Real estate and real estate note investor,author,consultant and professional speaker.

Joined January 2012

- Tweets 4,247

- Following 737

- Followers 1,141

- Likes 110

1,723 Photos and videos

Jun 10

Property Taxes! One of the Top Priorities when doing your research on notes.

Welcome to Watercooler Wednesday. Each week, we go over NEW case studies and updates in the note-investing industry. kevinshortle.com

2

27

Jun 5

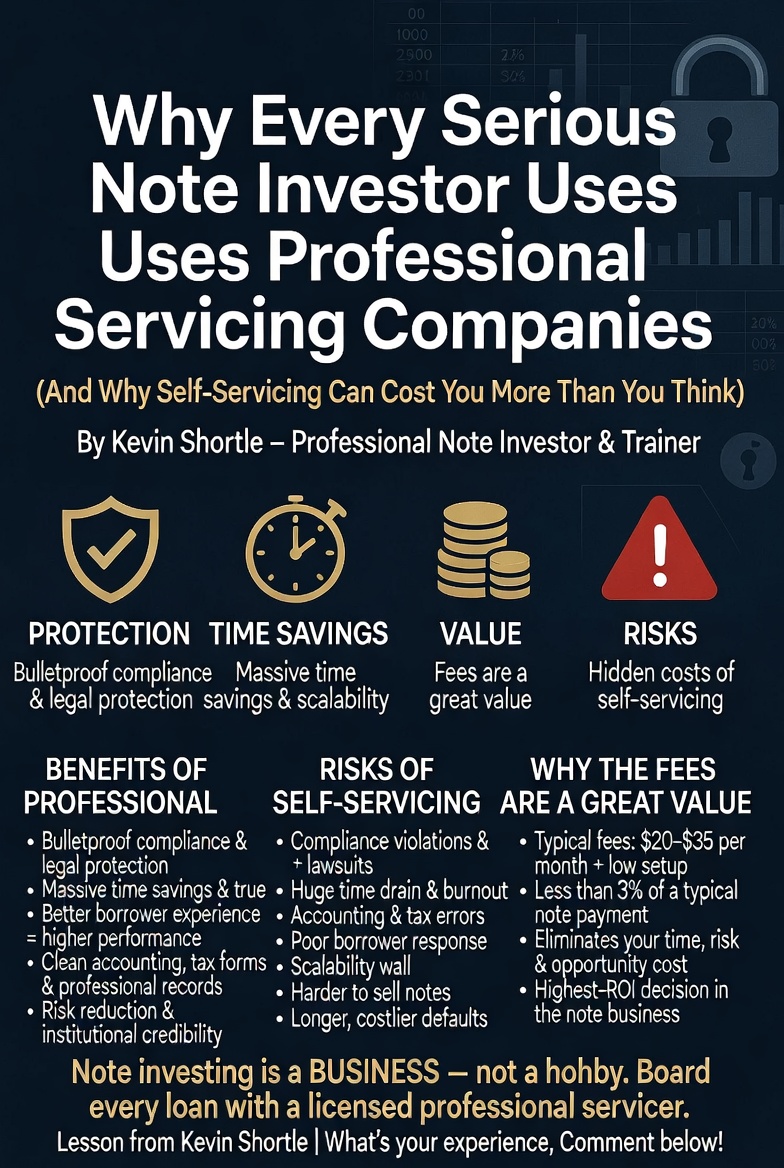

Why Every Serious Note Investor Uses Professional Servicing Companies (And Why Self-Servicing Can Cost You More Than You Think)

As someone who has been actively investing in notes for decades and training thousands of investors, I’ve learned one truth the hard way: the fastest way to turn a great-performing note into an expensive problem is to try servicing it yourself.

That’s exactly why I board every single loan I own with a licensed, bonded, and insured professional servicing company. In this article, I want to walk you through the real benefits of using a professional servicer versus going it alone, the actual risks of self-servicing, and why the industry-average fees are not only reasonable—they’re one of the smartest investments you can make in your note business.

