Joined August 2021

- Tweets 433

- Following 160

- Followers 56

- Likes 425

299 Photos and videos

Pinned Tweet

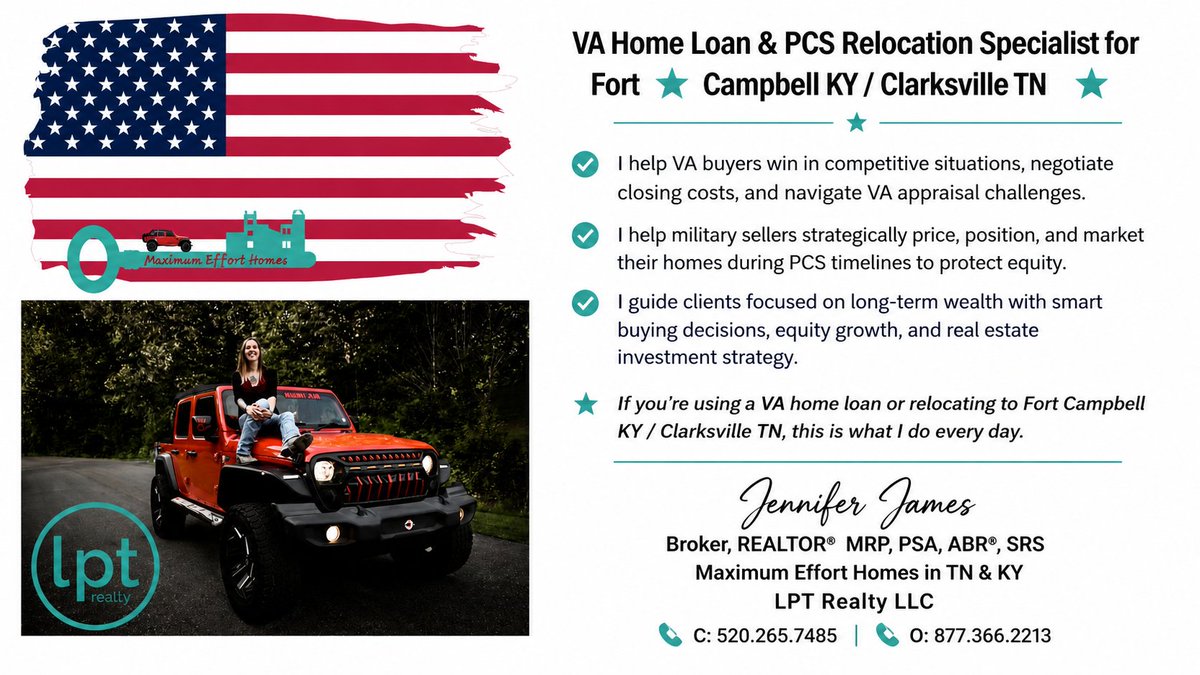

VA Home Loan & PCS Relocation Specialist for Fort Campbell KY / Clarksville TN. I specialize in working with active duty and veterans, helping VA buyers win in competitive situations, negotiate closing expenses, and navigate VA appraisal challenges.

I also help military sellers strategically price, position, and market their homes during PCS timelines to protect equity in a shifting market. For clients focused on long-term wealth, I provide guidance on smart buying decisions, equity growth, and real estate investment strategy.

If you’re using a VA home loan or relocating to Fort Campbell KY / Clarksville TN, this is what I do every day.

Jennifer James

TN Broker, KY REALTOR®,

MRP, PSA, ABR®, SRS

Maximum Effort Homes

Servicing Middle TN &

Southern / Western KY

📲 520-265-7485

📧 maximumefforthomes@gmail.com

🌎 maximumefforthomes.com

🌐 jenniferjames.lpt.com/

🏘 LPT Realty, LLC. TN Office

9041 Executive Park Dr. Ste 250

Knoxville, TN 37923

☎️ 877-366-2213

🏘 LPT Realty KY Office

424 Lewis Hargett Circle 2nd Floor

Lexington KY 40503

☎️ 877-366-2213

101

🇺🇸 Happy Flag Day! 🇺🇸

On June 14, 1777, our Founding Fathers adopted the Stars and Stripes as the official flag of the United States. Today, we honor that symbol of freedom, sacrifice, and the unbreakable spirit that defines our nation—especially here in Clarksville and near Fort Campbell.

