@FoxBusiness Contributor | EVP of Market Strategy $PROP | Founder of TheBigSkinny.com | Investor

Joined August 2009

- Tweets 6,360

- Following 1,357

- Followers 9,175

- Likes 5,891

609 Photos and videos

Pinned Tweet

Jun 4

LIVE ON AIR!

ETFs Gone Wild: How to Find the Few Worth Owning,

with @fitz_keith and @davidanicholas x.com/i/broadcasts/1wxWjjyLR…

2

5

30

6,037

OpenAI cutting prices to compete with Anthropic.

This is the Blockbuster vs. Netflix price war moment for AI, as I shared with @Varneyco this week.

Drive down the price. Drive up the usage. Win the market.

We're in the early innings of a race that changes leaders every other week. Which one wins?

$NFLX

3

17

1,886

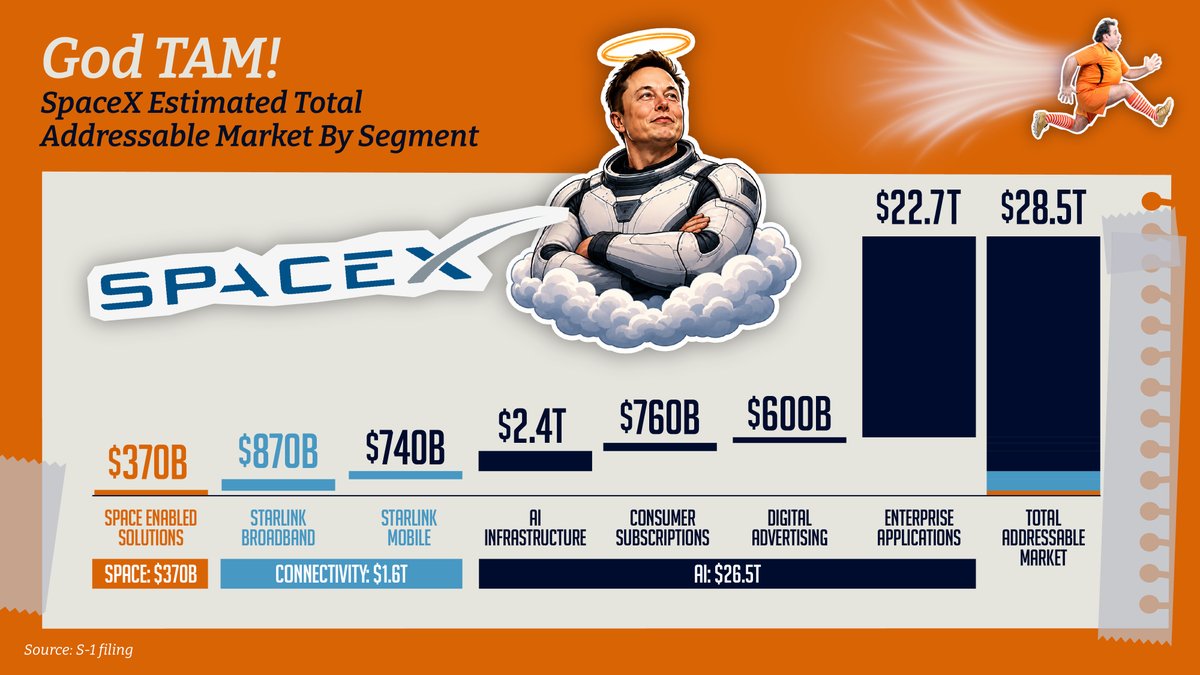

Had a blast starting my weekend with the @foxandfriends team talking $SPCX 👇

🚀 MAKING MARKET HISTORY: As SpaceX celebrates a record-setting IPO, Fox Business contributor @LouBasenese in on the company's impact on wealth creation, private markets, & the future of American innovation.

16

872

ICYMI: Oil dove $3 a barrel in real time while I was live with @SandraSmithFox @JessInskip_ on @AmericaRpts this week. All because President Trump canceled Iran strikes mid-segment.

We're seeing @CMEGroup oil futures back down in the $70's in October.

Will the declines hold and keep going lower next week?

$XLE

1

2

10

1,400

Varney asked why markets are rallying with inflation at 6.5%.

Is Trump finishing the job?

5

368

Happy Game 5 Saturday morning!

Joining @foxandfriends @GriffJenkins @CharlesHurt to talk yesterday’s historic $SPCX IPO ahead of tonight’s hopefully historic @nyknicks win!

1

8

293

Jun 12

Senator Surcharge ready to tax success every way and everywhere

Jun 12

Elon Musk just became the world's first trillionaire.

The typical American household would have to work more than 11 MILLION years to make Elon Musk's level of wealth.

We need a wealth tax.

6

492

Jun 12

Fighting the FOMO myself. Really hard with @marcuslemonis next to me saying, "Just buy 1 share." 🤣

“Don't buy into the IPO FOMO.”

@LouBasenese weighs the excitement surrounding SpaceX's IPO, arguing that history shows many of the biggest IPOs eventually pull back before rewarding long-term investors.

Are you buying or waiting for a better entry point?

2

9

714

Lou Basenese retweeted

"You should be at oil in the $70s... this is the sweet spot."

