Joined May 2026

- Tweets 535

- Following 36

- Followers 27

- Likes 474

22 Photos and videos

VOO, VTI, and SCHD are all popular ETFs, but they are not doing the exact same job.

VOO gives you exposure to the S&P 500.

VTI gives you broader U.S. stock market exposure.

SCHD focuses more on dividend-paying companies.

None of them are automatically “best.”

The better question is what role you want the ETF to play in your portfolio.

*Not financial advice.

#ETFs #VOO #VTI #SCHD #investing #investingtips #WealthBuilding #stockmarket

35

Day 6 of posting one thing I used to believe about money:

I used to think “I can afford the payment” meant I could afford the thing.

That mindset gets sneaky fast.

A car payment, a phone payment, a furniture payment, a payment plan for something you probably didn’t need in the first place.

Individually, they all seem manageable.

Then one day your paycheck shows up already spoken for.

10

Jun 13

Day 5 of posting one thing I used to believe about money:

I used to think credit cards were the problem.

Like if I just avoided them completely, I’d magically be better with money.

But the card was never really the issue.

It was the “I’ll figure it out later” spending.

The random little purchases.

The pretending future me would somehow be more responsible than current me.

Credit cards can definitely make bad habits easier to hide, but they don’t create the habits out of nowhere.

It's our job to learn and grow and develop those good habits for ourselves.

12

Jun 11

Most parents think building wealth for their kids requires a huge amount of money.

It doesn’t.

The real advantage is time.

Small amounts invested early can become meaningful because compounding has decades to work.

The goal is not to be perfect.

The goal is to start the habit, choose the right account, and give the money enough time to grow.

Assumes consistent investing and a 9% average annual return. Actual returns are not guaranteed.

Not financial advice. Just education.

11

Jun 11

the to-do list is undefeated at making 47 tiny things feel equally important

6

Jun 11

nothing will humble you faster than checking the numbers after saying “it feels like things are going pretty well”

6

Jun 11

today’s reminder: the numbers are not judging you. they’re just telling on you a little.

7

Jun 11

Day 4 of posting one thing I used to believe about money:

I used to think a raise would fix my finances.

Turns out, lifestyle creep hears about your raise before your savings account does.

4

MintedTools retweeted

Jun 11

$250/week invested

40 years at 8%:

≈ $2.8M

The math is simple.

The patience is hard.

1

2

16

773

Jun 11

Today was one of those market days where everybody suddenly remembered risk exists.

Stocks got hit.

Tech got hit harder.

Semiconductors got smoked.

Oil moved higher.

Geopolitical headlines got louder.

And everyone opened their portfolio with the same facial expression they use when the check engine light comes on.

I’m not going to pretend to be a foreign policy expert on here.

There are people who understand the Iran situation much better than I do, and honestly, not every market post needs to turn into a war room thread.

But from an investor perspective, the setup today was pretty clear.

Risk assets were already stretched.

AI and tech had been carrying a lot of the market.

Inflation and rate worries were creeping back into the conversation.

Then geopolitical tension added another reason for people to sell first and think later.

That’s usually how these days go.

It’s rarely one clean reason.

It’s usually a pile-up.

Tech valuation worries.

Rate fears.

Oil concerns.

Headline risk.

Positioning.

Profit taking.

People who bought too much too fast.

People who said they wanted a dip and then got personally offended when one arrived.

Put it all together and suddenly the market has a very bad attitude.

The funny part is how quickly the tone changes.

A few green days ago, everyone was calm, long-term, patient, and “built for volatility.”

Then one ugly session shows up and suddenly half the timeline is acting like the market broke into their house.

This is why I think red days are useful.

Not fun.

Useful.

They show you what you actually own.

They show you what you only liked because it was going up.

They show you which positions suddenly feel too big.

They show you whether your cash plan was real or just something you mentioned when everything was expensive.

They show you whether you had conviction, or just momentum with a nicer name.

Because when the market is green, everyone has a plan.

When the market is red, the plan either shows up or it doesn’t.

Today was a good reminder that “buy the dip” is much easier to type than execute.

It sounds great when prices are at highs.

It sounds smart when you’re imagining a clean little 5% pullback.

It feels very different when the dip comes with oil headlines, war headlines, tech selling, and everyone refreshing charts like they’re waiting for test results.

That’s where systems matter.

Not because a system predicts the next move.

It won’t.

Not because a system makes red days feel good.

