Joined June 2009

- Tweets 62,029

- Following 1,394

- Followers 103,739

- Likes 24,987

33,231 Photos and videos

Pinned Tweet

Bull Bear Report: Week Of June 11, 2026

A lot of stuff to cover this week from the SpaceX IPO, the end-of-week market rally that keeps the #bull trend intact, and why the most recent #CPI report we quickly "read through" by the stock and bond markets.

open.substack.com/pub/lancer…

1

2

10

2,644

Jun 13

This is a great reminder why Capitalism is the best economic system in human history...then...and still is today. You just have to be willing to do the work.

Jun 12

The first trillionaire in human history

- Elon Musk

- Born in South Africa

- Bullied relentlessly as a kid

- Immigrated to North America

- Arrived with a backpack and a dream

- Built Zip2 with his brother

- Sold it 4 years later for $300 million

- Co-founded PayPal with the profits

- Revolutionised digital payments

- Sold PayPal to eBay for $1.5 billion

- Bet everything on Tesla and SpaceX

- Got mocked for electric cars

- Got laughed at for reusable rockets

- Nearly went bankrupt in 2008

- Kept building anyway

- Turned Tesla into the world’s most valuable automaker

- Made EVs mainstream and transformed the automotive industry

- Made reusable rockets a reality

- Reduced the cost of reaching space by 95%

- Sparked the modern commercial space race

- Built Starlink and connected millions around the world to high-speed internet

- Turned SpaceX into the most valuable private company in history

- Bought Twitter for $44 billion

- The world said he overpaid

- He was called reckless, stupid & crazy

- Advertisers fled, media declared it dead

- Critics called it the worst acquisition in tech history

- Renamed it 𝕏

- Rebuilt the platform anyway

- Turned it into one of the most influential platforms on Earth

- Launched xAI and accelerated the global AI race

- Sent astronauts to space

- Is trying to get humans to mars

- Created millions of jobs

- Generated hundreds of billions in value

- Inspired an entire generation of builders

Before:

- Failed repeatedly

- Worked insane hours

- Slept in factories and offices

- Got bullied, laughed at and mocked

- Constantly told “it’s impossible”

- Kept building anyway

- Made it possible

Today:

- Richest person on Earth

- First trillionaire in human history

- Largest IPO in history $1.77 trillion

Most people quit when the world laughs at them.

Elon Musk built the future instead.

Love him or hate him…

Nobody has changed more industries in a single lifetime.

Payments. Cars. Energy. Space. Social Media. Communications. AI.

History won’t remember the people who said it couldn’t be done.

It will remember the people who did it anyway.

Congratulations Elon.

The first trillionaire. 🚀

8

7

67

6,891

Jun 13

This has to be the best X post, and comment, I have seen in a long time. 😅😅

7

7

112

11,653

Jun 12

Gold Accumulation Is Not De-Dollarization

In this Short video, Brent Johnson @SantiagoAuFund and I break down the relationship between #gold, Treasury #bonds, and central bank reserves, explaining why gold accumulation is often a portfolio management decision rather than a de-dollarization signal.

Many investors interpret rising central bank gold purchases as evidence that the world is abandoning the U.S. dollar, but the reality is far more nuanced.

Central banks hold reserve assets to facilitate international trade, manage liquidity, and preserve purchasing power. For decades, U.S. Treasuries have been a cornerstone of those reserves because they provide both safety and interest income. Gold serves a similar reserve function, but its return depends primarily on price appreciation rather than #yields.

When #interestrates rise, bond prices fall, making gold relatively more attractive. In that environment, reserve managers may choose to increase gold holdings while reducing Treasury exposure. That does not necessarily signal a rejection of the dollar system. It is often a response to changing market conditions and portfolio management considerations.

Geopolitics also plays a role. Following the freezing of Russian assets in 2022, many countries reassessed the risks associated with holding reserves that could potentially be subject to sanctions. Gold offers advantages because it is harder to freeze or confiscate. China, for example, increased its gold holdings while also restructuring parts of its Treasury exposure to reduce perceived sanction risk.

So, gold accumulation is not the same thing as de-dollarization. Gold and #Treasuries are both reserve assets, and central banks regularly adjust the balance between them based on yields, market conditions, and geopolitical considerations.

Brent @SantiagoAuFund also challenges a common contradiction among critics of central banking. Many argue that central bankers are responsible for excessive money creation, debt expansion, and financial distortions, yet often praise their gold purchases as evidence of foresight.

