BTC directly, which causes Kaspa’s hashrate to grow faster than Bitcoin’s.

This excess return can also be understood as KAS being more energy-efficient to mine than Bitcoin, which ties back to Kaspa’s lower reward variance and absence of stale or orphaned blocks. This is precisely what MARA’s CEO recognized when the company chose to begin mining KAS.

Again, I respect Asher’s analysis and the time he took to review the data, but it is flawed because it assumes USD-denominated revenue is globally determinative for mining incentivization. There are also confounding factors, such as temporary CEX price suppression, that the chart and its analysis do not capture.

The important question is whether Kaspa’s use as money is intact and growing; if it is, then the incentive to mine will remain intact and grow as well.

Kaspa is unstoppable, and the world has barely begun to grasp the scale of the disruption it will cause.

18 Nov 2025

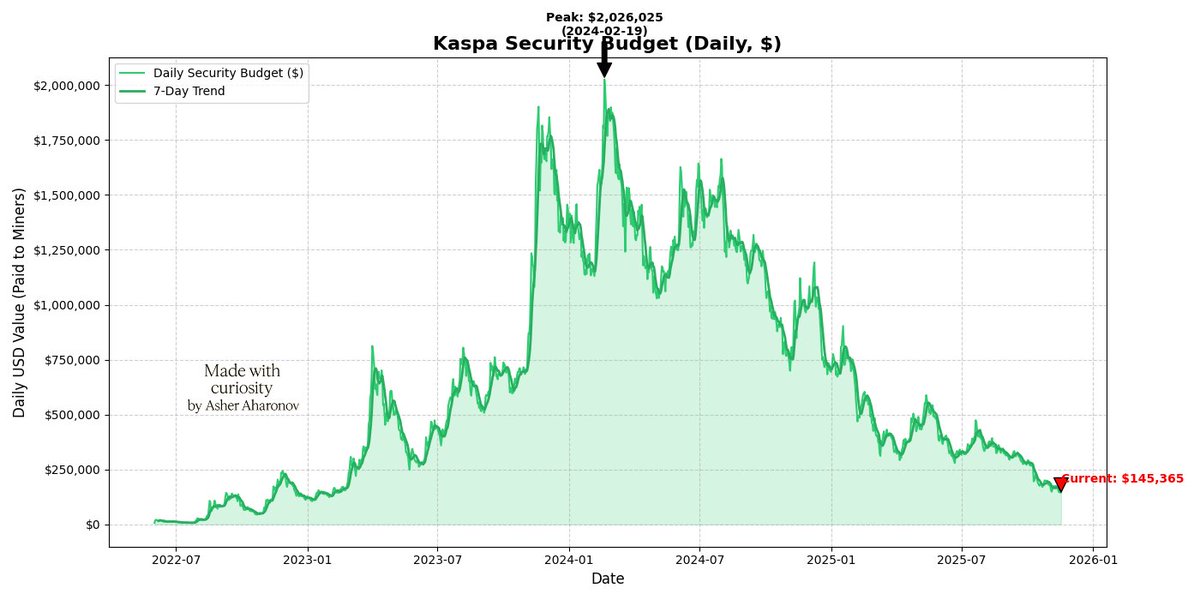

$KAS Security Budget Analysis

עברית אחרי אנגלית 👇

Continuing the momentum from my recent statistical research, this time I looked into Kaspa’s security budget - a PoW-based asset. I ran into a few challenges (most APIs were paid, so I had to find a workaround, and a technical upgrade whose effect mathematically cancels out), but here’s the result.

As the chart shows, the daily security budget peaked at roughly $2M per day, before collapsing to just $145k - a ~93% decline. This drop is driven by a combination of a sharp price correction (from $0.20 to $0.045) and an issuance schedule that effectively behaves like an annual halving.

This isn’t unprecedented - Bitcoin saw similar dynamics in its early days. But Bitcoin is the exception, not the rule. Most PoW alts don’t survive more than one or two cycles. I wouldn't go as far as declaring Kaspa dead, but there’s no doubt these are challenging times for the miners.

