At MD Market Insights, our mission is to be the cornerstone for capital market professionals and institutions seeking to excel.

Joined October 2023

- Tweets 3,229

- Following 529

- Followers 113

- Likes 2,373

2,050 Photos and videos

NEW E2E NEWSLETTER DROP 🚀

The strongest Business Analysts don't just document requirements.

They:

⚙️ Think like Product Owners

📊 Analyze like Data Professionals

👥 Understand user behavior

📈 Drive business outcomes

🚀 Influence platform strategy

The future belongs to professionals who move beyond backlog management and start shaping platform evolution.

👉 The future BA does not only capture what the business asks for — they shape what the platform must become.

Read the full E2E Newsletter via MD Market Insights.

linkedin.com/pulse/capital-m…

#CapitalMarkets #BusinessAnalysis #ProductThinking #FinTech #Leadership

━━━━━━━━━━━━━━━━━━━━

1

3

1

Most candidates fail because they explain tasks.

Not systems.

👉 ebooks.mdmarketinsights.com/

#MDMarketInsights #CapitalMarkets #BusinessAnalysis #FrontOffice #TradingSystems #FinanceCareers #TradeLifecycle #RiskManagement #FinancialMarkets #FinTech #CareerGrowth #CareerTransition #ProfessionalDevelopment #BreakIntoFinance #CapitalMarketsTraining #FrontOfficeBA #TradingCareers #RiskAnalytics #FinancialEngineering #FinanceEducation

If you can explain:

• OMS

• EMS

• risk flow

You immediately sound different.

👉 ebooks.mdmarketinsights.com/

#MDMarketInsights #CapitalMarkets #BusinessAnalysis #FrontOffice #TradingSystems #FinanceCareers #TradeLifecycle #RiskManagement #FinancialMarkets #FinTech #CareerGrowth #CareerTransition #ProfessionalDevelopment #BreakIntoFinance #CapitalMarketsTraining #FrontOfficeBA #TradingCareers #RiskAnalytics #FinancialEngineering #FinanceEducation

1

Quantitative finance transforms uncertainty into measurable frameworks. #QuantFinance @IIBA @IIBAToronto @credly

#MDMarketInsights #BusinessAnalysis #CapitalMarkets #FinancialServices #TradeFloor #FinanceIndustry #InvestmentAnalysis #DataAnalytics #RiskManagement #TradingStrategies #MarketResearch #FinancialData #InvestmentManagement #AssetManagement #Fintech #RegulatoryCompliance #PortfolioManagement #Derivatives #MarketAnalysis #FinancialTechnology #TradingTools #QuantitativeAnalysis #InvestmentStrategy #BusinessIntelligence #FinancialInnovation #EconomicAnalysis #TradingSystems #DataScience #HedgeFunds #PrivateEquity #RiskAnalysis

2

Effective governance supports sustainable growth. #CapitalMarkets @IIBA @IIBAToronto @credly

#MDMarketInsights #BusinessAnalysis #CapitalMarkets #FinancialServices #TradeFloor #FinanceIndustry #InvestmentAnalysis #DataAnalytics #RiskManagement #TradingStrategies #MarketResearch #FinancialData #InvestmentManagement #AssetManagement #Fintech #RegulatoryCompliance #PortfolioManagement #Derivatives #MarketAnalysis #FinancialTechnology #TradingTools #QuantitativeAnalysis #InvestmentStrategy #BusinessIntelligence #FinancialInnovation #EconomicAnalysis #TradingSystems #DataScience #HedgeFunds #PrivateEquity #RiskAnalysis

2

How are GenAI compute demands, dynamic cloud spend, and Basel III/IV changing the front office? 🏦💻

Top capital markets firms are throwing out legacy cost allocation models. The old way of splitting IT costs by headcount or revenue is dead. 🪦

The new playbook? Consumption-based FinOps. 📊

By tracking metadata down to the exact API call, server runtime, and compliance volume, firms are unlocking true client profitability and optimizing capital efficiency like never before. 🎯⚡

Read our latest deep dive on why precision cost transparency is no longer an accounting preference—it's a competitive necessity for survival in a compressed-margin environment. 📉🔥

🧵 Read the breakdown & find industry frameworks here: [mdmarketinsights.com/insight…]