They still suck.

But a system keeps you from becoming a completely different investor every time the market gets loud.

If you’re long-term, your job is not to react to every candle like it’s a personality test.

If you’re trading, your job is to respect risk before the market forces you to.

If you’re sitting on cash, days like this are when you find out whether you actually wanted lower prices.

If you were overexposed, the market probably just sent you the note you didn’t want to read.

None of that requires panic.

It just requires honesty.

Not every selloff is the start of a crash.

Not every dip is a gift.

Not every scary headline changes the long-term thesis.

And not every bounce means the all-clear is back.

Sometimes the market is warning you.

Sometimes it is just breathing after a big run.

Sometimes everyone is simply crowded on the same side of the boat and surprised when it tips.

The point is not to know exactly which one it is in real time.

Most people don’t.

The point is to make sure one ugly day does not force you into decisions you never meant to make.

Today was ugly.

Tech was weak.

The headlines were heavy.

The mood was worse.

But days like this are also when the market gives you useful information.

What do you still want to own?

What do you want more of?

What did you only like because it was green?

What position made you uncomfortable way too quickly?

What would you buy if the price got worse?

What would make you admit your thesis changed?

Those are the questions that matter.

Because red days do not just move prices.

They expose behavior.

And honestly, that’s usually the most useful part.

8

Jun 11

most people don’t need a more complicated system. they need a simpler one they’ll actually use

6

Jun 10

the more i see businesses grow, the more i think boring follow up is secretly a superpower

6

Jun 10

“we’ll figure it out later” is how tiny problems become expensive problems

13

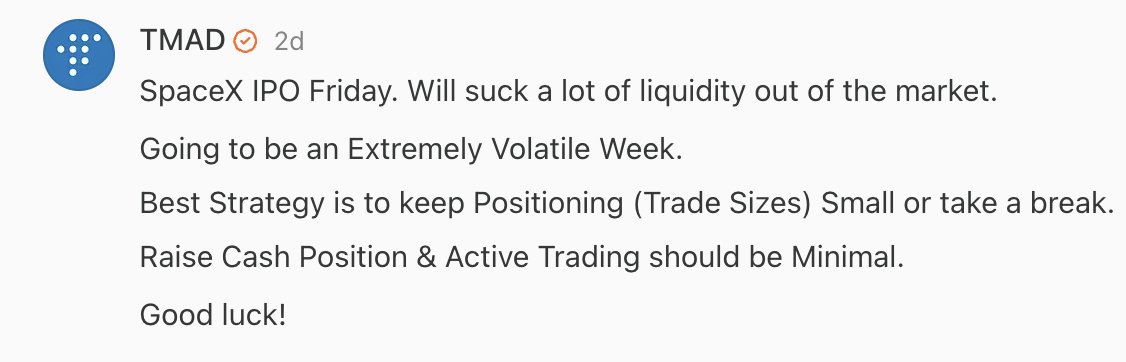

MintedTools retweeted

Jun 10

We are still in a market drawdown.

Midterm years are extremely volatile. Nothing out of the ordinary.

June is usually a crappy month also.

Trade wisely, be patient, or protect gains from the last 2 months. All that matters is not to give it all back!

12

7

79

5,580

Jun 10

Day 3 of posting one thing I used to believe about money:

I used to think investing was only worth doing once you had “real money.”

Turns out, waiting until you feel rich enough to invest is a pretty reliable way to stay behind.