To every active-duty service member, veteran, and military family who defends the red, white, and blue every single day: Thank you. Your service makes the American Dream possible, including the dream of homeownership.

At Maximum Effort Homes, we’re proud to help military families navigate VA loans, PCS moves, and finding the perfect home in the Clarksville / Adams / Oak Grove area. Whether you’re buying your first home with a VA loan, relocating to Fort Campbell, or investing in rental property—we’ve got your six.

Let’s keep flying the flag high!

What does the American flag mean to you and your family? Drop a comment below 👇

#FlagDay #IndependenceDayCountdown #FortCampbell #ClarksvilleTN #VASpecialist #MilitaryRelocation #MaximumEffortHomes #SupportOurTroops #AmericanFlag

34

📍 Fort Campbell Families: Know the OFF-LIMITS List!

Protect our service members with the official U.S. Army Garrison list of businesses/housing declared off-limits due to safety & risks. Updated periodically.

🔗 home.army.mil/campbell/off-l…

📞 Provost Marshal: 270-412-0176

Check BBB & local news too.

PCSing? VA loans or relocation help? DM me! 🇺🇸 🪖🫡🦅🏡🫶

#FortCampbell #ClarksvilleTN #MilitaryRelocation #VASpecialist #MaximumEffortHomes

6

Memorial Day is more than a long weekend, cookouts, or sales.

Today is for the men and women who never made it home.The ones who gave everything for people they would never even meet.

No matter your background, beliefs, or politics — freedom has always come at a cost carried by someone else’s family.

Take a moment today to remember them. Say their names. Fly the flag. Teach your kids why this day matters.