What a Professional Note Servicer Actually Does

A good servicing company becomes your fully staffed back office. They handle:

• Collecting payments (ACH, checks, online portals)

• Disbursing your principal and interest on time

• Managing escrow (taxes and insurance when required)

• Sending accurate monthly statements and proper year-end tax forms

• Compliant delinquency management and loss mitigation

• Modifications, short sales, forbearance, or foreclosure coordination when necessary

• Maintaining audit-ready records with investor portals for 24/7 visibility

• Full compliance with RESPA, TILA, FDCPA, Dodd-Frank, and every state regulation

They turn your note portfolio into a truly passive, professional investment—so you can focus on what actually grows your wealth: finding and buying more quality notes.

The Clear Benefits of Professional Servicing

1 Bulletproof Compliance and Legal Protection

Note investing sits under heavy regulation. One wrong late notice, missed disclosure, or improperly handled Qualified Written Request can expose you to fines, borrower lawsuits, or even rescission of the entire loan. Professional servicers are licensed in every state they operate, carry bonding and insurance, and have dedicated compliance teams. You get protection you simply cannot replicate on your own.

2 Massive Time Savings and True Scalability

One or two notes might feel manageable. Ten or twenty quickly become a full-time job. Professional servicing frees you up to do what you do best—sourcing, underwriting, and closing new deals. Your time is far more valuable than chasing payments or reconciling spreadsheets.

3 Better Borrower Experience = Better Performance

Borrowers treat communication from a professional, licensed servicer differently than from an individual investor. This leads to fewer disputes, smoother collections, and higher long-term performance.

4 Clean Accounting, Tax Reporting, and Professional Records

You get accurate ledgers, automated 1098/1099s, and reports your CPA will love. When you eventually sell or assign the note, buyers and title companies prefer professionally serviced paper—it’s cleaner and more marketable.

5 Risk Reduction and Credibility

Servicers carry errors-and-omissions insurance and fidelity bonds that protect you against their mistakes. Your portfolio looks institutional and serious, which matters when you’re raising capital or exiting positions.

The Real Risks of Self-Servicing (This Is Where Most Investors Get Burned)

I see it all the time: new investors decide to self-service to “save money.” Within months they discover the hidden costs:

• Compliance Violations – Easy to make mistakes on notice timing, disclosure rules, or collection practices. Even one error can trigger regulatory complaints, lawsuits, or thousands in legal defense costs.

• Time Drain – Monthly statements, payment tracking, delinquency calls, tax reporting, and escrow management eat evenings and weekends. That time could be spent finding your next 10–20% yield note.

• Accounting Nightmares – Spreadsheets get messy fast. Errors in interest calculations or tax forms create problems with the IRS or your CPA.

• Poor Borrower Response – Personal collection efforts often get ignored or create disputes. Borrowers are more likely to push back against an individual than a licensed servicing company.

• Scalability Ceiling – You simply cannot grow beyond a handful of notes without hiring staff or burning out.

• Selling Problems – Notes without a clean professional servicing history are harder (and sometimes impossible) to sell at top dollar. Title companies and buyers often require it.

• Higher Default Costs – Handling foreclosures, bankruptcies, or loss mitigation without expert systems and procedures almost always leads to longer non-performance periods and bigger losses.

Self-servicing only makes sense for a tiny handful of ultra-simple, business-purpose portfolios where the investor already has legal and accounting support on staff. For almost everyone else—especially with consumer-purpose or residential notes—it’s a false economy that creates far more risk than it saves.

Are Servicing Fees Actually a Good Value?

Yes—and here’s why.

Industry-average fees are very reasonable: monthly servicing for a performing note typically runs in the $20–$35 range, with one-time boarding/setup fees usually between $100 and $200 per loan. Additional transactional fees (payoffs, modifications, BPOs, etc.) are standard and modest.

Now do the math on a typical $100,000 note yielding 9–12%. The borrower’s monthly payment is roughly $900–$1,100. A $25–$30 servicing fee represents less than 3% of that payment. You keep the vast majority of your yield while eliminating all the administrative work, compliance risk, and opportunity cost.

