Former hedge fund manager; writes top 10 finance Substack netinterest.co/ and contributor to Bloomberg @opinion.

Joined September 2011

- Tweets 3,366

- Following 537

- Followers 26,317

- Likes 6,457

675 Photos and videos

Marc Rubinstein retweeted

Apr 30

May I gently suggest, @GreenJennyJones, without doubting your good intentions, that this sort of response is part of the problem.

If you meet a specific wrong with a general virtue, you have not answered the wrong; you have stepped around it.

Apr 30

I abhor cruelty and vindictiveness and hatred. Never mind who from, or who directed against.

4

50

464

25,204

Marc Rubinstein retweeted

Mar 30

Revolut’s pivot: Will going full bank kill its tech-level growth and valuation?

I read almost everything I can find about Revolut, but then I saw that Net Interest’s newsletter had dropped a new piece titled Revolut Unbound. I dropped my entire reading queue and started with it.

Net Interest is one of the top finance Substack newsletters, written by @MarcRuby, a former hedge fund manager, seasoned bank analyst, and Bloomberg Opinion contributor.

Marc and I have been following Revolut since almost the beginning, and we both have made small investments in the company. His Revolut Unbound piece is well written; it is best to read the whole thing yourself.

My top takes:

Marc suggests that low per-customer deposit amounts at Revolut could also be due to many customers joining rapidly and initially keeping low balances, which pulls down the overall average.

Another point Marc is making: can Revolut sustain its exceptional growth and high valuation as it fully transitions from a balance-sheet-light fintech company into a real, licensed global bank — or will the constraints of banking limit or alter its upside?

He writes: “One obstacle the group does face as it transitions more fully into a bank is capital. … One big difference though is valuation. … If Revolut can sustain both [rapid growth and 36% ROE], then Storonsky could be very rich.”

That is a great point. Initially, Revolut tried to be balance sheet-light, as I recall, CEO Nik Storonsky said in an interview that this way the company could grow faster and command a higher valuation as a tech company rather than as a bank.

Later, Nik admitted that avoiding heavier regulation was a mistake, and they are now embracing banking licences and biger balance sheets. One day, I will write my opinion piece on why I think it was a mistake.

The core idea of Marc piece: Revolut has come a long way from its early days of wanting to "replace banks" with a light, non-bank model — and securing full banking licences is a unlock that gives it new capabilities (deposits, higher net interest spreads, broader lending), but it also introduces real frictions and trade-offs that didn't exist in its more asset-light fintech phase.

Link to Net Interest newsletter: netinterest.co/?r=26ljc&utm_…

1

15

3,886

Mar 10

That’s four stock prices he’ll be managing. Almost as many as he has in the portfolio.

Mar 10

Today, Pershing Square Inc. (PSI), an alternative asset management company, filed to go public along with Pershing Square USA, Ltd. (PSUS) a new closed ended investment company managed by Pershing Square.

In the combined offering, investors in the IPO of PSUS will receive shares in PSI for no additional consideration. For example, if an investor buys 100 shares of PSUS in the IPO, they will receive 20 shares of PSI at no additional cost.

I explain the transaction in detail in a letter that can be found here:

sec.gov/Archives/edgar/data/… [sec.gov]

The prospectus for PSI can be found here:

sec.gov/Archives/edgar/data/… [sec.gov]

And the prospectus for PSUS can be found here:

sec.gov/Archives/edgar/data/… [sec.gov]

The PSI and PSUS Registration Statements have not yet become effective. The securities described therein may not be sold, nor may offers to buy be accepted, prior to the time the Registration Statements become effective. Before you invest in the combined offering, you should read the Registration Statements for more complete information about the PSI, PSUS, and the combined offering.

3

1

44

14,596

Marc Rubinstein retweeted

Feb 26

Here’s @marcruby’s debut Alphaville post, on the obvious arbitrage between disclosure-free “research” on social media and the massive burdens faced by traditional analysts. Hope it’s the first of many Rubyposts! ft.com/content/04b57c60-08b6…

6

27

5,041

Feb 23

The broker note moved markets. Now the Substack does.

Same impact, fewer regs.

30

7,704

Feb 19

As traders say: "The market is always right"

Feb 5

Kind of incredible. Reading through the Blue Owl earnings call, how different what they're saying is vs. how the market is behaving.

2

3

33

9,375

Marc Rubinstein retweeted

Feb 3

TOMORROW AT 11AM ET🚨🎙️

@MarcRuby and @michaelbatnick dig into the rapid rise of secondaries: why private assets are staying private for longer, how liquidity is being engineered rather than waited for, and what this shift means for valuations, incentives, and risk. They explore who wins, who loses, and whether secondaries are making private markets more efficient — or just more complex.👇🔥

Click me🎦youtube.com/live/N6P4tgIJhlo

3

16

35

18,378

17 Dec 2025

"Rubinstein is essential reading for finance geeks."

