Crypto is my Hobby || 👈 Roger that

Joined July 2023

- Tweets 15,596

- Following 600

- Followers 547

- Likes 18,470

3,386 Photos and videos

Pinned Tweet

4 Feb 2025

INJ soon 🤝

4 Feb 2025

17

1

26

5,933

Marvel King retweeted

Step aside, 𝗶𝘁❜𝘀 𝗼𝘂𝗿 𝘁𝘂𝗿𝗻 𝘁𝗼𝗱𝗮𝘆 🇦🇷🏆

153

1,517

11,521

253,929

Marvel King retweeted

Jun 13

Two decades of Lionel Messi at the #FIFAWorldCup 🇦🇷💫

1,460

7,406

82,940

1,687,639

Marvel King retweeted

Jun 11

🚨Ripple Sponsors “TEAM CLARITY” Merchandise At Congressional Baseball Game

From courtroom fights…

to congressional merch.

Clarity changes everything.

15

16

20

373

Marvel King retweeted

The chart isn't the story.

The story is that people stayed long enough to see it.

Still here.

22

23

26

641

Marvel King retweeted

Morning; I've become convinced that founders make better capital decisions when they make them in the company of other founders.

The reasoning is straightforward. Capital structure is among the most consequential set of choices a founder makes, and also among the most isolating.

Decisions about ownership, dilution, instrument design, and liquidity carry forward for years and constrain options in ways that are difficult to reverse.

Bringing founders together directly addresses that gap. When founders at different stages discuss capital openly, several things become available that are otherwise hard to obtain.

91

8

117

6,794

Marvel King retweeted

May 27

Eid Mubarak from everyone at Chelsea Football Club. 💙🌙

651

6,329

36,009

472,366

Marvel King retweeted

May 23

I read this as: the real business isn't Hyperliquid the venue. It's all the infrastructure that makes a derivatives brokerage actually work.

Because when a user trades a perp through a wallet or app, someone has to:

→ match the order

→ source liquidity

→ custody collateral

→ handle settlement and risk

The branded frontend is the visible part, and IMO the bigger opportunity lies in controlling the rails, matching engine, liquidity, settlement, cross-margin risk.

Builder codes have already routed $237B to Hyperliquid and paid out $75M to the platforms running distribution. Phantom alone: $40B in volume, $20M in fees in under a year.

Whoever owns the rails owns where institutional perps flow next.

105

10

94

7,870

Marvel King retweeted

May 19

Built on @alphakek, our new Jjmoji meme arena is cumin sewn :3

9

9

35

2,733

Marvel King retweeted

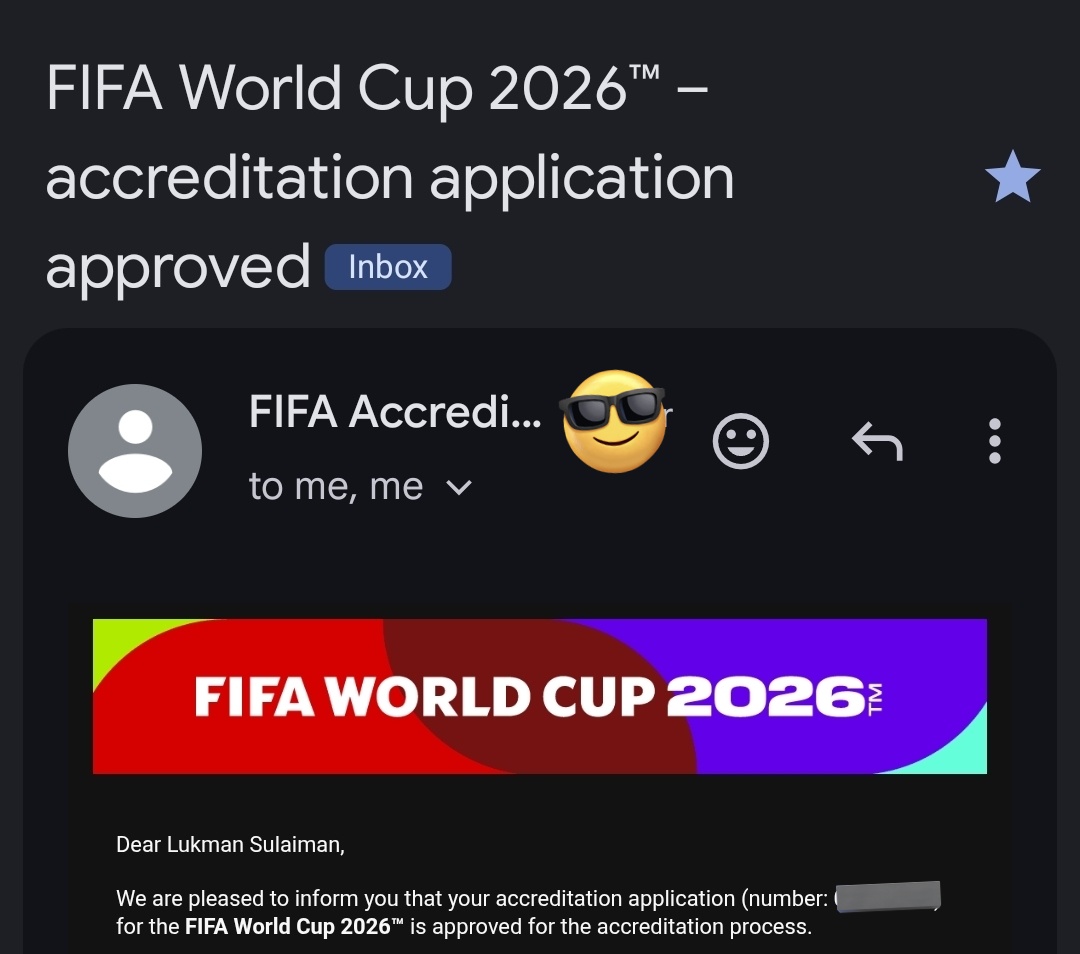

May 18

🚨 BREAKING!!!