Forever grateful. 🇺🇸

12

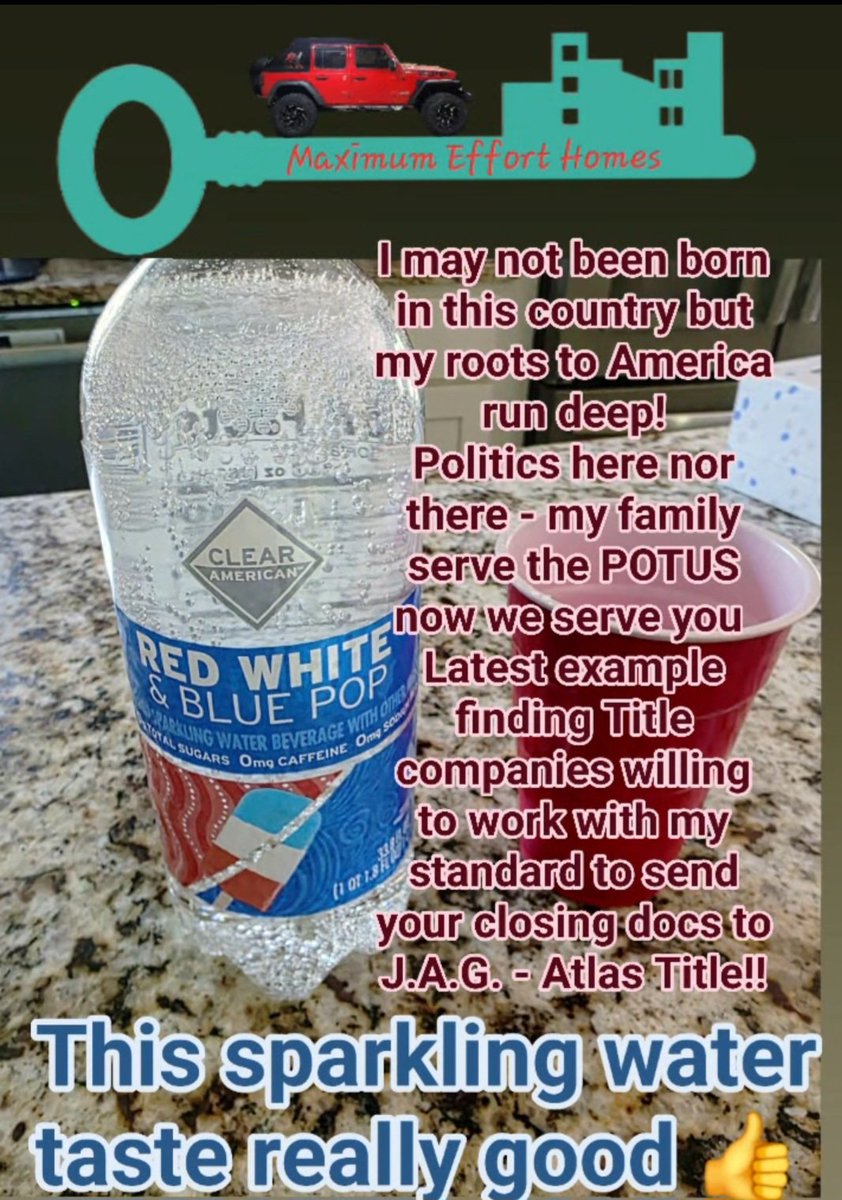

Hey there! Clarksville TN/ Fort Campbell KY

So besides this water taste like Freedom on a Sunday afternoon without the bad ingredients, like my services in real estate for veterans and active duty soldiers!

Here's a great example why to choose me as your VA Relocation Expert:

My clients that live out-of-state, and on post, that have a mailout closing. I asked a local title company here in Clarksville TN to send the documents package to my buyers home address on post. So my military clients can schedule a signing date and time take the package and go to J.A.G and have the office oversee the signing with a Paralegal or Attorney!! -> This does NOT change the closing company, they work for FREE for military personnel! It's no different than having a mobile closer!!

Any title company at the property's location could set this up very easily. I've done it myself in the past as well! Living on post in the boonies, or even OCONUS and avoiding the issue that the mobile closer may not have post access!! And the already stressed out Veteran family to drive to meet a closer somewhere for important documents to sign!!

IF the title company is truly about serving our military community here in Fort Campbell KY / Clarksville TN, they could have just set this up with Title Underwriting!! Yes there are new laws - but gues what J.A.G. isn't just anyone - they're ATTORNEYS

-> QUESTION = is the Title Company willing to make a simple phone call to save a Military Veteran Family $250-$500 -> NO, bc they could charge this amount to our home buying veterans!! And are out for profit rather than service!

-> YES, happy clients saved them $$ & you'll have clients for life!! The military community ALWAYS talks! They will soread the word if service was excellent or in the gutter!! =>Trust me this is my life since birth!!

-> On Friday I got connected with a cloud based title company licensed in 48 states and has their own Underwriting - They aren't even charging any side fees nor mailout closing fees for anyone - period!!

Thank you Angela D McCann - McCann Mortgages Services for getting me in contact with Will Gehl VP at Atlas Title will.gehl@atlastitleco.com

cell: (949) 514-0366

Atlas Title will beat anyone in Montgomery County in fees!!

Buyers & Seller Save $$ - agents check them out or you do a disadvantage to ypur clients!!

Folks remember NO one can tell you where to close!! IF an agent says you have to close at xyz Title / Attorney that's against the law!!

32

Repair amount: No strict VA cap, but many lenders limit renovation portion to $35k–$75k (varies; some higher).

Timeline: Usually completed within 120 days of closing (lender-specific).

Contractors: Must be licensed, bonded, insured per state/local rules (VA registration sometimes referenced but borrowers often choose qualified ones).

Appraisal: Based on "as-completed" value after repairs.

Contingency reserve: Up to 15% of repair costs for surprises.

Tip: Not all lenders offer VA Renovation Loans—shop around. Always verify latest details with a VA-approved lender and the official VA Lender’s Handbook.

DM me "VA RENO" if you want help checking eligibility or finding a lender! 💪🇺🇸 🫡🪖

#VALoans #VARenovationLoan

29

📢 FOLLOW-UP 🚨

⚠️ Veterans: Shop your VA loan. Don’t assume a company with “Veterans” in the name automatically has your best interest.

A newly filed federal class action lawsuit against Veterans United Home Loans alleges:

🚩 misleading advertising implying VA affiliation

🚩 steering buyers to preferred agents - illegal kickbacks!!

🚩 higher fees & interest rates

🚩 agents paying ~35% referral commissions

🚩 veterans being discouraged from shopping lenders

The lawsuit claims many borrowers believed the company was actually connected to the VA because of its branding and marketing.

Bottom line: Your VA loan benefit belongs to YOU — not a marketing company!! That charges local agents a 45% referral commission fee and VU is NOT crediting this back to the veteran client!! 😲 Paying Millions $$$ into advertising!!