A peace deal with Iran is in the works and could be signed in the coming days.

@LouBasenese and @marcuslemonis discuss what the target oil price could look like in the coming months... Do you agree?

2

1

8

1,021

Jun 12

On $SPCX IPO day, the words of Benjamin Graham are fitting...

“In the short run, the market is a voting machine but in the long run, it is a weighing machine.”

Investors will be voting on Elon today not valuation. But eventually valuation will matter.

1

1

5

721

Jun 11

Oil below $80 by year-end is the market’s bet.

Oil above $90 today is the consumer’s burden.

Talking this and more with @SandraSmithFox on @AmericaRpts alongside @JessInskip_. Tune in ~1:30 pm!

5

360

Lou Basenese retweeted

Jun 11

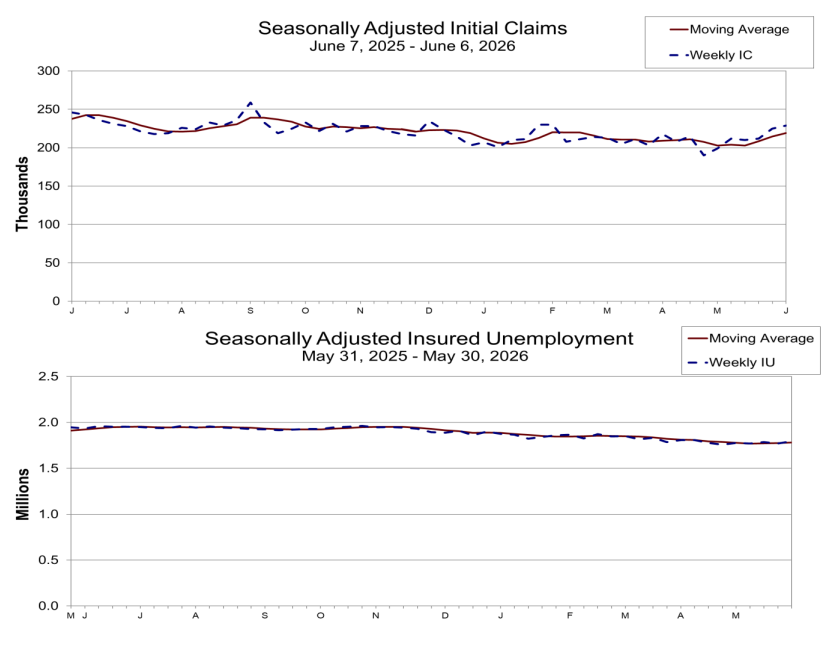

Initial UI claims rise to 4-month high but remain at a very low level (not even a quarter million) while continuing claims are still under 1.8 million; if there's stress in the labor market, it's not (yet) showing up here:

1

8

21

2,189

Jun 11

Another "buy the dip in chips" vote @RiggsReport 👇

Jun 11

On June 4th I posted “Coming into today, I was concerned over the increasing near-term bubble like behavior in the which the SOXX was up a staggering 95% from the market closing lows on March 30th through yesterday June 3rd which drove a 19% rally in the S&P.” There were numerous signs of near-term froth and I believed they would need to be worked off.

However, coming into today, the morning of June 11th, the S&P is now down 4.5% from its recent closing high while the SOXX is down 12.3%. While the SpaceX IPO tomorrow in which a staggering ~$75B will be raised in the largest IPO in history may cause some of their large cap peers to be sold, I think that should be the final negative catalyst in the near-term.

I also wrote on June 4th, “I remain bullish over the long-term given 1) S&P earnings are expected to increase 25% this year driven by the advent of Agentic AI, 2) I believe oil prices will come down, and 3) new Fed Chairman Warsh is likely to push back against calls to raise rates.”

$ORCL results last night once again pointed out how the spending on AI continues driven by the token generation required by Agentic. Capex was guided to $90-95B including pre-payments for FY27 from $56B in FY26. While not good for Oracle cash flows or their hyperscale competitors which are locked in a capex war, it is great for the beneficiaries of that spend in semiconductors. I believe starting to add back positions in this sector once again makes sense and that the sell-off in the overall market is near an end.

I believe this is the pause that refreshes.

3

416

Jun 11

The stat that stopped me in my tracks 👇

The average S&P 500 stock is beating the average Magnificent 7 stock this year.

@philrosenn: equal-weight S&P is up ~8-9%. The Mag 7? Only up ~6.5-7%.

So much for "it's just 7 stocks holding up the market."

Where does market breadth go from here?

$RSP $MAGS

1

6

715

Jun 10

Everyone keeps telling me AI is a bubble. But @philrosenn brought receipts that say otherwise.

Tech stocks are actually cheaper than six months ago. Not because prices fell. Because earnings grew faster.

Nobody ever makes that comparison. Why not?

4

3

27

6,588

Jun 10

"If I don't use AI in five years, am I guilty of malpractice?"

That's what doctors are asking now.

Mayo Clinic ran the study: given the choice between an AI diagnosis and a doctor, 80% of patients chose AI.

I sat down with @_AiSquared CEO @TFurniss to talk about where this is all heading 👇

$AIAI

2

2

8

629