He argues that while central bankers may be misguided or overly confident, they are not unintelligent. Managing the modern global financial system is extraordinarily complex, and the fact that the system continues to function despite repeated predictions of collapse suggests a level of skill that should not be ignored.

Gold buying may be increasing, but the broader message is not that the dollar is dying. It is that central banks are adapting to a changing financial and geopolitical landscape while continuing to operate within a dollar-centric global system.

Check out our comprehensive "15 Trading Rules" guide ▶️realinvestmentadvice.com/res…

This guide includes practical rules for managing positions, taking profits, controlling risk, and avoiding the emotional mistakes that often hurt returns during major market corrections.

If you like this video, please ❤️like and 🔁retweet

📺Full episode: youtube.com/watch?v=XnTrl2kb…

Catch me daily on The Real Investment Show: youtube.com/@TheRealInvestme…

12

11

101

14,355

Lance Roberts retweeted

Jun 11

The Structural Case For Continued Dollar Strength $DXYZ

In this Short video, Brent Johnson @SantiagoAuFund and I break down the structural forces supporting continued #USdollar dominance, from global trade and debt markets to reserve holdings and crisis-driven demand.

Despite years of predictions about the dollar’s demise, the global financial system remains deeply dependent on it. The key reason is that the #dollar is far more than a currency—it is the backbone of global trade, credit, funding markets, and financial infrastructure.

The dollar market outside the United States is actually much larger than the one inside it. Trillions of dollars of debt are owed by foreign governments, corporations, and banks. Much of that borrowing occurs between non-U.S. entities, yet it is still denominated in dollars.

That means the rest of the world owes enormous amounts in a currency it cannot create or control.

Roughly 58% of allocated global foreign exchange reserves are held in dollars, compared with about 20% in euros. Around half of global trade is invoiced in dollars, including transactions where the United States is not involved. The eurodollar system, the Treasury market, the SWIFT network, and the global banking infrastructure all reinforce the dollar’s dominant position.

Many investors point to central banks increasing their #gold $GLD holdings as evidence that the dollar is losing relevance. Gold has indeed become a larger share of reserves, but part of that shift reflects higher gold prices and lower Treasury prices as #interestrates have risen. Foreign ownership of U.S. #Treasuries remains near all-time highs, suggesting the world has not abandoned dollar assets.

The most overlooked point is what happens during a crisis. Countries may hold gold as a neutral reserve asset, but when they need liquidity, they often sell gold to obtain dollars. During periods of stress (like the Iran war), demand for dollars frequently rises because global trade, debt servicing, and commodity purchases still rely on them.

So, de-dollarization may be happening at the margins, but replacing the dollar is far more difficult than many assume. The structural foundations supporting dollar demand remain firmly in place, and in moments of uncertainty, the world still turns to dollars first.

Check out our comprehensive "15 Trading Rules" guide ▶️realinvestmentadvice.com/res…

This guide includes practical rules for managing positions, taking profits, controlling risk, and avoiding the emotional mistakes that often hurt returns during major market corrections.

If you like this video, please ❤️like and 🔁retweet

📺Full episode: youtube.com/watch?v=ppkqABin…

Catch me daily on The Real Investment Show: youtube.com/@TheRealInvestme…

6

17

71

13,344

Jun 12

The Truth About The K-Shaped Economy

While most of the media headlines have grabbed onto the "K-Shaped" economy to frame arguments for economic disparity, the reality is that the middle class shrunk because they moved up the wealth matrix.

open.substack.com/pub/lancer…

5

5

20

3,550

Jun 11

Will Kevin Warsh Trigger The Next Correction?

Kevin Warsh will preside over his first FOMC meeting as Fed Chair next week.

While many are debating whether he could raise rates and spark a market selloff, the Fed is more likely to stay on hold than tighten further.

Stable #crudeoil prices and signs of demand destruction could eventually help bring inflation lower, potentially opening the door for rate cuts down the road. But for now, neither hikes nor cuts appear imminent.

That doesn't mean markets won’t sell off.

If the Fed were to unexpectedly signal another rate hike, a 10-15% correction would not be surprising, given how extended stocks are relative to longer-term trend measures.

Still, a rate hike itself would not be the catalyst. More likely, another event exposes vulnerabilities that already exist beneath the surface.

Another point – investors should stop obsessing over correction percentages.

The key question isn't whether the market falls 5%, 10%, or 15%. It's whether sentiment, positioning, and technical conditions have reset enough to create a favorable buying opportunity.