When you compare that small, predictable fee to the real cost of self-servicing—your valuable time (easily worth $100 per hour), potential legal bills from one compliance slip-up, lost deals because you’re too busy managing payments, and the difficulty selling non-serviced notes—the value becomes obvious. Professional servicing is one of the highest-ROI decisions you can make in this business.

Final Thought

Note investing is a business, not a hobby. Professional servicing is what separates the serious, scalable investors from those who eventually burn out or get burned by avoidable mistakes.

If you’re still self-servicing, I strongly encourage you to interview a couple of reputable, licensed servicing companies and board your next note the right way. Your portfolio, your time, and your peace of mind will thank you.

8

151

May 27

Beware of borrower-created notes and mortgages.

Welcome to Watercooler Wednesday. Each week, we go over NEW case studies and updates in the note-investing industry. kevinshortle.com

1

2

26

May 27

KEVIN SHORTLE - Real Estate Note Strategies

Why own the property when you can own the DEBT?At

BYOB Blueprint (May 28th - May 30th), I'm teaching:

How to be the bank, not the landlord

Why notes beat rentals in any market

Built-in security most investors don't understand

No tenants, toilets, or midnight calls. Just mailbox money. 30 years of note investing condensed into one session.

$47 gets you in. beyourownbank.com/byob-bluep…

1

9

May 23

I'll be speaking at the BYOB Blueprint 3-Day Event (May 28th - May 30th) alongside some of the brightest minds in private banking, wealth building, legacy creation, and financial strategy.

3 days. One mission:

Teaching you how to think, plan, act, and invest like the wealthy.

This is the same type of financial system the wealthy have used for generations — and now it’s your turn to learn how it works.

✅ Private Banking Strategies

✅ Wealth Building Principles

✅ Legacy & Generational Planning

✅ Financial Education & Implementation

✅ Plus much more

🎟 $47 General Admission

🎟 $97 VIP (Includes 2 Bonus Sessions Full Recordings)

Register here: beyourownbank.com/byob-bluep…

2

3

52

May 20

Welcome to Watercooler Wednesday. Each week, we go over NEW case studies and updates on the note investing industry. kevinshortle.com

This one shows how you have to double-check the agents’ work on BPO’s.

1

2

38

May 19

📷 Note Sellers: Why Experienced Buyers Will NEVER Pay 100% ITB on Your Freshly Originated Notes

You originate solid seller-financed loans at 11–12% interest… then list them for sale at full face value (100% Investment-to-Balance).

Here’s the hard truth from a buyer’s side:

You walk away with 100% of your cash immediately and zero future risk.

The buyer takes on 100% of the long-term risk — default, property decline, foreclosure costs, servicing, and illiquidity — on a brand-new, completely unseasoned note with zero payment history.

No seasoning = higher perceived risk.

11–12% at par = yield that doesn’t compensate for the downside.

Smart note buyers demand a fair discount (typically 8–25% off balance) to create a proper risk-adjusted return. That’s just how the market works.

Price your new notes realistically and they’ll sell fast to serious, well-capitalized buyers. Keep asking for 100% ITB and they’ll sit on the shelf.

Serious note originators — if you underwrite strong deals and are willing to price them fairly, contact me. Good paper at the right numbers always finds a home.

What’s your experience selling fresh notes? Drop it in the comments 📷

#NoteInvesting #SellerFinancing #RealEstateNotes #PrivateLending #PassiveIncome #NoteBuying

1

1

27

May 13

Welcome to Watercooler Wednesday. Each week, we go over NEW case studies and updates on the note investing industry. kevinshortle.com

This one goes into detail about real estate prices and loan performance.

1

2

50

May 6

Welcome to Watercooler Wednesday. Each week, we go over NEW case studies and updates on the note investing industry. kevinshortle.com

This one covers the steps to take right before and right after the closing.

1

2

2

48

Apr 29

Welcome to Watercooler Wednesday. Each week, we go over NEW case studies and updates on the note investing industry. kevinshortle.com

This one covers the correct and incorrect ways to calculate return on investment with notes.

1

2

36

Apr 23

1

31