Shipping data, commodities, and trade flow analysis. We provide a data platform, private discord, and weekly report. Made by investors, for investors.

Joined February 2023

- Tweets 8,420

- Following 192

- Followers 26,341

- Likes 448

3,393 Photos and videos

Pinned Tweet

31 Dec 2025

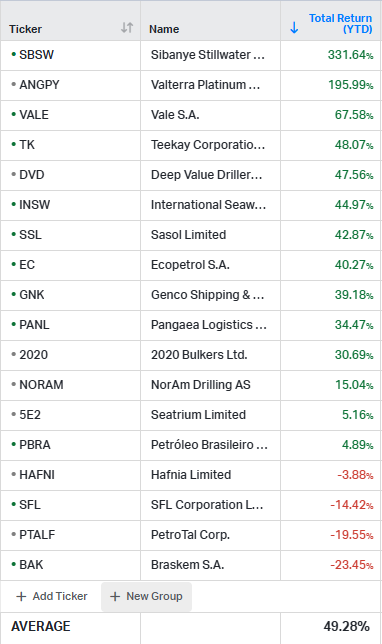

And 2025 is a wrap! Here were our 2025 picks

Not pictured is Seabird Exploration, which was acquired mid year up > 50% (good for 100% TWR)

Average pick returned ~50% for 2025, with 4/20 names providing a negative return

Best pick returned > 300%, worst pick returned -23%

5

5

180

84,194

Jun 12

While Capesize rates are falling daily, John Fredriksen is ordering ships. Another 4 Newcastlemaxes (211,000 dwt) for $300M. Smart money often buys tonnage when sentiment is weakest.

4

2

54

6,719

Jun 12

US refiners may take even more Venezuelan crude. Venezuela is currently sending ~600kbd (50% of its 1.2mbd exports) to the US, with volumes potentially rising in coming months.

2

23

3,107

Jun 12

OCP, the world's largest phosphate exporter, cut Q2 2026 production by 30% after sulphur replacement costs surged into the low-$700s/t CFR range.

A fertilizer crisis is quietly becoming a shipping story.

3

10

88

21,584

Jun 12

US LNG developers struggle to lock Europe deals. Talks are bringing interest but no long-term contracts, as Europe hesitates on deeper reliance on US supply, leaving next-gen LNG projects short of FID support.

Europe wants security… but not new dependence on US LNG.

5

3

38

3,786

Jun 12

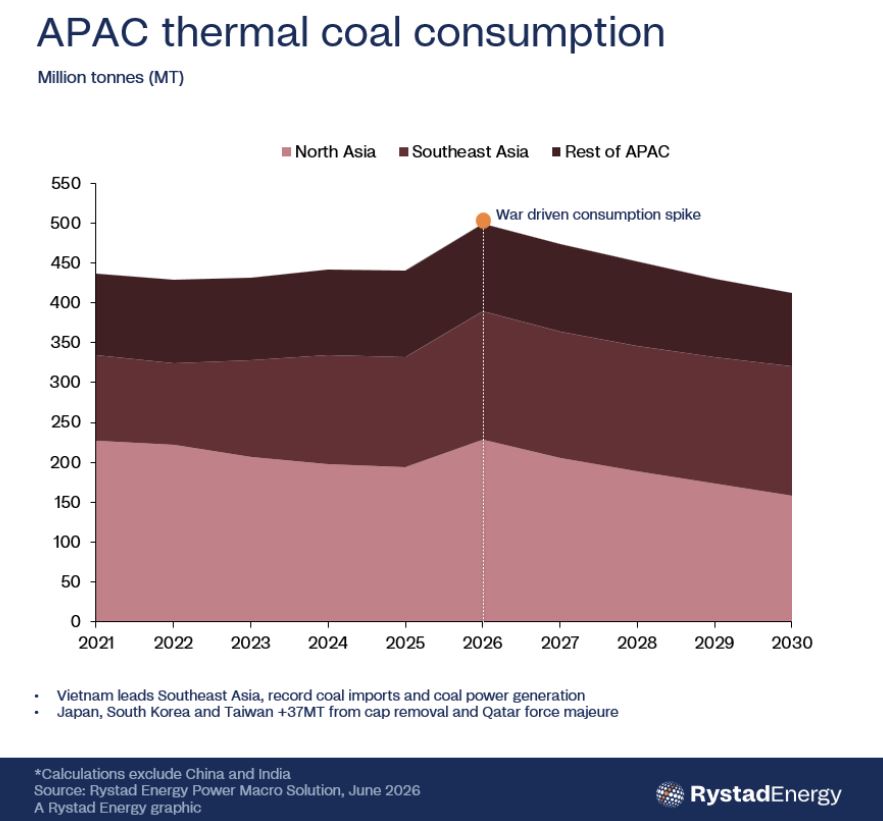

LNG shortages are doing what climate policy couldn't.

