I model professionally. HFT, MM, rust.

Joined January 2015

- Tweets 3,900

- Following 494

- Followers 3,508

- Likes 4,004

284 Photos and videos

Pinned Tweet

Feb 8

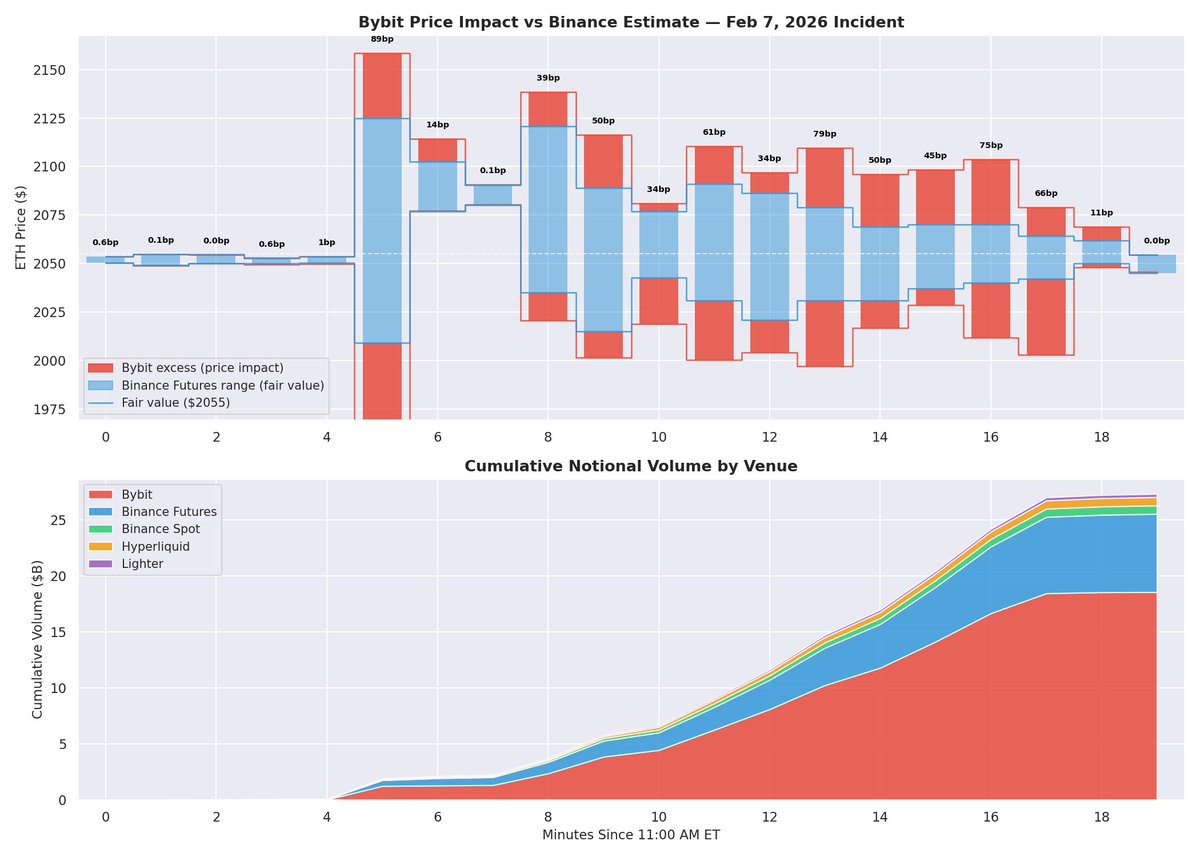

If anyone wants to read about one of the ways you can get flip flop bugs like this i wrote about it a few months ago. Its basically really easy to do and one of the fastest ways you can incinerate and account.

markrbest.github.io/position…

~100m gone in in 13 minutes

rough estimate assuming ~50-75 bps px impact times the 16b bybit volume

7

8

128

29,616

Mark Best retweeted

Jun 11

If wages had kept pace with the economy, the average worker would be on $150k .

Wages have fallen since the 1970s for 3 real reasons…

1. Technology has undermined the value of labour. Tech makes hard jobs easy. It outsources labour to cheaper countries. It completely replaces some jobs.

2. Governments print money and create cheap debt to stimulate the headline numbers of the economy. When they do it it’s an invisible tax on work and it inflates the value of anything that can be bought with debt (ie: houses but not wages).

3. We’ve massively increased the supply of labour. Both genders working full time doubled the supply of labour for many types of work. Then the ability to make work remote more than doubled it again. More supply equals lower prices.

Until we address the real reasons why the value of labour is so low we can’t solve the real problem. It might feel good to blame “billionaires” for everything but it’s a waste of time and energy if they’re not the real cause of the problem.

38

18

128

8,137

Mark Best retweeted

Jun 4

Two yachts have run aground at Ballina and Byron Bay recently and are both still stuck there, but last night Markus Pache 📷 took this shot of the one stuck at Flat Rock, East Ballina. Captures the dark emu at the perfect angle !

38

174

1,019

17,211

May 25

After getting a lot of unsolicited parenting advice I've come to the conclusion boomers are monsters.

1

5

462

Mark Best retweeted

May 1

When trying to fix negative markouts in your market making system, top of the list should be digging into fills that happened during inflight cancels.

These are trades your system knew were going to be toxic, but you got filled anyway.

This may happen because you're still too slow on the tails and quoting too tight for your latency, or it could be an inconsistency in your business logic.

Tracking these events involves accepting a small amount of overhead in the hot path but is generally worth it, especially in the testing phase with smaller amounts of capital.

When such events cross a certain threshold, I like to attach a cancel and fill context for detailed analysis of the system state before and after. This can include details about the BBO, alpha states, latency deltas, skew, etc.

Then, once such events have been reduced to an acceptable level, compile them out to shave the extra nanos off the hot path.

8

5

89

9,083

Apr 26

This plus they need to admit CPI is a lie

Apr 26

Ted Cruz: "We ought to index capital gains to inflation. We need to give a real impact to the economy that will impact affordability and do so before election day."

3

648

Mark Best retweeted

> meet guy who says he’s a quant

> ask him if he does linear regression or uses stochastic optimal control to model continuous-time limit order book dynamics

> he’s confused

> show chart explaining difference

> he says it’s a quant job

> check LinkedIn

> it’s linear regression

3

122

1,826

104,906

Apr 18

I urge you all to read when money dies. This is the same play book.

Apr 17

This week, Labour MPs voted to give ministers the power to decide how your pension savings are invested.

So ministers get pensions with guaranteed payouts, while they direct your savings towards their pet ideological causes, even if that means you lose money.

Disgraceful.

1

6

882

ive been slacking on my open source contributions for the past year or so, perhaps this will help me catch up: github.com/beatzxbt/stinkbid…

hope you find it useful!

1

10

120

7,736

Apr 3

RT @HFI_Research: One of the interesting dilemmas facing the oil market today is that even if the Strait of Hormuz opens fully tomorrow, th…

320

Mark Best retweeted

Apr 2

Watching the CI/CD pipeline run 1800 tests for a 1-line change that fixes a typo

125

766

11,790

603,618

Mark Best retweeted

Apr 2

Remember by longing Oil you're longing an asset that almost every country on Earth is incentivized to see trade lower

211

123

2,339

232,725

Mar 30

The fact they're having to say this tells you this is likely to get quiet bad

Mar 30

MIRAN: NO EVIDENCE OF INFLATION SHOCK FROM OIL

5

621