The takeaway for new PoW protocols is simple: make sure you have enough runway to fund security.

cc: @KaspaSilver @moshikrl I’d appreciate your take

8

18

149

11,724

16 Nov 2025

Wallet #1’s vast accumulation last month proves that real demand for KAS is extremely high: a single entity alone demanded more KAS than all miners combined could supply. Yet this exceptionally strong real demand is not reflected in Kaspa’s fiat price.

This is because Kaspa’s fiat price is being heavily suppressed by exchanges. Exchanges can suppress Kaspa’s price in multiple ways, including issuing Kaspa perpetual futures, manipulating order books/price oracles, and/or halting or delaying KAS withdrawals.

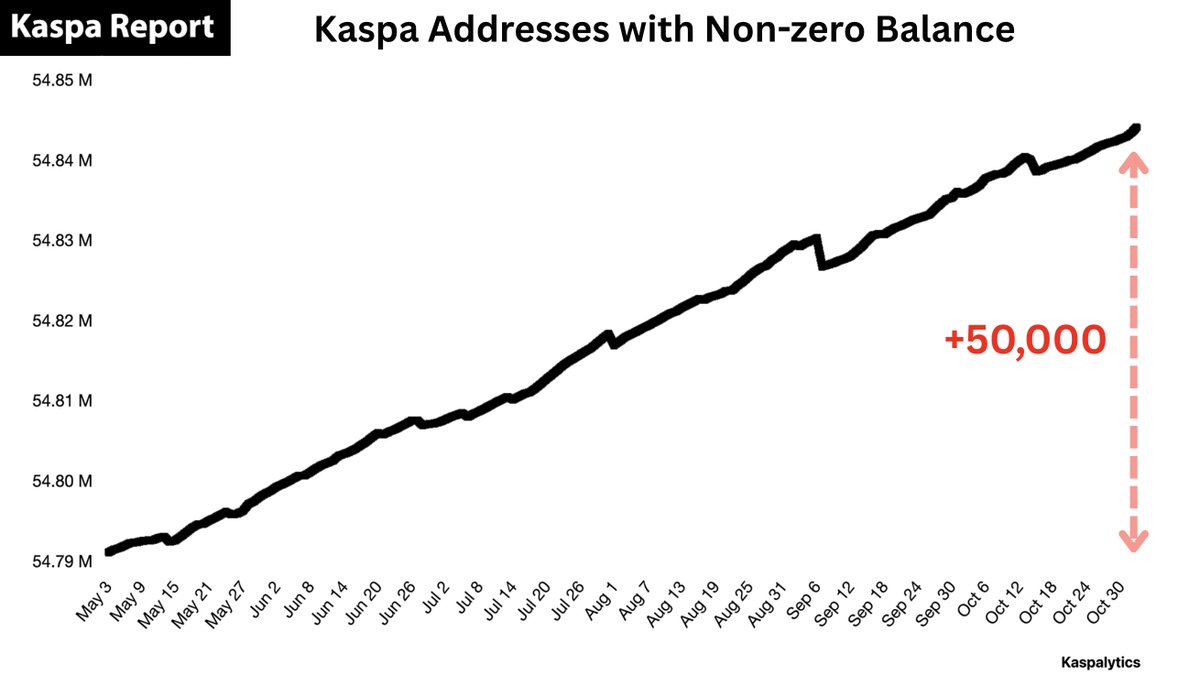

Consequently, fiat price is an unreliable measure of Kaspa’s real value. Certain on-chain metrics better capture the true value of Kaspa, and they cannot be easily manipulated. These metrics, such as inactive supply, suggest continued and reliable growth in the use of Kaspa as money.

Although it can be difficult to accept the idea of measuring Kaspa’s value in something other than fiat currency, a day will come when using fiat currency to measure Kaspa’s value will make no more sense than using Rai stones or cowrie shells to do so.