Today, the market looks very different from the environment that existed near the April 2025 lows. Back then, investor sentiment was extremely negative, allocations were low, and technical indicators were deeply oversold. Those conditions created a buying opportunity.

Now we have the opposite: extremely bullish sentiment, high investor optimism, aggressive positioning, and overbought conditions.

Historically, those ingredients are more common near market tops than market bottoms.

That's why we’ve been emphasizing risk management, rebalancing, and avoiding excessive exposure rather than aggressively chasing stocks higher.

For investors waiting to deploy cash, don't focus on the number. Focus on the conditions. The best opportunities emerge when fear, pessimism, and poor positioning replace the optimism and complacency that dominate today.

Check out our comprehensive "15 Trading Rules" guide ▶️realinvestmentadvice.com/res…

This guide includes practical rules for managing positions, taking profits, controlling risk, and avoiding the emotional mistakes that often hurt returns during major market corrections.

If you like this video, please ❤️like and 🔁retweet

📺Full episode: youtube.com/watch?v=ppkqABin…

Catch me daily on The Real Investment Show: youtube.com/@TheRealInvestme…

6

8

41

3,998

Jun 11

Bank of America’s research shows that elevated long-term earnings growth expectations have historically been associated with weaker subsequent equity returns, suggesting today’s exceptionally optimistic forecasts may leave the market vulnerable to disappointment.

2

21

113

6,177

Jun 11

Gains appear solid on the surface, but beneath it the foundation is thinner, with S&P 500 highs masking narrow breadth, still shy of Dot-Com-era extremes.

h/t @ISABELNET_SA

2

10

61

4,395

Jun 11

6-11-26 Why the Dollar Still Rules - Brent Johnson Interview x.com/i/broadcasts/1AKEmmDwP…

1

2

15

2,600

Lance Roberts retweeted

Jun 9

AI Won’t Save Us From The Next Credit Crisis

In this Short video, David Zugheri from RealFin Capital and Lance Roberts discuss one of the most persistent forces in financial markets: the credit cycle.

The economic growth is fueled by lending. Contrary to popular belief, money is not simply "printed" into existence. Much of it is created when banks extend loans, whether for homes, businesses, or investments. That credit then circulates through the economy, funding construction projects, hiring workers, supporting consumption, and driving growth.

The problem is that lending cycles rarely stop at a healthy balance point.

Throughout history, investors have constantly searched for higher yields, while lenders have looked for new places to deploy capital.

Residential real estate, commercial real estate, corporate credit, and other asset classes have all experienced periods of excessive lending.

The details change, but the pattern remains remarkably consistent: credit expands, risk-taking increases, optimism grows, and eventually excesses build up somewhere in the system.

David argues that borrowing itself is not inherently bad. Debt can be a powerful tool when used responsibly. It can help individuals buy homes, entrepreneurs build businesses, and investors create wealth.

The challenge is that financial markets are driven by incentives, and those incentives often encourage participants to push beyond reasonable limits.

One of the most interesting points in the discussion is the role of AI. While artificial intelligence may accelerate decision-making, capital allocation, and information flow, it will not eliminate human nature. Investors will still chase returns. Lenders will still compete for business. Markets will still experience periods of euphoria and excess.

In other words, AI may speed up future cycles, but it will not prevent them.

David believes another major lending-driven blow-up is likely at some point. He does not claim to know exactly where it will occur, but he argues that every cycle eventually creates a new area of excess.

For that reason, he emphasizes the importance of risk management, capital preservation, and recognizing that the next credit crisis may emerge from a different corner of the market than investors expect.

Technology changes. Human behavior does not.

Check out our comprehensive "15 Trading Rules" guide

▶️realinvestmentadvice.com/res…

This guide includes practical rules for managing positions, taking profits, controlling risk, and avoiding the emotional mistakes that often hurt returns during major market corrections.

