SME investing minus the circus. IPOs, OFS & business models. Market survivor. Not SEBI registered—just trying to be less wrong than yesterday.

Joined November 2013

- Tweets 728

- Following 5

- Followers 178

- Likes 878

33 Photos and videos

Why stop losses are often impossible in SME stocks:

Take Cosmic CRF as an example.

• IPO received a weak response and was extended due to insufficient subscription.

• Listed below expectations.

• Corrected nearly 40% within the first month.

• Most conventional stop losses would have been triggered.

Then came business execution, improving numbers, and positive news flow.

The stock moved well above its IPO price, while many investors who entered later paid much higher prices than those who got IPO allotment.

But the story doesn't end there.

Many promising-looking SME stocks have also fallen 40%, never recovered, and still trade 70% below their peaks.

That's why SME investing is difficult.

A 30-40% correction doesn't automatically mean the business is broken. But neither does every correction become a multibagger opportunity.

The real challenge is distinguishing temporary market pessimism from permanent business deterioration.

SME investing is less about reacting to price moves and more about understanding management quality, business model, capital allocation, and execution.

Disclosure: Holding a few IPO-allotted lots of Cosmic CRF. This is not a recommendation to buy, sell, or hold any security. Cosmic CRF is mentioned purely as an example of SME market behavior.

72

Jun 13

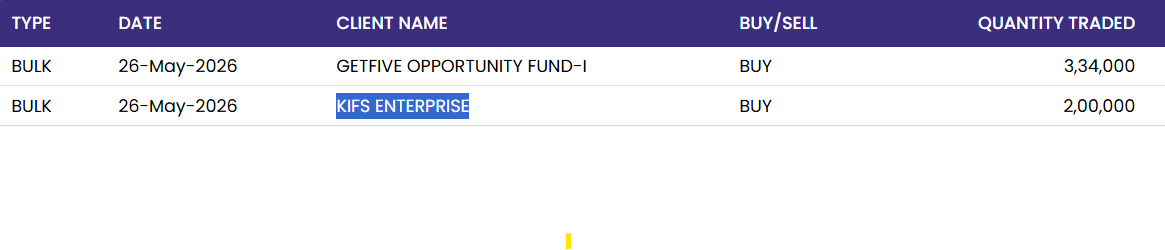

SJ Logistics

Promoter: 50.81%

DII FII: 1.25%

Retail: ~48%

P/E: ~7

K2 Infragen

Promoter: 40.70%

DII FII: ~1%

Retail: ~58%

P/E: ~4.77

Two different companies.

Two different sectors.

Yet both highlight the same SME lesson.

People ask why some SME stocks trade at valuations that traditional metrics struggle to justify.

Sometimes the answer isn't in the P&L.

It's in the shareholding pattern.

When ownership is fragmented, valuation can remain disconnected from what spreadsheets say it should be.

Numbers can prove value.

Promoters often unlock it.

Once a stock is fully distributed, retail investors, HNIs and even AIFs have limited ability to drive a rerating on their own.

The key question isn't just:

"Is the business growing?"

It's:

"What incentive does the promoter have to take the stock toward fair value?"

A cheap stock can get cheaper.

An expensive stock can stay expensive.

Ownership structure matters.

Disclaimer: The above is a general observation on SME market dynamics and shareholding patterns. It is not a recommendation to buy, sell or hold SJ Logistics, K2 Infragen, or any other security. Do your own research.

1

253

Jun 13

NLC India launches an OFS.

3 days later:

✅ 660 MW Ghatampur Unit-3 starts commercial operations, taking capacity to 8,405 MW.

✅ Wins a critical mineral block in Telangana.

✅ Signs MoU with CSIR-CECRI for rare earth & critical mineral extraction technologies.

Maybe the market was busy calculating OFS discounts while the company was busy building the future.

As always, corporate actions create noise. Business execution creates value.

1

147

MIT Engineers retweeted

Jun 8

Susan Electricals ipo- is coming at ~14x FY26 earnings.

Prime Cable trades at ~14.7x and J D Cables at ~14x, despite J D enjoying superior PAT margins.

