Joined March 2024

- Tweets 3,776

- Following 264

- Followers 127

- Likes 8,787

182 Photos and videos

Ken M Coin retweeted

Just a little thread documenting how unhinged @adam3us is in his attempts to have people NOT read the CAPTURE articles.

Let's start with the "sHinoBi deBunKed iT in MinuTes!" ones:

16

33

158

10,302

Ken M Coin retweeted

Jun 17

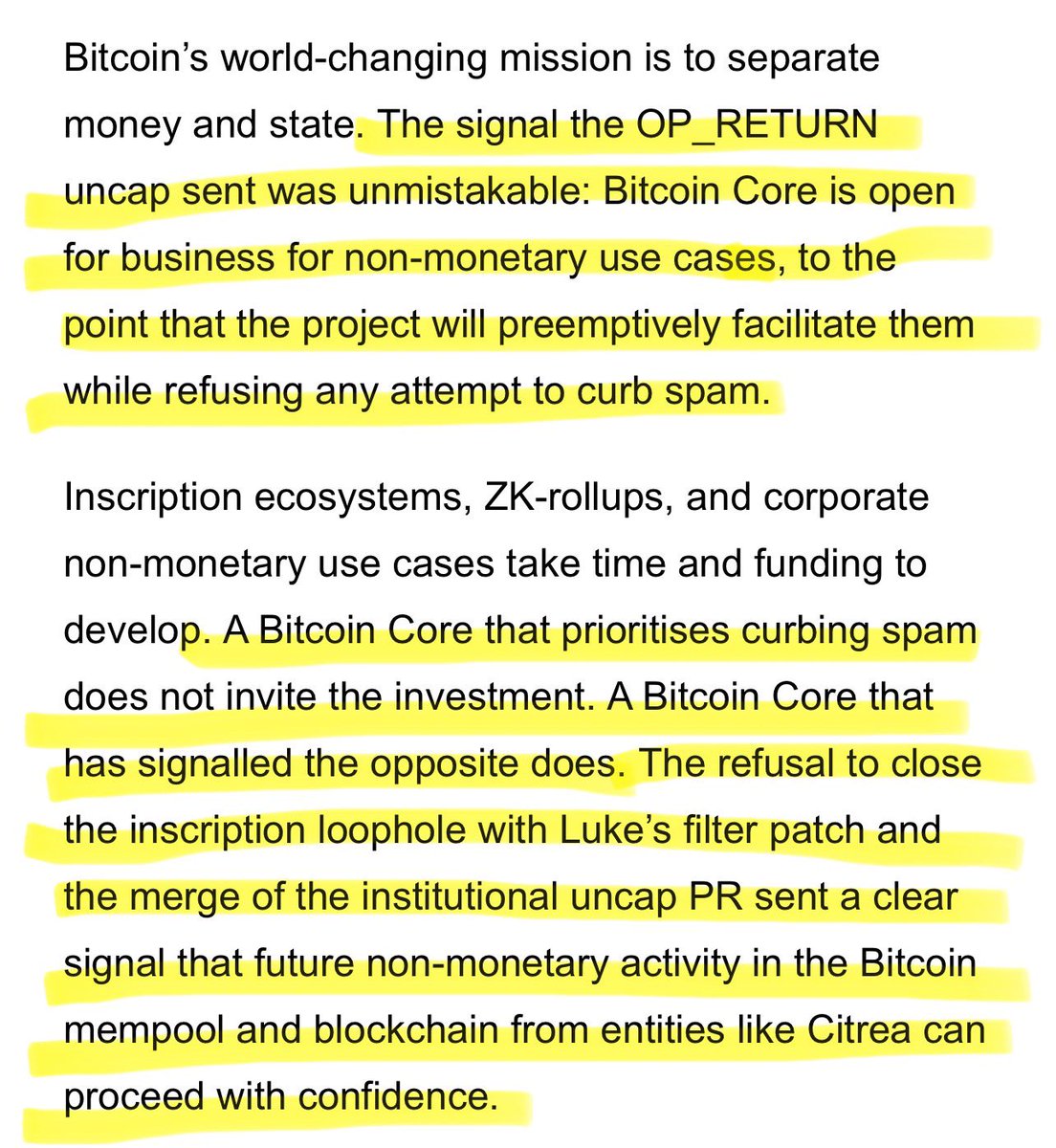

“The signal the OP_RETURN uncap sent was unmistakable: Bitcoin Core is open for business for non-monetary use cases, to the point that the project will preemptively facilitate them while refusing any attempt to curb spam.”