4

8

36

7,082

Jun 10

6-10-26 Wives Take Over: Money, Marriage, and Real Talk - ENCORE x.com/i/broadcasts/1AKEmmbzo…

1

1

7

2,656

Jun 10

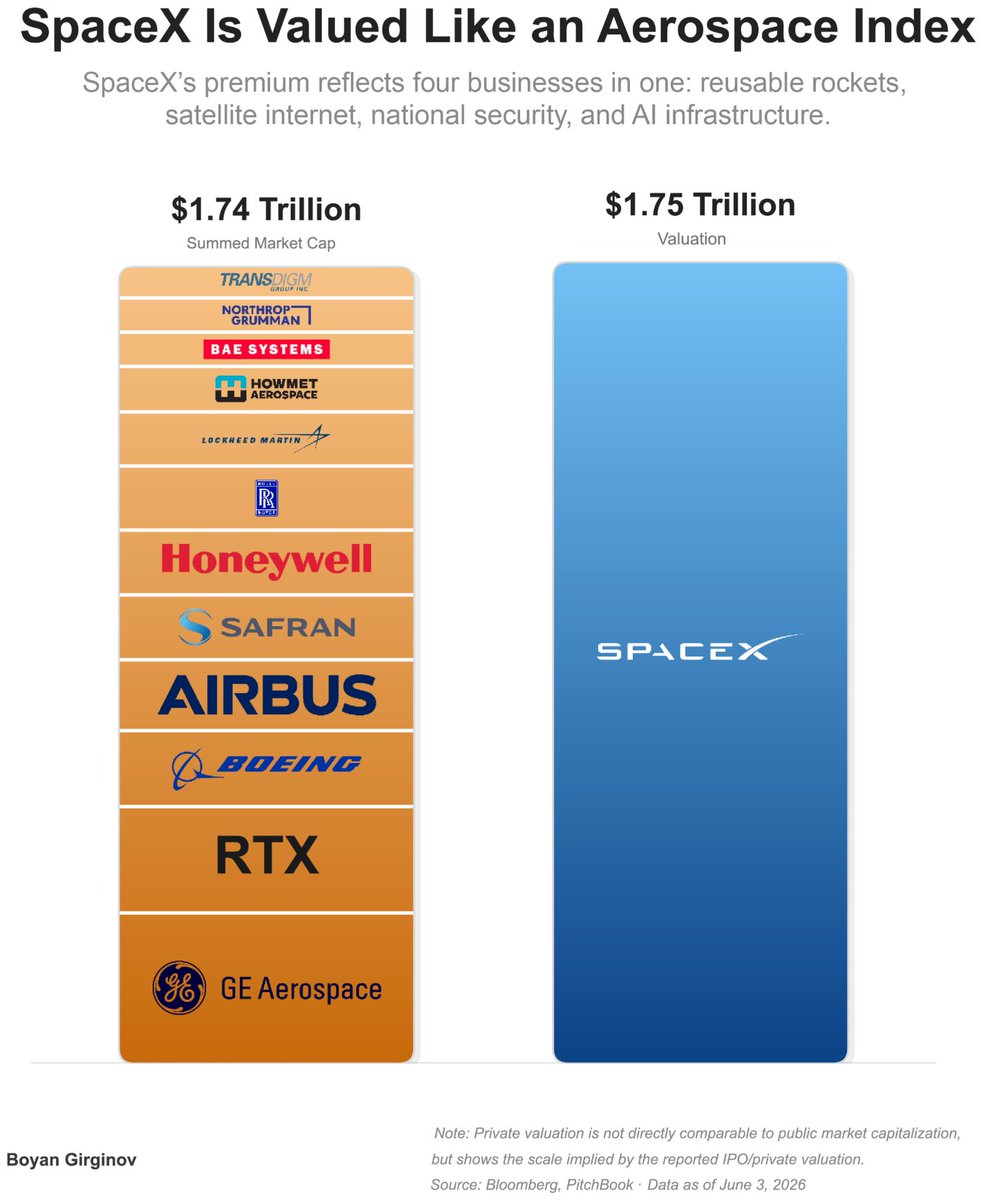

SpaceX’s reported $1.75 trillion valuation exceeds the combined market capitalization of 12 major aerospace and defense companies.