16 Nov 2025

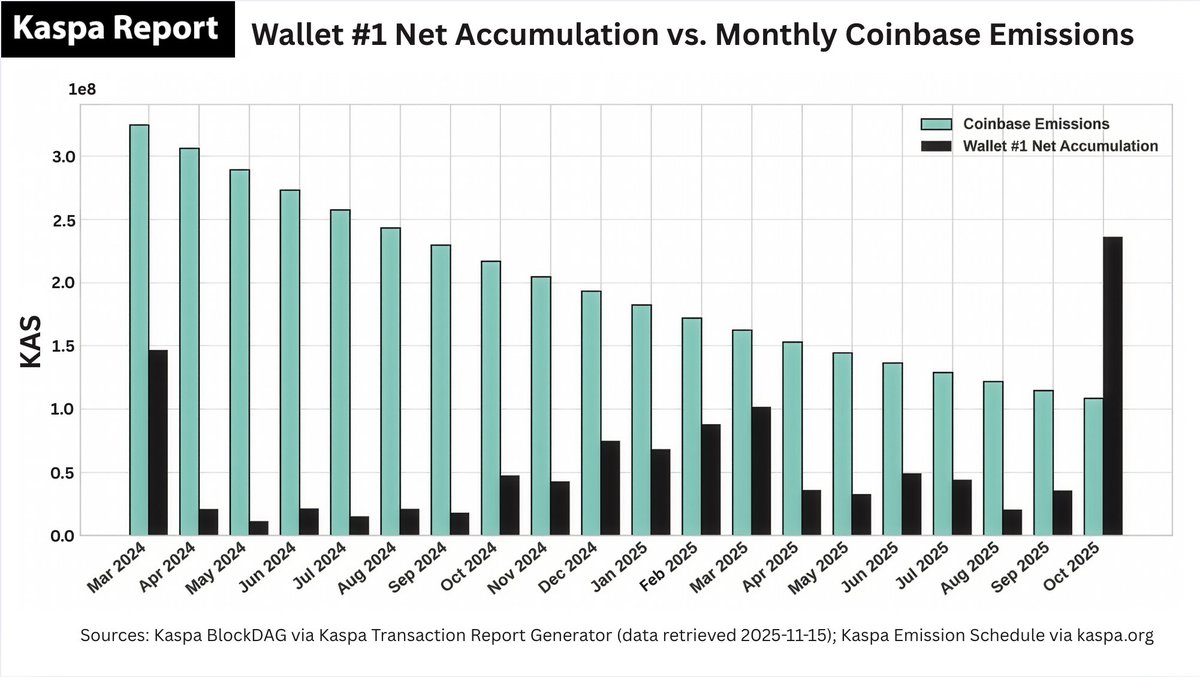

Kaspa’s Largest Wallet Accumulated More Than Double the New Supply of KAS in October

In October 2025, the holder of Kaspa’s largest address (ending in m7n4uk5a, hereafter “Wallet #1”) accumulated more than twice the total coinbase emissions generated that month.

On-chain data show that most inflows to Wallet #1 originated from an exchange that publicly stated that it is not associated with the address. This means Wallet #1’s accumulation concentrated KAS ownership, as the inflows were not simply the same owner moving funds between two addresses they controlled. Instead, KAS previously held by multiple entities became consolidated under a single holder.

The fact that this occurred during the same period in which the percentage of circulating supply held by the top 0.01% of addresses declined indicates that, even as Wallet #1 was increasing KAS concentration, the network as a whole was redistributing KAS from large addresses to smaller ones at a pace faster than Wallet #1 could offset. This means that despite Wallet #1's herculean attempt to centralize KAS ownership last month, the network's profound tendency toward decentralization proved resilient enough that redistribution still outpaced its accumulation.

The chart shows that October 2025 is the first month in which Wallet #1 accumulated KAS faster than new supply came into existence. Wallet #1's inflows spiked in the days following the October 10 market crash caused by Binance’s price oracle failure. The extreme price drop likely allowed Wallet #1 to accelerate its accumulation so drastically.

