𝗖𝗿𝗲𝗮𝘁𝗼𝗿| 𝐂𝐨𝐦𝐦𝐮𝐧𝐢𝐭𝐲 𝐌𝐨𝐝𝐞𝐫𝐚𝐭𝐨𝐫 | 𝐑𝐚𝐢𝐝𝐞𝐫 | 𝐀𝐦𝐛𝐚𝐬𝐬𝐚𝐝𝐨𝐫 | 𝐊.𝐎.𝐋 | 𝐂𝐨𝐩𝐲𝐰𝐫𝐢𝐭𝐞𝐫 | 𝐒𝐞𝐦𝐚𝐧𝐭𝐢𝐜

Joined September 2025

- Tweets 7,568

- Following 1,207

- Followers 1,050

- Likes 16,348

905 Photos and videos

Pinned Tweet

Omg, I am eligible for the @base Advocate Recruitment role

What's your status. Lemme know please

44

9

227

8,787

LexanderofX🦅✝️.BASE.eth retweeted

Day 1 of Joining Arc dropping what i learnt from Arc today

Unified Balance Kit: The Missing Layer for Scalable Web3 Payments and Treasury Management

One of the biggest challenges in crypto today isn't moving money across blockchains—it's managing liquidity spread across multiple chains.

As the ecosystem expands, users and businesses increasingly hold assets on networks like Ethereum, Base, Arbitrum, Solana, and others. While this creates more opportunities, it also introduces a major operational problem: fragmented balances.

Imagine having 100 USDC on Base, 150 USDC on Arbitrum, and 250 USDC on Solana. Technically, you own 500 USDC, but in practice, those funds are isolated across different networks. To spend or move funds efficiently, users often need to bridge assets, manage gas fees on multiple chains, and navigate a complex web of infrastructure.

This is the exact problem Arc's Unified Balance Kit is designed to solve.

The Core Idea: One Balance, Any Chain

Unified Balance Kit introduces a simple but powerful concept: instead of treating every blockchain balance separately, it aggregates supported USDC balances into a single unified balance.

From a user's perspective, it doesn't matter where the funds are located. What matters is how much they have available and where they want to send it.

This approach shifts the focus away from chain-specific management and toward a seamless financial experience. The blockchain becomes the infrastructure layer rather than the product itself.

Why This Matters

For years, developers building payment and treasury applications have been forced to manage multiple complexities:

• Chain-specific integrations

• Cross-chain routing logic

• Liquidity distribution across networks

• Balance synchronization systems

• Settlement mechanisms

• Fee estimation and optimization

Every additional blockchain support increases engineering costs, operational overhead, and maintenance requirements.

Unified Balance Kit abstracts these complexities into a single integration, allowing developers to focus on building products instead of infrastructure.

A Better Treasury Architecture

One insight that stood out to me is how relevant this is for treasury management.

Most treasury systems today operate with fragmented liquidity. Funds are spread across different chains, requiring teams to constantly monitor balances, move capital, and ensure sufficient liquidity exists where it's needed.

Unified Balance Kit introduces a more efficient model where liquidity can be viewed and managed as a single pool rather than isolated pockets of capital.

For businesses handling payouts, payroll, settlements, or cross-border payments, this could significantly reduce operational friction while improving capital efficiency.

Improving the User Experience

The average user doesn't care about bridges, settlement layers, or routing protocols.

Users care about three things:

How much money they have.

How quickly they can access it.

Where they can send it.

By removing chain-specific complexity from the user experience, Unified Balance Kit helps create products that feel closer to traditional financial applications while maintaining the advantages of blockchain infrastructure.

This is a major step toward mainstream adoption because it aligns crypto products with how people naturally think about money.

The Bigger Trend: Chain Abstraction

What makes Unified Balance Kit particularly interesting is that it reflects a broader industry trend.

We're entering an era where the best Web3 applications may not emphasize the blockchain they're built on. Instead, they'll abstract away the complexity and deliver seamless experiences.

The winners won't necessarily be the applications with the most chains integrated—they'll be the ones that make those chains invisible to users.