5

5

51

3,432

Jun 10

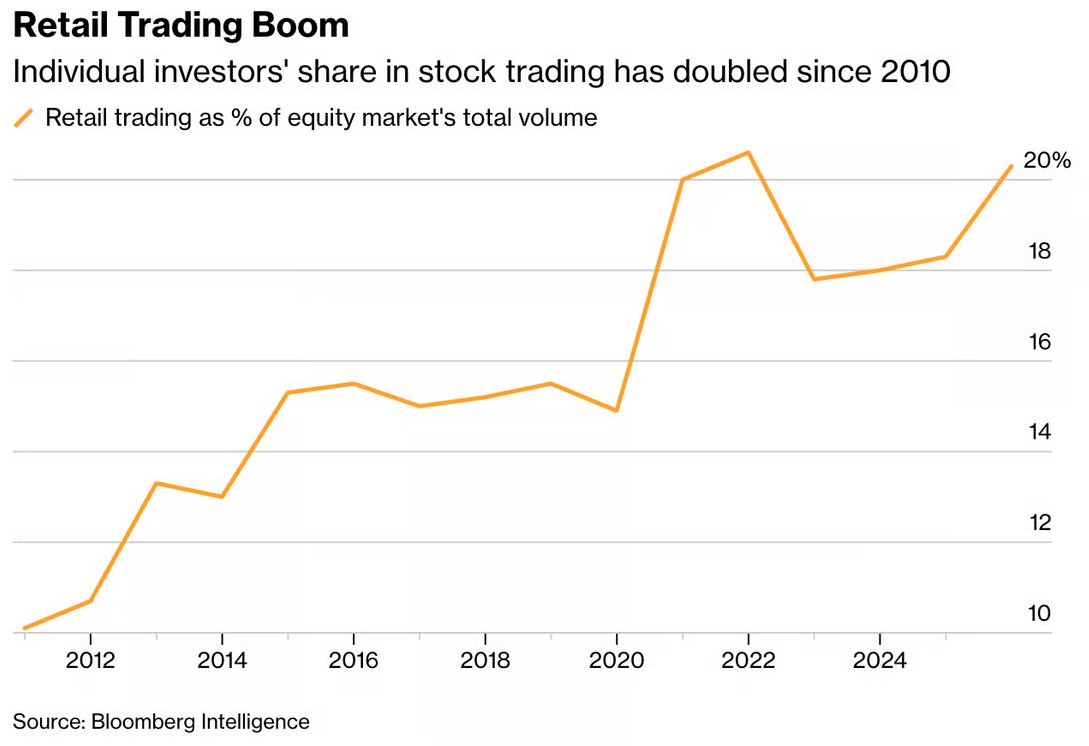

Last time retail investors were this heavily invested in equities was just before the 2022 correction. Maybe this time is different?