Always compare:

✅ Interest rates

✅ Lender fees

✅ Closing Expenses

✅ Lender credits

✅ Loan Origination Fees

✅ Underwriting Fees

✅ Local Lenders vs National Lenders

Veterans, YOU fought too hard for YOUR benefits to get overcharged on the biggest purchase of YOUR life. 🇺🇸

#VALoan #Veterans #MilitaryHomebuyers #FortCampbell #ClarksvilleTN #PCS #VAHomeLoan #RealEstateTruth

28

✅ VA Home Loan Tip for Veterans in ClarksvilleTN / FortCampbell KY!

Veterans: You don’t have to pay the VA appraisal fee out of pocket!

The buyer is technically responsible, but this is a fully negotiable closing cost. You can have the seller cover it through concessions or credits — and it doesn’t count against the 4% seller concession limit. Many sellers happily agree to this in negotiations.

Current VA Appraisal Fees

(as of May 1st 2026):

Kentucky: $650

Tennessee: $750

These are the standard allowable fees for single-family homes. Always confirm your exact county with your lender, as minor variations can apply.

Pro tip: Mention this early with your real estate agent and VA-approved lender. Build it into your offer and save that cash for moving or upgrades!

Tag a Veteran looking to purchase 💝🇺🇸🫶🏡

#militaryrelocationexpert

#VALoans #VeteransHousing #HomeBuyingTips #KYRealEstate #TNRealEstate #VABenefits

19

Just got a VA Tidewater call, so that’s what I’m digging into today. Let me explain here:

We’re definitely seeing more low appraisals lately as the market starts balancing back out. That doesn’t mean the market is falling apart — or even crashing — it just means some prices are getting ahead of what the comps can actually support.

Yes, inflation has driven up the cost of everything — labor, materials, insurance, repairs, even gas. Us Jeepers definitely feel that one. But appraisers still have to justify value based on real market data and comparable sales. - Inflation vs actual costs!

This is why having a LOCAL VA expert matters. Interview an agent that actually lives and breathes this area — not some Nashville guy that doesn’t even know what a Fobbit is. My job is to protect YOU guys here in Fort Campbell KY / Clarksville TN from overpaying while also doing everything possible to keep the deal together based on my buyers’ goals and wishes.

VA Tidewater was put in place in 2003 to help protect Veterans’ interests for a reason!!

Jennifer James

TN Broker, KY REALTOR®,

MRP, PSA, ABR®, SRS

Maximum Effort Homes

Servicing Clarksville TN / Ft. Campbell KY

📲 520-265-7485

📧 maximumefforthomes@gmail.com

🌎 maximumefforthomes.com

🌐 jenniferjames.lpt.com/

🏘 LPT Realty, LLC. TN Office

9041 Executive Park Dr. Ste 250

Knoxville, TN 37923

☎️ 877-366-2213

🏘 LPT Realty KY Office

424 Lewis Hargett Circle 2nd Floor

Lexington KY 40503

☎️ 877-366-2213

#movingthemilitary

#MaximumEffortHomes #realtorinajeep #thecoolagent #realtor #PCS

#VAHomeExpert #veterans

#middletennessee #southernky #ftcampbell #military #militaryfamilies #101stairborne #militarylife #financialplanning #militaryrealestate #beamilitarymillionaire #buildingwealth

26

SELLER OPEN HOUSE & MARKETING YOUR HOME INFO!!

You will see many brokerages won't allow other agents outside their brokerages to do an open house or even run an advertisement on your property if you would have hired them!!

This means less exposure, less people and agents seeing your home!! Less buyers!! -> This is VERY crucial in a military community where tight timelines are all that matter with PCS-ing season!!

LPT Realty LLC won't hinder agents to do any style marketing as along as it is within State and National laws!!

YOUR HOME 🏡 exposure and marketing before the agent's personal gain and advertising!!

Ask about our Listing Power Tools!!

Jennifer James

TN Broker, KY REALTOR®,

MRP, PSA, ABR®, SRS

Maximum Effort Homes

Servicing Clarksville TN / Ft. Campbell KY

📲 520-265-7485

📧 maximumefforthomes@gmail.com

🌎 maximumefforthomes.com

🌐 jenniferjames.lpt.com/

🏘 LPT Realty, LLC. TN Office

9041 Executive Park Dr. Ste 250

Knoxville, TN 37923

☎️ 877-366-2213

🏘 LPT Realty KY Office

424 Lewis Hargett Circle 2nd Floor

Lexington KY 40503

☎️ 877-366-2213

#MaximumEffortHomes #realtorinajeep #thecoolagent #realtor #PCS

#VAHomeExpert #veterans

#middletennessee #southernky #ftcampbell #military #militaryfamilies #101stairborne #militarylife #financialplanning #militaryrealestate #beamilitarymillionaire #buildingwealth

21

If you're using a VA loan or getting ready for a PCS move to Fort Campbell / Clarksville, this matters.