APAC thermal coal demand is projected to surge from ~440 Mt to ~500 Mt in 2026 ( 60 Mt).

Japan, South Korea and Taiwan alone add ~37 Mt.

When gas disappears, coal comes back.

3

12

67

5,037

Jun 11

Venezuelan crude is finding new homes in Asia. As Middle East supplies remain disrupted, Trafigura and Vitol are ramping up Venezuelan oil sales, with Merey 16 cargoes marketed to South Korea and deliveries already reaching Malaysia.

2

3

19

2,802

Jun 11

OPEC cuts its 2026 oil demand growth forecast again, now seeing demand rising by just 970,000 bpd. Meanwhile, OPEC output fell 190,000 bpd in May, led by Iran's decline, as the Hormuz crisis continues to squeeze supply. Bullish supply story, weaker demand story.

1

2

29

3,752

Jun 11

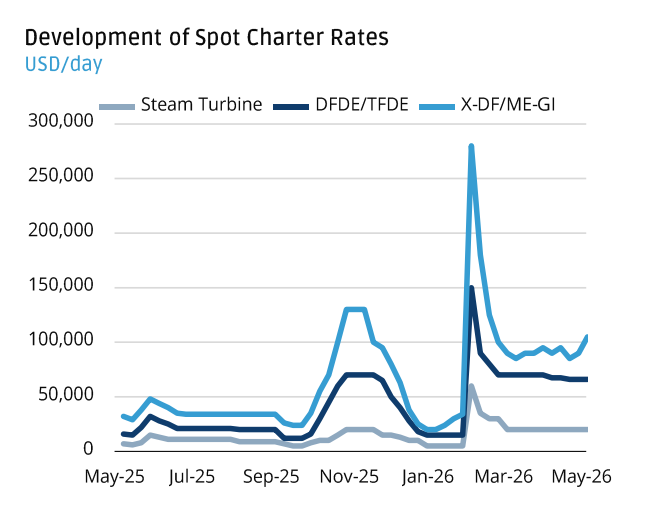

Modern X-DF/ME-GI LNG carriers are still earning around $105,000/day. That's nearly 5x the earnings of steam turbine tonnage at $20,000/day. Technology continues to separate winners from losers.

1

5

22

2,726

Jun 11

Japan goes full reroute mode: ~100% of July crude imports will avoid the Strait of Hormuz, with US supply set to jump 10x YoY as Tokyo scrambles alternative barrels from the Americas, Africa & Asia.

2

6

52

4,657

Jun 11

A telling signal from Greek LNG players: US suppliers are reportedly stepping back from 20-year LNG deals. With roughly 20% of global LNG supply disrupted, today's spot market may be too attractive to ignore.

2

8

53

4,779

Jun 11

China’s coal market is heating up fast. 5,500 kcal/kg coal surged to $127/ton CFR South China after mine disruptions and a heatwave boosted demand. Russian K-grade coking coal has climbed above $200/ton CFR.

2

6

72

9,449

Jun 11

China car exports explode: 809,000 cars in May ( 73% YoY), with EVs hitting 435,000 units (>50% share). RoRo market completely squeezed as spot rates hit $65,000/day, new fixtures up to $90,000/day, and China now dumping ~1m cars onto container ships due to lack of car carrier space.

1

4

35

3,246

Jun 11

Historic shift in global oil trade: The US has become the world’s largest oil exporter for a 3rd straight month, shipping 10.5m bpd in May vs 7.0m bpd from Russia and 5.9m bpd from Saudi Arabia. US crude & liquids output has surged to 22m bpd, reshaping global energy flows.

16

41

225

55,822

Jun 10

Everyone is watching Hormuz. Who is watching fleet availability?

Only 107 VLCCs are available in the MEG over the next 30 days while spot earnings remain at $112,500/day.

That's not a market with much spare capacity.