11

38

142

8,991

Ken M Coin retweeted

Jun 17

Where do you stand?

19%

Core is fine

55%

BIP-110

26%

Neutral/confused

627 votes • Final results

42

70

167

27,699

Ken M Coin retweeted

Jun 17

Elon's cult of followers do not care that he did a Nazi salute, they applaud him for it. Many of Elon and Trump's followers fly southern flags and belong to subversive organizations, like the KKK or neo-Nazi groups.

241

881

4,028

118,628

Ken M Coin retweeted

In one hour and forty five minutes our Monetary Bartender gives an update on drink prices, limits, closing time, blood alcohol warnings, etc.

What a ridiculous state of affairs that the most important price in capitalism, the price of capital itself, which is necessary to allocate capital intelligently, is set by one man and his committee. We claim free market capitalism and then price fix the price of money. 🤦♂️

50

95

855

27,713

Ken M Coin retweeted

Jun 17

I’m not employed by anyone.

I have no sponsors.

I’m not invested in anything else than BTC.

I don’t give a fuck about being shunned by influencers and talking heads.

I just want Bitcoin to succeed in separating money and state.

That’s why I support BIP-110

63

153

973

21,841

Ken M Coin retweeted

Jun 17

We get a lot of people who tell us to "go outside" or "touch grass". This is exactly how we would respond.

53

3,876

25,507

337,283

Jun 17

I'd like to see a weighted average of returns from runes. Can't believe all this Core v30 op_return bullshit was for some of the dumbest affinity scams to ever occur in crypto, led alone btc..