Most buyers are set up wrong before they ever step into a home—and that’s what costs them deals, money, and time.

I help VA buyers:

✔ Win in competitive situations

✔ Navigate appraisal challenges

✔ Negotiate closing costs the right way

I also help military sellers price, position, and protect their equity during tight timelines.

This isn’t theory—this is what I do every day.

📩 If you have questions or want to get ahead of the process, messa

37

Real estate isn’t just transactions—it’s timing, strategy, and protecting what you’ve worked for.

Maximum Effort Homes was built on one thing:

👉 doing right by people, every single time.

I work with military families, first responders, and local buyers/sellers who want straight answers, strong strategy, and someone who actually shows up for them.

Whether you're buying, selling, or relocating, my goal is simple:

✔ Protect your equity

✔ Reduce stress

✔ Make your next move your best move

If you’re planning a move in TN or KY, I’ve got you.

14

Behind every transaction is a real life move—and that’s something I take seriously.

I come from a military family, I’m married to a veteran, and I’ve personally experienced the stress, timelines, and unknowns that come with relocating.

That’s why I don’t just “sell homes.”

I help people:

✔ Make confident decisions

✔ Avoid costly mistakes

✔ Navigate the process without feeling overwhelmed

I treat my clients like family and I show up like it matters—because it does.

If you’re thinking about buying or selling, let’s talk.

14

A VA Renovation Loan

(also called a VA Rehab, Reno, or Alteration and Repair Loan) is a VA-guaranteed mortgage that lets eligible Veterans, service members, and qualifying surviving spouses finance both the purchase (or refinance) of a home and the cost of repairs/renovations in a single loan.

It functions similarly to the FHA 203(k) loan but with VA's signature benefits: typically no down payment, no private mortgage insurance (PMI), competitive interest rates, and limited closing costs. The VA guarantees a portion of the loan, which allows private lenders to offer favorable terms.

How It Works

* The loan rolls the home's purchase price (or refinance amount) estimated repair costs certain fees into one mortgage.

* Funds for repairs are held in an escrow/draw account and disbursed in stages (draws) as work progresses, with lender oversight and approvals.

* A VA appraiser determines the "as-completed" value (projected value after repairs). For purchases, the loan amount is generally the lesser of the total acquisition cost or this as-completed value. For refinances, the as-completed value can often be used more flexibly (up to 100% LTV in some cases).

* Work must typically be completed within a set timeframe (often 120 days, though lender-specific).

* Contractors/builders must be licensed, bonded, and insured (per state/local rules); some lenders or older guidelines reference VA registration, but borrowers generally choose qualified ones.

* A contingency reserve (up to 15% of repair costs) may be included for unexpected issues; unused funds are usually applied to the loan balance (or returned in refinances).

Eligible Uses

* Purchase a fixer-upper that doesn't initially meet VA Minimum Property Requirements (MPRs) and roll in repairs.

* Cash-out refinance on a home you already own and occupy to fund repairs.

Repairs/improvements must enhance livability, safety, functionality, or value and be typical for similar homes in the area.

Examples include:

* Roofing, siding, windows, doors, gutters.

* HVAC, plumbing, electrical systems.

* Flooring, insulation, energy efficiency upgrades.

* Mold/lead remediation, accessibility modifications (e.g., for disabilities).

* Kitchen/bath updates (non-luxury).

Not allowed: Major structural additions (e.g., new rooms/floors), cosmetic-only work (purely aesthetic), pools, landscaping, detached garages, or items needing structural engineering reports. You generally cannot do the work yourself.

Key Requirements and Limits

Eligibility: Standard VA loan eligibility (Certificate of Eligibility/COE required), plus lender overlays (e.g., credit score often 620 , stable income, acceptable DTI ratio). The home must be your primary residence.

Repair Amounts: No strict VA-wide cap, but many lenders limit renovation portions to around $35,000–$50,000 (some higher, lender-dependent). Total loan follows VA/conforming limits based on the as-completed value.

Appraisal and Inspections: VA appraisal considers post-repair value; final inspection confirms completion and MPR compliance.