Ships aren't even positioned for a Hormuz reopening.

3

18

171

27,395

Jun 10

JP morgan report shows little gains for energy producers over the past 3 months. Australian and Asian Independents have actually lost value despite the energy shortage.

4

3

39

5,224

Jun 10

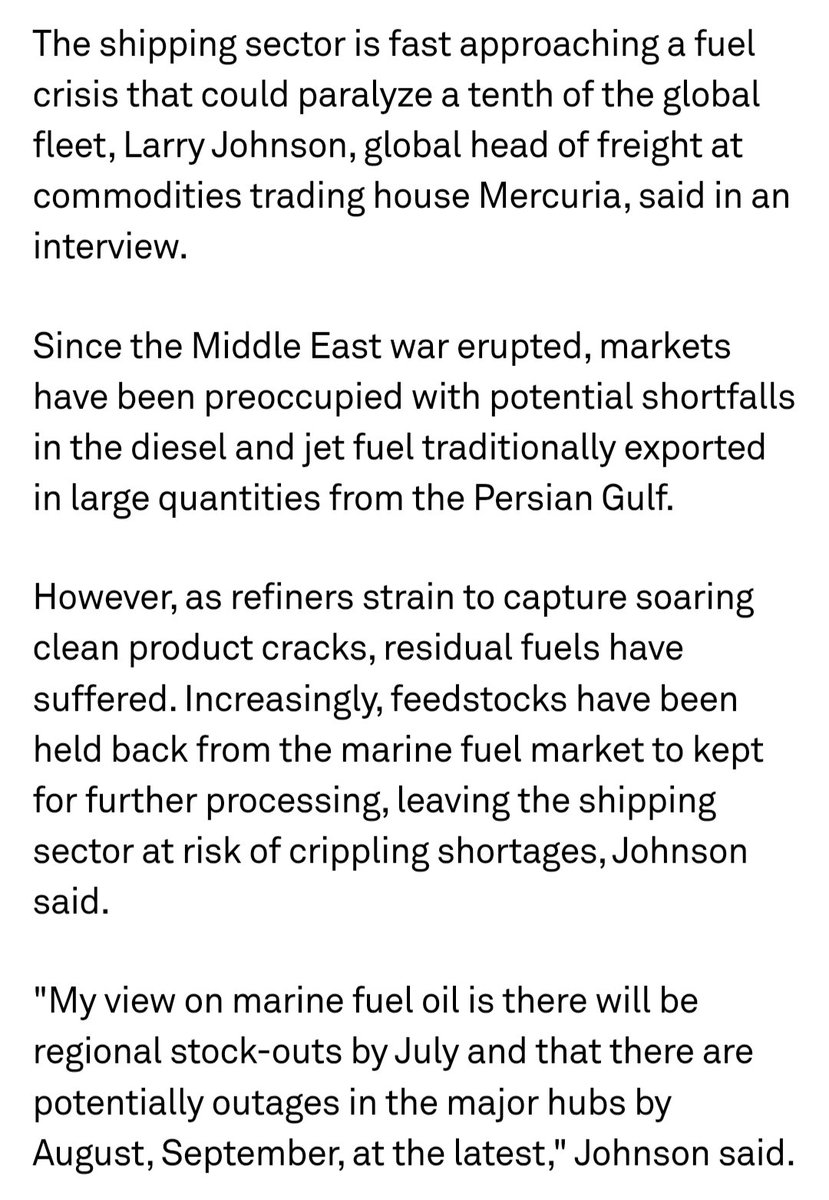

Reports of VLSFO shortages developing in east Asia with at least one state owned company advising earliest delivery July 1

Developing story

12

74

9,530

Jun 10

~20 laden dark tankers detected gathering off Iran’s main crude export terminal as ships switch off AIS amid US blockade constraints signaling intensified covert loading activity at Kharg Island.

1

6

26

4,583

Jun 10

Shell CEO says oil markets face a ~1.2 billion barrel supply gap tied to Strait of Hormuz disruptions.

2

69

4,713

Jun 10

Petronas and Japan’s JERA lock in up to ~2 million tonnes per annum of LNG for 20 years starting 2028, extending a supply partnership that began in 1983.

1

9

2,484

Jun 10

EIA sees Brent averaging ~$105/bbl in June–July and warns prices could stay in triple-digit territory through summer on supply shocks record-low OECD inventories.

7

49

4,693