4

9

79

5,029

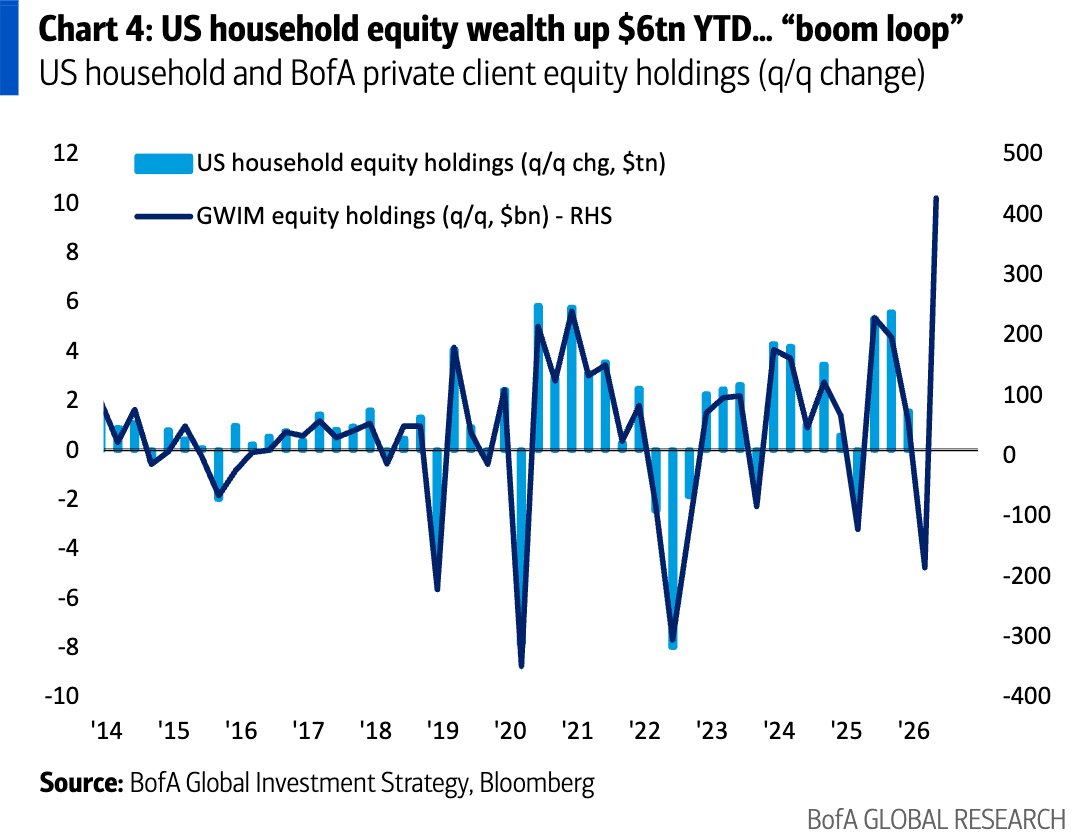

Jun 10

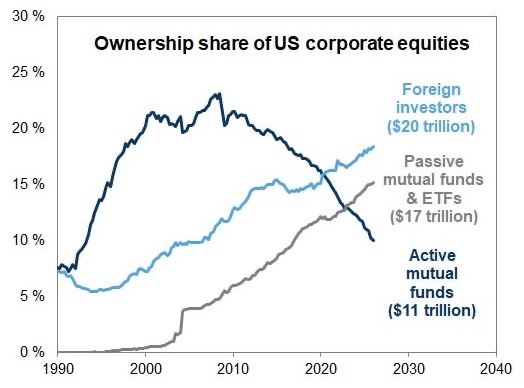

Another "thorn in the side" of the "Nobody wants the dollar" narrative. Yes. They. Do. Record high Treasury holdings and now record high Corporate Equity exposure which is all dollar based - via $GS

9

9

91

5,532

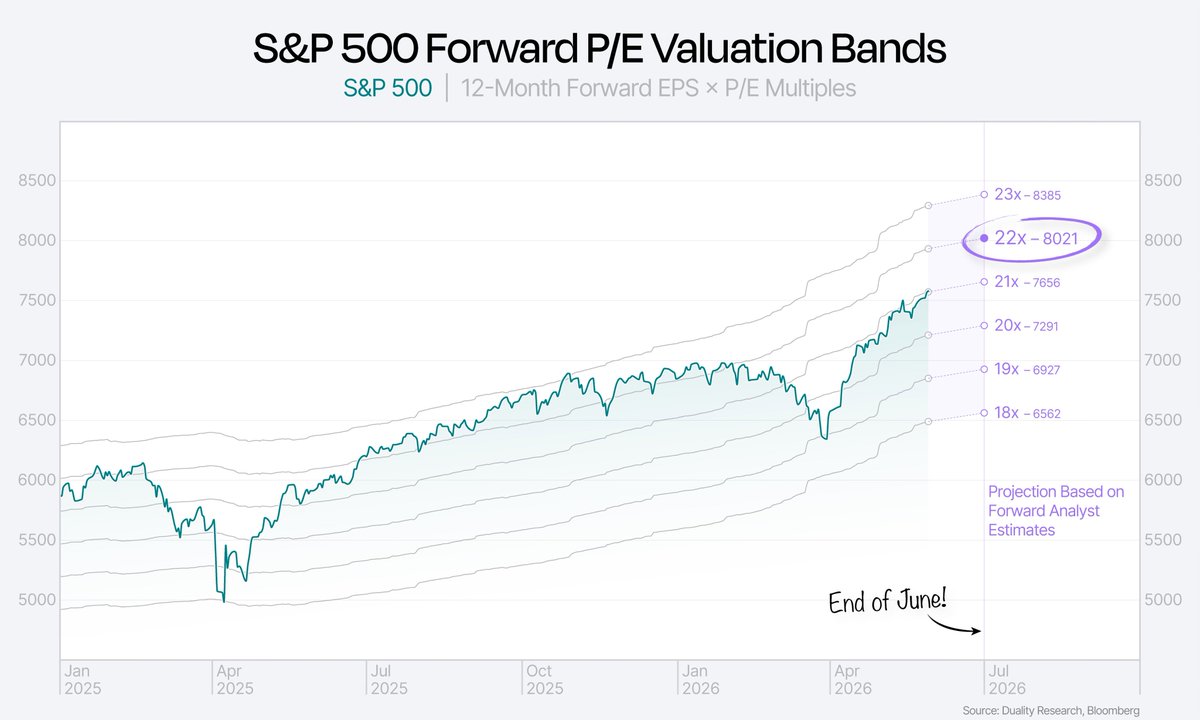

Jun 10

Here is a look at the S&P 500’s valuation bands. Based on forward estimates, Duality Research expects the index to reach 8,000 by the end of June if the market re-rates to a 22x forward multiple.

5

12

97

9,074