Given Kaspa’s rapidly declining new supply, an accumulation rate of this magnitude is unsustainable over the long term and substantially increases the risk of a major supply shock. With fewer new coins entering circulation each month, sustaining such inflows requires increasingly large volumes of KAS to be drawn from existing holders. Yet, on-chain data show that holders’ use of KAS for value storage increases over time, meaning the KAS available from existing holders tends to shrink with time.

In the years ahead, the magnitude of Kaspa’s supply shocks will likely be among the biggest ever observed in history. These shocks will occur concurrently with the opposite dynamics in global fiat currency supply (fiat currency supply will dramatically rise). The combination of these diametrically opposed dynamics will result in extreme deflation in the value of fiat currencies when measured in KAS. This is true even if demand for KAS remains constant. Any increase in demand for KAS would further amplify and accelerate that deflationary pressure, particularly since KAS supply is totally inelastic.

For additional detail on the entity most likely connected to Wallet #1, you can see our earlier report linked below.

5

29

154

7,687

16 Nov 2025

Kaspa’s Largest Wallet Accumulated More Than Double the New Supply of KAS in October

In October 2025, the holder of Kaspa’s largest address (ending in m7n4uk5a, hereafter “Wallet #1”) accumulated more than twice the total coinbase emissions generated that month.

On-chain data show that most inflows to Wallet #1 originated from an exchange that publicly stated that it is not associated with the address. This means Wallet #1’s accumulation concentrated KAS ownership, as the inflows were not simply the same owner moving funds between two addresses they controlled. Instead, KAS previously held by multiple entities became consolidated under a single holder.

The fact that this occurred during the same period in which the percentage of circulating supply held by the top 0.01% of addresses declined indicates that, even as Wallet #1 was increasing KAS concentration, the network as a whole was redistributing KAS from large addresses to smaller ones at a pace faster than Wallet #1 could offset. This means that despite Wallet #1's herculean attempt to centralize KAS ownership last month, the network's profound tendency toward decentralization proved resilient enough that redistribution still outpaced its accumulation.

The chart shows that October 2025 is the first month in which Wallet #1 accumulated KAS faster than new supply came into existence. Wallet #1's inflows spiked in the days following the October 10 market crash caused by Binance’s price oracle failure. The extreme price drop likely allowed Wallet #1 to accelerate its accumulation so drastically.

Given Kaspa’s rapidly declining new supply, an accumulation rate of this magnitude is unsustainable over the long term and substantially increases the risk of a major supply shock. With fewer new coins entering circulation each month, sustaining such inflows requires increasingly large volumes of KAS to be drawn from existing holders. Yet, on-chain data show that holders’ use of KAS for value storage increases over time, meaning the KAS available from existing holders tends to shrink with time.

In the years ahead, the magnitude of Kaspa’s supply shocks will likely be among the biggest ever observed in history. These shocks will occur concurrently with the opposite dynamics in global fiat currency supply (fiat currency supply will dramatically rise). The combination of these diametrically opposed dynamics will result in extreme deflation in the value of fiat currencies when measured in KAS. This is true even if demand for KAS remains constant. Any increase in demand for KAS would further amplify and accelerate that deflationary pressure, particularly since KAS supply is totally inelastic.

For additional detail on the entity most likely connected to Wallet #1, you can see our earlier report linked below.

12

62

251

16,118

16 Nov 2025

Link to earlier report about Kaspa’s largest address: x.com/KaspaReport/status/190…

17 Mar 2025

In this report, we pinpoint the probable owner of Kaspa's second-largest wallet and the three individuals primarily responsible for its inflows. In addition, we present a prediction regarding the wallet that is likely unknown even to its owner...

🧵1/24

4

12

2,122

Kaspa Report retweeted

19 Mar 2025

Not owning any Kaspa is always a bigger risk than owning some.

10

39

284

9,852