#CapitalMarkets #FinTech #FinOps #CostAllocation #InvestmentBanking #TradingSystems #CloudComputing #GenAI #AssetManagement #DataInfrastructure #BaselIII #FinancialOperations #FrontOffice #TradeLifecycle #BankingTech #FinancialAnalysts #DataAnalytics #CloudSprawl #OperatingModels #MarginOptimization #CorporateFinance #RiskManagement #QuantitativeTrading #AlgorithmicTrading #FinancialIntelligence #MarketInfrastructure #TechModernization #BusinessAnalysis #FinancialTechnology #FinanceTransformation #AlphaGeneration #ProductProfitability #ClientMargins #ResourceTracking #DigitalTransformation #BankingInnovation #RegulatoryCompliance #CostTransparency #DataSilos #OperationalEfficiency #PortfolioManagement #CapitalEfficiency #RiskWeightedAssets #Macroprudential #FinancialReporting #Accountability #TechBudgets #CloudOptimization #ModernFinance #MDMarketInsights

1

1

1

11

If you can explain:

• OMS

• EMS

• risk flow

You immediately sound different.

👉 ebooks.mdmarketinsights.com/

#MDMarketInsights #CapitalMarkets #BusinessAnalysis #FrontOffice #TradingSystems #FinanceCareers #TradeLifecycle #RiskManagement #FinancialMarkets #FinTech #CareerGrowth #CareerTransition #ProfessionalDevelopment #BreakIntoFinance #CapitalMarketsTraining #FrontOfficeBA #TradingCareers #RiskAnalytics #FinancialEngineering #FinanceEducation

Jun 13

What is an OMS?

Not just software.

It’s operational control.👉 ebooks.mdmarketinsights.com/

#MDMarketInsights #CapitalMarkets #BusinessAnalysis #FrontOffice #TradingSystems #FinanceCareers #TradeLifecycle #RiskManagement #FinancialMarkets #FinTech #CareerGrowth #CareerTransition #ProfessionalDevelopment #BreakIntoFinance #CapitalMarketsTraining #FrontOfficeBA #TradingCareers #RiskAnalytics #FinancialEngineering #FinanceEducation

1

1

6

Financial analytics supports strategic capital deployment. #CorporateStrategy @IIBA @IIBAToronto @credly

#MDMarketInsights #BusinessAnalysis #CapitalMarkets #FinancialServices #TradeFloor #FinanceIndustry #InvestmentAnalysis #DataAnalytics #RiskManagement #TradingStrategies #MarketResearch #FinancialData #InvestmentManagement #AssetManagement #Fintech #RegulatoryCompliance #PortfolioManagement #Derivatives #MarketAnalysis #FinancialTechnology #TradingTools #QuantitativeAnalysis #InvestmentStrategy #BusinessIntelligence #FinancialInnovation #EconomicAnalysis #TradingSystems #DataScience #HedgeFunds #PrivateEquity #RiskAnalysis

1

1

6

Market depth influences execution efficiency. #TradingSystems @IIBA @IIBAToronto @credly

#MDMarketInsights #BusinessAnalysis #CapitalMarkets #FinancialServices #TradeFloor #FinanceIndustry #InvestmentAnalysis #DataAnalytics #RiskManagement #TradingStrategies #MarketResearch #FinancialData #InvestmentManagement #AssetManagement #Fintech #RegulatoryCompliance #PortfolioManagement #Derivatives #MarketAnalysis #FinancialTechnology #TradingTools #QuantitativeAnalysis #InvestmentStrategy #BusinessIntelligence #FinancialInnovation #EconomicAnalysis #TradingSystems #DataScience #HedgeFunds #PrivateEquity #RiskAnalysis

1

1

5

MDMarketInsights retweeted

Rapid fire quant questions answered.

#quants #sellside #finance #math #statistics

youtube.com/shorts/1wgd2mBK8…

1

1

138

Jun 13

The biggest misconception in Capital Markets:

We think trades move through systems.

They don't.

Commitments do.

⚙️ OMS commits

⚡ EMS commits

📊 Risk commits

💰 Finance commits

🏦 Settlement commits

📋 Reporting commits

Every commitment creates dependency.

Every dependency creates risk.

New CNC Edition:

🟡 The Trade Lifecycle Is Not a Process — It Is a Chain of System Commitments

linkedin.com/pulse/trade-lif…

#CapitalMarkets #BusinessAnalysis #TradeLifecycle #TradingSystems

1

1

6

Jun 13

What is an OMS?

Not just software.