Chain abstraction is becoming a design philosophy, and Unified Balance Kit is a strong example of that vision in practice.

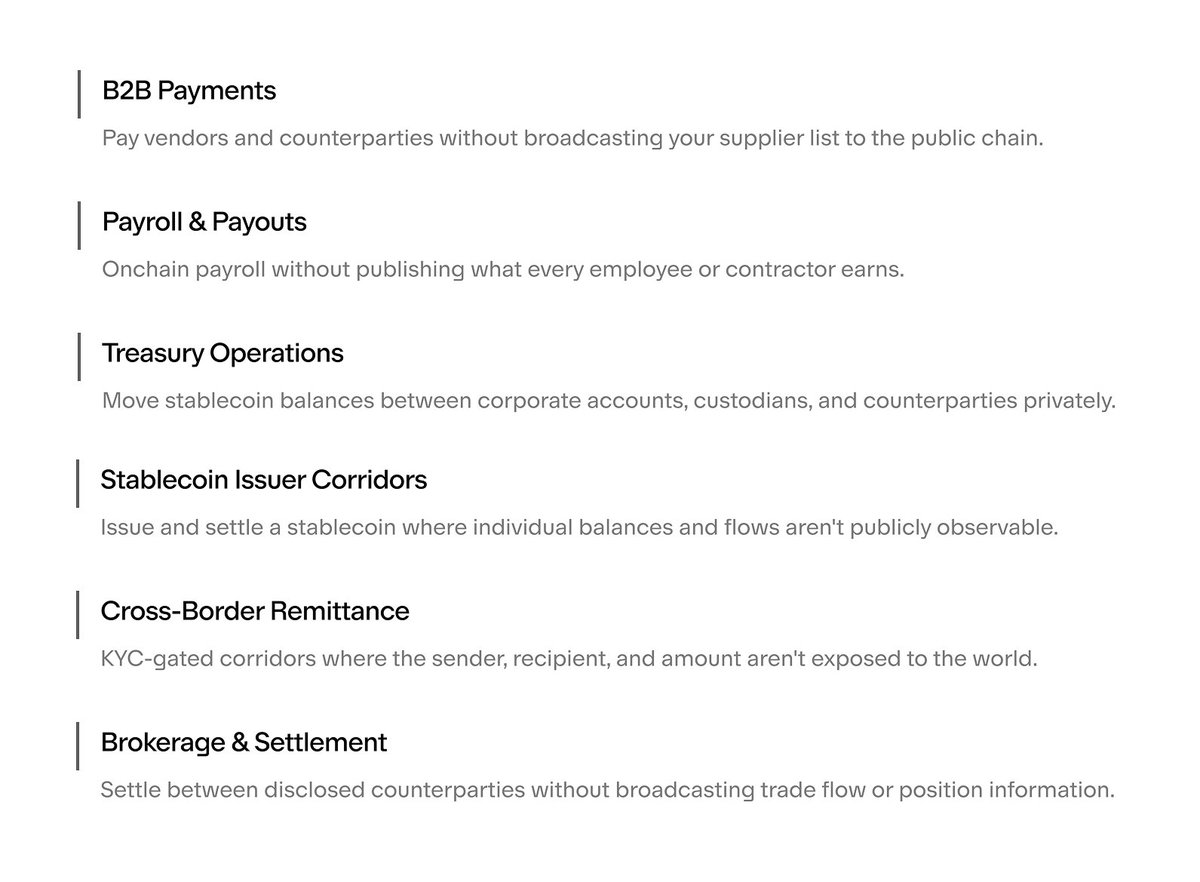

Potential Use Cases

The implications extend far beyond simple payments:

🔹 Fintech applications with unified customer balances.

🔹 Treasury platforms managing liquidity across multiple networks.

🔹 Payroll systems distributing funds globally.

🔹 Cross-border payment solutions.

🔹 AI-powered financial agents capable of spending from a unified pool without chain-specific decision making.

🔹 Enterprise settlement systems requiring efficient capital allocation.