Timeline and Process: Tighter than standard VA loans due to draws, contractor coordination, and inspections. Not all lenders offer it—availability is more limited.

Pros and Cons

Pros:

- No down payment one monthly payment.

- Finance repairs without separate high-interest loans.

- Increases home value and helps buy properties in competitive markets or those needing work.

Cons:

- Fewer lenders participate (shop around).

- Strict rules on eligible work and timelines.

- Requires coordination with contractors and potential multiple inspections.

- Sellers may prefer cash buyers for fixer-uppers.

Other VA Home Improvement Options

VA Energy Efficient Mortgage (EEM) — For specific green/energy upgrades.

Cash-out refinance — Tap equity for repairs (no specific renovation structure).

Specially Adapted Housing (SAH) grants — For disabled Veterans' accessibility needs.

Check VA Guide & consult with a VA Lender

25

🚨 VA BUYERS & SELLERS — BIG CHANGE (and it’s about time)

Today is the day! In the past few weeks I had posted about each item change!

Starting May 1, 2026… VA appraisals just got a LOT less deal-killing.

Let me translate what this actually means in the real world 👇

💥 Detached structures?Sheds. Barns. Workshops.👉 VA is DONE nitpicking them.

No more:• “This shed needs scraped & painted”• “That barn has to meet VA standards”• Deals falling apart over a storage building 🙄

💥 Radon requirements?👉 Gone.

💥 Ventless gas heater certifications?👉 Gone.

💥 Overly picky repair lists?👉 Dialed WAY back.

—

🏡 What STILL matters (don’t get it twisted):VA is still protecting buyers.

✔ Safe✔ Livable✔ Structurally sound

If it’s dangerous or broken—it still has to be fixed.

—

🔥 What this means for YOU:

BUYERS:👉 More homes qualify👉 Fewer repairs killing your deal👉 Stronger offers in competitive markets

SELLERS:👉 VA buyers just became WAY less risky👉 Fewer hoops👉 Faster closings

—

💬 Real talk:A LOT of homes in Clarksville, Oak Grove, and surrounding areas used to get flagged over dumb stuff…

That’s changing.

And VA buyers?👉 You just got a serious edge.

—

If you’ve been told “VA loans are hard” or “VA won’t pass on this house”…

That conversation just changed.

Message me—I’ll walk you through what this means for YOUR situation.

Jennifer James

TN Broker, KY REALTOR®,

MRP, PSA, ABR®, SRS

Maximum Effort Homes

Servicing Clarksville TN / Ft. Campbell KY

📲 520-265-7485

📧 maximumefforthomes@gmail.com

🌎 maximumefforthomes.com

🌐 jenniferjames.lpt.com/

🏘 LPT Realty, LLC. TN Office

9041 Executive Park Dr. Ste 250

Knoxville, TN 37923

☎️ 877-366-2213

🏘 LPT Realty KY Office

424 Lewis Hargett Circle 2nd Floor

Lexington KY 40503

☎️ 877-366-2213

#movingthemilitary

#MaximumEffortHomes #realtorinajeep #thecoolagent #realtor #PCS

#VAHomeExpert #veterans

#middletennessee #southernky #ftcampbell #military #militaryfamilies #101stairborne #militarylife #financialplanning #militaryrealestate #beamilitarymillionaire #buildingwealth

1

37

🚨 Hey TN folks, watch out on the roads after this long drought! 🌧️

When that first real rain finally hits, things get tricky out there. All the oil, dust, and tire gunk that built up on the dry pavement mixes with the water and turns the roads super slippery — especially those first 30-60 minutes. Braking and turning feel off, and accidents jump up.

Plus, you might notice dirty blotches on your car from all that western dust blowing in.

And longer term? Our clay soil shrinks up in the drought, roads crack, then rain seeps in and sets up more potholes down the line. Heavy stuff can bring flash flooding or mudslides too, especially in East TN.

Just take it easy — slow down, leave extra space, and watch for puddles. TDOT’s gonna have their hands full with repairs soon.

Stay safe out there, y’all! Drive careful ❤️

#TNRoads #DriveSafe #TNWeather

23

🚨 Real Talk for Homebuyers (Especially VA Buyers around Fort Campbell / Clarksville / Oak Grove) 🚨

Had another situation today that proves this point again…

👉 Not all “pre-approvals” are created equal.