It’s operational control.👉 ebooks.mdmarketinsights.com/

#MDMarketInsights #CapitalMarkets #BusinessAnalysis #FrontOffice #TradingSystems #FinanceCareers #TradeLifecycle #RiskManagement #FinancialMarkets #FinTech #CareerGrowth #CareerTransition #ProfessionalDevelopment #BreakIntoFinance #CapitalMarketsTraining #FrontOfficeBA #TradingCareers #RiskAnalytics #FinancialEngineering #FinanceEducation

Jun 12

A strong candidate sounds:

• structured

• calm

• system-aware

👉 ebooks.mdmarketinsights.com/

#MDMarketInsights #CapitalMarkets #BusinessAnalysis #FrontOffice #TradingSystems #FinanceCareers #TradeLifecycle #RiskManagement #FinancialMarkets #FinTech #CareerGrowth #CareerTransition #ProfessionalDevelopment #BreakIntoFinance #CapitalMarketsTraining #FrontOfficeBA #TradingCareers #RiskAnalytics #FinancialEngineering #FinanceEducation

1

1

11

Jun 13

Statistical models should adapt to structural market changes. #QuantResearch @IIBA @IIBAToronto @credly

#MDMarketInsights #BusinessAnalysis #CapitalMarkets #FinancialServices #TradeFloor #FinanceIndustry #InvestmentAnalysis #DataAnalytics #RiskManagement #TradingStrategies #MarketResearch #FinancialData #InvestmentManagement #AssetManagement #Fintech #RegulatoryCompliance #PortfolioManagement #Derivatives #MarketAnalysis #FinancialTechnology #TradingTools #QuantitativeAnalysis #InvestmentStrategy #BusinessIntelligence #FinancialInnovation #EconomicAnalysis #TradingSystems #DataScience #HedgeFunds #PrivateEquity #RiskAnalysis

1

1

5

Jun 13

Statistical models should adapt to structural market changes. #QuantResearch @IIBA @IIBAToronto

#MDMarketInsights #BusinessAnalysis #CapitalMarkets #FinancialServices #TradeFloor #FinanceIndustry #InvestmentAnalysis #DataAnalytics #RiskManagement #TradingStrategies #MarketResearch #FinancialData #InvestmentManagement #AssetManagement #Fintech #RegulatoryCompliance #PortfolioManagement #Derivatives #MarketAnalysis #FinancialTechnology #TradingTools #QuantitativeAnalysis #InvestmentStrategy #BusinessIntelligence #FinancialInnovation #EconomicAnalysis #TradingSystems #DataScience #HedgeFunds #PrivateEquity #RiskAnalysis

1

1

6

MDMarketInsights retweeted

Jun 12

One agentic workflow now does 1,000 hours of hedge fund analyst work.

Aakarsh Ramchandi founded the data team @ Third Point, built screening engines @ FactSet, & now builds agentic research tools @ RavenPack.

"There's gonna be a full convergence of quant and qual. Most discretionary analysts I know are somewhere in their Claude journey — and the quants are going the other way around."

We cover:

- Year one at Third Point: onboarding 100 data sets with a team of 4 — & why they kept point-in-time copies of every vendor feed to catch panels that silently changed overnight

- The Dan Loeb pitch story — a 45-page deck, six weeks of work, he stops at page 26, asks one question, & the whole thesis breaks

- "Kind but not nice" — the zero-politics office where everyone gets corrected by elite people daily

- Why analysts don't want your forecast — they want facts in Excel, red-green-blue, formatted their way

- Hedging a concentrated activist book with alt-data short baskets built from a 400-500 factor model

- Why Nvidia broke the Barra model — & building custom semiconductor factors instead

- The agentic earnings preview: 8-9 step workflows, 35M tokens per run, ~1,000 hours of analyst work encoded

- Self-improving loops — agents reviewing their own last 10 traces & patching their mistakes

- The WorldQuant hackathon: 7,000 quants turning unstructured text into 35M unique time series

Highlights:

(00:00) Intro

(01:38) Founding Third Point's data team in 2017

(03:55) Six months building point-in-time data infrastructure

(06:20) How an event-driven fund actually uses alt data

(12:40) Team structure & the original forward deployed engineer

(17:10) Nobody wants your forecast — just give it to them in Excel

(19:35) Measuring signals: direction, point estimates & confidence intervals

(24:05) Working with Dan Loeb — the elite bullshit detector

(26:05) The page-26 "Why?" story

(28:55) 5AM Saturdays & discipline that compounds

(32:05) Kind but not nice: the zero-politics office

(33:55) How an activist creates alpha by re-running the business

(43:10) Hedging the book with alt-data short baskets

(50:40) Why Nvidia broke standard factor models

(56:25) From search to RAG to agents

(1:04:20) Opus 4.5 changes the game: 70% → 90% accuracy

(1:11:00) Anatomy of an agentic earnings preview — 35M tokens per run

(1:17:20) Ambient agents: the always-on Jarvis

(1:19:40) Self-improving loops & encoded judgment

(1:20:20) Finance in 10 years: the full convergence of quant & qual

2

25

202

101,746

🚀 🚀🚀🚀🚀🚀🚀🚀🚀🚀🚀🚀🚀

Jun 12

Today, @SpaceX (Nasdaq: SPCX) makes its public market debut with a $75Bn offering (pre-greenshoe) at $135 per share, marking the largest IPO in history.

Congratulations to the SpaceX team. We are honored to serve as joint lead bookrunner and sole stabilization agent.

8,613

16,797

136,347

13,517,604

MDMarketInsights retweeted

Jun 11

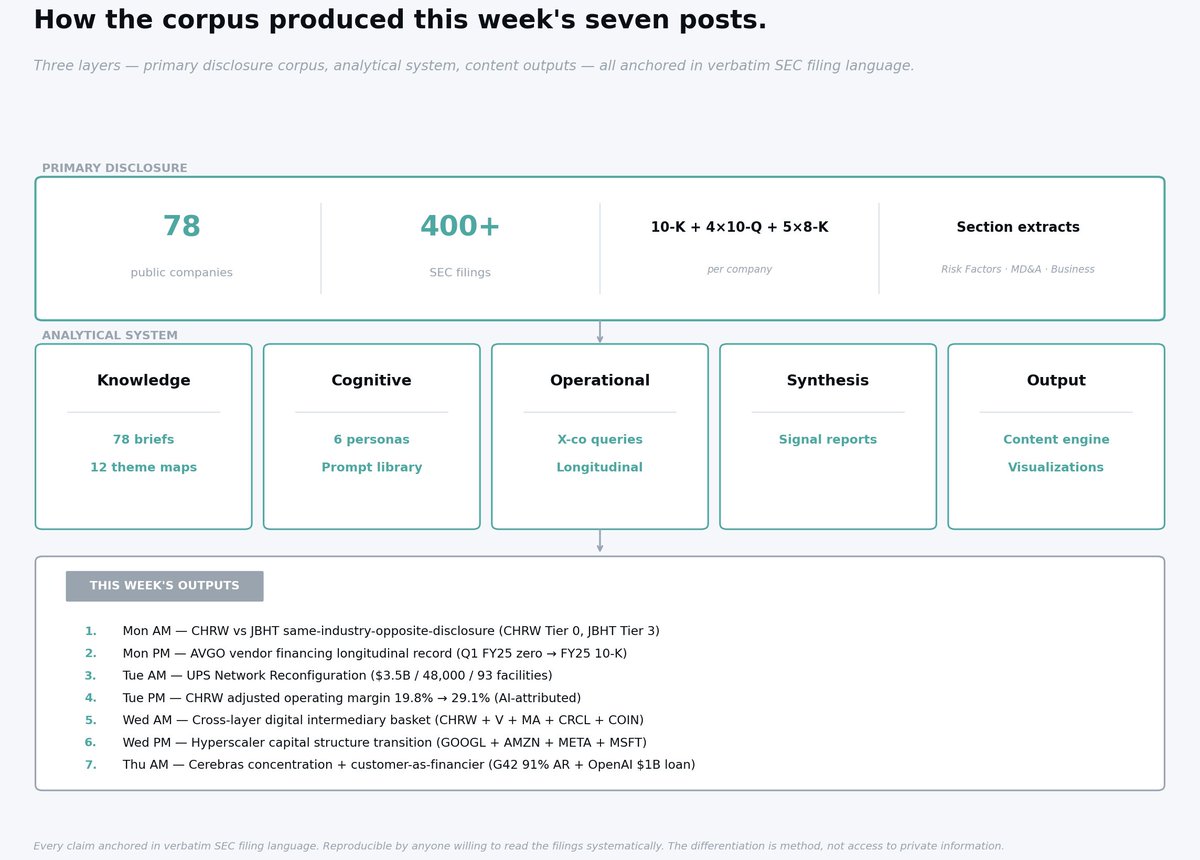

Seven posts this week. Each grounded in verbatim SEC filing language. Each surfaced by the same analytical system.

The engine behind them: 🧵

1

1

2

65