Key Takeaways

After studying Unified Balance Kit, my biggest takeaway is that the future of Web3 infrastructure is not about adding more complexity it is about removing it.

The innovation isn't just cross-chain movement. The innovation is creating an experience where users no longer need to think about chains at all.

Unified Balance Kit represents a shift from chain-centric architecture to balance-centric architecture, where liquidity becomes programmable, portable, and accessible regardless of where it resides.

If this model gains adoption, we may look back at fragmented multi-chain balances the same way we look at dial-up internet today: a necessary stage of evolution, but not the end state.

The future of payments and treasury management is likely to be unified, chain-agnostic, and user-focusedand Unified Balance Kit provides a glimpse of what that future could look like.

1

1

7

49

LexanderofX🦅✝️.BASE.eth retweeted

introducing the upgraded @baseapp

with many more updates coming

121

47

458

21,665

LexanderofX🦅✝️.BASE.eth retweeted

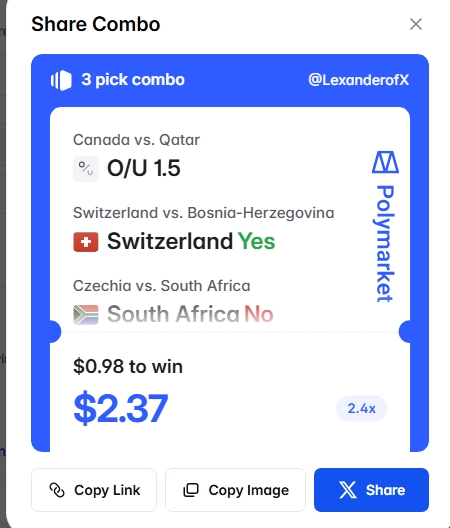

My 3 Combo on @Polymarket

A moving Man got nothing to lose🫥

7

1

10

117

LexanderofX🦅✝️.BASE.eth retweeted

Jun 17

every asset in the world can trade on base

tokenized stocks are up next

123

73

586

45,482

LexanderofX🦅✝️.BASE.eth retweeted

14h

Set your price, walk away.

Limit orders are on the @baseapp.

9

4

19

862

LexanderofX🦅✝️.BASE.eth retweeted

GM Bm Base

Another day to break Limits!

8

1

13

89

LexanderofX🦅✝️.BASE.eth retweeted

I’ve been building with AI for months

The funny part?

I’m not even a traditional developer.

From hackathons to testing new ideas, I’ve been using AI to turn concepts into working products, and @CodeXero_xyz has made that process much easier.

In this video, I break down:

• What CodeXero is

• How it helps builders ship faster

• Why AI-assisted development is changing how people build

• The fact that they are building on @base and backed by solid names

Would you use AI to build your next project?

Get started 👉🏾 codexero.xyz

15

4

39

1,827

LexanderofX🦅✝️.BASE.eth retweeted

Jun 17

🥷 NFTAlphaSpot × Ninji Collective 🥷

🎁 FLASH Giveaway LIVE NOW

How to enter:

✅ Follow @NFTALPHASPOT & @NinjiCollective

✅ Like & RT this post

✅ Tag 3 frens & Drop ADDY

⏰ Deadline: 24 Hours

16

13

18

198

LexanderofX🦅✝️.BASE.eth retweeted

Jun 17

検索エンジンが登場する前、Webサイトはバラバラに存在していました。

今、AIエージェントはMCPやマイクロサービスで同じ課題に直面しています。

1つの接続で、数千ものサービスへ。

@litebeam_xyz はエージェント経済のためのディスカバリーレイヤーを構築しています。ぜひチェックしてみてください👇

Jun 17

Litebeam x Base MCP Integration

1/

Litebeam is now available as a custom plugin for Base MCP.

One connection. An entire network of microservices, APIs, and agent-ready tools unlocked instantly.

3

2

10

645

LexanderofX🦅✝️.BASE.eth retweeted

Describe LOVE in one Piece

1

1

9

43

LexanderofX🦅✝️.BASE.eth retweeted

Jun 17

B20

11

4

46

1,182