Nice profile on @iimag

institutionalinvestor.com/ar…

2

3

64

7,326

There’s a long way to go before wagers on events can rival markets that allocate capital, writes @MarcRuby (via @opinion) bloomberg.com/opinion/articl…

1

1

8

17,815

4 Dec 2025

👇

25 Nov 2025

Founder of alternative asset firm Blue Owl reckons fears of ruptures in private credit are "like the Mandela effect of finance... just common population collective misimpression of what's going on." To explore the issue further, I'm hosting a webinar with Sayonton Roy of Citigroup.

1

6

4,734

Marc Rubinstein retweeted

25 Nov 2025

Founder of alternative asset firm Blue Owl reckons fears of ruptures in private credit are "like the Mandela effect of finance... just common population collective misimpression of what's going on." To explore the issue further, I'm hosting a webinar with Sayonton Roy of Citigroup.

2

1

6

8,436

Almost five years after the GameStop frenzy, retail traders are making their presence felt more widely in US markets, writes @MarcRuby (via @opinion) bloomberg.com/opinion/articl…

12

4

15

15,422

25 Nov 2025

Founder of alternative asset firm Blue Owl reckons fears of ruptures in private credit are "like the Mandela effect of finance... just common population collective misimpression of what's going on." To explore the issue further, I'm hosting a webinar with Sayonton Roy of Citigroup.

2

1

6

8,436

25 Nov 2025

2

1,321

15 Nov 2025

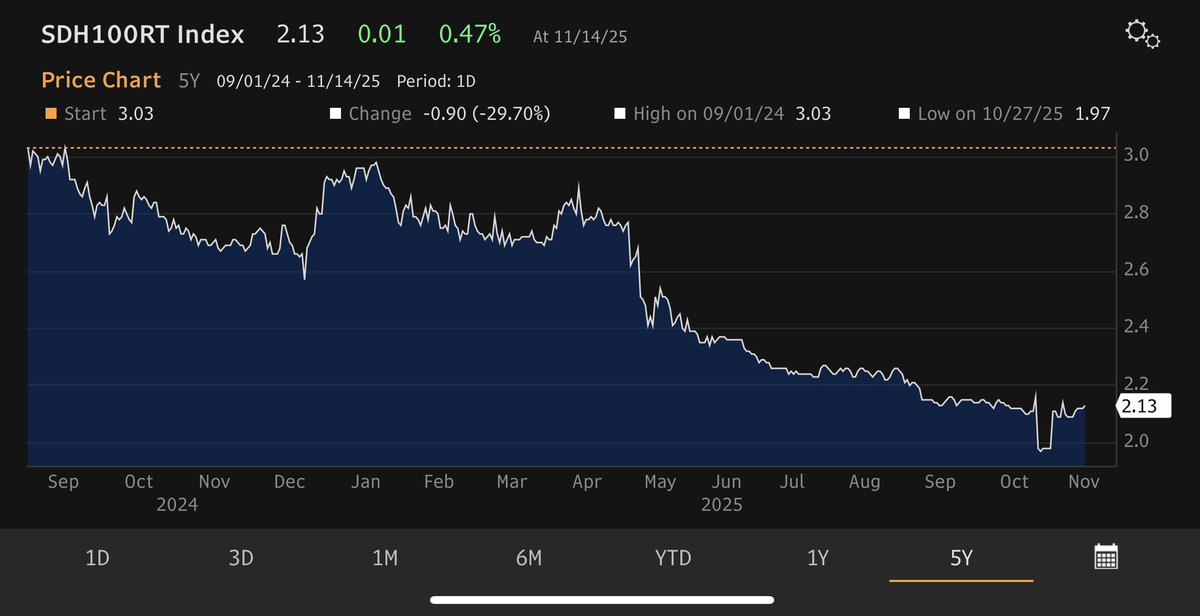

Launch of ABX index in Jan 06 created a coordination point for subprime unwind. Will H100 rental index (launched in May 2025) fulfil same role for compute?

“Goal is to turn GPUs into a benchmarked asset class that can be traded like any other financial instrument” says founder.

2

1

12

2,455

1 Nov 2025

As a bank CDS specialist I thought it was about time I learned about AI capex so that’s what this week’s Net Interest is about.

Remembering how in 2007-08 I worked with a tech analyst who would ask me about bank CDS spreads and how that was moving his stocks around so much (software or whatever), and have to think there are a lot of non-tech guys today frustrated by how much markets move on AI capex.

16

12,158

Marc Rubinstein retweeted

29 Oct 2025

US consumers have rarely been gloomier but lenders’ restraint on growth and risk are keeping losses at bay, writes @MarcRuby bloomberg.com/opinion/articl…

1

1

4

3,541