7

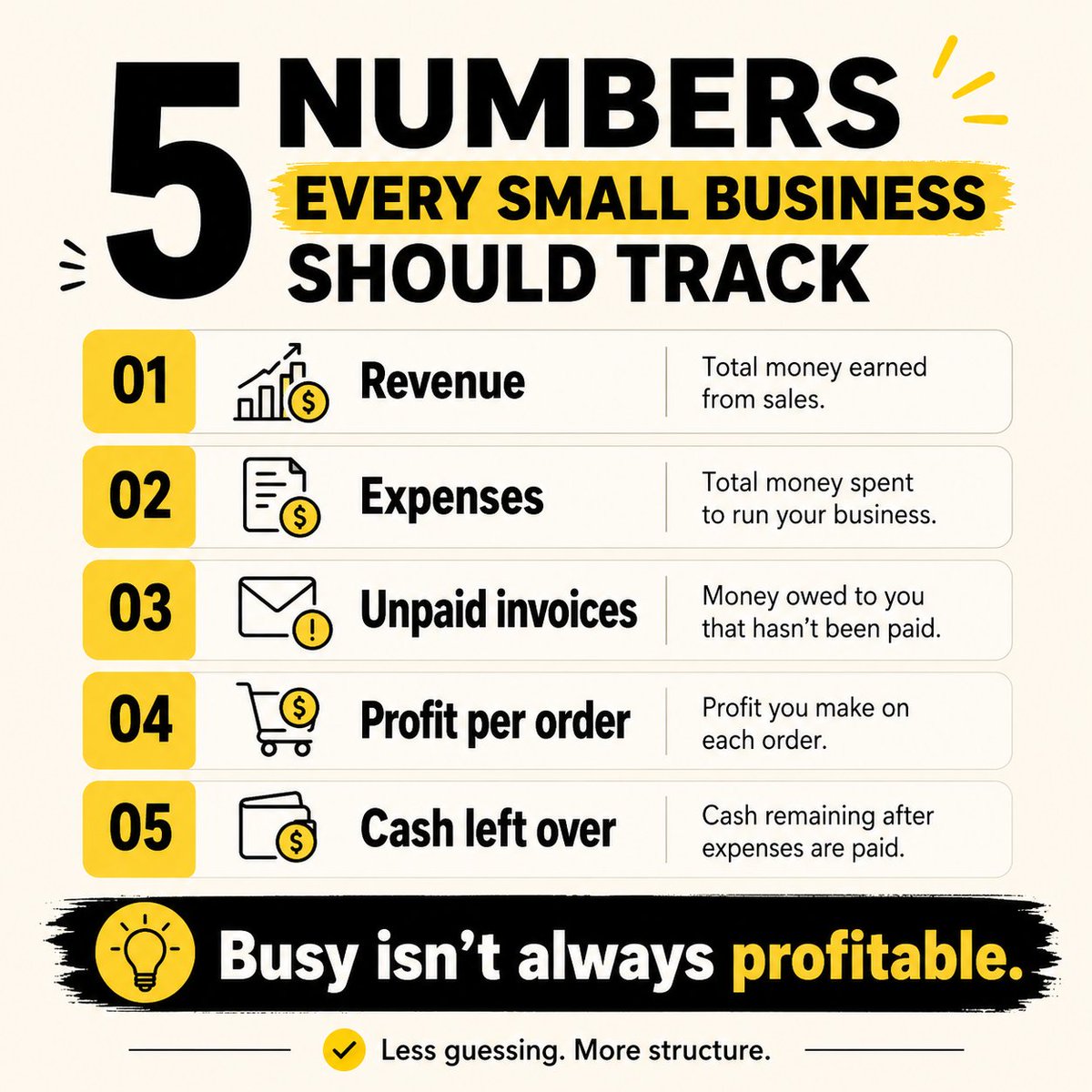

Jun 10

A lot of small business owners don’t have an idea problem.

They have a feedback problem.

They’re doing a lot.

Posting.

Selling.

Testing.

Updating.

Tweaking.

Trying new things.

But if the numbers are scattered or ignored, it becomes hard to know what actually worked.

That’s when everything starts to feel personal.

No sales means the product is bad.

Low views means nobody cares.

No clicks means the whole thing failed.

But maybe not.

Maybe the photo is weak.

Maybe the title is unclear.

Maybe the price is confusing.

Maybe the right people haven’t seen it yet.

Maybe the traffic source is wrong.

Maybe the offer is fine, but the expenses are eating the profit.

You can’t fix the right problem until you know which problem you actually have.

That’s where tracking helps.

Not because numbers magically solve everything.

They don’t.

But they make the next decision clearer.

And sometimes that’s all you need.

A little less guessing.

A little more structure.

6

Jun 10

Most parents want to give their kids a head start.

But a head start does not have to mean handing them a huge amount of money.

It can start with understanding the accounts available, choosing the right one for the goal, and building the habit early.

A 529 can help with education.

A custodial account can help build long-term assets.

A Roth IRA can be powerful later if your child has earned income.

The biggest advantage is not starting with a lot.

It is starting with time.

Not financial advice. Just education.

5

Jun 10

the best business advice is usually annoyingly simple and then weirdly hard to actually follow

7

Jun 10

portfolio down a little: healthy pullback

portfolio down more: long term opportunity

portfolio down a lot: suddenly very interested in homesteading

1

5