Jun 17

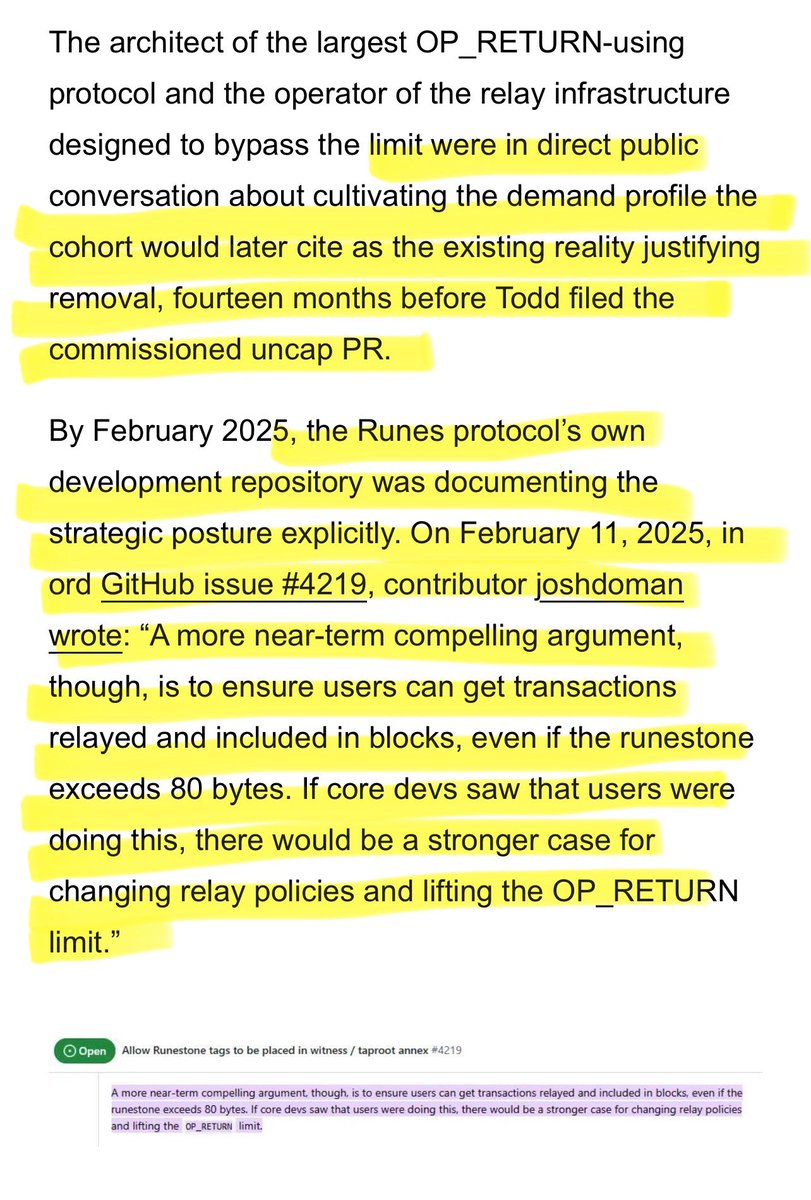

How the demand profile cited by Core as the justification to uncap OP_RETURN was cultivated.

1

16

Jun 17

It's all so obvious and out in the open. Core corrupted themselves for power and money. Not complicated.

1

7

Jun 17

2 Feb 2017

Iran was on its last legs and ready to collapse until the U.S. came along and gave it a life-line in the form of the Iran Deal: $150 billion

14

Jun 17

Sometimes the AI do be hittin tho

Jun 15

JD Vance heading to the morning shows to confirm US offered $300 BILLION to the Iranians:

1

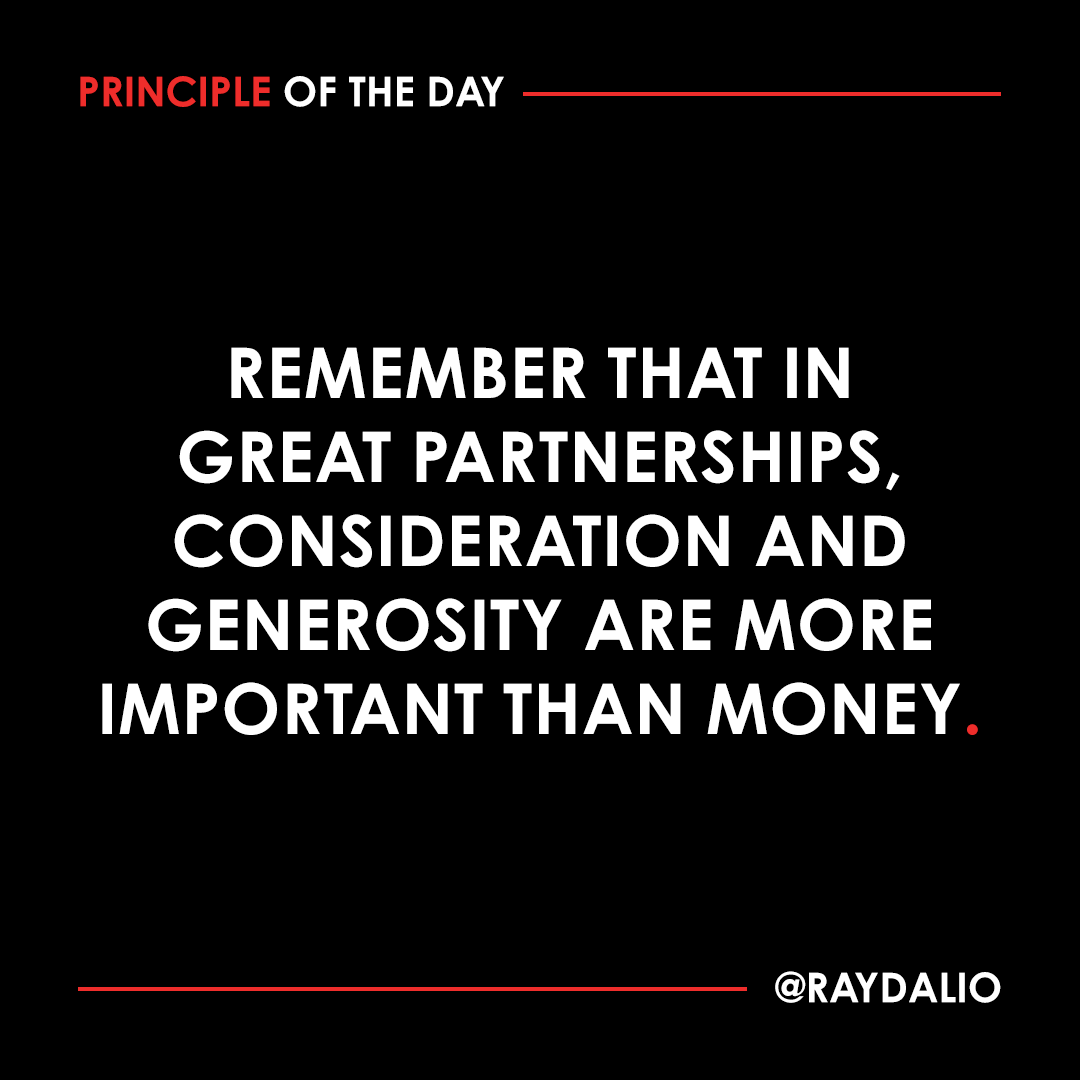

Someone who doesn't have much can be more generous giving a little than a rich person giving a lot. Some people respond to the generosity while others respond to the money. You want the first type with you, and you always want to treat them generously.

When I had nothing, I was as generous as I could be with people who appreciated my generosity more than the higher levels of compensation others could afford to give them. For that reason, they stayed with me. I never forgot that, and I made a point of making them rich when I had the opportunity to do so. And they in turn were generous to me in their own way when I needed their generosity most. We both got something much more valuable than money--and we got the money too.

Remember that the only purpose of money is to get you what you want, so think hard about what you value and put it above money. How much would you sell a good relationship for? There's not enough money in the world to get you to part with a valued relationship. #principleoftheday

53

103

717

66,101

Ken M Coin retweeted

Jun 16

$300bln could build 731,000 average single family homes, by the way

About $1,920 per working American

Imagine if that amount of money was invested in our own people, to fix problems in America

$1920 per American invested into our schools, might help our atrocious literacy rate

Jun 16

BREAKING: 🇺🇸🇮🇷 More than half of the $300 Billion in reparations for Iran has already been ‘committed’, per Reuters

17

12

94

4,854

Jun 16

Oh wow look, some more dishonest bullshit from Core, that inconveniently destroys their entirely contrived position

7

Jun 16

Getting to the heart of the bullshit

5

Jun 16

Adam hack coming with more irrelevant FUD while real bitcoiners do the work

Jun 16

Everything is sourced, Adam.

Your narrative doesn’t work.

1

Ken M Coin retweeted

Jun 15

Parker, this response actually proves the point I was making.

The entire purpose of correcting your framework was to help you explain exactly this issue correctly.

You are taking a Bitcoin treasury company whose common equity is structurally designed to have positive beta to Bitcoin, isolating a period that begins near Bitcoin’s late-2024 peak, and then highlighting that the common equity underperformed Bitcoin during a period where Bitcoin moved from that peak into a bear market.

Of course it did.

That is not a refutation of the thesis. That is how positive beta works.

If you isolate a period where Bitcoin peaks and then enters a drawdown, you should expect a company designed to amplify Bitcoin exposure to underperform Bitcoin during that specific period. That is not some surprising discovery. It is the expected behavior of the structure.

The entire thesis of Strategy, and the broader thesis behind what Strive is pursuing, is not that common equity will outperform Bitcoin over every arbitrary short-term interval. That has never been the claim.

The thesis is that over a long enough time horizon, if Bitcoin continues to go up and to the right, a company using the right structure can amplify Bitcoin exposure and outperform Bitcoin through that structure.

That structure matters. The ability to issue long-duration, structurally attractive liabilities against Bitcoin exposure matters.