If your lender is using estimated income — especially without a verified income letter from Defense Finance and Accounting Service (DFAS) for military buyers — you are NOT actually pre-approved.

You’re pre-qualified… and that’s a very different thing.

---

⚠️ Why this matters

When the numbers aren’t fully verified upfront, here’s what happens:

You go tour homes

You fall in love with one

You get under contract

You spend money on:

Home inspections

Specialty inspections

Appraisal fees

Possible re-inspections

💥 Then 3–7 days before closing…

The loan falls apart.

No house.

Money spent.

Time wasted.

Emotional rollercoaster for no reason.

---

💡 Do it the RIGHT way upfront

A true pre-approval means your lender has verified your file, not guessed at it.

Focus on this before you shop:

✔ Debt-to-Income (DTI)

VA loans can technically go high (yes, even up to ~80% in some cases)

But most lenders are more comfortable around ~37–50%

👉 Lower DTI = stronger approval better rates

✔ Income Documentation

LES / DFAS verified for military

Official employer letters

Bank statements (real ones — not screenshots)

✔ Credit Score

VA doesn’t set a minimum, but lenders DO

👉 Higher score = better rate lower monthly payment

---

🔑 Bottom Line

Quality over quantity.

A solid pre-approval on the front end saves you:

Thousands of dollars

Weeks of stress

Deals that fall apart at the finish line

---

If you’re buying around Fort Campbell, Clarksville, or Oak Grove and want to make sure you’re actually ready before you start shopping — ask questions early.

It makes all the difference.

Jennifer James

TN Broker, KY REALTOR®,

MRP, PSA, ABR®, SRS

Maximum Effort Homes

Servicing Clarksville TN / Ft. Campbell KY

📲 520-265-7485

📧 maximumefforthomes@gmail.com

🌎 maximumefforthomes.com

🌐 jenniferjames.lpt.com/

🏘 LPT Realty, LLC. TN Office

9041 Executive Park Dr. Ste 250

Knoxville, TN 37923

☎️ 877-366-2213

🏘 LPT Realty KY Office

424 Lewis Hargett Circle 2nd Floor

Lexington KY 40503

☎️ 877-366-2213

#movingthemilitary

#MaximumEffortHomes #realtorinajeep #thecoolagent #realtor #PCS

#VAHomeExpert #veterans

#middletennessee #southernky #ftcampbell #military #militaryfamilies #101stairborne #militarylife #financialplanning #militaryrealestate #beamilitarymillionaire #buildingwealth

18

TN & KY REAL TALK!!

Home Appraisal came back tide water (VA loan term when the value of the subject home appraised lower than contractual purchase prise!!)

LA (listing agent) admitting he rarely does business in the 37040 & 37042 Zip

🚩 Folks PLEASE hire people that are living in the area or at least doing constant business in the area and not people from a total different board!

We have:

🏢 CAR Clarksville Association of REALTOR®s (includes Montgomery & Stewart Country as well as Christian County in cooperation for the dual licensed folks with Blue Grass Association on the KY side)

🏢 RCAR Robertson County Association (the ne says it all!

🏢 GNAR Greater Nashville REALTORS® (formalty know of Nashville Association) (Davidson, Cheatham, Dickson, Hickman, Houston, and Humphreys)

You may ask can we as Brokers and Agents do business everywhere⁉️

✅️ Absolutely, YES - the entire state until you run out of gas money!!

✨️ BUT the NAR (National Association of REALTOR®S) says provide skill and care in your scope!! IF you do 1 or 2 closings a year in Clarksville and admit they don't know the customs and area at all - They should have referred the client to a local agent! They're not servicing their clients properly!! UNLESS they had this discussion and it is in writing!!

🕵♀️INTERVIEW the people you want to hire!!

💝 Till then auf Wiedersehen 😘🍻

Call me 🤳

Jennifer James

TN Broker, KY REALTOR®,

MRP, PSA, ABR®, SRS

Maximum Effort Homes

Servicing Clarksville TN / Ft. Campbell KY

📲 520-265-7485

📧 maximumefforthomes@gmail.com

🌎 maximumefforthomes.com

🌐 jenniferjames.lpt.com/

🏘 LPT Realty, LLC. TN Office

9041 Executive Park Dr. Ste 250

Knoxville, TN 37923

☎️ 877-366-2213

🏘 LPT Realty KY Office

424 Lewis Hargett Circle 2nd Floor

Lexington KY 40503

☎️ 877-366-2213

40