Positives:

• FY26 revenue nearly doubled

• 47% RoNW

• Revenue mix between Government and non-Government clients appears encouraging

• Backed by pre-IPO investors Gracious Advisors LLP and CCV Emerging Opportunities Fund-I

• IPO proceeds largely earmarked for expansion and working capital

Questions investors should ask:

• PAT margin expanded sharply in the IPO year and deserves closer scrutiny

• New facility's trial run and commercial production are expected to contribute meaningfully only after about a yearAnd one more thing...

The same Merchant Banker's previous issue, Rajnandini Fashion, turned into a post-listing disaster. This issue also carries an unusual 8.26% Market Maker reservation.

Valuation looks reasonable.

The key debate is whether FY26 earnings are the beginning of a new growth phase—or simply the best year before the IPO.

2

2

2,559

MIT Engineers retweeted

Jun 9

Horizon Reclaim (India) IPO

Horizon is coming at roughly ₹200 Cr market capitalization on FY26 numbers.

FY26 revenue is about ₹50 Cr, implying a 4x sales multiple.

IPO valuation is around 19.14x earnings.

Listed peer Lead Reclaim & Rubber Products trades near 16.6x P/E.

The Key Question

At first glance, Horizon appears superior:

PAT Margin FY26: ~20%

Lead Reclaim PAT Margin: ~10%

However, investors should focus on earnings quality and sustainability.

In FY24, Horizon's PAT margin was below 5%.

Within two years, margins expanded dramatically to 20% .Cost of Materials Consumed fell from 78.46% of revenue (FY24) to 57.09% (FY26), that's a massive 21 percentage point improvement?????

For a manufacturing/recycling company, such a change is extraordinary.

Similar sharp profit jumps have been seen in several recent SME IPOs just before listing.

1

3

524

Jun 10

Forget the temporary OFS noise and price dips. The long-term structural story for NLCINDIA is intact. 🚀3 major triggers driving value over the coming years:1️⃣ Value Unlocking: Upcoming NLC Renewables IPO to unlock massive clean energy asset valuation.2️⃣ Massive Expansion: ₹1.25 Lakh Cr CapEx to triple capacity to 20 GW by 2030.3️⃣ Margin Protection: New captive coal blocks mean near-zero fuel transit a ~12x P/E, this Navratna remains an undervalued structural transition play. 💎Disclaimer: For educational purposes only. Not financial advice or a SEBI-registered recommendation. Invest at your own risk.

1

6

940

Jun 12

"NLCIL declared as Preferred Bidder for Critical & Strategic Mineral Block Auctions conducted by Ministry of Mines, GoI”NLC India Limited, is declared as Preferred Bidder for Parvathapur Vanadium, Titanium & Aluminous Laterite block of Sanga Reddy, Telangana subsequent to the Critical & Strategic mineral blocks E-auction held on 11.06.2026 by Ministry of Mines, GoI.

122

Jun 12

EPW India: another positive development after a strong FY26.

✔️ FY26 PAT jumped to ~₹10 Cr from ~₹4 Cr in FY25.

✔️ Strong improvement in margins and bottom line.

✔️ Subsidiary has now received Hazardous Waste Authorization from the Telangana Pollution Control Board for collection, storage, transportation, processing and disposal of specified waste streams.

This approval enables full-scale operations and strengthens EPW's position in the recycling and circular economy space.

Interesting timing as a rubber recycling IPO is also opening today. The entire recycling theme is attracting increasing investor attention, and sector re-rating effects can sometimes spill over across listed players.

Disclosure: Holding EPW India since listing day This is not a buy/sell recommendation. Please do your own research.

#EPWIndia #SMEStocks #Recycling #CircularEconomy

92

Jun 12

Delta Autocorp IPO launched at ₹130, by GYR Capital & backed by big anchors: HDFC Bank, Bharat Venture, Vikasa India, Saint Capital, Veloce AIF, Shine Star & Knightstone.