That is the point.

As Bitcoiners, we are supposed to understand low time preference. We are supposed to zoom out. We are supposed to understand that cherry-picking a window from a local peak into a drawdown does not tell you whether the strategy works over the relevant time horizon.

Since Strategy began its Bitcoin strategy in 2020, the total return of the common equity has outperformed Bitcoin. That is the cleanest long-term test of whether the structure has worked.

Even in your original 2024 framing, the proper analysis on a total return basis for a single share showed outperformance. Then, when you shifted to a weighted average issuance argument, the issue became whether you were doing that analysis consistently.

You were not.

If you want to analyze common equity issued over time, you cannot simply take the weighted average price at which equity was issued and then compare it to Bitcoin over a return period that begins before much of that equity existed.

That was the original flaw.

You need to make the entire analysis internally consistent. If you use a weighted average equity issuance price, then you also need a weighted average issuance date. You then need to compare that to Bitcoin over the comparable cash-flow-weighted time period.

In other words, you need to match the dollars raised, the dates those dollars were raised, the price at which equity was issued, and the Bitcoin price over the same comparable timing.

You cannot weight one side of the analysis and then use an unweighted or mismatched start date on the other side.

That is not attribution. That is a framework error.

Your revised point appears to be moving closer to the right framework, but the conclusion you are drawing is still not the devastating critique you think it is.

The TLDR of your argument is now effectively this:

If you buy amplified Bitcoin exposure near a Bitcoin cycle peak, and then Bitcoin enters a bear market, that amplified Bitcoin exposure may underperform Bitcoin over that selected period.

Correct.

That is what should happen.

Again, that is not a refutation of the strategy. That is the expected outcome of positive beta in a Bitcoin drawdown.

The real question is not whether common equity can underperform Bitcoin over a cherry-picked period from a local peak into a bear market. The real question is whether the structure is attractive over the long run for investors who are bullish on Bitcoin and willing to maintain a low time preference.

My view is yes.

If you are bullish on Bitcoin over the long run, then a company that uses long-duration liabilities, digital credit, and a capital structure designed to accumulate and amplify Bitcoin exposure can be attractive.

If you are not bullish on Bitcoin, or if you are evaluating it over short windows from local peaks into drawdowns, then of course you may not like it.

That is fine.

But those are different debates.

What is not fine is presenting a flawed attribution framework as if it proves the strategy has failed.

Parker quote-tweeted my earlier response, and there have now been several replies across this discussion. I would strongly encourage people to read the full exchange carefully, and responses between Parker and @CJ_Bitcoin.

I think these back and forths are illuminating because it shows the core deficiencies in Parker’s analysis: inconsistent time periods, mismatched frameworks, selective windows, and conclusions that do not actually follow from the math being presented.

I do not think that is malicious. I do think it is analytically wrong.

And when the analysis is wrong, the conclusion becomes misleading, even if that was not the intent.

To be very clear, I am obviously a fan of people buying Bitcoin directly and putting it in cold storage. That is the purest expression of the asset.

But that does not mean every other structure is invalid.

A Bitcoin treasury company is a different instrument. It has different risks, different return drivers, different capital structure dynamics, and different upside and downside behavior.

If you want pure Bitcoin, buy Bitcoin.

If you want a structure designed to amplify Bitcoin exposure over time, then you evaluate that structure on its own terms.

But you do not evaluate amplified Bitcoin exposure by selecting a period from a Bitcoin peak into a drawdown and then acting surprised when positive beta works in both directions.

That is the entire point.

The structure is attractive if you are bullish on Bitcoin, understand the capital structure, and have a low time preference.

If you are not bullish on Bitcoin, or if your framework is short-term price comparison from a local high, then you probably will not find it attractive.

But that is a difference in thesis, not proof that the strategy has failed.

Investors deserve a higher-quality conversation than this.

Back to work.

42

42

467

37,754

Ken M Coin retweeted

Jun 16

Call me crazy, but I think parents should determine what their teenagers do online rather than the government.

And that governments shouldn't use system-level ID checks to identify and monitor everything.

401

963

9,572

232,340