POOJA IS GOING TO THE FIFA WORLD CUP 2026!!!

Accreditation Sorted ✅️

Visa Sorted ✅️

This will be my 2nd FIFA World Cup coverage. ✅️

For SPONSORSHIPS & DONATIONS, send a DM or email Poojamediacomms@gmail.com.

LET'S EXPOSE YOUR PRODUCTS & SERVICES.

3,225

3,469

23,455

1,938,478

May 18

1

29

Marvel King retweeted

May 17

$BABYASTEROID

Cute baby version of the viral Asteroid meme honoring Liv. Strong community on BSC, real donations, and meme power.

0xfecbda1b8dbd73c4eea7843c04db816107fa6666

x.com/BabyAsteroid_BB

11

10

20

870

Marvel King retweeted

May 14

be honest…

why does it suddenly feel like EVERYONE wants the CLARITY Act passed? 👀

banks nervous

institutions preparing

crypto finally entering the mainstream?

something big feels like it’s shifting ⏳

$CLARITY on XRP

15

18

26

854

Marvel King retweeted

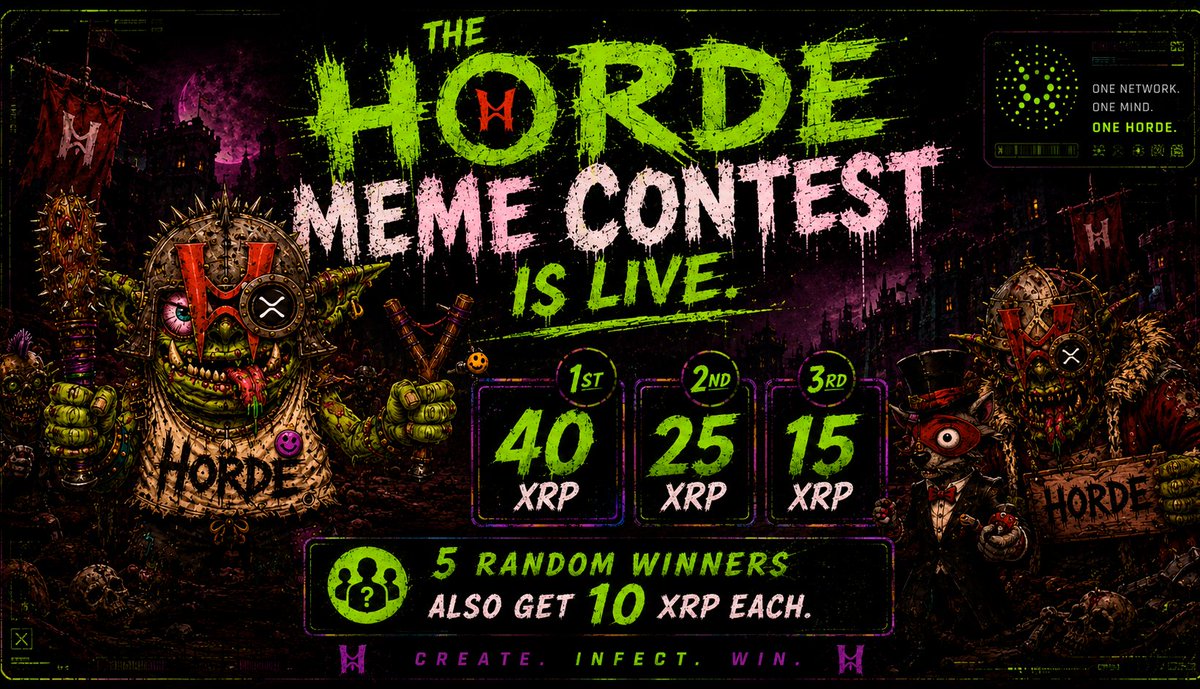

May 14

HORDE Meme Contest is LIVE.

Post a HORDE meme on X with #hordememecontest @HORDEonXRPL, then submit it at horde.pw/memecontest.

Vote if your XRPL wallet has 1 XRP in HORDE.

Prizes: 40 XRP / 25 XRP / 15 XRP

Bonus: like, repost tag 3 accounts for 5 random 10 XRP prizes.

84

112

171

7,532

Marvel King retweeted

May 13

May 13

13

12

32

810

Marvel King retweeted

May 12

It started with one.

SPY was never just watching.

The first one embraced the Horde.

And the Horde embraced him back.

This is how Infection begins.

Not with noise.

With recognition.

The spies found the Horde before the others. They became part of it.

@SpyDexNet is today’s top gainer on the infection index according to horde.pw/spread/

#HORDE #XRPL #SPY

18

20

28

785

Marvel King retweeted

May 12

I love building. For a long time, I built for myself - various bots and applications that helped me trade on the XRPL. Now I’ve found a community that infected me with its energy. It’s truly viral. I’m talking about HORDE. And I started building a website for this community. Today I made a page that shows the infection map of the XRPL by the HORDE virus.

horde.pw/spread/

We’re only at the beginning of the journey, but the outbreak is already spreading.

Embrace the Horde, and the Horde will embrace you!

@FUZZYPEPE_XRP @BreadXRP @DK64Trades @Waffl_XRP @XRPLWalrus @PHX_XRP @AmericanXRPcoin @CreatorXRPL @NorthXrpl

28

34

49

1,628

May 11

27