1 year later? Trading at just ₹38. 📉

Proof that prestigious anchor lists & merchant bankers are just marketing window dressing. If the business model is weak and promoter intent is flawed, your wealth gets eroded by 70%. Stop buying the social media buzz and look at the core fundamentals. 🧵

157

Jun 11

NLC India OFS: A Case Study in Market Psychology

Day 1 (For Non- Retail)

Floor price: ₹303

Market price: ~₹326

Many investors sold shares expecting OFS allotment near ₹310 range. Nearly 2.5 crore shares traded at an average price of ~₹326.33. for price arbritage

Then came the surprise.

The discovered OFS price wasn't near ₹310 but It was ₹323.10.

This suggests bidding remained aggressive, likely from a mix of HNIs, arbitrage funds and institutions seeking meaningful allocation. After successful OFS transactions in Coal India and NHPC, many smaller HNIs also appeared attracted by the perceived arbitrage opportunity.

An important difference was that NLC India is not in the F&O segment, limiting hedging options available to participants. This may have increased risk for investors pursuing short-term OFS arbitrage strategies.

Day 2 (For Retail)

The stock declined from around ₹326 to nearly ₹308. Panic spread among short-term and leveraged participants. More than 3 crore shares traded during the decline.

The interesting question is:

If weaker hands were exiting, who was absorbing such large volumes?

One possible interpretation is that stronger hands used the correction to accumulate shares while retail participation faded as the market price moved below expectations formed around the OFS process.

A possible by-product of this price action was that retail investors became less interested in bidding, as the market price moved below the effective retail economics of the OFS. Reduced retail participation, if it occurred, could potentially leave a larger portion of available shares to be allocated among non-retail categories under the OFS framework.

Markets often move not where the crowd expects, but where they create the maximum discomfort for the maximum number of participants.

Disclaimer: This post is a personal interpretation of publicly available price, volume and OFS data. It contains opinions, hypotheses and market observations only. References to "stronger hands" and "weaker hands" are market expressions and do not imply coordinated action by any participant. This is not an allegation of manipulation, collusion, insider trading or wrongdoing by any individual, institution, intermediary or regulator. Investors should conduct their own due diligence before making investment decisions.

For graphical understanding. #NLCINDIA OFS

1

395

Jun 11

Wipro buyback maths is not as attractive as many assume.

Suppose you hold 900 shares bought at ₹202.

Even If acceptance ratio is 40%:

✅ 360 shares accepted at ₹250

Profit = ₹17,280

But if the remaining 540 shares trade at ₹180 post-buyback:

❌ Loss = ₹11,880

Net gain = just ₹5,400.

And that's before taxes, opportunity cost, and the risk of a lower acceptance ratio.

Many investors focus only on the buyback premium and ignore the price risk on unaccepted shares.

Buyback arbitrage without proper hedging is not free money. Sometimes the entire expected profit can disappear with a small fall in the stock price.

Disclaimer: This is a simplified illustration using hypothetical acceptance ratios and post-buyback prices. Actual returns may vary significantly depending on acceptance ratio, market price movement, taxes, and transaction costs. Not investment advice.

1

706

Jun 10

NLC India OFS — A Case Study-Rarely do you see an OFS where retail investors have almost no incentive to apply.

In NLC India OFS, many retail applicants may still be bidding at cut off assuming allotment at the original floor price of ₹303. But after strong NII participation, the effective cut-off has moved to ₹323.10 — while the market price is trading below that.

When the market offers cheaper shares than the OFS itself, something has clearly gone wrong in the price discovery process.

Selling members ICICI Securities and DAM Capital Advisors should introspect on how this fiasco unfolded.

1

1

2

1,090

Jun 10

Team Tech 👀

Circuit filter expands from 5% to 20% from today.

Interesting timing: the company issued an order-win notification on the eve of the change. Markets love a good coincidence.

Freshara Agro continues to trade in the ₹197–₹230 range. A breakout with strong volumes is now the key level to watch.

Meanwhile, NLC OFS opens for retail today at a cut-off price of ₹323.10.

Disclosure: Personal holding. Not SEBI registered. Not a recommendation.

225

Jun 9

NLC ofs cut off as per bse and nse data is 323.10 .applied at 323.70 in NII

2

1

988