22 Photos and videos

$OCUL piper doesn’t cover $EYPT . But they have made a decent killing being book runners for $OCUL . Piper pads their pockets on book runner money that fuels dilution while giving rosey targets for naive investors played by the doughs of the world .

Jun 15

$EYPT most likely down today on piper remarks on regulatory comments at CTS further clarify views on sham mask and rescue injections

1

1,218

Mike retweeted

President Trump better not show up to Madison Square Garden tonight and cause any distractions

President Trump:

199

798

8,037

272,475

In early December $EYPT was at 40% of $OCUL . Now it’s 59% . Cream will rise to the top once markets digest Duravyu is the cleaner TKI with better commercial viability . Future SOC is multiple-MOA of cheap biosimiliar ( $HROW) premium TKI insert for long-lasting durability.

Mar 16

Guggenheim reiterated Top Pick $EYPT Buy; $68

$OCUL REGN RHHBY SRZN KOD $FDMT

Guggenheim said—Based our recent conversations with the buy-side, we get the sense that EYPT's key competitor OCUL has been cherry-picking and misrepresenting EYPT's Duravyu (TKI insert for aAMD/DME) safety data.

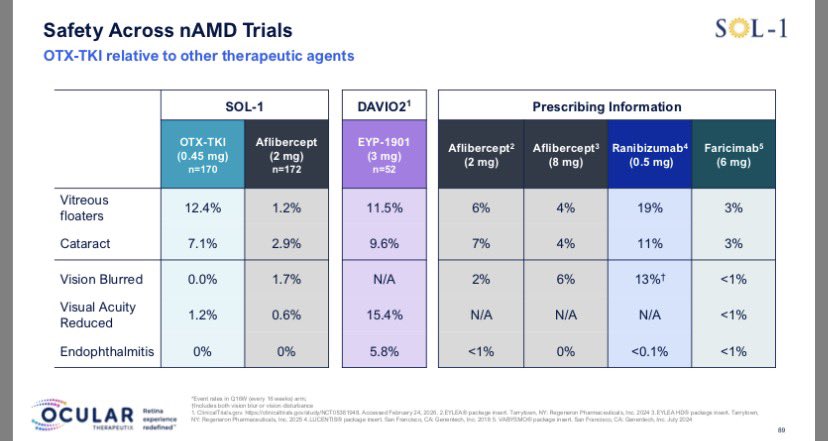

Here, we provide a detailed summary comparing the safety profiles of EYPT's Duravyu and OCUL's Axpaxli. In Exhibit 1, we list a total of 16 relevant adverse events (AEs) and the safety profile of Duravyu is highly favorable vs. that of Axpaxli. Notably, vitreous and anterior chamber opacities appear rather specific to Axpaxli, which has also shown a significantly higher rate of vitreous floaters. Importantly, there have been no cases of endophthalmitis associated with Duravyu; the three reported cases were related to Eylea injections.

We note that OCUL has misrepresented this in their handout by failing to disclose that these events were not related to Duravyu.

We further compiled data on vision loss (Exhibit 2), noting that significantly fewer patients experienced vision loss with Duravyu treatment compared to Axpaxli.

Hence, we continue to believe Duravyu's safety profile has been a key distinguishing feature, and its overall profile continues to look remarkably clean.

EYPT mgmt also reaffirmed the highly favorable safety profile of Duravyu in the ongoing Phase III LUGANO and LUCIA studies.

As of last week, 100% of LUGANO patients have received the 2nd injection (40% have received the third), and 80% of patients in LUCIA have received a 2nd injection.

Blinded safety data looks clean, with no safety events reported.

Finally, we believe EYPT's regulatory strategy is more robust, with two large non-inferiority studies versus SoC.

Given that multiple drugs are already approved for wAMD, we believe two Ph3 studies will be needed for approval. Hence, we expect EYPT to be first to market.

OCUL is currently trading at almost a 2x premium to EYPT (market cap of~$1.9Bn vs. EYPT at~$1.1Bn) and we expect this valuation gap to narrow. EYPT remains one of our Top Picks.

1

2

1,541

Mike retweeted

Mar 1

Fat JD is back yall and he’s undercover at Ali Khamenei’s street vigil in NY. Come come, don’t be shy 😆

84

310

924

48,587

Mike retweeted

Feb 28

۴۸ ساعته کلا سه ساعت نخوابیدم ولی از ذوق خبر مرگ خامنهای دارم میرقصم 😂🥂

56

421

2,129

64,800

Feb 20

$OCUL RBC KOL KOL Thinks Every Patient Wants Less Frequent Dosing, and Sees High Likelihood Axpaxli Gains

Approval from SOL-1 Alone - In a scenario where axpaxli is approved, our KOL notes he would be

an early adopter of the treatment. He is eager to see how it performs in patients, and he would

probably use it in a lot of patients.

1

492

Mike retweeted

Feb 17

Guggenheim reiterated Top Pick $EYPT Buy/$68

$OCUL $REGN RHHBY SRZN KOD FDMT

Guggenheim said in its note:

OCUL's (NC, $6.45) highly anticipated Phase III SOL-1 study (n=344) of Axpaxli (axitinib hydrogel) met its primary endpoint, demonstrating superior visual acuity versus a single aflibercept (Eylea 2 mg) injection at Week 36.

While the overperformance of the aflibercept control arm and the real-world meaningfulness of these data will likely be debated, the results clearly demonstrate that TKIs are effective in treating wet AMD, further de-risking the entire class, including EYPT's Duravyu, in our view.

We note that EYPT is conducting two identical non-inferiority trials with its TKI insert, with data anticipated starting in mid-2026.

Today's data should nonetheless give investors added confidence that TKIs are performing in line with, if not better than, SOC.

As a result, we believe the PoS for Duravyu's LUGANO and LUCIA (n =~ 400 each) studies should move higher, particularly as these studies have a far lower bar for success and greater real-world utility.

We believe EYPT's clinical strategy is more robust and differentiated, with two large non-inferiority studies versus standard of care. Given that multiple drugs are already approved for wAMD, we continue to believe that two adequately controlled studies will be needed for approval.

Hence, we expect EYPT to be first to market.

OCUL is currently trading at almost a 2x premium to EYPT (market cap of~$2Bn vs. EYPT at ~$1.1Bn). We expect this valuation gap to narrow as investors put today's readout into perspective and appreciate that the risk/reward heading into EYPT's readouts is now more attractive. EYPT remains one of our Top Picks.

Feb 5

RBC Capital reiterated $EYPT Outperform-$39 and said, We Maintain Our Conviction in the LongActing TKIs and See Recent Weakness as Buying Opportunity

$OCUL $XBI REGN RHHBY SRZN KOD FDMT RGNX - ABBV

RBC Capital said in its note:

EYPT shares are -30% YTD (vs 2% XBI), with no strong rationale for the downturn beyond investor jitters into competitor OCUL's pivotal SOL-1 readout.

We think the recent downturn is unfounded, as there has been no change to the long-thesis in our view.

We maintain conviction in EYPT and the long-acting TKI class given that:

1) the TKIs have demonstrated convincing Phase I/II data in wAMD;

2) EYPT is following the well-trodden path to approval with two non-inferiority studies which have a 78% historical success rate;

3) mgmt. sounded confident during our recent check-in;

4) corporate strategy including launching DME ahead of wAMD readouts and manufacturing registration batches for CMC, all suggest conviction; and

4) our multitude of KOL conversations are positive on the TKI class.

On SOL-1 RT, we see 40% upside to EYPT from current levels if the study meets expectations (or -10% if SOL-1 fails). Reiterate OP, Spec. Risk.

2

9

7,916